Global Social Commerce Market Research Report – Segmentation by Business Model (B2B, B2C, C2C); By Product (Personal & Beauty Care, Apparels, Accessories, Home Product, Health Supplements, Food & Beverage, Others); By Type (Laptops and PCs, Mo-bile, Tablets, E-readers, Internet – enabled TVs, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9485

Format:

Region: Global

Market Size and Overview:

The Global Social Commerce Market was valued at USD 1262.19 billion in 2024 and is projected to reach a market size of USD 6241.96 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 37.67%.

The social commerce market refers to the intersection of social media and e-commerce, where users can discover, evaluate, and purchase products directly within social platforms. This emerging sector has revolutionized the way consumers interact with brands and make buying decisions, shifting the shopping experience from traditional websites to more interactive and community-driven environments. Unlike conventional online shopping, social commerce integrates features like likes, shares, comments, influencer recommendations, and real-time interactions, creating a more engaging and trust-based shopping journey. The rise of social commerce is largely fueled by the widespread use of smartphones and the increasing amount of time people spend on platforms like Instagram, Facebook, TikTok, and Pinterest. These platforms have evolved into powerful marketing and selling tools, enabling businesses to target potential customers with personalized content and streamlined purchasing options without redirecting them to external websites.

Key Market Insights:

Social commerce is witnessing a rapid shift in consumer behavior, with over 70% of online shoppers now influenced by social media platforms in their purchasing decisions. Visual content, influencer endorsements, and real-time engagement have become powerful tools in shaping buyer preferences. Platforms like Instagram and TikTok have seen a significant rise in product discovery, with nearly 60% of Gen Z users discovering new brands through social feeds alone.

Another major trend is the growing role of influencers and content creators in driving sales. Micro and nano influencers, in particular, are gaining traction due to their high engagement rates and stronger personal connections with followers. Reports indicate that influencer-driven commerce can result in up to 5x higher conversion rates compared to traditional digital advertising, highlighting the growing trust consumers place in peer recommendations.

User-generated content and live shopping are also playing a critical role in enhancing purchase confidence. Around 80% of shoppers claim they are more likely to buy a product if they see photos or videos from real users. Similarly, live commerce—where products are showcased in real time with interactive Q&A—has seen high participation rates in markets across Asia and is steadily gaining momentum in other regions as a new form of immersive shopping.

Social Commerce Market Drivers:

Social Media Penetration and Engagement Are Powering Seamless Shopping Experiences

The widespread use of social media platforms has created a natural environment for social commerce to flourish. With billions of users actively engaging on platforms like Instagram, TikTok, Facebook, and Pinterest, brands are leveraging these spaces to reach consumers where they spend most of their digital time. These platforms offer visually rich content, stories, reels, and short videos that not only entertain but also inspire buying decisions. The blend of entertainment and commerce reduces the gap between discovery and purchase, making it easier for consumers to buy products with just a few clicks without leaving the app.

Influencer and Creator Economy Is Transforming Digital Word-of-Mouth Marketing

Influencers and content creators have become vital in shaping consumer preferences and brand trust. Their authentic product reviews, lifestyle integrations, and relatable content build emotional connections with followers. This creator-driven commerce is more than just marketing—it's social proof at scale. Unlike traditional ads, influencer content feels personal and organic, which resonates especially well with younger audiences. As a result, consumers are increasingly buying based on influencer recommendations, contributing significantly to the success of social commerce campaigns.

Increased Trust in Peer Recommendations and User-Generated Content Drives Conversions

Today’s consumers are more likely to trust real users over brand messages. User-generated content—such as reviews, unboxing videos, and testimonials—has become a key factor in purchase decisions. Seeing everyday people use and enjoy products creates a sense of authenticity and reliability that traditional marketing often lacks. This peer-driven validation plays a huge role in reducing buyer hesitation and increasing conversions, as customers feel more confident when others in their community endorse a product.

Technological Advancements and In-App Shopping Features Enhance User Convenience

Social media platforms are constantly evolving to integrate more advanced shopping tools, from shoppable posts and product tagging to AI-powered recommendations and augmented reality (AR) try-ons. These innovations simplify the purchase process, allowing users to explore, evaluate, and buy products without leaving the app. The seamless integration of technology not only improves user experience but also encourages impulse buying, making social commerce a frictionless and efficient way to shop in today’s fast-paced digital environment.

Social Commerce Market Restraints and Challenges:

Privacy Concerns, Trust Issues, and Platform Limitations Pose Key Challenges

Despite its rapid growth, the social commerce market faces remarkable restraints, primarily related to data privacy concerns, counterfeit products, and the limitations of platform infrastructure. Consumers are becoming increasingly cautious about how their personal data is collected and used by social media platforms, which can hinder their willingness to shop directly through these channels. Additionally, the rise of fake reviews, fraudulent sellers, and lack of standardized return policies can erode trust and affect buyer confidence. Many platforms also struggle to provide a consistent end-to-end shopping experience, especially across different regions and devices, which can disrupt the seamless flow social commerce aims to deliver. These challenges must be addressed to ensure sustainable growth and consumer trust in the evolving digital commerce space.

Social Commerce Market Opportunities:

The social commerce market holds vast opportunities driven by the surge of the creator economy, advancements in artificial intelligence, and the growing demand from emerging digital markets. As more content creators and influencers monetize their platforms, brands have new and highly engaging channels to connect with niche audiences. AI-driven tools like personalized recommendations, chatbots, and virtual try-ons enhance user experience and streamline shopping journeys. Additionally, large populations in regions like Southeast Asia, Latin America, and Africa are rapidly coming online, presenting untapped potential for social commerce growth. These factors collectively open doors for businesses to innovate, scale, and reach consumers in ways traditional e-commerce cannot.

Social Commerce Market Segmentation:

Market Segmentation: By Business Model:

• Business to Business (B2B)

• Business to Consumer (B2C)

• Consumer to Consumer (C2C)

The Business to Consumer (B2C) segment holds dominance in the social commerce market because of its wide reach, scalability, and direct engagement with customers. Most social platforms are built around consumer interactions, making them ideal for B2C transactions where brands showcase products through influencer partnerships, paid ads, and user-generated content. Consumers benefit from visually rich, interactive content and convenient shopping features like product tagging, in-app purchases, and instant customer support. These features allow businesses to build strong brand presence and drive conversions more effectively than traditional retail models.

The Consumer to Consumer (C2C) segment is emerging as the fastest-growing business model in the social commerce landscape. This growth is driven by peer-to-peer platforms and community marketplaces that empower individuals to sell products directly to one another. The informal, trust-based nature of C2C interactions—especially within niche groups and local networks—has become increasingly popular, particularly among younger generations. Platforms like Facebook Marketplace and WhatsApp groups have simplified selling and buying at a community level, driving a surge in C2C activity globally.

On the other hand, the Business to Business (B2B) model plays a smaller but still relevant role in social commerce. It focuses on enabling businesses to connect with other enterprises for wholesale deals, partnerships, and networking opportunities. Though not as interactive or consumer-facing as B2C or C2C, B2B social commerce is gradually evolving, especially on platforms like LinkedIn where content-driven lead generation and business relationship building are becoming more common.

Market Segmentation: By Product:

• Personal & Beauty Care

• Apparels

• Accessories

• Home Product

• Health Supplement

• Food & Beverage

• Others

The Personal & Beauty Care segment dominates the social commerce market because of its visual appeal, high engagement rates, and strong presence of influencers who frequently promote skincare, cosmetics, and grooming products. Consumers are more likely to buy beauty products after seeing tutorials, reviews, or before-and-after transformations on platforms like Instagram and TikTok. The trust built through influencer content and peer recommendations plays a major role in driving impulse purchases and repeat buying behavior in this segment.

Apparel is one of the fastest-growing segments, fueled by the trend of fashion hauls, outfit-of-the-day (OOTD) posts, and live try-on sessions. Social media users, especially younger demographics, are constantly on the lookout for affordable, trendy clothing, and they rely heavily on creator content for style inspiration. Fast fashion brands have embraced this model, making it easier than ever for consumers to discover, evaluate, and purchase apparel within seconds.

Accessories, home products, and health supplements also see steady demand through visually driven content and lifestyle-focused promotions. Products like jewelry, bags, decor, and wellness items are often featured in creator-curated collections, attracting niche audiences. The food & beverage category is growing through recipe videos, food vlogs, and influencer endorsements, while the "Others" category includes gadgets, pet care, and various niche interests that gain traction through community engagement and targeted content.

Market Segmentation: By Type:

• Laptops & PCs

• Mo-bile

• Tablets

• E-readers

• Internet-enabled TVs

• Others

Mobile devices lead the social commerce market by a remarkable margin, primarily due to their accessibility, ease of use, and integration with social media apps. The majority of social media interactions happen on smartphones, enabling users to seamlessly switch from browsing to shopping without leaving the app. Features like swipe-up links, shoppable posts, and push notifications are optimized for mobile use, making it the most dominant and effective device for social commerce engagement and conversions.

Tablets are gaining popularity as a fast-growing segment, especially for users who prefer a larger screen for browsing but still want the portability of a mobile device. Their enhanced display experience supports more immersive product exploration, making them suitable for live shopping events and product demos. As tablet use continues to rise for media and entertainment, it naturally supports growth in social shopping behavior.

Other devices like laptops, PCs, internet-enabled TVs, e-readers, and others play a supporting role in the market. While laptops and PCs are still used for more detailed browsing and professional interactions, they are less commonly used for instant social purchases. Internet-enabled TVs and smart devices may contribute to discovery through ad exposure or brand storytelling, but their interactive commerce capabilities remain limited. Nonetheless, as technology evolves, these platforms may play a more active role in multi-device commerce ecosystems.

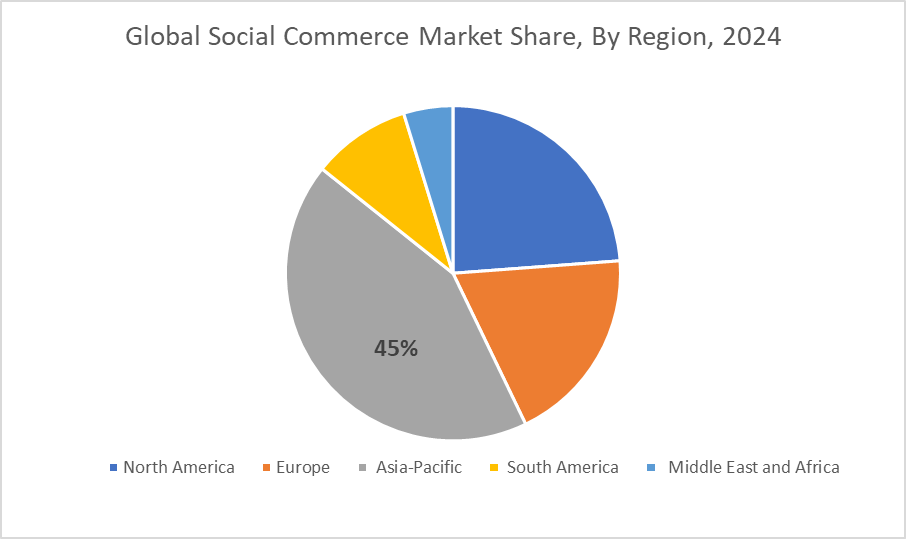

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

Asia-Pacific is the dominant region in the social commerce market, contributing around 45% of the global market share. This dominance is driven by the rapid adoption of mobile technology, high engagement on social media platforms, and a significant surge in e-commerce activities. Countries like China, India, and Japan have become leaders in integrating social commerce into daily life, where platforms such as WeChat and TikTok enable consumers to seamlessly shop without leaving the app. The region’s diverse, tech-savvy population further accelerates the growth of social commerce, making it the most influential and expansive market globally.

The Middle East and Africa, on the other hand, are emerging as the fastest-growing regions in the social commerce landscape. With increasing mobile internet penetration and a younger demographic, these regions are quickly embracing social commerce as an alternative to traditional shopping methods. Social media platforms like Instagram, Facebook, and TikTok are gaining traction, particularly among consumers in urban areas. As the digital ecosystem continues to mature, the region is expected to experience exponential growth in social commerce, driven by expanding internet access and changing consumer behaviors.

COVID-19 Impact Analysis on the Global Social Commerce Market:

The COVID-19 pandemic significantly accelerated the growth of the global social commerce market, as lockdowns and social distancing measures pushed more consumers to shop online. With traditional shopping methods restricted, social media platforms became essential for product discovery and purchasing. The shift toward digital experiences, coupled with increased time spent on social media, drove both brands and consumers to embrace social commerce.

Latest Trends/ Developments:

Recent developments in the social commerce market highlight a significant shift towards live shopping and augmented reality (AR) experiences. Live shopping, where brands host real-time events to showcase products, is becoming increasingly popular. Consumers enjoy the interactive nature of these live sessions, where they can ask questions, see products in action, and make purchases instantly. This real-time engagement creates a sense of urgency and excitement, boosting conversion rates. In addition, social platforms are integrating AR features, allowing users to virtually try on clothes, makeup, and accessories, enhancing the decision-making process.

Another key trend is the rise of influencer-driven commerce, particularly through micro-influencers who have strong, niche followings. These influencers create more authentic, personalized content that resonates deeply with their audiences, driving higher engagement and conversion rates. As a result, brands are moving away from traditional advertising and embracing influencer collaborations to reach specific target groups more effectively. This shift is also fostering stronger connections between consumers and brands, as people are more likely to trust recommendations from individuals they feel are relatable and credible. This trend is transforming social commerce into a more community-oriented, personalized shopping experience.

Key Players:

• Fashnear Technologies Private Limited (Meesho)

• Pinterest, Inc.

• WeChat (Weixin)

• Twitter, Inc.

• TikTok (Douyin)

• Trell Shop

• Etsy, Inc.

• Meta Platforms, Inc. (Facebook)

• Pinduoduo Inc.

• Roposo

Chapter 1. Global Social Commerce Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Social Commerce Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Social Commerce Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Social Commerce Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Social Commerce Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Social Commerce Market – By Business Model

6.1 Business to Business (B2B)

6.2 Business to Consumer (B2C)

6.3 Consumer to Consumer (C2C)

6.4. Y-O-Y Growth trend Analysis By Business Model

6.5. Absolute $ Opportunity Analysis By Business Model, 2025-2030

Chapter 7. Global Social Commerce Market – By Product

7.1 Personal & Beauty Care

7.2 Apparels

7.3 Accessories

7.4 Home Product

7.5 Health Supplement

7.6 Food & Beverage

7.7 Others

7.8. Y-O-Y Growth trend Analysis By Product

7.9. Absolute $ Opportunity Analysis By Product, 2025-2030

Chapter 8. Global Social Commerce Market – By Type

8.1 Laptops & PCs

8.2 Mo-bile

8.3 Tablets

8.4 E-readers

8.5 Internet-enabled TVs

8.6 Others

8.5. Y-O-Y Growth trend Analysis By Type

8.6. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 9. Global Social Commerce Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Business Model

9.1.3. By Product

9.1.4. By Type

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Business Model

9.2.3. By Product

9.2.4. By Type

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Business Model

9.3.3. By Product

9.3.4. By Type

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Business Model

9.4.3. By Product

9.4.4. By Type

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Business Model

9.5.3. By Product

9.5.4. By Type

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Social Commerce Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Fashnear Technologies Private Limited (Meesho)

10.2. Pinterest, Inc.

10.3. WeChat (Weixin)

10.4. Twitter, Inc.

10.5. TikTok (Douyin)

10.6. Trell Shop

10.7. Etsy, Inc.

10.8. Meta Platforms, Inc. (Facebook)

10.9. Pinduoduo Inc.

10.10. Roposo

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Social Commerce Market was valued at USD 1262.19 billion in 2024 and is projected to reach a market size of USD 6243.94 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 37.67%.

The global social commerce market is driven by increased social media usage, the rise of influencer marketing, seamless shopping experiences on platforms, and growing consumer trust in peer recommendations.

Based on Product, the Global Social Commerce Market is segmented into Personal & Beauty Care, Apparels, Accessories, etc.

Asia-Pacific is the most dominant region for the Global Social Commerce Market.

Facebook, Instagram, TikTok, Pinterest are the leading players in the Global Social Commerce Market.