Global Telecom Cloud Market Research Report – Segmentation by Component (Solution and Services); By Deployment (Private, Public, Hybrid); By Service (SaaS, PaaS, IaaS); By Application (Network, Data Storage and Computing, Traffic Management, Cloud Migration, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-10232

Format:

Region: Global

Market Size and Overview:

The Global Telecom Cloud Market was valued at USD 48.10 billion in 2024 and is projected to reach a market size of USD 125.38 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 21.12%.

The Telecom Cloud Market refers to the adoption of cloud computing technologies by telecommunication companies to enhance scalability, reduce infrastructure costs, and deliver more agile and efficient services. By migrating traditional network functions to the cloud, telecom operators can streamline operations, deploy new services faster, and meet the growing demands for high-speed connectivity and data processing. This market is rapidly evolving as 5G rollouts, edge computing, and IoT applications drive the need for more flexible, cost-effective, and reliable network infrastructure. Cloud-native solutions are now central to enabling digital transformation across the telecom industry, making the Telecom Cloud a strategic priority for service providers worldwide.

Key Market Insights:

The Telecom Cloud market is witnessing robust growth due to the rising adoption of 5G networks. Over 70% of telecom providers globally are shifting to cloud-native architectures to support the rollout of 5G services. This shift is driven by the need for low-latency, high-bandwidth capabilities and the flexibility to scale services based on real-time demand.

Telecom companies leveraging cloud infrastructure report faster service deployment times and improved network performance.

Network function virtualization (NFV) and software-defined networking (SDN) are also major contributors to market momentum. Studies show that telecom operators using NFV and SDN can reduce operational costs by up to 40% while improving service agility. These technologies allow telecom companies to replace costly hardware with software-driven network functions, which increases resource efficiency and accelerates innovation in service offerings.

The demand for hybrid and multi-cloud environments is surging, with nearly 60% of telecom enterprises adopting a combination of public and private clouds. This approach enhances data sovereignty, security, and workload optimization across regions. The rising emphasis on digital transformation, edge computing, and IoT integration continues to boost investment in telecom cloud infrastructure, making it a critical component of modern communication networks.

Telecom Cloud Market Drivers:

Growing Adoption of 5G Networks is Revolutionizing Telecom Cloud Integration

The rollout of 5G technology is one of the most significant catalysts for the expansion of the telecom cloud market. With its ultra-low latency, high bandwidth, and massive device connectivity, 5G requires telecom providers to shift away from legacy hardware-based systems toward agile, software-defined, and cloud-native infrastructures. This transformation enables faster network deployment, improved scalability, and greater flexibility in managing traffic loads. Telecom operators are increasingly leveraging cloud platforms to virtualize their core networks and support dynamic service delivery. The push for 5G also aligns with customer expectations for high-speed, uninterrupted connectivity, prompting providers to modernize their networks using robust and flexible cloud environments.

Rising Demand for Cost Efficiency and Network Virtualization is Driving Cloud Migration

Telecom providers face intense competition and pressure to reduce operational and capital expenditures, which has intensified the shift toward cloud-based solutions. Network Function Virtualization (NFV) and Software-Defined Networking (SDN) allow operators to replace expensive proprietary hardware with more affordable, scalable software solutions hosted in the cloud. This not only reduces infrastructure costs but also enhances service agility and network reliability. As a result, telecom companies are able to deploy new services faster, adjust resources based on demand, and scale operations without the burden of physical hardware upgrades. These economic advantages make cloud adoption a strategic priority for telecom businesses seeking long-term profitability.

Increasing Demand for Digital Services and IoT Connectivity Boosts Cloud Utilization

The explosion of digital services, including video streaming, online gaming, smart devices, and Internet of Things (IoT) applications, is placing unprecedented demand on telecom infrastructure. To handle this rise, operators are moving to the cloud to support real-time data processing, distributed architecture, and seamless connectivity across millions of devices. The cloud's ability to scale rapidly and manage vast data flows is essential for telecom providers aiming to offer consistent and high-quality digital experiences. Moreover, IoT-driven applications require edge computing and low-latency processing, both of which are effectively supported through integrated telecom cloud solutions, thereby reinforcing the cloud’s critical role in telecom evolution.

Strategic Partnerships and Technological Advancements are Accelerating Market Growth

Collaborations between telecom operators and major cloud service providers like AWS, Microsoft Azure, and Google Cloud are reshaping the industry landscape. These partnerships help telecoms gain access to advanced technologies, AI-driven analytics, and scalable infrastructure without massive internal investments. At the same time, the ongoing innovation in cloud-native software, container orchestration (e.g., Kubernetes), and automation tools is empowering telecom providers to enhance operational efficiency and reduce downtime. These advancements are enabling end-to-end network visibility, seamless orchestration, and faster time-to-market for new services—key advantages in an industry that is becoming increasingly digital and customer-centric.

Telecom Cloud Market Restraints and Challenges:

Data Security Concerns and Legacy Infrastructure Limit Widespread Cloud Adoption

Despite the numerous benefits of telecom cloud solutions, the market faces significant restraints due to persistent concerns over data security, regulatory compliance, and the complexity of integrating with existing legacy systems. Telecom operators handle vast volumes of sensitive customer data, and transitioning these operations to the cloud raises fears of potential breaches, data loss, and unauthorized access—particularly in regions with strict data protection laws. Moreover, many telecom companies still rely on traditional, hardware-based infrastructure that is difficult and costly to migrate to cloud environments. These legacy systems often lack compatibility with modern cloud-native architectures, creating operational disruptions and requiring substantial investment in reconfiguration and workforce training.

Telecom Cloud Market Opportunities:

The telecom cloud market presents immense opportunities driven by the growing demand for digital transformation, especially in emerging economies where telecom infrastructure is still evolving. As mobile and internet penetration continues to rise, telecom operators in these regions have the chance to leapfrog legacy systems and adopt scalable, cloud-native architectures from the start. Additionally, the increasing adoption of edge computing, AI-powered network optimization, and cloud-based customer engagement platforms offers telecom providers new revenue streams and operational efficiencies. With the shift toward virtualized network functions and the continued rollout of 5G, telecom companies can capitalize on cloud technologies to offer innovative, data-driven services, enhance user experience, and stay competitive in a rapidly evolving digital landscape.

Telecom Cloud Market Segmentation:

Market Segmentation: By Component:

• Solution

• Services

The Solution segment encompasses a wide range of cloud-based tools and platforms used by telecom operators to virtualize their networks, manage traffic, automate operations, and deliver digital services. This includes network function virtualization (NFV), software-defined networking (SDN), and other cloud-native solutions that help enhance flexibility, scalability, and cost-efficiency. As telecom companies continue to modernize their infrastructure, the need for innovative and customized solutions continues to rise, making this segment a vital contributor to market growth.

On the other hand, the Services segment plays a crucial role in enabling telecom providers to transition smoothly into cloud environments. These services include consulting, integration, maintenance, and support offerings that ensure effective deployment and management of telecom cloud infrastructure. With increasing reliance on cloud services, telecom operators are seeking expert assistance to align cloud strategies with business goals, manage operational risks, and ensure security compliance. Managed services, in particular, are gaining traction as they allow telecom companies to focus on core operations while outsourcing complex IT functions to specialized cloud providers. Both segments together fuel the telecom industry's shift toward a more agile and digitally-enabled ecosystem.

Market Segmentation: By Deployment:

• Private

• Public

• Hybrid

The Private deployment model dominates the telecom cloud market due to its enhanced security, control, and compliance features, which are critical for telecom operators handling sensitive customer data and mission-critical network functions. Private clouds provide a dedicated environment tailored to meet strict regulatory requirements, making them the preferred choice for large telecom enterprises and service providers focused on minimizing risks related to data breaches and ensuring high availability. The customization and control offered by private clouds also allow telecom companies to optimize performance and reliability, further reinforcing their dominance in sectors where data privacy is paramount.

Meanwhile, the Hybrid deployment model is witnessing the fastest growth as it combines the best of both private and public cloud environments. Hybrid clouds enable telecom operators to maintain sensitive workloads on private infrastructure while leveraging the scalability and cost-efficiency of public clouds for less-critical applications. This flexibility is especially valuable in managing dynamic traffic loads and accelerating the rollout of new services, making hybrid solutions ideal for telecom providers aiming to balance security with agility. The rapid adoption of hybrid cloud is fueled by the need to seamlessly integrate legacy systems with modern cloud technologies, providing a scalable and adaptable framework for ongoing digital transformation.

Market Segmentation: By Service:

• Software as a Service (SaaS)

• Platform as a Service (PaaS)

• Infrastructure as a Service (IaaS)

The Software as a Service (SaaS) segment holds a dominant position in the telecom cloud market, fueled by its ability to deliver ready-to-use applications that streamline network management, customer engagement, and billing processes. Telecom operators benefit from SaaS offerings because they reduce the need for extensive in-house IT resources, lower upfront costs, and enable rapid deployment of new services. These cloud-based applications are continually updated and maintained by providers, allowing telecom companies to focus on core business functions while ensuring access to the latest technological advancements. The convenience and efficiency of SaaS make it a preferred choice across various telecom operations, contributing significantly to its market dominance.

In contrast, the Platform as a Service (PaaS) segment is witnessing the fastest growth as telecom companies increasingly require customizable development platforms to build, test, and deploy new applications quickly. PaaS enables telecom providers to innovate by offering scalable environments that support the creation of network functions, IoT solutions, and analytics tools without worrying about underlying infrastructure management. This flexibility accelerates time-to-market and fosters agility in adapting to evolving customer demands and technological trends. As digital transformation intensifies, PaaS adoption is rising sharply, empowering telecom operators to differentiate themselves through innovative, cloud-native services.

Market Segmentation: By Application:

• Network, Data Storage & Computing

• Traffic Management

• Cloud Migration

• Others

The Network, Data Storage & Computing segment dominates the telecom cloud market, as it forms the backbone of telecom infrastructure modernization. Telecom operators rely heavily on cloud-based network solutions to virtualize their core systems, enhance data storage capabilities, and boost computing power. This segment’s dominance is driven by the growing demand for scalable, efficient, and flexible network operations that can support increasing data traffic, 5G rollouts, and edge computing initiatives. By leveraging cloud technologies, telecom companies can optimize resource utilization, reduce operational costs, and accelerate service delivery, solidifying this segment’s leading position in the market.

Meanwhile, the Traffic Management segment is witnessing the fastest growth due to the surging demand to handle massive volumes of real-time data generated by mobile devices, IoT networks, and digital services. Efficient traffic management solutions powered by cloud platforms help telecom providers monitor, control, and optimize network traffic to ensure high-quality user experiences and avoid congestion. The rise in data-intensive applications and smart devices is driving telecom operators to adopt advanced cloud-based traffic management tools rapidly, positioning this segment for accelerated expansion in the near future.

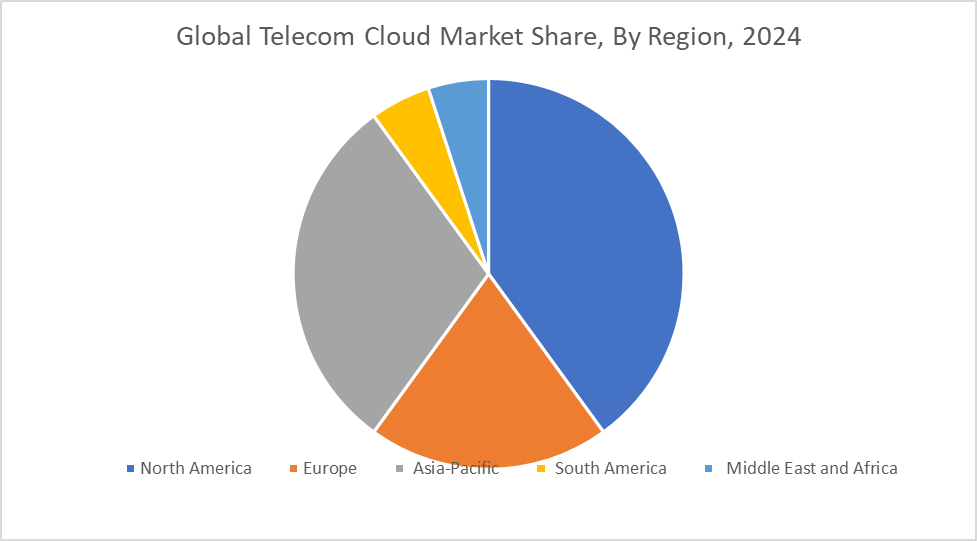

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is the dominant region in the telecom cloud market, commanding the largest share due to its advanced telecommunications infrastructure, early adoption of cloud technologies, and presence of major telecom service providers and cloud vendors. The region benefits from substantial investments in 5G networks, edge computing, and digital transformation initiatives, which drive the demand for telecom cloud solutions. Additionally, stringent data security regulations and strong government support further reinforce North America’s leadership position in the market.

Asia-Pacific is the fastest-growing region in the telecom cloud market, driven by rapid digitalization, increasing mobile and internet penetration, and the expansion of telecom infrastructure across emerging economies such as India, China, and Southeast Asian countries. The surge in demand for cost-effective and scalable cloud solutions among telecom operators, coupled with government initiatives promoting smart cities and digital services, accelerates cloud adoption.

COVID-19 Impact Analysis on the Global Telecom Cloud Market:

The COVID-19 pandemic acted as a catalyst for accelerating cloud adoption in the telecom industry. With a sudden rise in remote work, digital communication, and internet usage, telecom operators turned to cloud solutions to manage increased network demand, enhance service reliability, and maintain operational continuity. The crisis highlighted the need for scalable, agile, and resilient infrastructure, prompting a shift from legacy systems to cloud-based platforms. This transformation not only addressed immediate challenges but also laid the groundwork for long-term growth and innovation in the telecom cloud market.

Latest Trends/ Developments:

One of the latest trends in the telecom cloud market is the rising integration of AI and machine learning into cloud platforms to optimize network management and service delivery. Telecom companies are using AI-driven insights for predictive maintenance, traffic routing, and customer behavior analysis. This not only enhances operational efficiency but also enables more personalized user experiences. Additionally, the rise of edge computing is reshaping cloud architecture by bringing data processing closer to users, reducing latency and improving real-time data handling for applications like IoT and 5G.

Another key development is the increasing collaboration between telecom operators and cloud service providers. Strategic partnerships are being formed to co-develop next-generation cloud infrastructure tailored for telecom needs. These alliances focus on accelerating 5G rollouts, enhancing virtual network functions, and launching cloud-native platforms that offer greater scalability and automation. At the same time, there is a rising emphasis on multi-cloud and hybrid deployment models, giving telecom providers more flexibility, control, and security over their cloud environments.

Key Players:

• Juniper Networks, Inc.

• IBM Corporation

• Mavenir

• Metaswitch Network

• Affirmed Networks

• Fortinet

• Orange

• Huawei Technologies Co., Ltd.

• VMWare

• Cisco

• Nokia

• Ericsson

Chapter 1. Global Telecom Cloud Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Telecom Cloud Market – Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Telecom Cloud Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Telecom Cloud Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Telecom Cloud Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Telecom Cloud Market – By Component

6.1. Solution

6.2. Services

6.3. Y-O-Y Growth trend Analysis By Component

6.4. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global Telecom Cloud Market – By Deployment

7.1. Private

7.2. Public

7.3. Hybrid

7.4. Y-O-Y Growth trend Analysis By Deployment

7.5. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 8. Global Telecom Cloud Market – By Service

8.1. Software as a Service (SaaS)

8.2. Platform as a Service (PaaS)

8.3. Infrastructure as a Service (IaaS)

8.4. Y-O-Y Growth trend Analysis By Service

8.5. Absolute $ Opportunity Analysis By Service, 2025-2030

Chapter 9. Global Telecom Cloud Market – By Application

9.1. Network, Data Storage & Computing

9.2. Traffic Management

9.3. Cloud Migration

9.4. Others

9.5. Y-O-Y Growth trend Analysis By Application

9.6. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 10. Global Telecom Cloud Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Deployment

10.1.4. By Service

10.1.5. By Application

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Deployment

10.2.4. By Service

10.2.5. By Application

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Deployment

10.3.4. By Service

10.3.5. By Application

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Deployment

10.4.4. By Service

10.4.5. By Application

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Deployment

10.5.4. By Service

10.5.5. By Application

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Telecom Cloud Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1 Juniper Networks, Inc.

11.2 IBM Corporation

11.3 Mavenir

11.4 Metaswitch Network

11.5 Affirmed Networks

11.6 Fortinet

11.7 Orange

11.8 Huawei Technologies Co., Ltd.

11.9 VMWare

11.10 Cisco

11.11 Nokia

11.12 Ericsson

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Telecom Cloud Market was valued at USD 48.10 billion in 2024 and is projected to reach a market size of USD 125.38 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 21.12%.

Rising 5G deployment, digital transformation, and demand for scalable telecom infrastructure are key drivers of the global telecom cloud market.

Based on Service Provider, the Global Telecom Cloud Market is segmented into SaaS, PaaS, IaaS.

North America is the most dominant region for the Global Telecom Cloud Market.

Juniper Networks, Inc., IBM Corporation, Mavenir are the leading players in the Global Telecom Cloud Market.