Global Utility Drones Market Research Report – Segmentation By Drone Type (Multirotor, Fixed-Wing, Hybrid), By Application (Inspection & Monitoring, Surveillance & Security, Mapping & Surveying, Delivery & Logistics, Others), By End-Use Industry (Power Generation, Power Transmission & Distribution, Renewable Energy, Oil & Gas, Telecommunication, Others), By Service Model (Direct Sales, Rental, Managed Services), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-4290

Format:

Region: Global

Market Size and Overview:

The Global Utility Drones Market was valued at USD 1.86 billion in 2024 and is projected to reach a market size of USD 4.27 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 18.09%.

Rising worker‑safety standards favoring remote asset inspections, utilities need to minimize outages and inspection expenses, and quick developments in drone autonomy, payload capacity, and battery life expanding operational envelopes all drive this steep growth.

Key Market Insights:

Over 60% of utility-drone deployments come from inspection and monitoring as quicker, safer unmanned aircraft replace helicopters and ground crews for repetitive line and asset surveys.

Valued for vertical take‑off/landing (VTOL), hovering stability, and ready sensor integration in restricted transmission‑line corridors, multirotor drones hold approximately 75% of the market by drone kind.

Reflecting utilities' preference for turnkey products, end-to-end solution providers, bundling hardware, software analytics, and flight services, captured more than 50% of the market income.

Driven by large grid expansion initiatives in China and India and rising renewable energy asset inspections, Asia Pacific is predicted to have the highest regional CAGR between now and 2030.

Utility Drones Market Drivers:

The minimization of outage and inspection costs is a major market growth driver.

Using helicopters and ground teams, conventional utility inspections may cost between USD 5,000 and 10,000 per flight hour and necessitate protracted downtimes for safe access. On the other hand, utility drones use automated flight routes to survey kilometers of transmission lines in a single sortie without line de‑energization, thereby lowering per‑mission costs by up to 70%. By reducing inspection periods from several months to as little as a few days, drone systems allow weekly or even daily hallway monitoring. Early detection of corrosion, equipment failures, and vegetation intrusion made possible by more frequent inspection lowers unexpected downtime by 15–20%. Case studies reveal that drones can boost inspection efficiency by as much as 80%, therefore allowing ground crews to concentrate on specific maintenance instead of general surveys. These savings not only help to reduce operating expenses but also increase general grid dependability and consumer happiness.

The strict regulations regarding the safety of the workers are also said to drive the need for this market.

Utilities are required to reduce human contact with high-voltage equipment by requirements such as those of OSHA for minimizing live-line exposure in the United States and those of European EN 13849 machine-safety standards. Drones carry out remote asset inspections, tower climbs, substation checks, and line surveys without endangering worker safety, therefore helping prevent expensive OSHA penalties and compliance fines. Substituting UAVs hovering precisely near conductors for human climbers in one FAA-sanctioned pilot allowed utilities to avoid any safety events throughout high-voltage pylon inspections. Beyond compliance, this change promotes a safer workplace culture and lowers insurance premiums linked to work-related injuries. The adoption of drone-based inspections keeps speeding throughout transmission, distribution, and renewable-energy applications as required safety audits grow more demanding.

The recent advancements in battery and sensor technologies are considered to be great market drivers.

With energy densities reaching 400–410 Wh/kg and flight times of utility drones surpassing 40 minutes even under strong payloads, 20 to 30% longer than two years ago, recent developments in lithium‑ion and lithium‑sulfur battery chemistry have driven energy densities. At the same time, ultra‑light LiDAR devices and thermal‑imaging cameras now weigh under 1 kg, hence allowing for combined visual, thermal, and 3D‑mapping payloads without sacrificing endurance. These integrated sensor suites capture high-resolution point clouds and identify hotspots in a single pass, hence lowering the number of flights needed for exhaustive examinations. Autonomous battery‑management systems optimize discharge curves in real time, hence maximizing usable flight time while protecting battery longevity. These technical developments enable utilities to carry out longer, more data-rich operations, therefore enhancing both the depth and frequency of asset monitoring.

The rising demand for real-time analytics is also driving the growing demand for this market.

Beyond simple image capture, utilities are demanding actionable intelligence, vegetation‑encroachment alerts, thermal‑anomaly flags, and exact 3D line‑clearance models, delivered through cloud‑based analytical platforms. AI/ML pipelines ingest raw drone data in minutes, detecting equipment faults with up to 90% accuracy and automatically prioritizing maintenance tasks based on severity. Real-time dashboards include geographical overlays so dispatchers can view fault sites contextually and distribute teams more effectively. With this immediacy, the latency between detection and repair is decreased, thereby lowering reactive maintenance costs by 20 to 25%. Preliminary analysis running directly on the drone or at the substation accelerates fault identification and enables autonomous BVLOS inspections with little human intervention as edge‑computing gateways develop.

Utility Drones Market Restraints and Challenges:

The market faces challenges from the regulatory constraints regarding airspace, which hampers market growth.

To examine long transmission corridors, utility drones sometimes need beyond‑visual‑line‑of‑sight (BVLOS) approvals, but the regulatory environment is still inconsistent. Operators in the U. S. have to get waivers under Part 107, a procedure that authorized just 203 BVLOS permissions in 2024 despite a 256% rise in applications, therefore highlighting a waiver system never intended as permanent law. With no main portal, the Drone Rules 2021 define several “red” and “yellow” areas surrounding sensitive sites, necessitating permissions from civilian aviation, military, and local authorities, thereby extending approvals by 6–9 months. Comparable administrative obstacles are found throughout Latin America and Europe, where each nation's aviation authority upholds different BVLOS standards. These drawn-out timelines choke big-scale utility deployments both by raising operating expenses and by discouraging pilots from funding specialized BVLOS-capable platforms without regulatory assurance.

The upfront investment needed for this market is considered to be very high, which makes it less affordable.

Beyond equipment, utilities pay for maintenance, insurance, and data-management infrastructure, raising total project capex well over six figures for a little fleet. Smaller and mid-tier utilities, especially in developing countries, find it difficult to obtain such budgets in light of competing grid-modernization priorities. Usually 12–18 months, this financial impediment delays ROI realization and causes some utilities to test single drones instead of full fleets, therefore constraining the economies of scale and data-frequency advantages that justify greater drone-program investment.

The rising concerns regarding data privacy and security are a major market challenge.

Utility drone inspections produce high‑resolution imagery, LiDAR point clouds, and thermal data, all of which travel public cellular or satellite channels en route to cloud platforms. Without strong end‑to‑end encryption (TLS 1.3+) and secure key‑management systems, operators risk interception or tampering of sensitive infrastructure data, exposing grid vulnerabilities to malicious actors. Strict access controls and data-retention policies are required by compliance requirements such as NERC CIP in North America and GDPR in Europe, which add layers of complexity and recurring expenses for secure-storage systems. Many utilities, therefore, team with specialized cybersecurity companies or use private LTE/5G networks to segregate drone telemetry, yet these actions raise program expenses and prolong project deployment timelines.

The growing shortage of skilled professionals needed for this market is slowing down its operations.

Efficient utility-drone systems call for multidisciplinary teams: certified remote-pilot-in-command (RPIC) operators acquainted with BVLOS procedures, geospatial analysts with great skill interpreting multispectral data, and power-systems engineers to give findings context. Still, industry studies show that 65% of such drone projects are postponed owing to a lack of skilled UAV pilots and data analysts. Training RPICs under changing airspace rules can take 3–6 months, and geospatial certifications (e.g., Esri ArcGIS) add additional ramp‑up time. Many utilities depend so on third‑party managed‑service providers, foregoing in‑house know-how and long-term knowledge sharing. Staffing restrictions will still be a major impediment to scaling utility‑drone activities worldwide until workforce development initiatives and a set curriculum catch up with the requirements of the industry.

Utility Drones Market Opportunities:

The emergence of hybrid VTOL and fixed-wing platforms presents a great market opportunity to grow further.

While fixed‑wing VTOLs such as the JOUAV CW‑25E may stay aloft for up to 8 hours and cover 200 km per mission, platforms such as the Autel Dragonfish reach up to 120 minutes of flight duration with a 2.5 kg payload, almost three times that of similar quadcopters. With a 10 kg payload capacity, the ST50F hybrid combines battery power with a gasoline engine to lengthen flight times beyond 10 hours, making it perfect for examining isolated transmission corridors in a single mission. These hybrids cut the number of staging sites and required ground support by enabling vertical takeoff to effective wing-borne cruise. For utilities, this means fewer mission interruptions, reduced per‑mile inspection expenses, and the capacity to quickly survey line miles in barely reachable terrain, features that are crucial for extensive grid and renewable‑site monitoring.

The advent of subscription-based inspection services is said to give this market an opportunity to expand its reach.

Offering on‑demand inspection packages without the need for capital‑intensive fleet ownership, drone‑as‑a‑service (DaaS) models are changing the way utilities interact with UAV technology. For a predictable subscription fee, Meticulous Research says DaaS lets utilities outsource flight operations, sensor analysis, and regulatory compliance, therefore lowering initial expenditures and in-house training load. Tiered service levels let providers combine hardware, pilot staffing, and AI‑powered data processing, including thermal‑anomaly detection and vegetation‑encroachment alerts. Early users claim 30–40% cuts in inspection-program costs and quicker ROI times, frequently under 12 months, while sustaining high data quality and regulatory compliance thanks to this flexibility, which lets utilities scale from ad‑hoc surveys to continuous monitoring without further capex.

The opportunity to integrate with the digital twin platform will enhance predictive maintenance and management.

Incorporating drone-gathered geographical data into electrical-grid digital twins improves predictive maintenance and asset management procedures. Businesses such as Geo-4D add RTK GNSS and terrestrial laser-scanning data to drone photographs and LiDAR scans to create cm-accurate 3D twins of substations and transmission corridors, enabling virtual commissioning and scenario planning. Using APIs for SOC-2 compliant data encryption, DroneDeploy's utility module combines seamlessly with GIS and SCADA systems to superimpose high-resolution orthomosaics on real-time network models. In a ComEd study, integrating drone point clouds into the network's digital twin cut labor expenses by USD 10,000 per tower upgrade and reduced site-visit times by 52%. By perfectly combining aerial data with virtual assets, operators may anticipate failure risks, maximize maintenance schedules, and simulate grid reactions under extreme-weather scenarios, hence improving network resilience and lowering life-cycle expenses.

The recent automation of BVLOS (Beyond Visual Line Of Sight) is said to bring innovation to the market.

Regulatory development on BVLOS operations is opening entirely automated, long‑distance utility-drone surveys. In April 2025, Osmose Utilities received an FAA waiver to undertake nationwide BVLOS examinations of utility poles without geographical restrictions, therefore enabling vast flight corridors and real-time structural-defect detection. The CAA's new policy for "atypical air environments" offers routine BVLOS clearances for infrastructure inspection, therefore paving the way for nightly, unattended corridor patrols by 2027. These advances reduce human‑in‑the‑loop expenses and enable consistent data collection even in harsh weather or low-light circumstances. With the maturation of AI‑driven detect‑and‑avoid solutions, BVLOS automation will let utilities get 24/7 surveillance coverage, hence lowering labor costs and guaranteeing early fault detection over whole grid networks.

Utility Drones Market Segmentation:

Market Segmentation: By Drone Type

• Multirotor

• Fixed-Wing

• Hybrid

The Multirotor segment dominates this market, and the Hybrid segment is said to be the fastest-growing segment. At around 75% market share, multirotor drones lead because of VTOL capacity, steady hovering for thorough examinations, and straightforward payload integration in small utility corridors. Offering extended range and endurance, 3 to 5 times longer flight times, hybrid VTOL/fixed-wing platforms are expanding at around 30% CAGR, hence perfectly suited for distant transmission-line and renewable-site surveys. Fixed-wing drones, which make up about 15% of the market, are outstanding for high-speed corridor inspections and broad area mapping, but their need for runways/launch systems restricts their adaptability in difficult terrains.

Market Segmentation: By Application

• Inspection & Monitoring

• Surveillance & Security

• Mapping & Surveying

• Delivery & Logistics

• Others

The Inspection & Monitoring segment is said to dominate this market, and the Surveillance & Surveying segment is said to be the fastest-growing one. Inspection and monitoring dominated, making up more than 60% of deployments. This category cuts helicopter and ground-crew expenses by roughly 70%, hence allowing weekly line-and-tower inspections that preempt failures. The Surveillance and Security segment is driven by utilities protecting remote substations and solar farms against theft and vandalism, with real-time video analytics improving asset protection, growing at roughly 25% CAGR.

The Mapping and Surveying segment is a part of asset-management processes; this section experiences consistent demand for pre-construction site modeling and vegetation-encroachment analysis. When it comes to the Logistics and Delivery segment, emerging use for transporting spare parts and critical supplies to remote tower sites, cutting crew travel time and outage restoration intervals. The Others segment represents an emerging specialty including wildlife surveys along rights‑of‑way, environmental monitoring, and emergency response.

Market Segmentation: By End-Use Industry

• Power Generation

• Power Transmission & Distribution

• Renewable Energy

• Oil & Gas

• Telecommunication

• Others

The Power Transmission and Distribution segment is said to dominate this market. Holds the most as utilities use drones for overhead-line, substation, and pole inspections, vital to sustaining grid reliability and regulatory compliance. The Renewable Energy segment is considered the fastest-growing segment. Driven by quick renewable asset buildups in APAC and EMEA, the projected 32% CAGR will increase as wind‑turbine blade and solar‑field inspections expand.

The Power Generation segment includes gas and steam plant operators who utilize drones for various purposes, like thermal imaging, stack inspection, and surveys related to steam-turbine casing in order to optimize maintenance. In the Oil & Gas segment, using drones for corrosion monitoring and leak detection, pipelines, rigs, and storage tanks improve safety in dangerous settings. When it comes to the telecommunication segment, this helps in reducing climber risk by introducing tower and antenna inspections. This also helps in streamlining maintenance cycles. The Others segment includes water utilities, rail systems, and street-light surveys using drones, respectively.

Market Segmentation: By Service Model

• Direct Sales

• Rental

• Managed Services

The Direct Sales segment is said to dominate this market. Utilities and major EPC companies buy in-house drone fleets (~ 60% share) for complete operational control and compatibility with current maintenance crews. The Managed Services segment is the fastest-growing segment of the market. DaaS providers eliminate up-front capex and in-house skill requirements with roughly 35% CAGR by providing turnkey inspections, pilot, data analytics, and report generation. The Rental segment represents about 15% of the market, favored for short-term pilot projects or seasonal peaks in work because it offers flexibility without long-term obligations.

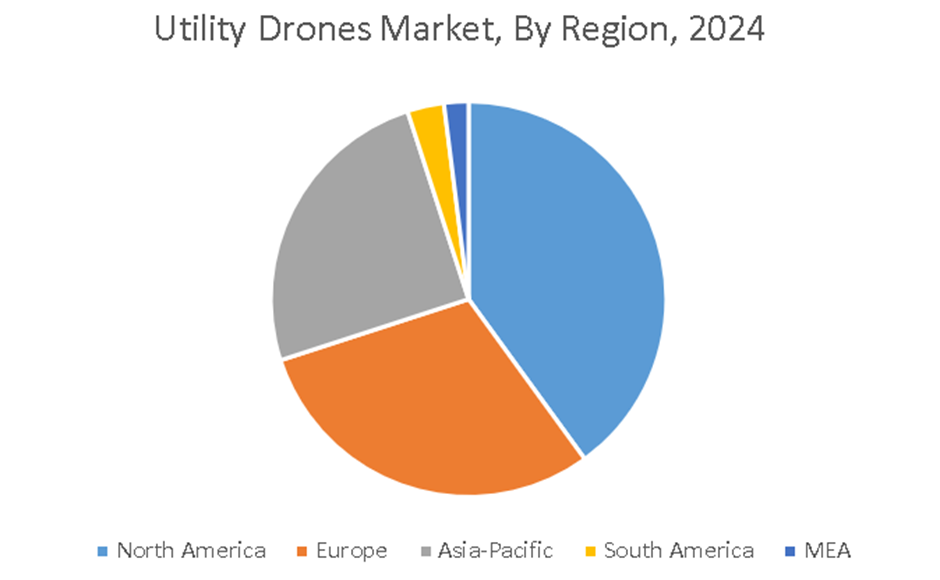

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America leads this market. Driven by widespread uptake throughout industries including energy, telecommunications, and infrastructure inspection, North America is the biggest market for utility drones. Essential elements fueling expansion include regulatory backing and drone technology advancements like better battery life and payload capability. The Asia-Pacific region is said to be the fastest-growing region of the market. Especially in nations such as India, Japan, and China, the Asia-Pacific region is expanding quickly. The increasing demand for effective utility management, urbanization, and infrastructure development is propelling the use of drones in utility applications.

Growing investment in smart grid technology and the need for effective infrastructure management drive Europe's remarkable expansion. Adopting utility drones for inspection and repair jobs, nations including Germany, the UK, and France are leading the way. The South American market is developing with increasing awareness of the advantages of drone technology in utility management. Although the market is still developing, nations like Brazil and Argentina are starting to look into using utility drones for monitoring and maintenance. Although the MEA region's market is smaller, interest in utility drones is growing as businesses try to boost operational efficiency and cut expenses. Adoption of drone technology is fueled by infrastructure and energy projects.

COVID-19 Impact Analysis on the Global Utility Drones Market:

Due to travel restrictions, the pandemic temporarily disrupted equipment supply chains and delayed field deployments, which caused a 15–20% slowdown in 2020–2021. Social‑distancing guidelines and lower onsite staffing, however, sped utilities' interest in remote‑inspection drones. Regulatory agencies fast‑tracked UAV-operation waivers for asset surveys, resulting in a 30% rebound in contract awards by late 2021. The crisis highlighted the worth of drones in guaranteeing minimal human contact grid reliability, therefore securing their function in long-term utilities-inspection plans.

Latest Trends/ Developments:

Real-time fault detection, vegetation encroachment, and corona effects, using onboard artificial intelligence processors, helps to remove post-flight analysis delays.

By 50%, coordinated drone swarms cut inspection hours, and survey several towers simultaneously.

Field-deployed hubs speed anomaly warnings and lower bandwidth requirements by pre‑processing data at substations.

Using 5G networks, pilot projects in Europe and the United States enable live-stream telemetry and autonomous beyond-visual-line-of-sight activity.

Key Players:

• Cyberhawk (Scotland)

• Delair (France)

• Measure (US)

• PrecisionHawk (US)

• HEMAV (Spain)

• DJI Inspire

• AeroVironment, Inc.

• Skyward

• Kespry

• Flyability SA

Chapter 1. Global Utility Drones Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Utility Drones Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Utility Drones Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Utility Drones Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Utility Drones Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Utility Drones Market- By Drone Type

6.1. Introduction/Key Findings

6.2. Multirotor

6.3. Fixed-Wing

6.4. Hybrid

6.5. Y-O-Y Growth trend Analysis By Drone Type

6.6. Absolute $ Opportunity Analysis By Drone Type, 2025-2030

Chapter 7. Global Utility Drones Market– By Application

7.1 Introduction/Key Findings

7.2. Inspection & Monitoring

7.3. Surveillance & Security

7.4. Mapping & Surveying

7.5. Delivery & Logistics

7.6. Others

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Utility Drones Market– By End-Use Industry

8.1. Introduction/Key Findings

8.2. Power Generation

8.3. Power Transmission & Distribution

8.4. Renewable Energy

8.5. Oil & Gas

8.6. Telecommunication

8.7. Others

8.8. Y-O-Y Growth trend Analysis By End-Use Industry

8.9. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 9. Global Utility Drones Market– By Service Model

9.1. Introduction/Key Findings

9.2. Direct Sales

9.3. Rental

9.4. Managed Services

9.5. Y-O-Y Growth trend Analysis By Service Model

9.6. Absolute $ Opportunity Analysis By Service Model, 2025-2030

Chapter 10. Global Utility Drones Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Drone Type

10.1.3. By Application

10.1.4. By End-Use Industry

10.1.5. By Service Model

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Drone Type

10.2.3. By Application

10.2.4. By End-Use Industry

10.2.5. By Service Model

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Drone Type

10.3.3. By Application

10.3.4. By End-Use Industry

10.3.5. By Service Model

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Drone Type

10.4.3. By Application

10.4.4. By End-Use Industry

10.4.5. By Service Model

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Drone Type

10.5.3. By Application

10.5.4. By End-Use Industry

10.5.5. By Service Model

10.5.6. By Region

Chapter 11. Global Utility Drones Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Cyberhawk (Scotland)

11.2. Delair (France)

11.3. Measure (US)

11.4. PrecisionHawk (US)

11.5. HEMAV (Spain)

11.6. DJI Inspire

11.7. AeroVironment, Inc.

11.8. Skyward

11.9. Kespry

11.10. Flyability SA

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Utility Drones Market was valued at USD 1.86 billion in 2024 and is projected to reach a market size of USD 4.27 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 18.09%.

Steep inspection cost savings, strict rules and regulations regarding safety, and advancements in drone autonomy and battery technology are some of the factors that are driving the growth of this market.

As power companies move from helicopter and ground surveys to drone-based line inspections, the inspection and monitoring segment takes the front stage (>60%).

Important obstacles faced by the market include BVLOS legislative approvals, high initial fleet expenses (over USD 100,000), and a lack of qualified UAV pilots and data analysts.

The epidemic sped up remote inspection demands, therefore enabling quick regulatory approvals and a permanent move toward drone-centered maintenance plans.