Customer Experience Management (CEM) Market Research Report – Segmentation by Component (Solutions , Services); By Touchpoint Type (Call Centers, Websites & Web Portals, Mobile Applications, Social Media Platforms, Email Interactions, In-Store/Branch Interactions, AI-Powered Chatbots & Virtual Assistants, Messaging Apps (e.g., WhatsApp, SMS)); By Deployment Model (Cloud-Based, On-Premises); By End-User Industry (Retail & eCommerce, Banking, Financial Services, and Insurance (BFSI), IT & Telecommunication, Healthcare & Life Sciences, Hospitality & Travel, Government & Public Sector, Manufacturing, Media & Entertainment, Automotive, Others (e.g., Utilities, Education)); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-2214

Format:

Region: Global

Market Size and Overview:

The Customer Experience Management (CEM) market was valued at USD 19.34 Billion in 2024 and is projected to reach a market size of USD 42.95 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 17.3%.

The global Customer Experience Management (CEM) market has unequivocally transitioned from a peripheral business consideration to a central pillar of corporate strategy and competitive differentiation in the contemporary digital economy. As of 2024, the market demonstrated robust vitality, reflecting an escalating understanding among enterprises worldwide that the holistic perception a customer holds about a brand, shaped by every interaction across their journey, is paramount to sustainable growth, loyalty, and advocacy.

Key Market Insights:

Industry analyses from 2024 revealed that over 75% of organizations identified CX as a primary competitive differentiator, a notable increase from previous years.

Data from early 2024 indicated that companies investing significantly in omnichannel CEM strategies reported a 25% higher customer retention rate compared to those with siloed channel approaches.

Furthermore, AI adoption within CX operations saw a substantial surge, with around 60% of enterprises in 2024 actively deploying or planning to deploy AI-powered tools for personalization and customer support.

The demand for real-time customer analytics solutions grew by an estimated 30% in 2024, as businesses sought immediate insights into customer behaviour.

Statistics showed that personalized email campaigns, a core CEM tactic, generated up to 18 times more revenue in 2024 than broadcast emails.

Market Drivers:

Escalating Customer Expectations for Personalized and Omnichannel Experiences

A primary engine propelling the Customer Experience Management market is the dramatic and continuous escalation of customer expectations. In the current hyper-connected, information-rich environment, consumers and B2B clients alike demand more than just quality products or services; they seek seamless, intuitive, and highly personalized interactions across every touchpoint and throughout their entire lifecycle with a brand. This expectation is no longer a preference but a baseline requirement. Customers anticipate that businesses will understand their individual needs, preferences, and history, and use this knowledge to deliver relevant content, tailored offers, and proactive support, irrespective of whether they are interacting via a mobile app, website, social media, call center, or in a physical store. This demand for cohesive omnichannel experiences, where transitions between channels are fluid and context is maintained, compels organizations to invest heavily in sophisticated CEM platforms.

The Proliferation of Customer Data and Advancements in AI/ML Technologies

The exponential growth in the volume, velocity, and variety of customer data generated across digital and physical touchpoints serves as another critical driver for the CEM market. Every click, purchase, interaction, and feedback provide a wealth of information that, if harnessed effectively, can unlock profound insights into customer behaviour, sentiment, and intent. Concurrently, significant advancements in Artificial Intelligence (AI), Machine Learning (ML), and Big Data analytics have provided organizations with the powerful tools necessary to collect, process, analyse, and act upon this data at scale. These technologies enable businesses to move beyond basic segmentation to achieve hyper-personalization, predict future customer needs and actions (like churn or purchase propensity), automate customer service interactions intelligently through chatbots and virtual assistants, optimize marketing campaigns in real-time, and uncover hidden patterns that can inform strategic CX improvements.

Market Restraints and Challenges:

The CEM market, despite its robust growth, faces challenges such as increasing concerns around data privacy and stringent regulatory compliance (like GDPR and CCPA), which demand meticulous data governance. Integrating complex CEM solutions with legacy IT systems often proves difficult and costly, while the persistent shortage of skilled professionals capable of managing and interpreting sophisticated CX data and tools also acts as a restraint for some organizations.

Market Opportunities:

Significant opportunities lie in the further development and adoption of predictive and prescriptive analytics to enable proactive customer engagement and problem resolution before issues arise. The expansion of Internet of Things (IoT) devices creates new data streams and touchpoints for innovative CX strategies. Moreover, there is considerable untapped market potential in tailoring CEM solutions for specific industry verticals and for small and medium-sized enterprises (SMEs) in emerging economies that are rapidly digitizing.

Market Segmentation:

Segmentation by Component:

• Solutions

Customer Relationship Management (CRM) Software

Customer Analytics Platforms (including Voice of Customer, Sentiment Analysis)

Personalization Engines

Customer Feedback Management Tools

Omnichannel Communication Platforms

Customer Journey Orchestration Tools

• Services

o Professional Services

Strategic Consulting & Advisory

Implementation & Integration Services

Training & Support Services

o Managed Services

Outsourced CX Operations

Platform Management & Optimization

Software solutions form the foundational technological backbone of any CEM strategy, providing the essential tools for data collection, analysis, engagement, and personalization. Organizations initially invest in these platforms to build their CX capabilities, making the solutions segment the largest in terms of market share as of 2024.

As CEM strategies mature and technologies become more complex, the demand for specialized expertise is surging. Services, particularly those involving AI-driven analytics, advanced consulting for journey optimization, and managed services for outsourcing CX operations, are witnessing the fastest growth, enabling companies to maximize ROI and stay ahead of the curve.

Segmentation by Touchpoint Type:

• Call Centers (Voice, IVR)

• Websites & Web Portals (including e-commerce)

• Mobile Applications

• Social Media Platforms

• Email Interactions

• In-Store/Branch Interactions (Physical)

• AI-Powered Chatbots & Virtual Assistants

• Messaging Apps (e.g., WhatsApp, SMS)

Historically, call centers and corporate websites have been primary channels for customer interaction and service, handling a high volume of inquiries and transactions. In 2024, while digital channels are surging, these established touchpoints still represent a dominant portion of overall customer engagement, particularly for complex issue resolution and information seeking.

The ubiquity of smartphones makes mobile apps a critical and rapidly expanding touchpoint for personalized engagement and service. Concurrently, AI-powered chatbots and virtual assistants are experiencing explosive growth, driven by their ability to provide instant, 24/7 support and handle a large volume of routine interactions efficiently across various digital platforms.

Segmentation by Deployment Model:

• Cloud-Based (SaaS, PaaS)

• On-Premises

While the shift to cloud is undeniable and rapid, in 2024, a significant portion of established enterprises, particularly in highly regulated industries like finance and healthcare, still relied on on-premises CEM solutions. This dominance is often attributed to long-standing investments, perceived data control, and specific security or compliance requirements, though this is rapidly changing.

The cloud-based deployment model is unequivocally the fastest-growing segment. Its inherent advantages, such as lower upfront costs, scalability, flexibility, ease of integration with other cloud services, automatic updates, and accessibility for remote teams, make it highly attractive for businesses of all sizes seeking agility and innovation in their CEM strategies.

Segmentation by End-User Industry:

• Retail & eCommerce

• Banking, Financial Services, and Insurance (BFSI)

• IT & Telecommunication

• Healthcare & Life Sciences

• Hospitality & Travel

• Government & Public Sector

• Manufacturing

• Media & Entertainment

• Automotive

• Others (e.g., Utilities, Education)

The BFSI sector, with its high volume of customer interactions, intense competition, and stringent regulatory environment, has been a leading adopter of CEM solutions. The critical need for trust, personalization in financial advice, and seamless digital banking experiences made BFSI a dominant segment in 2024.

The Retail & eCommerce sector is experiencing rapid growth in CEM adoption, driven by the imperative to offer personalized shopping experiences and manage complex omnichannel journeys. Simultaneously, the Healthcare sector is increasingly focusing on patient experience, leveraging CEM for better communication, personalized care plans, and streamlined service delivery, making it another fast-growing vertical.

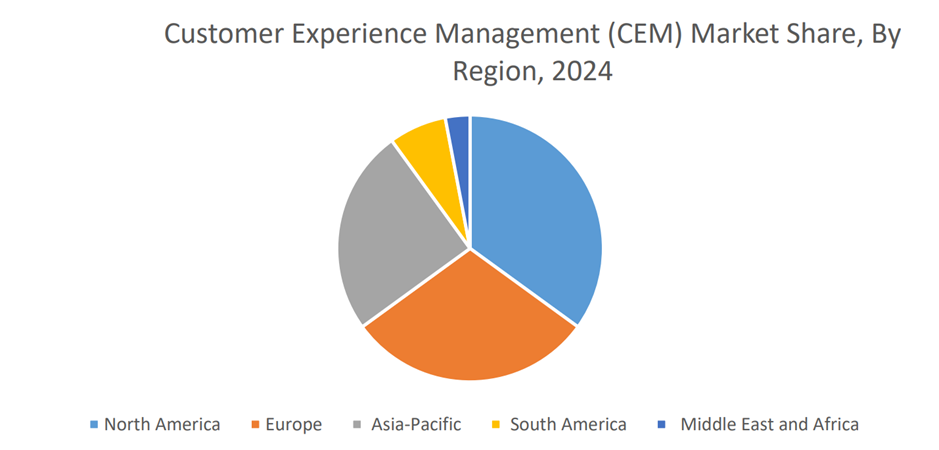

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• Latin America

• Middle East & Africa

North America's dominance is attributed to its advanced technological infrastructure, high concentration of leading CEM solution providers, significant investments by enterprises in customer-centric initiatives, and a mature market with highly discerning customers who demand exceptional service and personalized interactions across all channels.

The Asia-Pacific region is the most rapidly expanding market for CEM. This growth is fueled by widespread digital transformation across industries, a massive and increasingly affluent consumer base adopting digital channels, governmental pushes for smart city initiatives, and businesses recognizing CX as a key differentiator in highly competitive local markets.

COVID-19 Impact Analysis:

The COVID-19 pandemic acted as a significant accelerator for the CEM market. It forced an abrupt shift towards digital channels for almost all businesses, dramatically increasing the volume of online interactions. This highlighted the urgent need for robust digital CX capabilities, personalized communication, empathetic customer support, and seamless omnichannel experiences, thereby compelling organizations to rapidly adopt or upgrade their CEM solutions to meet evolving customer behaviors and ensure business continuity.

Latest Trends and Developments:

Key trends in 2024 include the sophisticated integration of Generative AI for creating highly personalized content and conversational experiences, a surge in proactive and predictive customer service models, and an intensified focus on ethical AI and data privacy in CX. Furthermore, the convergence of Employee Experience (EX) and Customer Experience (CX) is gaining traction, recognizing that empowered and engaged employees are crucial for delivering superior customer outcomes.

Key Players in the Market:

• Adobe

• IBM

• Oracle

• Avaya

• Nice

• Nokia

• SAP

• OpenText

• Tech Mahindra

• Verint Systems

Chapter 1. Global Customer Experience Management (CEM) Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Customer Experience Management (CEM) Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Customer Experience Management (CEM) Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Customer Experience Management (CEM) Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Customer Experience Management (CEM) Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Customer Experience Management (CEM) Market – By Component

6.1. Introduction/Key Findings

6.2. Solutions

6.3. Services

6.4. Y-O-Y Growth trend Analysis By Component

6.5. Absolute $ Opportunity Analysis By Component, 2024-2030

Chapter 7. Global Customer Experience Management (CEM) Market – By Touchpoint Type

7.1. Introduction/Key Findings

7.2. Call Centers

7.3. Websites & Web Portals

7.4. Mobile Applications

7.5. Social Media Platforms

7.6. Email Interactions

7.7. In-Store/Branch Interactions

7.8. AI-Powered Chatbots & Virtual Assistants

7.9. Messaging Apps (e.g., WhatsApp, SMS)

7.10. Y-O-Y Growth trend Analysis By Touchpoint Type

7.11. Absolute $ Opportunity Analysis By Touchpoint Type, 2024-2030

Chapter 8. Global Customer Experience Management (CEM) Market – By Deployment Model

8.1. Introduction/Key Findings

8.2. Cloud-Based

8.3. On-Premises

8.4. Y-O-Y Growth trend Analysis By Deployment Model

8.5. Absolute $ Opportunity Analysis By Deployment Model, 2024-2030

Chapter 9. Global Customer Experience Management (CEM) Market – By End-User Industry

9.1. Introduction/Key Findings

9.2. Retail & eCommerce

9.3. Banking, Financial Services, and Insurance (BFSI)

9.4. IT & Telecommunication

9.5. Healthcare & Life Sciences

9.6. Hospitality & Travel

9.7. Government & Public Sector

9.8. Manufacturing

9.9. Media & Entertainment

9.10. Automotive

9.11. Others (e.g., Utilities, Education)

9.12. Y-O-Y Growth trend Analysis By End-User Industry

9.13. Absolute $ Opportunity Analysis By End-User Industry, 2024-2030

Chapter 10. Global Customer Experience Management (CEM) Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Touchpoint Type

10.1.4. By Deployment Model

10.1.5. By End-User Industry

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Touchpoint Type

10.2.4. By Deployment Model

10.2.5. By End-User Industry

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Touchpoint Type

10.3.4. By Deployment Model

10.3.5. By End-User Industry

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Touchpoint Type

10.4.4. By Deployment Model

10.4.5. By End-User Industry

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Touchpoint Type

10.5.4. By Deployment Model

10.5.5. By End-User Industry

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Customer Experience Management (CEM) Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Adobe

11.2. IBM

11.3. Oracle

11.4. Avaya

11.5. Nice

11.6. Nokia

11.7. SAP

11.8. OpenText

11.9. Tech Mahindra

11.10. Verint Systems

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

As organizations across industries accelerate their shift to digital-first models, they require comprehensive CEM platforms to orchestrate seamless, personalized experiences across web, mobile, contact center, and in-person channels. The need to unify disparate customer touchpoints and deliver consistent journeys has become mission-critical in a world where convenience and speed directly impact loyalty.

Bringing together customer data from CRM systems, marketing platforms, contact centers, social feeds, and IoT devices remains a significant technical hurdle. Many organizations struggle to build a single, accurate customer profile, leading to fragmented insights and inconsistent experiences.

Adobe, IBM, Oracle, Avaya, Nice, and Nokia are the leading players in Customer Experience Management Market.

North America currently holds the largest market share, estimated at around 35%.

Asia-Pacific has shown significant room for growth in specific segments.