Global Telecom Expense Management Market Research Report – Segmentation By Solution (Dispute Management, Invoice Management, Ordering & Provisioning Management, Sourcing Management, Usage Management, Others), By Service (Managed Services, Professional Services), By Deployment (Cloud, On-premises), By Enterprise Size (Large Enterprises, SMEs), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-10233

Format:

Region: Global

Market Size and Overview:

The Global Telecom Expense Management Market was valued at USD 4.95 billion and is projected to reach a market size of USD 9.64 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 14.26%.

By means of invoice audit, use tracking, dispute resolution, and automated provisioning, TEM solutions and services let companies acquire visibility and control over their telecommunications and IT expenditure, covering mobile, fixed‑line, and cloud services. Rising mobile subscriptions, challenging multi-vendor settings, 5G deployments, and cost-cutting demands all help to drive growth. For both major and mid-market companies, TEM systems interface with procurement solutions and OSS/BSS to automatically manage lifecycle-wide expenses, therefore providing OPEX savings and strategic insights.

Key Market Insights:

Offering quick scalability, worldwide invoice consolidation, and SaaS‑based analytics, which account for about 62% of deployments in 2024, cloud‑hosted TEM solutions dominate.

As companies give error-free billing and dispute reduction top priority, invoice management, including automated audit, validation, and consolidation, grabs roughly 28% of solution income.

Driven by SME's desire for turnkey operations, outsourced managed services, covering 24x7 support, dispute resolution, and process outsourcing are expanding at around 16% CAGR (2025–2030).

Larger companies with complicated telecom portfolios and committed IT budgets drive around 70% of the whole market by using TEM to handle international multi‑carrier agreements and legal compliance.

Telecom Expense Management Market Drivers:

The rise in the subscription rate of 5 G networks and mobile is driving the growth of this market.

Driven by rapid network rollouts in China, India, and North America, ABI Research projects that 5G connections will increase from 934 million to more than 3 billion by 2027 at a 27% CAGR, reflecting saturated consumer adoption and the addition of IoT links. 8.8 billion mobile subscriptions, up from 8.7 billion a year ago, reflect saturated consumer demand and the addition of IoT connections. This outburst of fast, low‑latency devices doubles service plans, covering voice, data, IoT, and private‑network slices, and greatly increases organizational telecom cost footprints. Enterprises are increasingly deploying tens of thousands of new SIM-enabled sensors and 5 G-powered endpoints, yet they are faced with opaque, varied rate structures that make precise use monitoring and rate-plan optimization practically impossible without specialized TEM platforms. Therefore, companies are using TEM systems to automatically ingest carrier invoices, reconcile consumption against agreed-upon rates, and highlight anomalies, thereby avoiding the tsunami of 5G and IoT-driven consumption from resulting in uncontrolled telecom expenses.

The existence of a multi-vendor environment has raised the need for this market.

Usually working with 10 to 50 carriers and service providers covering mobile, fixed‑line, cloud connection, and field‑service links, businesses each issue invoices in different styles and employ varied pricing structures. Because of this diversity, frequent billing mistakes result: analysts estimate 7–15% of telecom invoices include errors; hence, manual dispute management that burdens AP teams and slows cost recovery is required. Telecom Expense Management solutions address this complexity by standardizing various invoice data through strong ETL pipelines and unified analytics engines, therefore lowering invoice disputes by up to 40% and accelerating dispute-resolution cycles by 50%. Combining provisioning, usage, and billing data on a single dashboard helps procurement and finance to enforce policy compliance, automate vendor‑rate benchmarking, and simplify vendor negotiations, therefore turning a turbulent multi‑vendor terrain into manageable, cost‑optimized portfolios.

The rising need for OPEX reduction and visibility is driving the growth of this market.

Usually accounting for 3 to 8% of an organization's overall IT budget, telecom costs are an ideal candidate for CFOs under pressure to reduce operational expenses. Without central visibility, unused lines, under-utilized data plans, and superfluous cloud-connectivity services quietly raise bills. Implementing TEM provides quick OPEX savings: businesses report a 15–20% reduction in telecom spending within the first year by spotting and decommissioning orphaned services, maximizing rate plans, and renegotiating carrier contracts dependent on usage analytics. Real-time spend dashboards let finance teams quickly detect abnormalities, such as runaway roaming expenses, and apply policies through automated alerts. With this granular control, telecommunications becomes a strategic tool for operational efficiency and cash flow management rather than a vast cost center.

The need to comply with the rules and audit requirements is also driving the growth.

Stringent rules like GDPR in Europe, CCPA in California, and Sarbanes‑Oxley for public corporations call for thorough expense‑trail documentation and quick audit response. Conventional manual methods of collecting usage logs and invoice records can take weeks and are susceptible to human error. TEM systems automatically log every invoice line, contract term, and dispute action, producing audit‑ready reports in minutes and lowering manual audit‑preparation time by 50%. Built-in compliance modules automatically update reporting templates, therefore guaranteeing continuous adherence without additional personnel, and keep tabs on legislative changes like those for new data protection laws. By embedding governance and traceability into expense flows, TEM solutions not only lower audit risk but also free compliance teams to focus on higher-value, risk-management activities.

Telecom Expense Management Market Restraints and Challenges:

The process of implementation for this market is quite complex, which poses a major challenge for the market.

Integrating TEM platforms into already installed OSS/BSS systems, ERP modules, and several carrier billing systems remains a difficult undertaking for businesses. Grand View Research reports that 68% of TEM deployments encounter major integration obstacles as custom ETL pipelines must be created to extract and transform call detail logs, invoice line items, and service‑provisioning data into a single schema. Further prolonging timelines and increasing budgets by 20–25% owing to consultancy fees and middleware licenses, constructing API connections for each carrier's unique billing interface. Particularly labor-intensive is data-model harmonization: inconsistent billing codes across vendors and mismatched field definitions call for manual mapping and verification, therefore adding a continual maintenance burden. Many companies have strained IT resources and delayed return on investment as a result; therefore, TEM suppliers have created low‑code ETL frameworks and pre‑built integration adapters to speed up deployments.

The risk to the privacy and sovereignty of the data is a big issue faced by the market.

Under strong global privacy restrictions are telecoms use and location data, encompassing call logs, geolocation pings, and IoT‑device telemetry. According to The Business Research Company, 74% of companies using TEM in the cloud have to satisfy data‑residency requirements like those under GDPR, which call for EU citizen information to remain within the European Economic Area. Cross‑border cloud deployments often set off regulatory reviews; therefore, businesses must embrace hybrid designs that store sensitive data on local servers yet use public‑cloud analysis for non‑regulated tasks. This hybrid approach increases operational overhead, managing two environments, synchronizing data sets, and guaranteeing uniform security measures, and could restrict the TEM platform's scalability and feature agility. To solve these problems, TEM suppliers now provide built‑in encryption key‑management services and region‑specific data‑centers, but these features may cost extra that smaller businesses may deem excessive.

The huge skill gap in the workforce is slowing down the operations of the market.

Advanced TEM systems increasingly include predictive analytics and machine-learning models to anticipate telecom costs and identify strange billing patterns. Only 42% of companies, according to a GlobeNewswire poll, have the necessary internal data‑science expertise to properly create, train, and maintain these models. The specialized skill set—combining telecom domain expertise, ETL pipeline design, and ML algorithm tuning—is in great demand; therefore, many companies hire external consultants and professional services. This dependence raises prices and stretches project schedules. Compared to internal projects, outsourced analysis engagements can cost 30–40% more and need 3–6 months longer to provide practical insights. Leading companies are investing in internal training initiatives and working with universities to create a pipeline of telecom-focused data scientists to bridge the gap; however, these projects need time and tactical commitment.

The problem of ROI measurement is a major market challenge that affects the market severely.

Still, a major challenge is proving an obvious, measurable return on investment from TEM projects. Often in finance, cost savings, such as unused-line deactivations and invoice audit recoveries, accumulate; operating efficiencies show in IT and procurement, therefore causing siloed advantages hard to harmonize. Many companies lack consistent governance systems and KPIs to combine these benefits into one business case, hence causing stakeholder conflict and under-resourced projects. Cross-functional TEM steering committees should be set up, shared metrics (e.g., total telecom spend reduction, dispute-resolution cycle time, and compliance audit savings) should be defined, and change-management best practices should be used to spur user adoption, according to industry analysts. Companies that use such systems often record 20–25% quicker fulfillment of anticipated savings and greater project satisfaction rates, therefore highlighting the need for organized ROI measurement in supporting TEM investments.

Telecom Expense Management Market Opportunities:

The use of predictive expense analytics, which is driven by AI, is seen as a major market opportunity.

Predictive analytics modules can forecast monthly telecom budgets with 90% accuracy by examining historical invoices, usage patterns, and vendor rate changes, therefore assisting finance departments in resource allocation and cost overrun avoidance. Real-time identification of anomalies, such as unexpected surges in roaming fees or data-plan overages, by these systems sets alarms that help to avoid unanticipated costs. What‑if scenario planners allow procurement to simulate the effect of changing service providers or negotiating rate plans, hence measuring possible savings before contracts are signed. Early users of AI-driven TEM analytics claim 20 to 25% decreases in contested costs and 15% closer budget adherence within six months. Predictive analytics tools will become vital for businesses looking for operational efficiency as well as strategic foresight driven by 5G and IoT implementations, as the volume and complexity of telecom spending rise. As companies widely embrace UC&C systems (e.g., Microsoft Teams, Zoom Phone), TEM solutions go beyond conventional voice and mobile administration to include partnership‑license tracking and quality‑of‑service analysis.

The opportunity to integrate with the unified communications and collaboration is helping the market to develop further.

When combined with TEM, unified call analytics offers end‑to‑end visibility: while call analytics pulls CDRs directly from IP‑PBXs and UCaaS platforms to assess actual usage and peak concurrent sessions, TEM manages carrier billing specifics and rate‑plan costs. By matching these databases, companies may find over-licensed users, for example, chairs set for premium conferencing but infrequently used, thereby freeing up 15–20% in license cost savings. Moreover, TEM‑UC&C integration facilitates automated policy enforcement: when quality metrics fall below thresholds, service-level warnings can cause quick corrections or escalations. This whole approach improves user productivity and cooperation performance in addition to maximizing expense management across all communication mediums.

The latest SME-oriented SaaS TEM offerings are said to be a great market growth opportunity.

Traditionally, the domain of large businesses, TEM is now democratizing through cloud‑native, self‑service platforms designed for SMEs. Solutions like Spenza's TEM system provide modular, pay‑as‑you‑go pricing, starting at as little as USD 1 per device per month, and low‑touch onboarding that imports carrier invoices, maps usage, and produces automated alerts within days. Pre‑configured dashboards that highlight orphaned lines, roaming‑charge spikes, and unused data pools benefit SMEs; they frequently capture 10–15% in immediate cost savings without expensive consulting fees. Integrating with popular business tools (IAM, MDM, Slack), these platforms automate provisioning changes, such as upgrades or deactivations, hence lowering manual overhead. By lowering technical and financial barriers, SME‑focused SaaS TEM offerings are expanding the market and empowering smaller organizations to achieve enterprise‑grade spend visibility.

The emergence of value-added vendor negotiation services is an important market development opportunity.

Leading TEM providers are installing sophisticated procurement engines that benchmark contract rates and automate RFP processes beyond simple auditing and monitoring. Services like Cass Information Systems' Telecom Procurement use proprietary market‑rate databases to evaluate an organization's contracted rates against rivals, providing 5–8% additional savings on renewals. These platforms can ingest hundreds of RFP responses, harmonize pricing systems across currencies, and show simulated savings scenarios in interactive dashboards. In addition to expert negotiation assistance, either advisory or fully managed, firms obtain a data‑driven advantage to get better terms. Clients using such value-added negotiation services often obtain a 500% ROI within the first year; hence, TEM becomes a strategic means for continuing carrier-contract optimization.

Telecom Expense Management Market Segmentation:

Market Segmentation: By Solution

• Dispute Management

• Invoice Management

• Ordering & Provisioning Management

• Sourcing Management

• Usage Management

• Others

The Invoice Management segment dominates the market as it quickly removes overcharges and recovers challenged sums. Invoice-management systems comprise the biggest segment (about 28%) of TEM sales; firms give accurate billing and automated auditing processes topmost priority. The Dispute Management segment is the fastest-growing segment of the market. The demand for automated dispute-resolution solutions is increasing as carriers' billing complexity grows; the dispute-management category is expected to have the highest CAGR (approximately 16%) as companies try to simplify supplier negotiations and resolve billing mistakes faster.

The Ordering and Provisioning Management segment includes automating service requests, line activations, and device provisioning across several carriers. This section helps to lower fulfillment mistakes by 25% and cut manual order‑to‑activation times by as much as 40%. Centralizing carrier contract comparison, rate‑plan benchmarking, and RFP processes, sourcing management solutions let businesses negotiate better conditions and save 5–8% more money on new contracts. Real-time consumption of voice, data, and cloud services is monitored by usage management, which also enforces policy restrictions and notifies of overages to lower bill-shock events by 30% and strengthen budgetary adherence. Other TEM solutions provide whole visibility that results in an extra 10–12% in operating efficiencies beyond core spending controls by including asset management, policy compliance, and network‑usage analysis.

Market Segmentation: By Service

• Managed Services

• Professional Services

The Managed Services, which hold roughly 60% of revenue, are the dominant segment of the market. It is the backbone of TEM initiatives, is continuous, 24x7 operations, fraud monitoring, invoice dispute handling, and reconciliation, which propel constant managed-services acceptance. The Professional Services segment is the fastest-growing segment of the market, with around 16% CAGR. Demand for expert consulting, integration, and custom analytic services is surpassing core managed‑services usage as implementations get more sophisticated (integrations, bespoke analytics).

Market Segmentation: By Deployment

• Cloud

• On-premises

The Cloud-based segment dominates this market. Rapid scalability, worldwide invoice consolidation, and SaaS‑based analytics offered by cloud‑native TEM make it the preferred choice for big, dispersed companies. The On-premises segment is the fastest-growing, though with longer setup times, more controlled sectors and businesses with high data-sovereignty needs are choosing on-premise deployments, therefore spurring quicker expansion in this area.

Market Segmentation: By Enterprise Size

• Large Enterprises

• SMEs

Large Companies constitute roughly 70% of all spend. The majority of TEM investments come from large firms with large, multi‑carrier telecom portfolios to handle global contracts and complicated invoicing environments. SMEs (~18% CAGR)SMEs are reducing the barrier to entry thanks to cloud-based, self-service TEM systems, therefore facilitating quick deployment and real cost transparency, and accelerating SME adoption.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

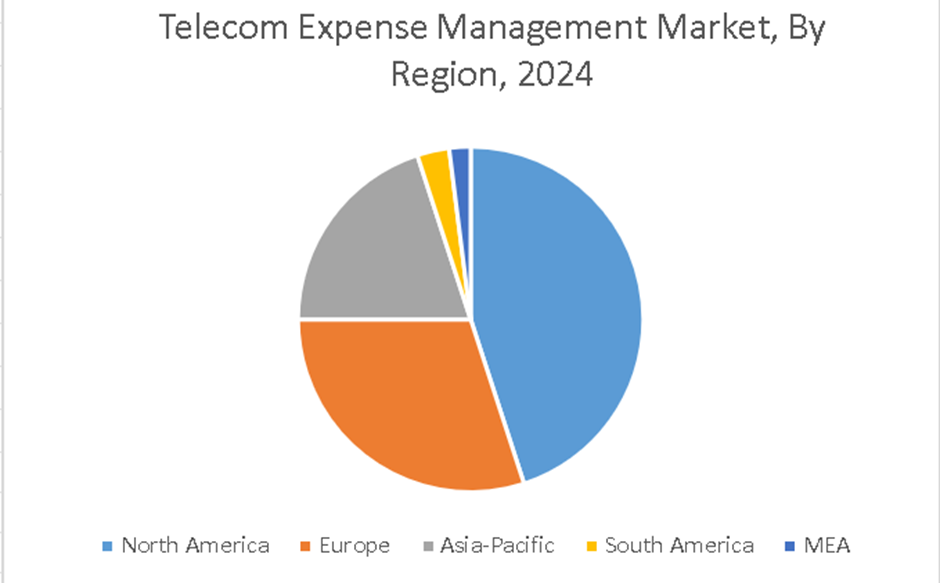

North America leads this market. North America (38% share), early cloud-TEM adoption, mature telecommunications networks, and strong per-capita mobile and device penetration all help the U. S. and Canada to dominate. The Asia-Pacific region is the fastest-growing region. Asia Pacific (CAGR of roughly 16%). Highest regional growth rates are being driven by rapid 5G rollouts, growing IoT deployments, and corporate digitalization in China, India, and Southeast Asia.

Europe has around 26% of the market share. Driven by GDPR-mandated audit trails, sophisticated multi-country carrier environments, and quick 5G and IoT installations in Germany, the UK, and the Nordics. South America offers about 11%. With around 11% of worldwide TEM expenditure, South America uses companies in Brazil and Argentina to control steep mobile‑data expenses and regulate prepaid‑plan complexity amid growing smartphone adoption. Middle East and Africa: about 5%. As Gulf Cooperation Council countries and South African companies use TEM to maximize growing 5G deployments and negotiate cross‑border operator contracts under diverse regulatory settings, MEA makes up around 5%.

COVID-19 Impact Analysis on the Global Telecom Expense Management Market:

The move to remote work and rise in digital cooperation tools increased businesses' telecom and UC&C expenses by 15–20% in 2020–21. Consequently, 42% of companies sped TEM deployments to get a real-time view into fast-increasing cloud-TELCO spending and to automatically audit invoices for recently granted mobile and collaboration licenses. This emphasis on cost control continued; many companies kept high TEM budgets to administer hybrid‑work telecoms portfolios and guarantee cost predictability amid current digital-transformation projects.

Latest Trends/ Developments:

Offering end‑to‑end visibility of communications expenses, TEM platforms now combine UC&C license tracking and QoS analysis.

For company mobile subscribers, app-based TEM agents offer real-time usage notifications and policy implementation.

To produce immutable billing records and simplify multi-party invoice reconciliation, some TEM providers are testing blockchain.

Without help from IT, drag-and-drop workflow builders let business users customize audit rules, alarms, and reporting dashboards.

Key Players:

• Accenture

• CGI Inc.

• WidePoint Corporation

• Tangoe

• Vodafone Group Plc

• AVOTUS

• Calero

• Sakon

• Upland Software, Inc.

• TeleManagement Technologies, Inc.

Chapter 1. Global Telecom Expense Management Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Telecom Expense Management Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Telecom Expense Management Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Telecom Expense Management Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Telecom Expense Management Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Telecom Expense Management Market- By Solution

6.1. Introduction/Key Findings

6.2. Dispute Management

6.3. Invoice Management

6.4. Ordering & Provisioning Management

6.5. Sourcing Management

6.6. Usage Management

6.7. Others

6.8. Y-O-Y Growth trend Analysis By Solution

6.9. Absolute $ Opportunity Analysis By Solution, 2025-2030

Chapter 7. Global Telecom Expense Management Market– By Service

7.1 Introduction/Key Findings

7.2. Managed Services

7.3. Professional Services

7.4. Y-O-Y Growth trend Analysis By Service

7.5. Absolute $ Opportunity Analysis By Service, 2025-2030

Chapter 8. Global Telecom Expense Management Market– By Deployment

8.1. Introduction/Key Findings

8.2. Cloud

8.3. On-premises

8.4. Y-O-Y Growth trend Analysis By Deployment

8.5. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 9. Global Telecom Expense Management Market– By Enterprise Size

9.1. Introduction/Key Findings

9.2. Large Enterprises

9.3. SMEs

9.4. Y-O-Y Growth trend Analysis By Enterprise Size

9.5. Absolute $ Opportunity Analysis By Enterprise Size, 2025-2030

Chapter 10. Global Telecom Expense Management Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Solution

10.1.3. By Service

10.1.4. By Deployment

10.1.5. By Enterprise Size

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Solution

10.2.3. By Service

10.2.4. By Deployment

10.2.5. By Enterprise Size

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Solution

10.3.3. By Service

10.3.4. By Deployment

10.3.5. By Enterprise Size

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Solution

10.4.3. By Service

10.4.4. By Deployment

10.4.5. By Enterprise Size

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Solution

10.5.3. By Service

10.5.4. By Deployment

10.5.5. By Enterprise Size

10.5.6. By Region

Chapter 11. Global Telecom Expense Management Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Accenture

11.2. CGI Inc.

11.3. WidePoint Corporation

11.4. Tangoe

11.5. Vodafone Group Plc

11.6. AVOTUS

11.7. Calero

11.8. Sakon

11.9. Upland Software, Inc.

11.10. TeleManagement Technologies, Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Telecom Expense Management Market was valued at USD 4.95 billion and is projected to reach a market size of USD 9.64 billion by the end of 2030 with a CAGR of 14.26%.

The Invoice Management segment is said to lead this market due to the priority given to accurate billing consolidation and automated auditing in order to avoid overcharges.

Managed Services center on implementation, system integration, and customizations; professional services concentrate on continuous operations (e.g., fraud monitoring, dispute resolution).

Cloud-based TEM reigns supreme (~62%) because it provides quick scalability, worldwide access, and SaaS-driven analytics; however, on-premise stays important in controlled industries.

Driven by quick 5G and business digitalization in China, India, and Southeast Asia, which spurs telecom‑cost visibility and optimization demand, Asia Pacific (about 16% CAGR) leads development.