Global Virtual Cards Market Research Report – Segmentation By Organization Size (Large Enterprises, Medium-Sized Enterprises, Small-sized Enterprises); By Type (B2B Virtual Cards, Consumer Virtual Cards, Prepaid Virtual Cards, Credit Virtual Cards); By End User (IT & Telecom, BFSI, Heathcare, Retail); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16498

Format:

Region: Global

Market Size and Overview:

The Virtual Cards Market was valued at USD 22.97 billion in 2024 and is projected to reach a market size of USD 60.06 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 21.2%.

Indeed, the Virtual Cards Market is transforming fast into a channel in which digital payment could be made more secure, flexible, and contactless compared to the traditional physical cards. The virtual cards, generated online for one-time or limited use, are mainly used for online transactions and payment features, including business-to-business (B2B) payments and subscription services. The boom in cyber threats, coupled with increased customer demand for seamless and convenient mobile transactions, makes virtual cards the ultimate solution for fraud prevention and expense control. From banks to fintech startups to establishments, much development in tokenization, integrated with API-based integration, results in further adoption across different sectors. Of course, the virtual cards have bright prospects for continuous and immense growth since this trend towards cashless economies is global.

Key Market Insights:

Over 60% of enterprises now use virtual cards for B2B transactions. Businesses are leveraging them to simplify expense management, enhance transaction transparency, and reduce fraud risk, especially in procurement and travel payments.

More than 35% of online shoppers globally have used virtual cards in the past year. With the rise of e-commerce and digital wallets, consumers prefer virtual cards for their single-use nature and added payment security.

Virtual Cards Market Drivers:

The explosive growth of e-commerce and digital shopping has been a major catalyst for the rise of virtual cards.

A fiery booster to online shopping has given rise to virtual cards. With consumers preferring online platforms that offer speed, convenience, and security, all of which meet the needs of users of virtual cards, usage of virtual cards continues to increase. The post-COVID-19 era has seen an increased norm of contactless payment, which virtual cards provide an alternative to actual handling or swiping. They certainly present an added layer of security that they are capable of generating single- or even merchant-specific card numbers, at least significantly when used for online and overseas transactions. More so, the developing association with digital wallets as well as mobile banking apps would make virtual cards readily accessible. Because of this, younger generations, especially Gen Z and millennials, drive use as they usually already understand these digital-first financial products. For businesses, virtual cards improve workflows in managing and approving costs that can significantly help the remote team, and even for services offered through a subscription. Indeed, these trends cause a strong tally for the consumer and business sections.

In an era of increasing cyber threats and payment fraud, virtual cards offer a secure payment mechanism that minimizes risk.

Virtual cards are a safe payment mechanism against increasing cyber threats and payment fraud. Traditional cards are prone to being victimized by data theft, phishing, and not-present fraud when used online. Virtual cards counter these types of threats by providing temporary or masked card numbers, which are often single-use or restricted for certain merchants, greatly limiting their misuse. Built-in spend limits, expiration dates, and usage restrictions provide additional layers of protection for both businesses and consumers. Virtual cards have become part of a larger picture in security strategy development by financial institutions and fintech platforms. Their increased adoption and use in the travel, healthcare, and education sectors, which process most of their payments through third-party vendors, exemplifies their use in protecting sensitive financial information. Virtual cards are emerging as compliant and risk-averse solutions, with the rising regulatory emphasis on data privacy and secure payments. Such a solid security advantage continues to spur market growth and propel innovation in product segments.

Virtual Cards Market Restraints and Challenges:

One of the key challenges restraining the growth of the virtual cards market is limited merchant acceptance and compatibility with existing payment infrastructure.

Limited acceptance by merchants and a lack of compatibility with existing payment infrastructure are two of the most profound challenges that inhibit growth in the area of virtual cards. With online and mobile transactions, virtually every transaction can now be done using virtual cards. However, there are still many merchants, particularly those in developing regions or traditional physical markets, that lack the necessary systems to accept these cards. In many places, where cash predominates, these cards for consumers do not provide the same functionality or convenience as contactless physical cards or QR-based payments. Those global merchants or recurring billing platforms that do not, for instance, accept virtual cards tend to be a turn-off to consumers because they fear expired card numbers or failed transactions. These frustrations turn people off the idea of repeated use, especially in B2B use cases, as linking with enterprise accounting and expense platforms may be a technical challenge for small to medium-sized companies. Until everything can be integrated to support general usage, this technical barrier continues to be a formidable one against widespread adoption of virtual cards.

Virtual Cards Market Opportunities:

The Virtual Cards Market has a huge open space in the fintech innovation and digital inclusion in emerging economies. More smartphones will be sold along with digital banking across continents, particularly in Asia-Pacific, Africa, and Latin America. This can make virtual cards an accessible and safer tool for unbanked and underbanked populations in the future. Fintech startups are leveraging this opportunity for instant card issuance, flexible credit models, and interfaces tailored to the end-user with little local adaptation. Furthermore, new scenarios where virtual cards will be cost-effective and very widely applicable are emerging, such as entrepreneur-on-demand and remote worker marketplaces, or crossing borders, and subscription services. Virtual cards will find new ground in areas such as travel management, automated procurement, and employee expense control. With the rising demand for contactless and card-not-present transactions worldwide, virtual cards are on the path to securing connectivity and accessibility in scalable digitized financial ecosystems. The future Virtual Cards Market has an unrealized potential, especially with fintech innovation, and has crucially highlighted the digital inclusion of emerging economies. With more smartphones sold, together with digital banking, the countries that will see the most access will include Asia-Pacific, Africa, and Latin America. Virtual cards will also transform into safe and accessible financial tools for the unbanked and underbanked shortly. Fintech startups have targeted this opportunity to provide instant card issuance, flexible credit models, and user-loved interfaces with minimal local adaptation.

Virtual Cards Market Segmentation:

Market Segmentation: By Organization Size

• Large Enterprises

• Medium-Sized Enterprises

• Small-sized Enterprises

The major users of virtual cards are the large enterprises for the very reasons that their volume of transactions is high, their procurement processes are rather complicated, and they need enhanced visibility over expenditure. They usually have virtual cards for B2B transactions, travel payments, and vendor management with various global members within the organization. Medium-sized enterprises are adopting virtual cards because of the scaling factor, as they need to secure digital payments and expand automation tools.

These kinds of companies usually rely on cloud-based platforms for virtual card access without requiring a heavy IT infrastructure. Small-sized companies are still under the early adoption process; however, they are continuously maturing with interest due to easy onboarding, low-cost fintech solutions, and the requirement for fraud protection in online transactions. Since virtual card providers provide flexible, scalable, and easy-to-use platforms, penetration in the SME sector is expected to grow significantly in the coming years of forecasting.

Market Segmentation: By Type

• B2B Virtual Cards

• Consumer Virtual Cards

• Prepaid Virtual Cards

• Credit Virtual Cards

In corporate life, the B2B virtual cards manage supplier payments and automate invoicing, not to mention employee expense management, particularly for the travel and logistics industries. The popularity of consumer virtual cards is growing among those who feel the need for more secure payment methods when making online purchases, subscriptions, or services through applications. Most of these cards go into a mobile wallet for quick access. Prepaid virtual cards are perfect for setting limits on spending, such as reward programs for employees, gifts, and other restricted payments. Hence, they are perfectly suited for corporate reward and promotional efforts. On the other hand, crediting virtual cards enables a user to enjoy all the perks of a traditional credit card while benefiting from digital antipiracy and protection measures like single-use numbers or custom limits. The issuers have a broader choice to cater to personal or professional usage, thus ensuring robust market growth across all segments.

Market Segmentation: By End User

• IT & Telecom

• BFSI

• Healthcare

• Retail & E-commerce

The IT & Telecom sector employs virtual cards to manage recurring expenses such as cloud services, digital tools, and remote workforce reimbursements. This segment benefits from seamless integration of the cards with automation and accounting software. Virtual cards are used in the BFSI (Banking, Financial Services, and Insurance) sector to reduce fraud, enhance secure client disbursements, and boost compliance. Banks also offer these cards as part of their clients' digital banking services. In healthcare, virtual cards streamline provider payments, insurance reimbursements, and patient refunds while ensuring compliance with data privacy regulations. Retailers use virtual cards for supplier payments, e-commerce transactions, and employee expenses, primarily during promotional periods and high-volume sales cycles. Each of these sectors establishes a value proposition for virtual cards in terms of tracking spending, fraud prevention, and operational excellence.

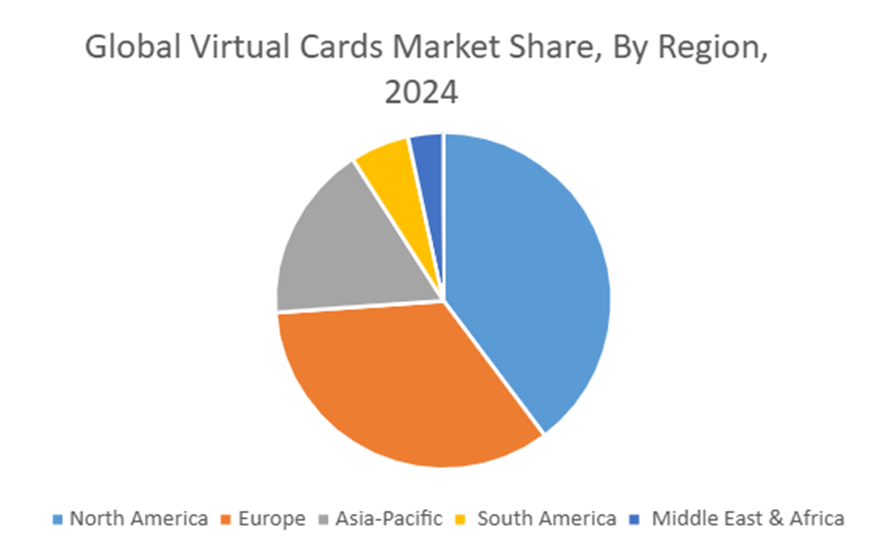

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

Notable markets for virtual cards are based in North America, with growth supported by early adoption of digital payment technologies, a mature fintech ecosystem, and strong dominance of B2B virtual card solutions. Europe closely follows behind, with contactless payments widely used, regulatory support such as PSD2, and seamless integration of virtual cards into the e-commerce space. The rapid development of the Asia-Pacific region is supported by the increased usage of smartphones, growing penetration of digital wallets, and a surge of fintech startups serving consumers and small enterprises. In South America, the rise of digital banking and a growing preference for mobile payments would bolster the implementation of virtual cards among the unbanked and gig economy users alike. The Middle East and Africa are rising markets with immense potential, backed by government-led digital transformation initiatives and the spread of regional fintech hubs that power innovative, mobile-first payment solutions.

COVID-19 Impact Analysis on the Virtual Cards Market:

The COVID-19 pandemic made the immediate adoption of virtual cards by any business or consumer in terms of payment because these had contactless and digital payment options. The lockdowns and public health issues limited in-person payment methods; online shopping, remote working, and digital services increased and demanded secure and flexible payment instruments. Virtual cards thus became the remedy of most B2B or B2C transactions with single-use numbers and spending controls that helped in blocking fraud and unauthorized charges. They increasingly provided these spaces for enterprises in the management of remote employee expenses and vendor payments, while consumers enjoyed them for subscription services and online purchases. Financial institutions and fintechs supplied this demand by expanding virtual card products, easy onboarding, and integrations to mobile wallets. The pandemic has changed the face of virtual cards from a niche product to a mainstream mode of payment, carving out a permanent place in the global trend toward cashless and digital economies. The momentum is expected to last way beyond the crisis.

Latest Trends/ Developments:

The Virtual Cards Market is changing quickly with innovations for security, automation, and the integration of digital assets. Among the more noticeable trends is having stablecoins and crypto-linked payments are evolving alongside virtual card products, such as driving global transactions with currencies using digital technology through Mastercard. Meanwhile, more strict biometric authentication and tokenization security advances now allow users to authenticate payments by the use of their fingerprints or facial features and create dynamic one-time codes for every transaction. Another future-changing technology is the introduction of virtual cards with AI-integration, where intelligent agents autonomously manage transactions under preset limits, which is even co-developed by Visa and AI companies like OpenAI and Anthropic. These innovations are certainly a touch of what will be a fruitfully successful future in imagining virtual cards as not merely secured digital devices but intelligent and adaptable assets in the growing financial ecosystem center stage for both consumers and businesses in payments.

Key Players:

• American Express Company

• BTRS Holdings, Inc.

• Wise Payments Limited

• JPMorgan Chase & Co.

• Marqeta, Inc.

• MasterCard

• Skrill USA, Inc.

• Stripe, Inc.

• WEX, Inc.

• Adyen

Chapter 1. Global Virtual Cards Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Virtual Cards Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Virtual Cards Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Virtual Cards Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Virtual Cards Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Virtual Cards Market – By Organization Size

6.1. Introduction/Key Findings

6.2. Large Enterprises

6.3. Medium-sized Enterprises

6.4. Small-sized Enterprises

6.5. Y-O-Y Growth trend Analysis By Size

6.6. Absolute $ Opportunity Analysis By Size, 2025-2030

Chapter 7. Global Virtual Cards Market – By Type

7.1. Introduction/Key Findings

7.2. B2B Virtual Cards

7.3. Consumer Virtual Cards

7.4. Prepaid Virtual Cards

7.5. Credit Virtual Cards

7.6. Y-O-Y Growth trend Analysis By Type

7.7. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 8. Global Virtual Cards Market – By End User

8.1. Introduction/Key Findings

8.2. IT & Telecom

8.3. BFSI

8.4. Healthcare

8.5. Retail

8.6. Y-O-Y Growth trend Analysis By End User

8.7. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 9. Global Virtual Cards Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Service Type

9.1.3. By Technology

9.1.4. By End User

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Organization size

9.2.3. By Type

9.2.4. By End User

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Organization Size

9.3.3. By Type

9.3.4. By End User

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Organization size

9.4.3. By Type

9.4.4. By End User

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Organization size

9.5.3. By Type

9.5.4. By End User

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Virtual Cards Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. American Express Company

10.2. BTRS Holdings, Inc.

10.3. Wise Payments Limited

10.4. JPMorgan Chase & Co.

10.5. Marqeta, Inc.

10.6. MasterCard

10.7. Visa

10.8. Skrill USA, Inc.

10.9. Stripe, Inc.

10.10. WEX, Inc.

10.11. Adyen

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Virtual Cards Market was valued at USD 22.97 billion in 2024 and is projected to reach a market size of USD 60.06 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 21.2%.

The Virtual Cards Market is driven by rising demand for secure, contactless payments and the rapid growth of e-commerce and digital wallets. Businesses and consumers alike seek enhanced fraud protection and flexible, real-time payment solutions.

The Virtual Cards Market by type is segmented into B2B Virtual Cards, Consumer Virtual Cards, Prepaid Virtual Cards, and Credit Virtual Cards. Each type caters to different user needs ranging from corporate transactions to individual online purchases.

North America is the most dominant region for the Virtual Cards Market.

American Express Company, BTRS Holdings, Inc., Wise Payments Limited, JPMorgan Chase & Co., Marqeta Inc., MasterCard, Skrill USA, Inc., Stripe Inc., WEX Inc., and Adyen are the key players in the Virtual Cards Market.