Global Service Robotics Market Research Report – Segmentation by Application (Professional and Personal); By End Use (Defense, Field, Medical, Transportation and Logistics, Mobile Platforms, Underwater System, Construction, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-2215

Format:

Region: Global

Market Size and Overview:

The Global Service Robotics Market was valued at USD 36.1 billion in 2024 and is projected to reach a market size of USD 99.18 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.4%.

The Service Robotics market is rapidly evolving as robots increasingly take on roles that assist, support, or perform tasks for humans across diverse sectors. Unlike industrial robots used in manufacturing, service robots are designed for non-industrial environments—ranging from healthcare and hospitality to logistics, agriculture, and even households. These robots are being adopted to improve efficiency, reduce labor costs, and deliver consistent performance in tasks such as cleaning, delivery, elderly care, surgery assistance, and customer service. With advances in artificial intelligence, sensor technology, and autonomous navigation, service robots are becoming smarter, more interactive, and capable of operating in dynamic real-world settings. As demand surge for automation in everyday life and business operations, the service robotics market is emerging as a critical pillar of the modern automation ecosystem.

Key Market Insights:

The adoption of service robots is accelerating across industries, with over 70% of hospitals in developed countries integrating robotic assistance for surgical support, patient monitoring, and sanitation. The healthcare sector continues to lead in adoption due to increasing demand for precision, hygiene, and staff support, especially in post-pandemic environments. Service robots are also being used to reduce physical strain on healthcare workers and ensure uninterrupted patient care, even under high-demand conditions.

In the logistics and delivery sector, more than 60% of large-scale warehouses have started deploying autonomous mobile robots (AMRs) for tasks such as inventory handling, sorting, and last-mile delivery. These robots not only reduce manual labor but also increase operational speed and reduce error rates. The trend is gaining momentum as e-commerce continues to expand and companies seek scalable automation solutions to meet growing order volumes efficiently.

Consumer and domestic applications are also seeing steady growth, with over 55% of households in tech-forward cities using robotic vacuum cleaners, lawnmowers, or personal assistant robots. Smart home integration and voice-controlled features have made these products more appealing to end-users, while improvements in navigation, battery life, and obstacle detection continue to enhance their usability. As costs decrease and functionality expands, adoption in the residential sector is expected to climb steadily.

Service Robotics Market Drivers:

Rising Labor Shortages and High Operational Costs Are Driving the Demand for Automated Service Solutions Across Multiple Sectors

One of the key drivers of the service robotics market is the global shortage of skilled labor and the rising cost of human workforce across industries such as healthcare, logistics, hospitality, and agriculture. As employers face increasing difficulty in finding and retaining workers for physically demanding, repetitive, or high-risk tasks, service robots offer a cost-effective and reliable alternative. These robots can operate continuously without fatigue, reduce human error, and improve productivity in environments where efficiency and consistency are critical. In aging societies, particularly in Europe and parts of Asia, service robots are also being deployed to fill gaps in elder care, patient monitoring, and household assistance—further emphasizing the role of automation as a necessary workforce supplement. As operational expenses rise and margins tighten, businesses are turning to robotic solutions to lower long-term costs while maintaining service quality.

Technological Advancements in AI, Machine Vision, and Autonomous Navigation Are Enhancing Robot Intelligence and Versatility

Rapid progress in artificial intelligence, sensor technology, and machine learning has significantly increased the capabilities of service robots, enabling them to operate in dynamic and unstructured environments with greater autonomy and accuracy. Robots today can understand human speech, recognize faces, detect obstacles, and make decisions in real time using data from multiple sensors and AI algorithms. These innovations have expanded the scope of applications for service robotics—from robots that deliver food in hotels and hospitals to drones that monitor crops and robots that assist in surgeries with precision. The improvement in user interfaces, including voice recognition and gesture controls, is also making robots more accessible to consumers and businesses alike. As technology continues to evolve, robots are becoming more adaptive, multifunctional, and scalable, which is fueling broader acceptance and deployment across new use cases.

Growing Demand for Contactless and Hygienic Solutions in Healthcare, Hospitality, and Public Services Is Accelerating Adoption

In the wake of global health concerns and changing consumer expectations, there is a rising preference for contactless service experiences, especially in sectors like healthcare, hospitality, and public infrastructure. Service robots provide a hygienic alternative for performing tasks such as sanitization, food delivery, patient interaction, and room cleaning—minimizing human-to-human contact while ensuring operational continuity. Hospitals are increasingly using autonomous robots for disinfection and patient monitoring, while hotels are deploying robots to manage guest services without physical interaction. This shift toward automation is not just a temporary response to health concerns but a long-term transformation in how service industries operate. The ability of robots to maintain cleanliness, safety, and reliability without fatigue makes them a valuable asset in a post-pandemic world where hygiene and efficiency are critical to customer satisfaction and regulatory compliance.

Government Support, Industry Collaborations, and R&D Investments Are Catalyzing Market Growth and Innovation

Supportive government policies, funding programs, and public-private collaborations are playing a crucial role in accelerating the development and adoption of service robotics across various regions. Governments in technologically advanced economies are promoting robotics through subsidies, pilot projects, and innovation hubs, aiming to boost automation and reduce reliance on manual labor. At the same time, industry leaders and startups are investing heavily in research and development to enhance robotic design, mobility, and software integration. These investments are leading to the emergence of specialized robots tailored for specific sectors such as agriculture (for harvesting and monitoring), education (for interactive learning), and retail (for inventory and customer engagement). Cross-industry partnerships are also fostering innovation, with tech companies collaborating with healthcare providers, logistics firms, and educational institutions to create next-generation service robots.

Service Robotics Market Restraints and Challenges:

High Initial Costs, Limited Interoperability, and Safety Concerns Restrict Widespread Adoption of Service Robots

Despite the promising growth of the service robotics market, several significant restraints and challenges continue to hinder its broader adoption. One of the primary barriers is the high upfront cost of robotic systems, including the investment in hardware, software, integration, and training, which can be prohibitive for small and mid-sized businesses. Additionally, a lack of standardization and interoperability across different platforms and manufacturers makes it difficult to implement robots seamlessly within existing operational frameworks. Safety and ethical concerns, especially in sectors involving human interaction like healthcare and education, further slowdown adoption, as stakeholders demand rigorous testing and compliance with evolving regulations. Moreover, the need for specialized technical knowledge to operate, maintain, and troubleshoot advanced robots creates a skills gap that limits deployment, particularly in emerging economies.

Service Robotics Market Opportunities:

The service robotics market is poised for strong expansion as opportunities emerge across untapped sectors such as education, agriculture, elderly care, and retail, where automation is beginning to transform daily operations and service delivery. The integration of artificial intelligence, natural language processing, and machine learning is enabling robots to perform more personalized, context-aware tasks, from tutoring students to assisting elderly individuals with daily routines. Meanwhile, the growing demand for smart homes and connected consumer devices is driving interest in domestic service robots with advanced features like voice control and real-time environmental sensing. As AI capabilities become more affordable and scalable, and as user comfort with robotics grows, businesses and consumers alike are exploring how robots can add value to everyday life, creating a wide field of opportunity for innovation and commercialization.

Service Robotics Market Segmentation:

Market Segmentation: By Application:

• Professional

• Personal

In the service robotics market, the professional application segment holds the dominant share, driven by strong adoption across industries such as healthcare, logistics, hospitality, agriculture, and defense. These robots are designed to perform specialized tasks like surgical assistance, hospital delivery, warehouse automation, and field surveillance—often in high-demand or high-risk environments where precision, efficiency, and reliability are critical. The need for professional service robots is growing rapidly due to increasing labor shortages, the need for cost-effective operations, and a strong push for automation in both public and private sectors. Additionally, regulatory support, technological advancement, and industry partnerships are accelerating the integration of robots into professional workflows, reinforcing this segment's leadership in the market.

On the other hand, the personal application segment is growing steadily as consumers increasingly adopt robots for domestic tasks such as cleaning, lawn mowing, elderly care, and entertainment. Technological improvements in navigation, voice interaction, and energy efficiency are making these robots more accessible, intuitive, and desirable for everyday use. The rising trend of smart homes and connected living is further driving demand, with users seeking personalized robotic solutions that can seamlessly integrate with their digital lifestyles. As affordability improves and awareness grows, the personal robotics segment is expected to expand significantly, especially in urban areas and aging societies where convenience, safety, and independent living are becoming top priorities.

Market Segmentation: By End-Use:

• Defense

• Field

• Medical

• Transportation and Logistics

• Mobile Platforms

• Underwater systems

• Construction

• Others

In the service robotics market, the medical segment is currently the dominant end-use category, fueled by the widespread adoption of robots in hospitals and healthcare facilities for surgery, disinfection, rehabilitation, patient monitoring, and medication delivery. The growing need for precision, hygiene, and consistent performance in critical care environments has made robots indispensable, especially in tasks that demand accuracy and minimal human error. Surgical robots, in particular, have gained significant traction for minimally invasive procedures, while mobile robots are being used to assist with tasks such as delivering supplies and reducing contact in infection-sensitive zones. With the aging global population and increasing focus on healthcare efficiency, the medical sector continues to lead in both innovation and deployment of service robotics.

Meanwhile, transportation and logistics is emerging as the fastest-growing end-use segment, driven by the boom in e-commerce, same-day delivery expectations, and the automation of warehouse operations. Autonomous mobile robots (AMRs), robotic arms, and drone delivery systems are being rapidly integrated into supply chain processes to manage inventory, sort packages, and transport goods with minimal human intervention. Companies are investing heavily in robotic systems to reduce operational costs, increase speed, and improve fulfillment accuracy. As logistics providers continue to scale their operations and adopt robotics to meet growing demand, this segment is expected to witness accelerated growth and transformation in the coming years.

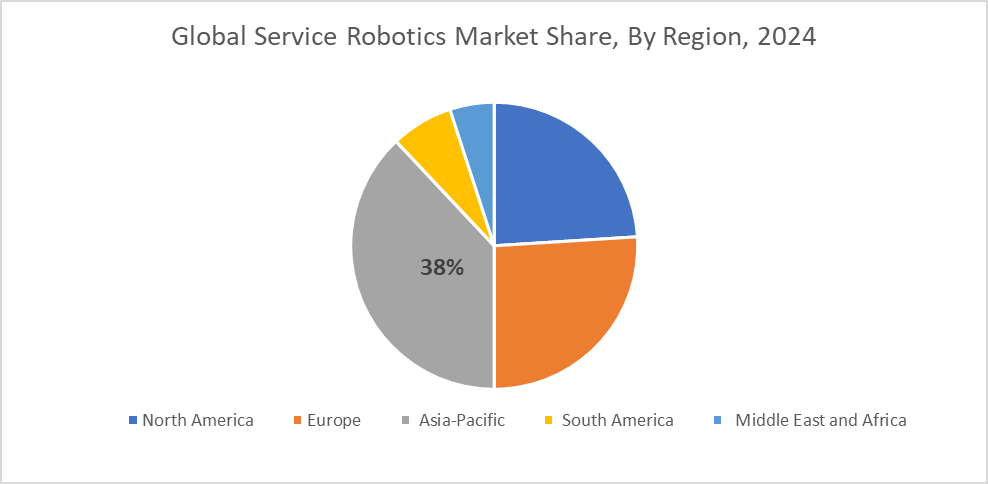

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

In the service robotics market, Asia-Pacific holds the dominant position with 38% of the global share, driven by rapid technological advancement, strong manufacturing capabilities, and large-scale deployment across sectors like healthcare, logistics, and consumer electronics. Countries like China, Japan, and South Korea are leading in both the production and adoption of service robots, supported by government initiatives, aging populations, and the push for automation in everyday life. Japan, for example, has integrated robots into elder care and hospitals at a national level, while China continues to invest heavily in robotics for delivery, education, and smart city development.

Europe is emerging as the fastest-growing region in the service robotics market, propelled by its strong emphasis on ethical AI, safety regulations, and innovation in sectors such as healthcare, agriculture, and public services. The European Union is actively funding robotics projects through Horizon programs, encouraging collaboration between academia, startups, and industry leaders. Moreover, European countries are rapidly adopting robotic solutions for elderly care, rehabilitation, and smart farming, where precision and labor efficiency are critical. With high digital literacy, favorable regulatory support, and growing public acceptance, Europe is witnessing accelerated adoption of intelligent service robots, positioning itself as a key growth engine for the global market in the coming years.

COVID-19 Impact Analysis on the Global Service Robotics Market:

The COVID-19 pandemic significantly accelerated the adoption of service robotics across various sectors as organizations sought safer, contactless, and more efficient ways to operate during health crises. In healthcare, robots were deployed for disinfection, patient monitoring, and medication delivery to reduce the risk of virus transmission. Similarly, in logistics and retail, autonomous robots were used to handle increased demand for delivery and minimize human contact. The pandemic also drove interest in domestic robots as people spent more time at home and sought automation for cleaning and assistance. Overall, COVID-19 acted as a catalyst, reshaping perceptions and proving the essential role of service robots in maintaining continuity, safety, and productivity.

Latest Trends/ Developments:

One of the most prominent trends in the service robotics market is the growing use of AI-driven collaborative robots (cobots) in industries that demand close interaction with humans. These robots are designed to work safely alongside people in dynamic environments, adapting in real-time to human behavior, voice commands, and changing surroundings. Their applications are expanding rapidly in healthcare (for rehabilitation and elderly care), retail (for customer assistance and inventory management), and education (for interactive learning). Cobots equipped with emotion recognition, natural language processing, and adaptive movement capabilities are transforming how service roles are automated, making human-robot collaboration more seamless, intuitive, and efficient than ever before.

Another major development is the rising integration of service robots into cloud platforms and IoT ecosystems, enabling remote access, real-time monitoring, and centralized control. This advancement allows businesses to scale robot fleets across multiple locations while maintaining consistency in performance and updates. Cloud connectivity also facilitates data sharing between robots, enhancing collective learning and operational optimization. In the consumer segment, service robots are increasingly being designed to interact with smart home systems and voice assistants, offering users a connected, personalized experience. These innovations are pushing service robots beyond isolated tasks, embedding them as intelligent, responsive components of wider digital infrastructure in both professional and personal environments.

Key Players:

• Intuitive Surgical Operations, Inc. (US)

• DJI (China)

• Daifuku Co., Ltd. (Japan)

• JD.com, Inc. (China)

• iRobot Corporation (US)

• Samsung Electronics Co., Ltd. (South Korea)

• KONGSBERG (Norway)

• Northrop Grumman (US)

• Softbank Robotics Group (Japan)

• DeLaval (Sweden)

Chapter 1. Global Service Robotics Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Service Robotics Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Service Robotics Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Service Robotics Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Service Robotics Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Service Robotics Market – By Application

6.1. Introduction/Key Findings

6.2. Professional

6.3. Personal

6.4. Y-O-Y Growth trend Analysis By Application

6.5. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 7. Global Service Robotics Market – By End Use

7.1. Introduction/Key Findings

7.2. Defense

7.3. Field

7.4. Medical

7.5. Transportation & Logstics

7.6. Mobile Platforms

7.7. Underwater systems

7.9. Construction

7.10. Others

7.11. Y-O-Y Growth trend Analysis By End Use

7.12. Absolute $ Opportunity Analysis By End Use, 2025-2030

Chapter 8. Global Service Robotics Market, By Geography – Market Size, Forecast, Trends & Insights

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Application

8.1.3. By End Use

8.1.4. Countries & Segments – Market Attractiveness Analysis

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Application

8.2.3. By End Use

8.2.4. Countries & Segments – Market Attractiveness Analysis

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia-Pacific

8.3.2. By Application

8.3.3. By End Use

8.3.4. Countries & Segments – Market Attractiveness Analysis

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Application

8.4.3. By End Use

8.4.4. Countries & Segments – Market Attractiveness Analysis

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. United Arab Emirates (UAE)

8.5.1.2. Saudi Arabia

8.5.1.3. Qatar

8.5.1.4. Israel

8.5.1.5. South Africa

8.5.1.6. Nigeria

8.5.1.7. Kenya

8.5.1.8. Egypt

8.5.1.9. Rest of MEA

8.5.2. By Application

8.5.3. By end Use

8.5.4. Countries & Segments – Market Attractiveness Analysis

Chapter 9. Global Service Robotics Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

9.1 Intuitive Surgical Operations, Inc. (US)

9.2 DJI (China)

9.3 Daifuku Co., Ltd. (Japan)

9.4 JD.com, Inc. (China)

9.5 iRobot Corporation (US)

9.6 Samsung Electronics Co., Ltd. (South Korea)

9.7 KONGSBERG (Norway)

9.8 Northrop Grumman (US)

9.9 Softbank Robotics Group (Japan)

9.10 DeLaval (Sweden)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Service Robotics Market was valued at USD 36.1 billion in 2024 and is projected to reach a market size of USD 99.18 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.4%.

Rising automation demand, labor shortages, AI advancements, and hygiene needs.

Based on Application, the Global Service Robotics Market is segmented into Professional and personal.

Asia-Pacific is the most dominant region for the Global Service Robotics Market.

Intuitive Surgical Operations, Inc. (US), DJI (China), Daifuku Co., Ltd. (Japan) are the leading players in the Global Service Robotics Market.