V2X Cybersecurity Market Research Report – Segmentation by Type (Endpoint Security, Network Security, Cloud Security, Application Security); By Unit Type (On-Board Units, Roadside Units); By Communication Type (Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), Vehicle-to-Grid (V2G), Vehicle-to-Cloud (V2C)); By Vehicle Type (Passenger Cars, Commercial Vehicles); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16501

Format:

Region: Global

Market Size and Overview:

The V2X Cybersecurity Market was valued at USD 2.80 Billion in 2024 and is projected to reach a market size of USD 6.71 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 19.1%.

The V2X Cybersecurity Market has cemented its position as an indispensable segment of the automotive and technology sectors, driven by the paradigm shift towards connected and autonomous mobility. This market provides the critical security infrastructure necessary to protect the intricate web of communications between a vehicle and every entity it may interact with (Vehicle-to-Everything or V2X). The push for autonomous driving further accentuates the need for unassailable cybersecurity, as the safe operation of self-driving cars is entirely dependent on the integrity of the data they receive and transmit.

Key Market Insights:

The On-Board Units (OBUs) segment represents a significant portion of this, accounting for over 59% of the market revenue.

In terms of connectivity, Dedicated Short-Range Communications (DSRC) technology holds the largest revenue share, contributing over 64% to the market in 2024.

The Vehicle-to-Vehicle (V2V) communication segment is the most dominant, with a market share of over 33%.

Similarly, passenger cars command the largest portion of the vehicle type segment, accounting for over 68% of the market share.

The market for V2X cybersecurity in vehicles with Internal Combustion Engines (ICE) holds a share of around 60%.

The number of attempted cyber-attacks on connected vehicles has increased by an estimated 99% in the first half of 2024 compared to the same period last year.

Approximately 82% of automotive manufacturers have stated that cybersecurity is a top priority in their V2X development roadmaps.

Market Drivers:

Proliferation of Connected and Autonomous Vehicles

The primary driver propelling the V2X cybersecurity market is the exponential increase in the adoption of connected vehicles and the steady march towards full autonomy. As vehicles become increasingly integrated with external networks to provide features like real-time traffic updates, remote diagnostics, and advanced driver-assistance systems (ADAS), their vulnerability to cyber threats escalates. Each connected vehicle represents a potential entry point for hackers. This necessitates a robust security framework to protect against unauthorized access, data breaches, and manipulation of vehicle functions, thereby driving the demand for specialized V2X cybersecurity solutions to ensure passenger safety and data integrity.

Stringent Government Regulations and Industry Standards

Governments and international regulatory bodies are increasingly imposing stringent regulations and standards for vehicle cybersecurity. Mandates such as the UN Regulation No. 155 (UN R155) require automotive manufacturers to implement certified Cybersecurity Management Systems (CSMS) in new vehicles. These regulations compel carmakers to integrate security by design throughout the vehicle lifecycle, from initial concept to post-production. Compliance with these standards is non-negotiable for market access, forcing manufacturers to invest heavily in advanced V2X cybersecurity solutions, thus fueling market growth and fostering a culture of security within the automotive industry.

Market Restraints and Challenges:

The V2X cybersecurity market grapples with the immense complexity of its ecosystem, which involves a multitude of stakeholders, including automakers, tier-1 suppliers, and infrastructure providers, making standardization difficult. The constantly evolving nature of cyber threats requires continuous innovation and adaptation, which can be resource-intensive. Furthermore, the high cost of implementing robust security solutions can be a deterrent for some manufacturers, particularly in price-sensitive vehicle segments. Data privacy concerns and ensuring consumer trust also remain significant challenges for the industry.

Market Opportunities:

The market for V2X cybersecurity is ripe with opportunities, particularly in the development of AI and machine learning-based security solutions that can proactively detect and neutralize threats in real-time. The rollout of 5G networks will enable more complex V2X applications, creating a demand for more advanced and low-latency security protocols. Furthermore, the growing electric vehicle (EV) market presents unique opportunities, especially in securing Vehicle-to-Grid (V2G) communications. There is also a significant opportunity for companies offering cybersecurity testing, validation, and managed services for the entire V2X ecosystem.

Market Segmentation:

Segmentation by Type:

• Endpoint Security

• Network Security

• Cloud Security

• Application Security

Cloud security is the fastest-growing segment as automakers increasingly rely on cloud platforms for data processing, OTA updates, and a wide array of connected services. Securing the vast amounts of data transmitted between vehicles and the cloud is paramount, driving the demand for robust cloud-native security solutions that offer scalability and centralized management.

Endpoint security remains the most dominant segment, as it involves securing the primary components of the V2X ecosystem, namely the On-Board Units (OBUs) in vehicles and the Roadside Units (RSUs). Protecting these hardware endpoints from tampering and malware is the first and most critical line of defense in the V2X security architecture.

Segmentation by Unit Type:

• On-Board Units (OBUs)

• Roadside Units (RSUs)

The RSU segment is the fastest growing as cities and transportation authorities accelerate the deployment of smart infrastructure to support V2X communication. The increasing number of RSUs being installed to manage traffic flow and provide safety alerts creates a corresponding need for robust cybersecurity to protect this critical infrastructure from attacks.

On-Board Units continue to be the dominant segment as they are an integral part of every connected vehicle. With millions of new connected cars hitting the road each year, the volume of OBUs requiring embedded cybersecurity solutions far surpasses that of RSUs, making it the largest segment by a significant margin.

Segmentation by Communication Type:

• Vehicle-to-Vehicle (V2V)

• Vehicle-to-Infrastructure (V2I)

• Vehicle-to-Pedestrian (V2P)

• Vehicle-to-Grid (V2G)

• Vehicle-to-Cloud (V2C)

Vehicle-to-Cloud communication is the fastest-growing segment, driven by the proliferation of cloud-based services such as telematics, infotainment, and remote vehicle management. The increasing data exchange between vehicles and cloud servers for a wide range of applications necessitates advanced security measures, fueling the growth of this segment.

Vehicle-to-Vehicle communication remains the most dominant segment. As the foundational element of cooperative safety systems, secure V2V communication is essential for collision avoidance and other critical safety applications. The focus on enhancing road safety through inter-vehicular communication ensures the continued dominance of this segment in the V2X cybersecurity market.

Segmentation by Vehicle Type:

• Passenger Cars

• Commercial Vehicles

The commercial vehicle segment is growing at the fastest rate, driven by the increasing adoption of telematics and fleet management solutions to optimize logistics and enhance safety. The need to protect sensitive cargo information and prevent disruption to commercial operations is a major factor driving the demand for advanced cybersecurity in this segment.

Passenger cars continue to be the dominant segment in the V2X cybersecurity market. The sheer volume of passenger cars being produced and sold with advanced connectivity features ensures their market dominance. Consumers' growing expectation for sophisticated infotainment, safety, and convenience features in their personal vehicles fuels the integration of V2X technology and, consequently, its security.

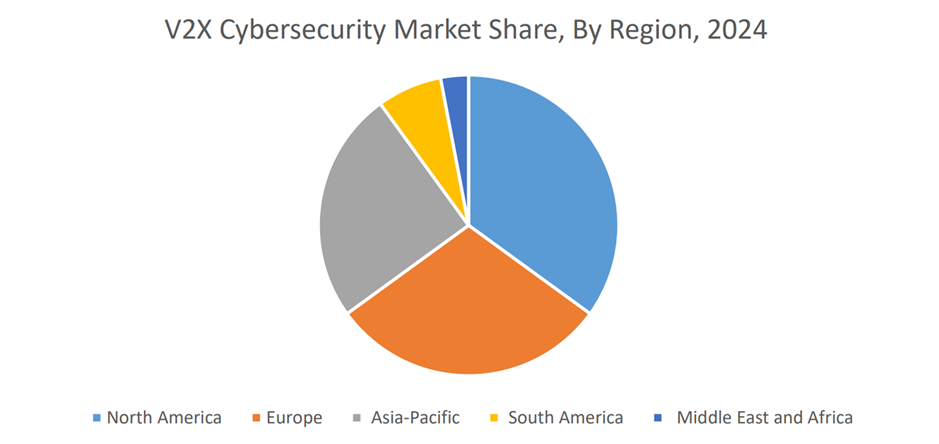

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

North America holds the largest market share, commanding approximately 32% of the global market. This dominance is attributed to the early adoption of connected vehicle technologies, the presence of major automotive and cybersecurity players, and strong government initiatives promoting intelligent transportation systems.

The Asia-Pacific region is the fastest-growing market for V2X cybersecurity. This growth is fueled by massive government investments in smart city projects, the region's burgeoning automotive market, and the rapid adoption of 5G technology, particularly in countries like China, Japan, and South Korea.

COVID-19 Impact Analysis:

The COVID-19 pandemic initially caused disruptions in the automotive supply chain and a slowdown in vehicle production, which temporarily impacted the V2X cybersecurity market. However, the crisis also accelerated the push towards digitalization and remote connectivity. This led to a heightened awareness of the importance of secure connected services and has ultimately acted as a catalyst for the market, with automotive companies increasing their investments in cybersecurity to support the new reality of a more connected and digital world.

Latest Trends and Developments:

The V2X cybersecurity market in 2024 is being shaped by several key trends. The integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive threat analytics is becoming mainstream, enabling more proactive security measures. There is also a growing focus on developing quantum-resistant cryptography to future-proof V2X communications against emerging threats from quantum computing. Additionally, the adoption of secure Over-the-Air (OTA) update mechanisms is critical for deploying security patches and new features efficiently and securely across entire vehicle fleets.

Key Players in the Market:

• Continental AG

• Robert Bosch GmbH

• HARMAN International

• NXP Semiconductors

• Infineon Technologies AG

• Vector Informatik GmbH

• Autotalks

• AUTOCRYPT

• ESCRYPT

• Green Hills Software

Chapter 1. Global V2X Cybersecurity Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global V2X Cybersecurity Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global V2X Cybersecurity Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global V2X Cybersecurity Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global V2X Cybersecurity Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global V2X Cybersecurity Market – By Type

6.1. Introduction/Key Findings

6.2. Endpoint Security

6.3. Network Security

6.4. Cloud Security

6.5. Application Security

6.6. Y-O-Y Growth trend Analysis By Type

6.7. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global V2X Cybersecurity Market – By Unit Type

7.1. Introduction/Key Findings

7.2. On-Board Units

7.3. Roadside Units

7.4. Y-O-Y Growth trend Analysis By Unit Type

7.5. Absolute $ Opportunity Analysis By Unit Type, 2024-2030

Chapter 8. Global V2X Cybersecurity Market – By Communication Type

8.1. Introduction/Key Findings

8.2. Vehicle-to-Vehicle (V2V)

8.3. Vehicle-to-Infrastructure (V2I)

8.4. Vehicle-to-Pedestrian (V2P)

8.5. Vehicle-to-Grid (V2G)

8.6. Vehicle-to-Cloud (V2C)

8.7. Y-O-Y Growth trend Analysis By Communication Type

8.8. Absolute $ Opportunity Analysis By Communication Type, 2024-2030

Chapter 9. Global V2X Cybersecurity Market – By Vehicle Type

9.1. Introduction/Key Findings

9.2. Passenger Cars

9.3. Commercial Vehicles

9.4. Y-O-Y Growth trend Analysis By Vehicle Type

9.5. Absolute $ Opportunity Analysis By Vehicle Type, 2024-2030

Chapter 10. Global V2X Cybersecurity Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Unit Type

10.1.4. By Communication Type

10.1.5. By Vehicle Type

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Unit Type

10.2.4. By Communication Type

10.2.5. By Vehicle Type

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Type

10.3.3. By Unit Type

10.3.4. By Communication Type

10.3.5. By Vehicle Type

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Unit Type

10.4.4. By Communication Type

10.4.5. By Vehicle Type

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Unit Type

10.5.4. By Communication Type

10.5.5. By Vehicle Type

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global V2X Cybersecurity Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Continental AG (Germany)

11.2. Robert Bosch GmbH (Germany)

11.3. HARMAN International (US)

11.4. NXP Semiconductors (Netherlands)

11.5. Infineon Technologies AG (Germany)

11.6. Vector Informatik GmbH (Germany)

11.7. Autotalks (Israel)

11.8. AUTOCRYPT (South Korea)

11.9. ESCRYPT (Germany)

11.10. Green Hills Software (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary growth drivers are the rapid increase in the number of connected and autonomous vehicles on the road and the implementation of stringent government regulations and industry standards that mandate robust cybersecurity measures in new vehicles to ensure safety and data protection.

The main concerns revolve around the high complexity of the V2X ecosystem, which makes standardization and interoperability challenging. Other significant challenges include the constantly evolving threat landscape, the high cost of implementation, and addressing data privacy concerns to build and maintain consumer trust.

Key players include Continental AG, Robert Bosch GmbH, HARMAN International, NXP Semiconductors, Infineon Technologies AG, Vector Informatik GmbH, Autotalks, AUTOCRYPT, ESCRYPT, Green Hills Software, Karamba Security, Qualcomm, Aptiv, Lear Corporation, and DENSO CORPORATION.

North America currently holds the largest market share, at approximately 32%, due to early technology adoption and strong regulatory support.

The Asia-Pacific region is expanding at the highest rate, driven by significant investments in smart city infrastructure, a booming automotive market, and the rapid deployment of 5G technology.