Global Storage Area Artificial Intelligence Network Market Research Report – Segmentation By Offering (Hardware, Software), By Storage Architecture (File Storage, Object Storage, Block Storage, Hybrid Storage), By Storage Medium (HDD, SSD), By End-Use Industry (Telecommunication, Cloud Software Provider, Government Bodies, Branding & Advertising, Others), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16523

Format:

Region: Global

Market Size and Overview:

The Global Storage Area Artificial Intelligence Network Market was valued at USD 5 billion and is projected to reach a market size of USD 10 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 14.87%.

Rapid data growth, cloud adoption, and the need for smart storage orchestration all propel this expansion. Real-time performance monitoring, predictive maintenance, and self-healing storage networks depend on AI-powered SAN solutions as companies adopt cloud-native architectures and GenAI workloads. To solve the soaring volumes of unstructured and structured data generated by IoT, 5G, and edge-computing settings, AI-enabled SAN solutions leverage machine-learning and deep-learning algorithms to optimize data placement, automate tiering, and predict hardware failures. AI-powered SAN solutions are progressively used in telecommunications, cloud-service providers, and corporate data centers to guarantee performance, resilience, and cost efficiency as data-intensive applications like GenAI seek ultra-low-latency access and dynamic scaling.

Key Market Insights:

Reflecting strong investment in AI orchestration and analytics modules, the software segment earned USD 6,818.2 million in revenues and will reach USD 28,105.7 million by 2030 at a 27.3% CAGR.

Driven by national AI-data-center projects, South Korea is predicted to have the fastest regional CAGR through 2030, whereas North America had the biggest share in 2024 because of old data-center infrastructure.

Though hybrid storage is the fastest-growing, combining on-premise and cloud levels to match cost and scalability, block storage continues to be the most common architecture for high-performance workloads.

While cloud-software companies are the quickest expanding end customers integrating AI-SAN to automate multi-tenant storage solutions, the telecommunications companies segment drives adoption by deploying AI-SAN to enable 5 G-backhaul networks.

Storage Area Artificial Intelligence Network Market Drivers:

The use of real-time analytics and the exponential growth of data drive the need for this market.

Emerging GenAI services, IoT devices, and social media are driving the world's data footprint, global data creation jumped from 64.2 ZB in 2020 to an estimated 181 ZB by 2025. A fleet of enterprise apps will surely follow. AI-powered SAN systems ingest telemetry from storage arrays, network fabric, and host workloads, using real-time analytics to continuously reorganize data placement and I/O paths, therefore avoiding hot-spot bottlenecks and maintaining end-to-end latencies below 1 ms for mission-critical applications.

Advanced telemetry, such as per-volume queue depths and dynamic QLC/TLC wear metrics, feeds machine-learning models that predict capacity thresholds and automatically trigger tier-migration policies moments before performance degrades. Fewer FTEs are achieved as edge and 5G workloads drive data to geo-distributed micro-data centers. This constant feedback loop replaces manual tuning, therefore enabling storage architects to manage petabyte-scale estates. AI-driven SAN analytics guarantee consistent QoS across thousands of nodes, scaling linearly with data development and driving the adoption of intelligent storage orchestration across every industry.

The rise in the popularity of cloud and virtualization is driving the growth of this market.

Powered by cloud-first virtualization trends, the global AI-powered storage market is predicted to reach USD 66.5 billion by 2028 at a 24.5% CAGR, therefore transforming storage with a pivot to cloud-native and hyperconverged infrastructures (HCI). Compute and storage meet at the same nodes in HCI settings, which creates tightly linked resource pools that require AI-driven orchestration to optimize VM placement, balance I/O loads, and automate tiering across NVMe and HDD backends. KVB Research notes that AI-SAN orchestration can cut manual policy configurations by 70%, while reducing operating expenses by up to 30% through smart cold-data offloading to object-storage tiers. AI agents continuously check latency distributions and proactively modify replication ratios to meet five-nines availability SLAs as companies run hundreds of micro-VMs for containerised services. Virtualization at scale, which drives cloud migrations and increasingly broadens the AI-SAN addressable market, depends on this desire for independent storage management.

Due to its high accuracy level, this market is gaining popularity, being a major market driver.

With an estimated USD 300,000 in downtime every hour, hardware failures account for over 50% of unplanned storage outages. AI-enabled SAN solutions predict component degradations, such as media wear, controller memory errors, and fan-speed anomalies, with up to 90% accuracy by employing supervised-learning models trained on millions of SMART telemetry data points. Early adopters in telecom and hyperscale settings claim self-healing routines cut unplanned outages by 40%. These forecasts activate automated processes that elegantly move data off at-risk drives, replacing spare nodes and rebalancing erasure-coding groups without human intervention. By avoiding reactive rebuild storms, this feature not only cuts maintenance windows but also extends hardware lifecycles—thereby transforming SAN operations from break-fix to proactive resilience and supporting the value offer of AI-augmented storage networks.

The rise in the demand for performance from the AI/ML workloads is driving the need for this market.

Large language and picture models, especially big language and vision models, can produce sustained I/O loads exceeding 1 GB/s per GPU and peaks of over 200,000 IOPS in random-access patterns. AI-SAN systems guarantee that "hot" parameter tensors and feature maps are staged on ultra-low-latency NVMe levels while cold checkpoints reside on high-capacity HDD arrays by integrating real-time cache-hit analytics and dynamic prefetching. Benchmarks show these systems deliver 2–3× faster throughput for GPU-accelerated training compared to traditional tiering schemes, shortening model-train times by up to 50%. Inference at scale, such as real-time recommendation engines, benefits from AI-powered QoS engines that isolate tenant workloads and throttle noisy neighbors, guaranteeing sub-millisecond tail latencies. The need for smart SAN orchestration for consistent performance becomes a major motivation for AI-SAN acceptance as companies add more AI services into production.

Storage Area Artificial Intelligence Network Market Restraints and Challenges:

High cost of implementation is considered a big market challenge as it reduces its affordability.

Further inflating costs, companies spend significantly on NVMe SSD arrays, priced at USD 2–$4 per gigabyte to obtain the low latencies AI demands. Compared to USD 1.5 trillion for conventional workloads, a recent McKinsey study projects that AI-ready data centers would need USD 5.2 trillion in capital investments by 2030. Licensing proprietary AI orchestration software and analytics tools adds yet another layer of cost, as enterprise software subscriptions can easily top USD 200,000 yearly per petabyte of managed storage. For mid-market companies, total deployment costs including compute, storage, networking, and software could top USD 1 million, a significant obstacle preventing market penetration outside of hyperscale and big corporate sectors.

It is challenging for the latest technologies to be integrated with the existing ones, making it a big challenge for the market.

Although only 15% of AI-SAN systems provide uniform orchestration APIs, forcing 28% of IT teams to undertake weekly manual reconciliations between storage controllers and virtualization layers, Storage Area Networks are inherently heterogeneous, including multi-vendor arrays, varied hypervisor platforms, and legacy management tools. Custom CLI interfaces, vendor-specific SNMP MIBs, and proprietary protocols (e.g., Fibre Channel versus iSCSI) demand bespoke middleware or adapter layers—projects with professional-services costs ranging from $100,000 to $250,000 and typically spanning 6–12 months. Integration with corporate ITSM and AIOps systems is made more difficult by the absence of common data models for telemetry and performance metrics, therefore reducing the expected automation advantages. Even hyperscalers find handling multi-cloud storage orchestration challenging: a GSMA report states service providers spend 20–30% of network-operations staff time on manual storage-network configuration and troubleshooting. This integration load not only slows time-to-value but also raises TCO from continual connector maintenance and version-compatibility modifications.

There is a high risk of data leaks hampering the growth potential of the market.

Under rules like GDPR, HIPAA, and PCI DSS, AI-powered SANs handle sensitive business, personal, and controlled data, thereby activating strict supervision. Only 45% of AI-SAN deployments, however, expose data to intercept risks by enforcing AES-256 encryption at rest and in transit. Maintaining explainable AI (XAI) models for audit trails is essential under GDPR’s right-to-explanation provisions require additional logging, versioning, and metadata-capture capabilities, increasing storage and processing overhead by 15–20%. Compliance validation adds USD 50,000–150,000 per year in external audit and legal fees for Fortune 500 SAN deployments. Moreover, cross-border data-sovereignty mandates force some organizations to provision on-premise or localized SAN clusters, raising CAPEX and fragmenting global data estates. As legal and IT teams negotiate data-use agreements and encryption standards, this confluence of security requirements and regulatory complexity increases operational risk and can postpone AI-SAN rollouts by three to six months.

A skill gap between AI and storage slows down the operations of the market.

Effective AI-SAN management calls for a unique mix of machine-learning expertise and deep storage-architecture knowledge skills that are in short supply. 65% of IT teams lack in-house competence for AI-SAN deployments, according to a 2024 IDC survey, which leads to lengthy proof-of-concept processes and over-reliance on outside experts. Universities and professional organizations rarely address the intersection of storage networks and AI ops, therefore, recent graduates are ill-equipped for the complexity of the field. Upskilling current employees gives businesses a 6–9 month learning curve to certify engineers in SAN-specific AI models and data-placement algorithms. With external consultancy charges of USD 200–350 per hour, this talent deficit increases labor costs and may extend implementation schedules beyond one year for big projects. Though at a 20–30% premium over self-managed solutions, many companies choose managed-service models or SAN-as-a-service products to close the skills gap.

Storage Area Artificial Intelligence Network Market Opportunities:

The proliferation of Edge-AISAN Solutions has increased the demand for this market.

Driven by 5G rollouts and Industry 4.0 initiatives, edge computing is proliferating, which is generating demand for small Storage Area Network devices with on-device AI inference that allows localised data processing on factory floors and telco base stations. These edge-AI SAN devices help companies keep operational continuity when connectivity is sporadic by processing data locally, cutting WAN bandwidth costs by up to 60%, lowering latency to under 1 ms, and maintaining operational continuity. By integrating machine-learning algorithms directly into storage controllers, vendors such as Lanner and Arrcus are working to provide turnkey edge-AI SAN solutions with GPU acceleration and optimized power profiles, targeting telco and industrial IoT use cases. Early tests at manufacturing sites have shown 30% improvements in real-time defect detection and 25% reductions in unplanned downtime via on-premise predictive maintenance. Edge-AI SAN provides a scalable model as hyperscale data center workloads decentralize, allowing enterprises to deploy hundreds of micro-SAN nodes managed through a unified AI orchestration layer.

The adoption of SSD and NVMe is expected to grow at a higher rate, improving the efficiency of the market.

Given that companies want sub-millisecond access to "hot" datasets, NVMe adoption in data centers is projected to exceed 70% by 2026, underpinning quicker AI inference and training from HDD to NVMe SSDs in SAN arrays. Supporting high-concurrency AI applications without storage I/O constraints, NVMe drives provide up to 14 GB/s read throughput and 10 GB/s write rates on PCIe Gen5 connections. In GPU-accelerated clusters, AI-SAN platforms use NVMe-based caching layers to pre-stage huge model checkpoints straight from slower HDD levels, hence cutting training time by 50% and inference latency by 40%. Offering multi-namespace capability and superior telemetry via NVMe-MI, companies like Innodisk are debuting high-capacity (128 TB) Gen5 NVMe SSDs tuned for AI and big-data analytics.

The integration of SDS with AI engines will help businesses in defining the high-level policies.

By separating control-plane intelligence from physical equipment, software-defined storage (SDS) systems enable AI-SAN solutions to manage data placement, replication, and tiering across on-premise and multi-cloud environments. Businesses can specify high-level rules, such as “keep machine-learning datasets on flash for 24 hrs post-training” by combining AI engines with SDS layers, and the system will manage dynamic data movement automatically. Using policy-driven strategies, hybrid-cloud solutions let companies use on-prem NVMe for low-latency tasks and public-cloud object storage for archival data without manual intervention. KVB Research projects that AI-integrated SDS deployments would rise at a 28% CAGR through 2030, propelled by demand for unified management of heterogeneous storage topologies. Leading SDS suppliers—such as DataCore's SANsymphony—are embedding AI modules to negotiate I/O patterns and proactively redistribute workloads during peak usage periods.

The adoption of this market will help in the optimization of GenAI workload, being a great market growth opportunity.

With training tasks writing terabytes of intermediate data per epoch, the fast uptake of Generative AI (GenAI) models, such as big language models (LLMs) and diffusion-based picture generators, places hitherto unheard-of demands on SAN performance and QoS. Automatic tuning of storage Qo2 parameters and pre-warming cache layers for frequently accessed model weights can cut end-to-end training times by 30–40% in AI-SAN solutions. To optimize GPU utilization and minimize wasted cycles, Microsoft’s DeepSpeed ZeRO-Inference offloads kv-cache to NVMe SSDs and modifies GPU-to-storage data paths. Additionally, NVIDIA’s GPUDirect Storage avoids CPU buffers to quicken data transfers straight between GPUs and SSDs, resulting in up to 4× throughput increases for large-model inference. AI-SAN orchestration guarantees data locality as hyperscalers deploy dispersed training across geo-spread clusters, co-locating model shards on the closest storage nodes to reduce network hops and maintain sub-1 ms latencies. For production deployments of chatbots and real-time AI solutions, where any latency spike might impair user experience and breach SLA obligations, this capacity is crucial.

Storage Area Artificial Intelligence Network Market Segmentation:

Market Segmentation: By Offering

• Hardware

• Software

The Software segment dominates the market, with USD 6,818.2 million generated in 2024. The AI-SAN software segment has the biggest share of the market owing to the great need for AI orchestration, analytics, and management components. The Hardware segment is the fastest-growing segment. This segment includes NVMe SSD arrays, GPU-accelerated controllers, and specialized ASICs. It is the fastest-growing as companies replace storage systems to enable real-time AI inference and high-throughput analytics workloads.

Market Segmentation: By Storage Architecture

• File Storage

• Object Storage

• Block Storage

• Hybrid Storage

The Block Storage segment dominates the market because it has the largest market share due to low latency and high IOPS, making it important for AI-driven SAN deployments. The Hybrid Storage segment is the fastest-growing segment. Hybrid storage mixes on-premise high-performance tiers with cloud-based capacity tiers are the fastest-growing architecture under AI orchestration policies, allowing dynamic tiering and cost optimization.

Growing at a 22.5% CAGR as businesses progressively store and index unstructured data (documents, media) on AI-optimized SAN systems, the file-storage sector generated USD 5,400.0 million in revenues in 2024 and is forecast to reach USD 17,659.3 million by 2030. Ideal for large, unstructured data sets in cloud-native environments, object storage, which comprises about 26% of SAN AI-network revenues in 2024, is set to expand at more than 23% CAGR driven by demand for scalable metadata management and artifact versioning in AI/ML workflows.

Market Segmentation: By Storage Medium

• HDD

• SSD

Here, the HDD segment dominates the market. Given its lower cost per terabyte and ongoing usage in archival and compliance storage levels, HDD continues to be the preferred medium for cold and bulk data. The SSD segment is said to be the fastest-growing segment here, as AI-SAN solutions use NVMe and flash for high-speed caching and persistent memory, fulfilling the ultra-low-latency demands of GenAI and real-time analytics. SSD is the fastest-growing medium.

Market Segmentation: By End-Use Industry

• Telecommunication

• Cloud Software Provider

• Government Bodies

• Branding & Advertising

• Others

The Telecommunication segment dominates this market, as they are deploying AI-SAN to manage 5 G networks. The Cloud Software Provider segment is said to be the fastest-growing segment in the market as the cloud software providers are incorporating AI-SAN into multi-tenant systems to automatically provide storage provisioning, QoS tuning, and billing for many client workloads.

With national data-sovereignty projects speeding up, public-sector agencies are using AI-SAN solutions for e-government portals, citizen-data services, and critical-infrastructure monitoring. With an expected USD 1,200 million in 2024 and a 24% CAGR increase through 2030. With real-time bidding, campaign analysis, and rich-media delivery, this segment generated around USD 1,450 million in revenues in 2024 and is on track for a 25.8% CAGR as ad platforms demand ultra-low-latency storage for high-volume creative assets. With USD 3,000 million revenues and a 20.5% CAGR growth rate as companies across BFSI, retail, education, healthcare, and other sectors embrace AI-SAN for specialized analytics, compliance archives, and hybrid-cloud storage solutions, 'others' (including BFSI, retail, education, healthcare) will become increasingly important.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

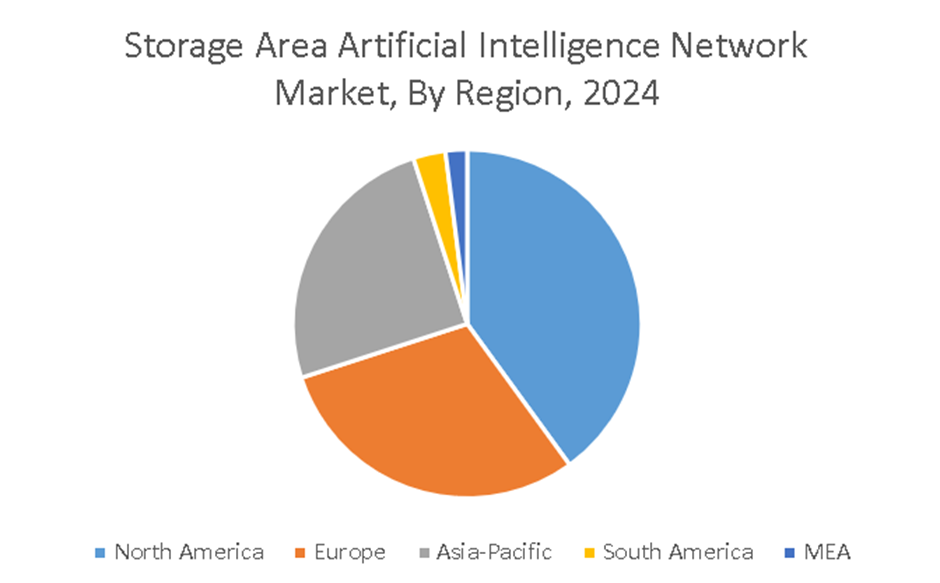

North America again dominates this market, as it accounts for the largest market share, which is due to mature data center infrastructure, early deployment of AI-SAN, and a high level of expenditure in the field of R&D. The Asia-Pacific region is said to be the fastest-growing segment in the market. Driven by government smart-data initiatives, 5G rollouts, and AI-enabled data center investments, the Asia Pacific region is predicted to record the highest CAGRs till 2030.

With expected revenues of USD 4,091.5 million in 2024 and USD 14,629.8 million by 2030 at a 24.3% CAGR, Europe's AI-SAN market is driven by strong investment in AI data centers in the UK, Germany, and the Nordics. Driven by public-sector modernization and increasing telecom backbones, the South America AI-SAN market (including Brazil, Argentina, and Chile) generated roughly USD 1,634.5 million in 2024 and is projected to expand at a 24.2% CAGR through 2030. With markets like UAE (USD 372.3 million) and Saudi Arabia leading, the MEA area recorded USD 1,257.2 million in AI-SAN revenues in 2024; under government smart-city and 5G data-hub initiatives, the region is expected to develop at 23.5% CAGR through 2030.

COVID-19 Impact Analysis on the Global Storage Area Artificial Intelligence Network Market:

As businesses turned to remote operations and digital services, the epidemic accelerated demand for AI-powered Storage Area Network (SAN) solutions dramatically. First, lockdowns and social-distancing mandates drove a 13.7% growth in cloud storage demand in 2020, up from 9.3%, prompting SAN vendors to integrate AI-driven tiering and predictive-caching features into their cloud offerings. Remote work surges strained legacy SAN infrastructures, leading 73% of enterprises to prioritize cloud migration and cost-optimization initiatives, thereby boosting AI orchestration module uptake.

Latest Trends/ Developments:

AI models currently 60% cut manual configuration by automating sophisticated storage setups and performance tuning in real time.

Emerging edge and telco use cases are small SAN devices with embedded artificial intelligence that allow localised analytics and autonomy.

Self-diagnosis and repair processes replacing failing disk parts automatically enhance uptime to 99.999% and are part of AI-SAN solutions.

Integration of blockchain guarantees unchangeable audit trails for data access and AI-model decisions, therefore improving compliance in controlled sectors.

Key Players:

• IBM

• Intel Corporation

• NVIDIA Corporation

• Samsung

• Microsoft Corporation

• SAP

• Hitachi Vantara

• NetApp

• Oracle

• Lenovo

Chapter 1. Global Storage Area Artificial Intelligence Network Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Storage Area Artificial Intelligence Network Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Storage Area Artificial Intelligence Network Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Storage Area Artificial Intelligence Network MarketEntry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Storage Area Artificial Intelligence Network Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Storage Area Artificial Intelligence Network Market– By Offering

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Y-O-Y Growth trend Analysis By Offering

6.5. Absolute $ Opportunity Analysis By Offering, 2025-2030

Chapter 7. Global Storage Area Artificial Intelligence Network Market– By Storage Architecture

7.1. Introduction/Key Findings

7.2. File Storage

7.3. Object Storage

7.4 Block Storage

7.5 Hybrid Storage

7.6. Y-O-Y Growth trend Analysis By Storage Architecture

7.7. Absolute $ Opportunity Analysis By Storage Architecture, 2025-2030

Chapter 8. Global Storage Area Artificial Intelligence Network Market– By Storage Medium

8.1. Introduction/Key Findings

8.2. HDD

8.3. SSD

8.4. Y-O-Y Growth trend Analysis By Storage Medium

8.5. Absolute $ Opportunity Analysis By Storage Medium, 2025-2030

Chapter 9. Global Storage Area Artificial Intelligence Network Market– By End-Use Industry

9.1. Introduction/Key Findings

9.2. Telecommunication

9.3. Cloud Software Provider

9.4 Government Bodies

9.5 Branding & Advertising

9.6 Others

9.7. Y-O-Y Growth trend Analysis By Storage Medium

9.8. Absolute $ Opportunity Analysis By Storage Medium, 2025-2030

Chapter 10. Global Storage Area Artificial Intelligence Network Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Offering

10.1.3. By Storage Architecture

10.1.4. By Storage Medium

10.1.5 By End-Use Industry

10.1.6 By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Offering

10.2.3. By Storage Architecture

10.2.4. By Storage Medium

10.2.5 By End-Use Industry

10.2.6 By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Offering

10.3.3. By Storage Architecture

10.3.4. By Storage Medium

10.3.5 By End-Use Industry

10.3.6 By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Offering

10.4.3. By Storage Architecture

10.4.4. By Storage Medium

10.4.5 By End-Use Industry

10.4.6 By Region

10.5. Middle East & Africa

9.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Offering

10.5.3. By Storage Architecture

10.5.4. By Storage Medium

10.5.5 By End-Use Industry

10.5.6 By Region

Chapter 11. Global Storage Area Artificial Intelligence Network Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. IBM

11.2. Intel Corporation

11.3 NVIDIA Corporation

11.4 Samsung

11.5 Microsoft Corporation

11.6 SAP

11.7 Hitachi Vantara

11.8 NetApp

11.9 Oracle

11.10 Lenovo

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Storage Area Artificial Intelligence Network Market was valued at USD 5 billion and is projected to reach a market size of USD 10 billion by the end of 2030 with a CAGR of 14.87%.

Thanks to investments in AI orchestration and analytics tools, the software sector with USD 6,818.2 million revenues in 2024 will lead, but the hardware sector is the fastest expanding one as GPU-accelerated storage arrays for real-time AI workloads and NVMe SSDs rapidly invade the market, driving its development.

Supported by developed data-center infrastructure and early AI-SAN implementations, North America had the biggest regional share in 2024. Driven by national AI data-center projects and 5 G-backhaul needs, the Asia-Pacific region is expected to have the highest regional CAGR until 2030.

Dynamic tiering, which employs AI to automatically transfer "hot" data to high-performance NVMe levels, maximizes performance and cost; predictive maintenance, in which machine-learning models predict hardware failures to lower unplanned downtime by up to 40%, is among the important applications.

High implementation costs (up to USD 1 million for large-scale AI-SAN deployments), integration difficulty across varied storage arrays (causing 28% of users to perform weekly manual reconciliations), and a skill gap, with 65% of IT teams lacking in-house AI-SAN expertise constitute major barriers requiring external consulting and lengthening deployment schedules.