Global Terrestrial Trunked Radio Market Research Report – Segmentation By Product Type (Portable Radios, Vehicular Radios, Base Stations, Repeaters), By Deployment Mode (On-premises, Cloud, Hybrid), By Frequency Band (380 – 400 MHz, 430 – 470 MHz, 800 – 960 MHz), By Distribution Channel (Direct Sales, Distributors, Online Retail), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-1781

Format:

Region: Global

Market Size and Overview:

The Global Terrestrial Trunked Radio Market was valued at USD 5.28 billion in 2024 and is projected to reach a market size of USD 10.71 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 15.2%.

Offering secure, excellent voice and data services across public safety, utilities, transportation, and defense sectors, TETRA is a mature standard for mission-critical digital two-way radio. Persistent investments in next-generation public safety systems, major transit upgrading projects, and the need for resilient, interoperable communication systems in hostile environments drive growth.

Key Market Insights:

First‑responder organizations, law enforcement, and emergency medical services together make up the largest application vertical because TETRA has shown dependability and end‑to‑end encryption for crisis communication.

Most unit shipments are handheld TETRA terminals preferred for their toughness, long battery life, and built-in AES‑based voice/data encryption.

The need for committed, very secure networks, particularly in utilities and the military, drives ongoing demand for on-premise TETRA infrastructure above cloud or hybrid solutions.

With its great propagation features and worldwide harmony for public-safety and utility trunked networks, this group dominates.

Terrestrial Trunked Radio Market Drivers:

The recent modernization of public safety communications is said to drive the growth of this market.

Driving markets, public‑safety organizations all over are speeding the digital update from legacy analog radios to TETRA to meet obligations like Next‑Generation 9-1-1 in North America and Europe's "112 EEA" emergency-call demands. Modern deployments of TETRA networks also include broadband backhaul (e.g., MCPTT over LTE) to provide video streaming and telemetry for situational awareness, although they inherently support secure, priority‑based group calls and push‑to‑talk functionality. Though late, the Emergency Services Network (ESN) of the UK is investing in 20,840 new and updated 4G sites, combining TETRA's mission-critical voice with IP-based data services to cover both distant roads and urban areas. Ensuring all first-responder departments have access to a standard platform for interoperable communications during big incidents, similar to next-generation trunked networks, is under installation in Australia (ESRI), Scandinavia (Nødnett in Norway), and the Netherlands. Backed by multi-billion-dollar government spending, these modernization projects are maintaining consistent demand for both ruggedized terminals and TETRA infrastructure throughout 2030.

The recent expansion of critical infrastructure networks is driving the growth of this market.

Oil and gas operators, as well as utilities, need dependable private communications that TETRA alone offers. Beyond conventional SCADA backhaul, TETRA's Direct‑Mode Operation (DMO) allows peer‑to‑peer connections in the absence of base‑station coverage, essential for distributed‑generation locations, offshore platforms, and pipeline inspections. Integrating gas‑detector telemetry and worker‑man‑down warnings into the trunked network, major electrical companies in North America are deploying multi‑site TETRA systems over 30,000 km of transmission corridors. Large solar and wind farms in the Middle East employ TETRA for real-time monitoring and control; hence, they need hardened base stations able to endure intense heat and sandstorms. APAC's LNG and petrochemical facilities are duplicating these designs, therefore propelling purchases of base stations and gateways. Resilient fallback and group-call features of TETRA keep it front and center for important-infrastructure communication as smart-grid and Industry 4.0 projects spread.

The growing need for mission-critical interoperability is also considered to be a major market driver.

Cross-jurisdictional crises and huge events, natural catastrophes, and mass gatherings call for flawless coordination between several departments. TETRA's ETSI‑standardized interfaces and support for multi‑site roaming let police, fire, EMS, and utility teams share talk‑groups in real time, independent of the underlying provider or frequency band. Regional interoperability frameworks like Europe's CROSSBOW project standardize talk‑group mappings, while national initiatives like Canada's Public Safety Broadband Network (PSBN) incorporate TETRA gateways for voice‑priority services. Under development (ETSI TS 300 392‑12‑16), Pre‑emptive Priority Call (PPC) standards will let first responders bypass non‑critical traffic, therefore improving interoperability during multiagency activities. Underlying persistent growth in TETRA deployments across vital-service sectors is this nonstop push for standards-based, cross-vendor compatibility.

The regulatory push for spectrum efficiency is driving the need for this market.

Regulators are encouraging spectrum refarming and efficiency as commercial broadband and 5G services cover UHF bands. To reduce idle-channel occupancy, TETRA uses 25 kHz channels and implements Dynamic Channel Selection (DCS), hence allowing trunked networks to handle more users per MHz than older analog PMR systems. Under the ECC Decision (07)01, European governments are demanding that TETRA licensees maximize channel allocations and install DCS to avoid interference with neighboring services. Spectrum-scarce cities like Tokyo and Singapore in Asia Pacific need TETRA operators to group low-use sites and use frequency-reuse algorithms, therefore guaranteeing strong coverage with a small spectrum footprint. These regulatory measures, along with auction incentives for narrowband technologies, are driving network expansions and license renewals, as agencies-seek-long‑term-authorization-for their mission-critical TETRA systems.

Terrestrial Trunked Radio Market Restraints and Challenges:

The upfront cost related to its infrastructure is very high, which negatively impacts its adoption rate.

Deploying or growing a TETRA network calls for substantial upfront investment: base‑station locations costing USD 100–200k each, switching centers, hardened shelters, and certified spectrum fees, sometimes making up 30–40% of an agency's yearly communications budget. In emerging markets, where site acquisition, civil works, and power provisioning dominate CapEx, total build‑out for a mid‑sized network can exceed USD 20 million, thereby discouraging governments that might otherwise prefer lower‑cost LTE solutions or shared‑infrastructure models. Moreover, lengthy lead times for particular equipment and the need for bespoke installation and training expand original project timetables to 12–18 months. Many smaller utilities and towns postpone upgrades without concessional funding or public‑private partnerships, choosing to maintain aging analogue systems far beyond their best service life.

The market faces tough competition from broadband technologies that are evolving day by day.

The growing 3GPP‑standard Mission‑Critical Push‑to‑Talk (MCPTT) and new 5G MC services are undermining TETRA's historic edge in field‑voice reliability. Along with voice, MCPTT provides high-bandwidth data (video, GIS) and end-to-end QoS guarantees and standard IMS-based Interworking. By 2026, the ESN initiative of the UK intends to replace the Airwave TETRA network with an LTE‑based platform, therefore pointing to a change toward converged broadband‑centric solutions. Although TETRA still outperforms for ultra-low-latency group calls in deep coverage situations, hybrid devices that support both TETRA and LTE are now preferred by agencies looking for continuous multimedia communications, therefore endangering new pure-TETRA deployments and driving vendors to include broadband modules into phones.

The complexity in the migration of this market is said to be a huge challenge faced by it.

Transitioning from first-generation TETRA systems or analog networks to next-gen broadband-integrated networks requires sophisticated preparation and extended dual-network activities. Airbus points out that moving dispatch centers, tailored narrowband data apps, and control‑room workflows to LTE/5G requires specific interface development for each of the hundreds of legacy control‑room solutions in use, often a 3–5 year project with simultaneous‑network OPEX until decommissioning is complete. In effect, agencies must map current talk group setups, recertify encryption profiles, and confirm emergency call processes across both networks while preventing service outages. These problems have a major influence on project return on investment and discourage quick technological updates in industries where business continuity is critical.

The existence of a limited vendor ecosystem also hampers the growth potential of this market.

Few specialized suppliers, Airbus DS, Motorola Solutions, Hytera, Sepura, and some regional players, dominate the TETRA market, therefore, limiting competitive pricing and innovation cycles compared to more extensive cellular ecosystems. Longer procurement lead times, greater warranty and service expenses, and fewer choices for end‑customers looking for multi‑technology convergence (e.g., TETRA + P25 + MCPTT) could arise from this oligopoly. Although the TETRA Association supports many companies, actual multi-vendor interoperability still calls for intensive testing and integration effort, hence slowing down new entrants and maintaining strong hurdles to admission in the mission-critical communications industry.

Terrestrial Trunked Radio Market Opportunities:

The emergence of TETRA-LTE Convergence gateways is said to bring in new opportunities for this market.

Real‑time video streaming, GIS mapping, and improved situational‑awareness applications are possible using Sepura's "Migration to LTE" gateways, which let legacy TETRA radios tunnel data over private LTE networks, therefore avoiding the replacement of already installed handsets. This approach unlocks broadband access for field teams while maintaining TETRA's mission-critical voice quality, complete with encryption and QoS. Early adopters claim a 30–40% cut in capital expenditures since only data-backhaul routes demand LTE upgrades. Governments and utilities are testing these portals to prolong the lifespan of their TETRA fleets, so postponing significant device refreshes and spread data-service expenditures throughout the current LTE infrastructure.

The high-speed integration of smart cities with IoT is said to be beneficial for the market.

Using their TETRA networks, municipalities are transporting non‑voice IoT data and generating income for smart‑city services by means of trunked‑radio capacity. Over a shared network, Huawei's eLTE + TETRA solutions merge public-safety voice with IoT-sensor feeds, such as gunshot detectors, air-quality monitors, and traffic-incident warnings, feeding city-wide command centers in real time. For example, Barcelona's pilot program overlays trash-bin fill-level and parking-sensor information onto the TETRA spine to reduce dispatch-fleet mileage by 25% and allow dynamic route scheduling. Cities create fresh revenue streams from pay-per-use IoT applications while guaranteeing that emergency-response traffic keeps top priority by treating their trunked-radio spectrum as a multi-service platform. Beyond simple voice communications, this full-stack integration highlights the adaptability of TETRA.

The recent software-defined upgrades in the radio industry are said to be a major market growth opportunity.

Adding multi-protocol capability (TETRA, P25, DMR) through firmware upgrades rather than hardware swaps, software-defined radio (SDR) transceivers, such as those from Analog Devices' RF Agile SDR family, are revolutionizing hardware refreshes in TETRA. High out‑of‑band rejection, on‑the‑fly filtering, and fast protocol upgrades are all provided by FPGA/DSP architectures in HELIOS's SDR-based off‑air repeaters without fresh RF front-ends. By combining several legacy-narrowband-networks into one single-SDR-platform, agencies can therefore save 15–20% on total cost of ownership over five years. As field teams transport identical hardware that may be configured in real time to meet changing mission needs or spectrum reallocations, this flexibility speeds normal migrations and streamlines logistics.

The use of private LTE adjuncts for the purpose of coverage gaps is an opportunity for the market to develop.

By supplementing TETRA with a few LTE cells, blind‑spot problems in tunnels, high‑rise buildings, and isolated locations are addressed without expensive civil infrastructure projects. Alongside TETRA base stations, local LTE solutions (e.g., CBRS in North America) can ensure guaranteed broadband data while TETRA continues to be the main voice network. Private‑LTE hotspots have been installed by logistics professionals at port and railroad facilities to guarantee zero data loss even when TETRA coverage temporarily disappears by maintaining perfect video surveillance and asset monitoring throughout subterranean rail yards. Integrators are providing single enclosures combining TETRA and LTE as private‑LTE experience advances, therefore lowering site‑installation costs by 30% and allowing unified management of narrowband voice and broadband data across critical‑communications estates.

Terrestrial Trunked Radio Market Segmentation:

Market Segmentation: By Product Type

• Portable Radios

• Vehicular Radios

• Base Stations

• Repeaters

The Portable Radios segment dominates this market. Preferred by first responders and field crews for toughness, long battery life, and built-in encryption, handheld TETRA terminals catch nearly 60% of device sales. The vehicular Radios segment is said to be the fastest-growing segment of the market. Driven by metro, rail, and fleet-management improvements needing embedded trunked communications in cars, in-vehicle TETRA devices are growing at around 8% CAGR.

Accounting for roughly 25% of infrastructure expenditure are base stations, which mirror continuing network construction and capacity growth initiatives in public safety and utilities. Representing a niche segment (<10%) employed to broaden coverage in difficult locations, such as mountain areas, tunnels, and large complexes, is the Repeaters segment.

Market Segmentation: By Deployment Mode

• On-premises

• Cloud

• Hybrid

The On-premises segment leads this market. On-premise networks hold around 70% of the market share as utilities and agencies give data sovereignty, assured QoS, and direct mission‑critical communication control top priority. The Hybrid segment is the fastest-growing one in the market. Combining on‑prem TETRA core with cloud‑hosted administration and analytics is rising at almost 12% CAGR, so enabling quick feature upgrades and remote‑maintenance capabilities. Despite security and latency issues, pure cloud-native deployments remain restricted (~ 10% share), yet they are gaining ground in non-mission-critical business environments.

Market Segmentation: By Frequency Band

• 380 – 400 MHz

• 430 – 470 MHz

• 800 – 960 MHz

The 800 – 960 MHz segment is said to dominate this market, and the 380 – 400 MHz segment is said to be the fastest-growing segment. Widely harmonized for public‑safety and utility trunked networks, this band controls about 50% of worldwide deployments, providing balanced coverage and data‑capacity trade-offs. 380–400 MHzGrowing at about 9% CAGR in Eastern Europe and APAC, where lower-frequency propagation helps to provide better coverage and penetration within structures. The 430 – 470 MHz segment is used for government and defense networks needing spectrum in this UHF band, holds around 30% share in Latin America and Europe.

Market Segmentation: By Distribution Channel

• Direct Sales

• Distributors

• Online Retail

The Direct Sales segment is the dominant segment here. OEM direct contracts make up roughly 55% of sales since big public‑safety and utility clients buy integrated TETRA solutions together with professional services. The Online Retail segment is considered to be the fastest-growing segment. Serving smaller companies and third-party accessories markets, specialist web portals and e-marketplaces are expanding at around 15% CAGR. When it comes to the Distributors segment, providing local inventory, financing, and integration assistance for mid-market and regional companies, value-added resellers have nearly 30% market share.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

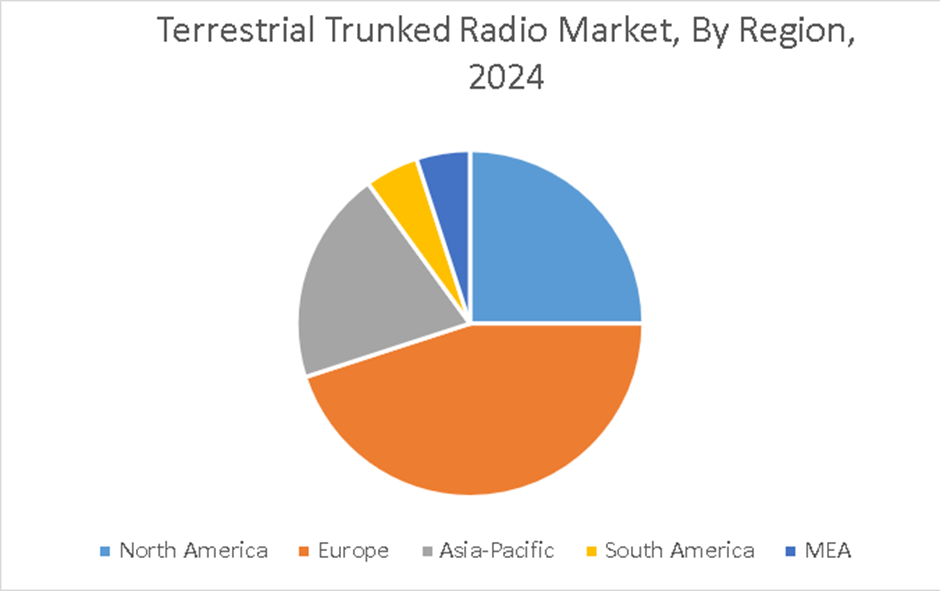

Here, Europe is said to dominate the market. With extensive adoption across many industries, including public safety, transportation, and utilities, Europe is the largest market for TETRA. Supported by government policies and a great focus on secure communication systems, countries like the UK, Germany, and France are ahead in TETRA deployment. The Asia-Pacific region is the fastest-growing region. Particularly in nations like India, Australia, and China, the Asia-Pacific area is seeing notable expansion in the TETRA market. Driving the TETRA system's acceptance are growing urbanization, the need for effective communication in emergency services, and the development of transportation networks.

Market expansion in North America is being driven by the need for dependable and secure communication solutions in urgent circumstances, even if other communication technologies are dominating the area. South America is an emerging market that is increasingly cognizant of the advantages TETRA systems provide for public safety and transportation. Though the market is still growing and presents problems, including legislative obstacles and infrastructure constraints, nations like Brazil and Argentina are starting to use these technologies. When it comes to the MEA region, though its market is limited, the MEA region is seeing growing interest in TETRA systems since governments and businesses look for trustworthy communication solutions for public safety and emergency response. Investments in infrastructure and security initiatives are anticipated to fuel future development.

COVID-19 Impact Analysis on the Global Terrestrial Trunked Radio Market:

Restrictions on site access and supply chain disruptions caused the postponement of many major deployments in 2020–2021, thereby slowing down base station and equipment installations by 10–15%. But TETRA networks' critical‑communications character gave top priority to emergency‑response upgrades' completion, and stimulus‑funded infrastructure projects revived momentum by 2022. Moreover, highlighting TETRA's resilience was the necessity for secure, dependable communications in healthcare and public-safety command centers, which sped up equipment refresh cycles and remote-maintenance abilities.

Latest Trends/ Developments:

Machine-learning algorithms are being integrated in TETRA core controllers to forecast traffic surges, auto-adjust channel assignments, and preempt network congestion in real-time.

New TEDS (TETRA Enhanced Data Service) modules increase data rates from 28.8 kbps to over 100 kbps, therefore enabling video‑streaming features on normal TETRA devices.

Supporting effortless fall between TETRA and LTE/5G MCPTT, dual-mode handsets guarantee universal coverage and high-bandwidth data on the same device.

In remote areas, solar‑powered off‑grid TETRA repeaters and base stations are being used to lower OPEX for rural network expansions and carbon footprints.

Key Players:

• Motorola Solutions

• Airbus Defence and Space

• Hytera Communications

• Sepura Ltd.

• Cassidian

• Tait Communications

• Rohill Engineering

• Simoco Wireless Solutions

• Codan Communication

• Leonardo S.p.A.

Chapter 1. Global Terrestrial Trunked Radio Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Terrestrial Trunked Radio Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Terrestrial Trunked Radio Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Terrestrial Trunked Radio Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Terrestrial Trunked Radio Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Terrestrial Trunked Radio Market- By Product Type

6.1. Introduction/Key Findings

6.2. Portable Radios

6.3. Vehicular Radios

6.4. Base Stations

6.5. Repeators

6.6. Y-O-Y Growth trend Analysis By Product Type

6.7. Absolute $ Opportunity Analysis By Product Type, 2025-2030

Chapter 7. Global Terrestrial Trunked Radio Market– By Deployment Mode

7.1 Introduction/Key Findings

7.2. On-premises

7.3. Cloud

7.4. Hybrid

7.5. Y-O-Y Growth trend Analysis By Deployment Mode

7.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global Terrestrial Trunked Radio Market– By Frequency Band

8.1. Introduction/Key Findings

8.2. 380 – 400 MHz

8.3. 430 – 470 MHz

8.4. 800 – 960 MHz

8.5. Y-O-Y Growth trend Analysis By Frequency Band

8.6. Absolute $ Opportunity Analysis By Frequency Band, 2025-2030

Chapter 9. Global Terrestrial Trunked Radio Market– By Distribution Channel

9.1. Introduction/Key Findings

9.2. Direct Sales

9.3. Distributors

9.4. Online Retail

9.5. Y-O-Y Growth trend Analysis By Distribution Channel

9.6. Absolute $ Opportunity Analysis By Distribution Channel, 2025-2030

Chapter 10. Global Terrestrial Trunked Radio Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Product Type

10.1.3. By Deployment Mode

10.1.4. By Frequency Band

10.1.5. By Distribution Channel

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product Type

10.2.3. By Deployment Mode

10.2.4. By Frequency Band

10.2.5. By Distribution Channel

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Product Type

10.3.3. By Deployment Mode

10.3.4. By Frequency Band

10.3.5. By Distribution Channel

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Product Type

10.4.3. By Deployment Mode

10.4.4. By Frequency Band

10.4.5. By Distribution Channel

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Product Type

10.5.3. By Deployment Mode

10.5.4. By Frequency Band

10.5.5. By Distribution Channel

10.5.6. By Region

Chapter 11. Global Terrestrial Trunked Radio Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Motorola Solutions

11.2. Airbus Defence and Space

11.3. Hytera Communications

11.4. Sepura Ltd.

11.5. Cassidian

11.6. Tait Communications

11.7. Rohill Engineering

11.8. Simoco Wireless Solutions

11.9. Codan Communication

11.10. Leonardo S.p.A.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Terrestrial Trunked Radio Market was valued at USD 5.28 billion in 2024 and is projected to reach a market size of USD 10.71 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 15.2%.

Increased public‑safety network upgrades, utility‑infrastructure improvements, and a desire for safe, resilient communications in difficult settings all fuel growth.

Public Safety and Government has about a 45% share because of TETRA's encryption, group-call features, and emergency alert capability.

High infrastructure costs, rivalry from broadband‑based MCPTT, legacy‑system migration complexity, and a focused vendor environment all present adoption challenges that are faced by this market.

Integrations with LTE/5G, expanded data services (TEDS), artificial intelligence–based network management tools, and green–site solutions are increasing the relevance of TETRA in next–generation mission–critical networks.