Global Wireless Infrastructure Market Research Report – Segmentation By Type (Macrocell RAN, Small Cells, Distributed Antenna System, Cloud RAN, Carrier Wi-Fi, Mobile Core, Backhaul), By Technology (2 G/3 G, 4 G/LTE, 5 G), By End-Use (Telecom Operators, Enterprises, Public Safety, Others), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16488

Format:

Region: Global

Market Size and Overview:

The Global Wireless Infrastructure Market was valued at USD 241.5 billion and is projected to reach a market size of USD 401.47 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 10.7%.

Persistent 5G deployments, density of tiny cell networks, and the need for high-speed, low-latency connections to enable growing mobile broadband, IoT applications, and corporate private networks propel this expansion. Modernizing legacy RAN architectures, moving toward cloud-native and open-RAN models, service providers are enhancing backhaul and mobile-core domains to manage the enormous data traffic rise while lowering operating costs.

Key Market Insights:

Mid-2025 will see over 60% of worldwide mobile subscriptions on 5G networks, expected to account for roughly 40% of wireless infrastructure CAPEX by 2030 as operators update macro and small-cell sites to enable multi-gigabit services.

Driven by urban densification and indoor coverage requirements, the small-cell sector is predicted to expand at roughly 8% CAGR, capturing more than 25% of unit deployments by 2030 as operators overlay networks for capacity and coverage.

Investments in edge-computing infrastructure coupled with base-station sites are rising at around a 7% CAGR, hence enabling offloading of data from core clouds and ultra-low-latency applications.

15% of wireless infrastructure revenue by 2030 will come from private LTE/5G networks in production, logistics, and campus settings as businesses look for committed, safe connections.

Wireless Infrastructure Market Drivers:

The exceptional growth seen in the mobile data traffic is driving the need for this market.

While emerging use cases, including cloud gaming, AR/VR, and telemedicine, require ultra-high bandwidth and constant throughput, video streaming alone makes up close to 70% of this traffic. To avoid congestion and keep QoS, operators are under an ongoing need to raise base-station capacity, backhaul connections, and spectrum holdings. To offload hotspots, multi-gigabit small cells, high-capacity microwave and fiber backhaul, and smart traffic-steering solutions must be used. This unending traffic increase calls for it. Networks run the risk of reduced user experiences and churn if they do not get ongoing infrastructure improvements as data-hungry customers and companies look for more dependable connections.

The rapid transition towards 5 G New Radio (NR) is also considered a major market growth driver.

With more than 200 commercial networks launched by 2024 and covering 1.5 billion people, 5G NR deployments have swiftly advanced from trial phases to full-scale deployments. 5G's promise of multi-gigabit peak speeds, sub-millisecond latency, and massive IoT connectivity is motivating operators to refarm already available mid-band spectrum and obtain new mmWave licenses. Network designers are including massive-MIMO antennae, dynamic spectrum-sharing solutions, and carrier aggregation into macrocell and microcell sites to release the full potential of 5 G. Apart from improving consumer broadband and corporate private-network capabilities, this change opens fresh vertical uses requiring deterministic performance: industrial automation, autonomous cars, and smart cities. With 5G accounting for most of network-capex expenditures, capital expenditures for RAN equipment are therefore projected to rise at a 5% CAGR across 2030.

The growing densification of networks and small-cell proliferation are also driving the demand for this market.

To match 5G's high-frequency bands and increase capacity in dense urban settings, operators are aggressively densifying networks with small cells and Distributed Antenna Systems (DAS). In 2024, worldwide small-cell deployments surpassed 1 million units, up from 600,000 in 2021. Small cells, ranging from picocells to compact outdoor units, provide targeted coverage and offload traffic from overloaded macrocells, improving spectral efficiency and user throughput. In-building DAS installations and public-venue small cells address indoor capacity challenges, particularly in stadiums, malls, and transportation hubs. Self-organizing network (SON) features and fiberized backhaul are also used in the densification approach to speed out deployments. Small-cell density is expected to increase fivefold by 2030 as cities grow and data requirements intensify, radically changing network topologies.

The emergence of virtualization and architecture for cloud native RAN is said to be an important market driver.

Network Function Virtualization (NFV) and Cloud-Native RAN (vRAN) designs are revolutionizing the way telecom providers install and administer their infrastructure. By splitting baseband units into software executing on general-purpose servers, vRAN facilitates centralized or regionalized baseband pooling, dynamic resource allocation, and flawless software upgrades. Leading operators have introduced vRAN clusters in major markets; Verizon and Rakuten have achieved 20% reductions in energy consumption and 30% quicker feature rollouts. Virtualization and open-RAN standards (O-RAN) are expected to take up 40% of new-RAN deployments by 2030, driving a basic shift from hardware-centric to software-driven networks as telcos aim for operational agility and lower TCO.

Wireless Infrastructure Market Restraints and Challenges:

The existence of high costs related to its deployment is a major challenge, as it discourages businesses from adopting it.

Based on tower height and backhaul complexity, industry research estimates USD 150,000–500,000 per site for macrocells alone, comprising tower reinforcement, new radios, and fiber backhaul. Costing USD 10,000–50,000 apiece, including site prep, electricity improvements, and installation, small cells are vital for urban coverage. Operators need to invest in edge-compute nodes beyond hardware to enable ultra-low-latency applications, thereby increasing capital expenditures. Particularly in under-penetrated markets, these cumulative costs stress budgets, driving many operators to investigate network-sharing alliances, vendor financing, and infrastructure-as-a-service ideas to reduce initial costs.

The availability of spectrum and its cost are also hindering the growth of the market.

Gaining mid-band and mmWave operating rights calls for multi-billion-dollar auction bids and continuing licensing fees. With individual operators spending €7–€12 billion each for national coverage auctions, European 3.6 GHz auctions raised almost €100 billion. C-band spectrum licenses cost carriers up to USD 80 billion in the U. S., thereby compelling AT&T and Verizon to direct significant capital toward spectrum rather than just network build-outs. Fragmented holdings across areas complicate harmonized network planning and roaming agreements as carriers haggle over sharing arrangements to cover geographical gaps. High spectrum costs, hence, increase the entry hurdle and lengthen payback periods for new technology installations.

The market faces hurdles when it comes to the acquisition of the site and zoning.

Small cells and new macro sites' attempts to densify networks usually fail due to zoning rules and local opposition. Approvals for small-cell installations can take 6–9 months in important U. S. cities like Los Angeles, hence impeding fast roll-out strategies. As cities monetize public infrastructure, local governments may levy exorbitant attachment costs—Boston charges USD 2,500 per pole; New York USD 4,500 yearly. On average, community "not-in-my-backyard" (NIMBY) objections over aesthetic and health concerns further delay deployments by 6–12 months, thereby driving operators to conduct thorough stakeholder outreach, design camouflage techniques, and negotiate local incentive programs to simplify site acquisition.

The issues related to interoperability and its security are major market challenges.

Open RAN provides cost reductions and vendor diversity, yet presents security and integration issues. Multi-vendor radio and software stacks need thorough interoperability testing because poor configurations can cause performance loss or security issues. The Telecom Infra Project observes that matching different RAN elements across 3–5 suppliers could increase integration timelines by 20–25% and calls for integrated orchestration systems to control policy execution and software upgrades. Furthermore, a broken ecosystem widens the attack surface, therefore necessitating strengthened security systems, such as end-to-end encryption, secure boot, and continuous integrity checks, to protect against supply-chain risks and zero-day attacks, therefore adding operational overhead and specialized staffing needs.

Wireless Infrastructure Market Opportunities:

The emergence of private 5 G networks is seen as a major market growth opportunity.

Offering committed, secure, and high-performance connections for mission-critical IoT applications, private cellular networks are changing industrial connectivity. With a CAGR of 54. 1%, the global private 5G network market was estimated at USD 2 00 billion and is expected to grow to USD 36 billion. 08 billion by 2030 as manufacturing, logistics, healthcare, and utilities adopt on-premises RAN, core, and edge solutions suited to demanding enterprise SLAs. This path means a least USD 5 billion additional potential by 2030 in specialized hardware, software, and professional-service categories alone. Leading operators and system integrators are working with chipset and equipment manufacturers to provide end-to-end private-LTE/5G solutions, including spectrum licensing, network design, and managed services, therefore speeding time-to-value and guaranteeing predictable network performance for Industry 4.0 implementations.

The growing popularity of Multi-Access Edge Computing (MEC) is said to be a great market opportunity.

By extending cloud-like compute and storage to base-station sites, MEC enables ultra-low-latency services including AR/VR cooperation, autonomous-vehicle telemetry, and real-time industrial analytics. Worth USD 3.39 billion, the worldwide MEC market is expected to grow at a 49. 1% CAGR through 2030, finishing at about USD 20 billion by the end of the decade. Operators incorporating edge servers next to micro cells and macro sites drive this expansion, providing developers flawless APIs for containerized microservices and AI inference workloads. As 5G rollouts pick up speed, MEC will become necessary for organizing mission-critical, latency-sensitive applications, driving demand for edge-hardware platforms, orchestration software, and particular integration services.

The recent growth of the open RAN ecosystem is transforming this market at a faster pace.

Open RAN's open interface, decoupled architecture, is helping to create a multi-vendor environment that could cut total RAN expenditures by 15–20% over the next five years. Open interfaces let operators mix and match best-of-breed components, hence lowering equipment prices and preventing vendor lock-in, by decoupling radio units (RUs), distributed units (DUs), and central units (CUs). Open RAN solutions are especially appealing for private-network applications and rural coverage where price and flexibility are crucial. As-interoperability-testing-matures-and-open-source-software-(e.g., O-RAN-SC) stabilizes, the Open-RAN-segment-is-set-to-capture-an-increasing share of greenfield and brownfield 5G infrastructure investments.

The expansion of broadband across rural areas is said to be an important market opportunity.

With governments directing substantial financial help via programs such as the U. S. BEAD initiative (USD 42.5 billion) and comparable grants in Europe and Asia, closing the digital divide in unserved and disadvantaged areas has become a policy priority. Public-private collaborations, where agencies offer funding and regulatory clarity and private companies offer technical innovation and infrastructural flexibility, define success, though. Often driven by local ISP groups, middle-mile fiber and wireless backhaul projects are making affordable small-cell and fixed-wireless-access solutions possible for far-flung areas. These collaborative projects provide major market chances for companies selling point-to-multipoint radios, small base stations, and network management solutions by opening fresh subscriber bases and stimulating the local economy.

Wireless Infrastructure Market Segmentation:

Market Segmentation: By Type

• Macrocell RAN

• Small Cells

• Distributed Antenna System

• Cloud RAN

• Carrier Wi-Fi

• Mobile Core

• Backhaul

The Macrocell RAN segment is said to dominate this market. Because of its vital role in initial 4G and 5G implementations, Macrocell RAN is considered the cornerstone of wireless networks, providing wide-area coverage and driving approximately 45% of wireless-infrastructure investment. The Small Cells segment is the fastest-growing segment of this market. With operators densifying metropolitan and internal environments to manage growing data traffic, offload macro networks, and provide ultra-low-latency 5G services, small cells are growing at an expected 35% CAGR.

With about 8% market share, distributed antenna systems (DAS) improve internal coverage for stadiums, shopping malls, and campuses. For the purpose of cost and energy savings, cloud RAN, which has around 7% market share, centralizes baseband processing. Carrier Wi-Fi, with about 6% of the market share, augments cellular capability in hotspots. Mobile Core, which is said to have a 15% market share, aids network slicing and 5G SA/NSA. RAN connectivity depends on investments in fiber and microwave transport, totaling around 10%.

Market Segmentation: By Technology

• 2 G/3 G

• 4 G/LTE

• 5 G

Here, 5 G technology is said to be both the dominant and the fastest-growing segment of this market. Driven by significant network-building investments in urban centers and high-bandwidth enterprise use cases, 5G infrastructure commands roughly 50% of the market worth. The fastest growing segment, projected at about 60% CAGR over the forecast period, as operators switch from pilot to commercial rollouts and scale standalone (SA) deployments. The 4 G/LTE segment continues to modernize NB-IoT and LTE-Advanced Pro with a market share of 35%. Rural and legacy IoT devices with less new spending continue to use 2G/3G with a 15% market share.

Market Segmentation: By End-Use

• Telecom Operators

• Enterprises

• Public Safety

• Others

The telecom operator segment is said to dominate this market. To satisfy customer and corporate SLAs, carriers make up roughly 70% of infrastructure purchases, macrocell expansion finance, spectrum refarming, and core-network improvements. The Enterprises segment is the fastest-growing segment of this market. They have a market share of 20%. As they are used especially in manufacturing, logistics, and campuses, which are erecting private LTE/5G networks for Industry 4.0 automation, safe connection, and IoT deployments.

When it comes to the Public Safety segment, this segment has a market share of about 5%. Here, the majority of the spending goes toward first-responder networks based on LTE. The Others segment includes utilities, transportation departments, and rural broadband projects with approximately 5% market share.

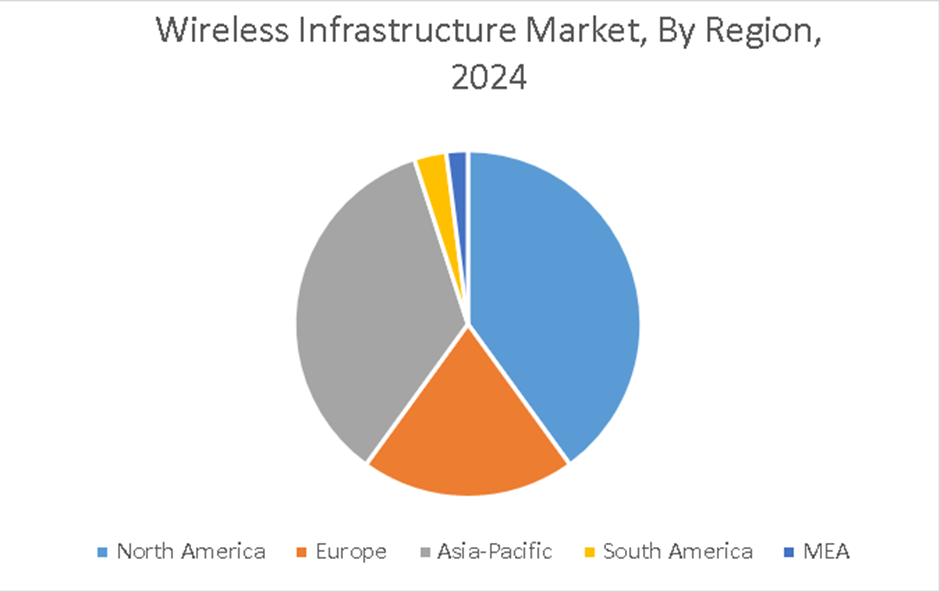

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America dominates this market, and the Asia-Pacific region is said to be the fastest-growing region. Driven by the fast deployment of 5G networks, large investments in wireless infrastructure by telecom providers, and expanding demand for high-speed internet and mobile connectivity, the North American market is the largest. Fast urbanization, significant investment in telecom infrastructure, and growing use of wireless technologies in nations including China, India, and South Korea are driving robust expansion of the Asia-Pacific region.

The market of Europe is defined by growing wireless infrastructure adoption supported by legislative frameworks encouraging 5G implementation, the need for enhanced connectivity, and investments in smart city projects in many European countries. South America is said to be an emerging market with potential growth as nations work to expand their telecommunications infrastructure, driven by the increasing demand for mobile services and internet access. The MEA region is characterized by reduced market size, yet increasing interest in wireless infrastructure as governments and commercial sectors strive to improve connectivity and encourage economic growth through enhanced telecommunications.

COVID-19 Impact Analysis on the Global Wireless Infrastructure Market:

The COVID-19 epidemic forced major short- and medium-term delays on wireless infrastructure deployments. Lockdowns and employment restrictions in 2020–21 delayed site builds and small-cell rollouts, thereby pushing 5G macrocell and backhaul installation dates out by six to nine months in many locations. Supply-chain interruptions for crucial components, RF modules, and fiber-optic cables further slowed network densification, forcing some carriers to temporarily cease new tower and DAS expansions. Furthermore, reallocated capital toward emergency healthcare and remote-work programs caused telecom-capex to grow by around 10% in 2020 relative to 2019. But stimulus programs and increased digital-transformation expenditure from 2022 onward have helped to re-energise consumption, bringing total market value for wireless infrastructure back to US$ 120.5 billion by 2022 and set for consistent recovery by 2025.

Latest Trends/ Developments:

Open RAN compatibility is now present in over 42% of new RAN installations, allowing for multi-vendor interoperability and lowering vendor lock-in. Faster innovation cycles and flexible network function scaling are enabled by virtualized, segmented RAN architectures.

About 34% of networks have built AI/ML orchestration for self-optimizing RAN (SON), predictive maintenance, and real-time load balancing, therefore cutting OPEX and reducing manual tuning labor.

Operators are using integrated access and backhaul (IAB) tiny cells to satisfy urban capacity needs and expand indoor coverage without fresh fiber, therefore increasing network densification by 50% yearly in major cities.

Tightening sustainability requirements, 31% of new equipment designs give low-power components, liquid-cooling technologies, and dynamic sleep modes top priority, achieving reductions in site energy consumption of up to 25% while maintaining throughput.

Key Players:

• ZTE Corporation

• Cisco Systems, Inc.

• NXP Semiconductors

• Qualcomm Technologies Inc.

• D-Link Corporation

• Fujitsu Ltd.

• NEC CORPORATION

• Capgemini

• Huawei Technologies Co., Ltd.

• Ciena Corporation

Chapter 1. Global Wireless Infrastructure Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Wireless Infrastructure Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Wireless Infrastructure Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Wireless Infrastructure Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Wireless Infrastructure Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Wireless Infrastructure Market- By Type

6.1. Introduction/Key Findings

6.2. Macrocell RAN

6.3. Small Cells

6.4. Distributed Antenna System

6.5. Cloud RAN

6.6. Carrier Wi-Fi

6.7. Mobile Core

6.8. Backhaul

6.9. Y-O-Y Growth trend Analysis By Type

6.10. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 7. Global Wireless Infrastructure Market– By Technology

7.1 Introduction/Key Findings

7.2. 2 G/3 G

7.3. 4 G/LTE

7.5. 5 G

7.4. Y-O-Y Growth trend Analysis By Technology

7.5. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 8. Global Wireless Infrastructure Market– By End-Use

8.1. Introduction/Key Findings

8.2. Telecom Operators

8.3. Enterprises

8.4. Public Safety

8.5. Others

8.6. Y-O-Y Growth trend Analysis By End-Use

8.7. Absolute $ Opportunity Analysis By End-Use, 2025-2030

Chapter 9. Global Wireless Infrastructure Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Type

9.1.3. By Technology

9.1.4. By End-Use

9.1.5. By Region

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Type

9.2.3. By Technology

9.2.4. By End-Use

9.2.5. By Region

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Type

9.3.3. By Technology

9.3.4. By End-Use

9.3.5. By Region

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Type

9.4.3. By Technology

9.4.4. By End-Use

9.4.5. By Region

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Type

9.5.3. By Technology

9.5.4. By End-Use

9.5.5. By Region

Chapter 10. Global Wireless Infrastructure Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. ZTE Corporation

10.2. Cisco Systems, Inc.

10.3. NXP Semiconductors

10.4. Qualcomm Technologies Inc.

10.5. D-Link Corporation

10.6. Fujitsu Ltd.

10.7. NEC CORPORATION

10.8. Capgemini

10.9. Huawei Technologies Co., Ltd.

10.10. Ciena Corporation

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Wireless Infrastructure Market was valued at USD 241.5 billion and is projected to reach a market size of USD 401.47 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 10.7%.

With broad geographical coverage, Macrocell RAN is the biggest section by revenue, while tiny cells are the fastest-growing (at around 12% CAGR) because of urban densification and indoor-coverage requirements.

Driven by early 5G commercialization, North America leads in absolute spend; however, the Asia Pacific region is the fastest-growing (roughly 6% CAGR), fueled by ambitious 5G network buildouts in China, South Korea, and developing Southeast Asian countries.

Key driving forces are the spike in mobile data traffic calling for greater capacity, the switch to 5G NR for ultra-low latency and huge IoT support, and the demand to densify networks with tiny cells and DAS for dependable indoor and urban coverage.

Initially interfering with worldwide wireless infrastructure deployments was the COVID-19 epidemic. The rise in distant work and digital services traffic, however, encouraged faster investments despite these challenges.