Millimeter Wave Technology Market Research Report – Segmentation by Component (Antennas & Transceivers, Amplifiers & Radio-Frequency Integrated Circuits (RFICs), Oscillators & Frequency Converters, Control Devices & Filters); By Application (Telecommunications, Automotive & Transport, Aerospace & Defense, Consumer Electronics & Industrial); By Frequency Band (E-Band, V-Band, D-Band, Other Bands); By Product Type (Scanner & Imaging Systems, Radar & Satellite Communication Systems, Telecommunication Equipment); – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-2309

Format:

Region: Global

Market Size and Overview:

The Millimeter Wave Technology Market was valued at USD 4.22 Billion in 2024 and is projected to reach a market size of USD 10.36 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 20.3%.

The Millimeter Wave (mmWave) Technology Market represents a pivotal frontier in the evolution of wireless communication and sensing technologies, carving out a crucial niche in the global technology landscape. This market revolves around the spectrum of electromagnetic frequencies between 30 GHz and 300 GHz, a band once considered too complex and challenging for commercial use. Today, it stands as the cornerstone for next-generation innovations, fundamentally redefining the paradigms of data transmission, environmental sensing, and connectivity. The core value proposition of mmWave technology lies in its ability to support immense bandwidth, enabling data transfer rates that are orders of magnitude greater than conventional sub-6 GHz frequencies. As manufacturing processes mature and economies of scale begin to take effect, the cost and complexity of implementing mmWave solutions are gradually decreasing, paving the way for broader adoption across a more diverse range of applications and industries, and solidifying its position as a critical enabler of the digital future.

Key Market Insights:

This growth was significantly propelled by the telecommunications sector, which accounted for approximately 55% of all mmWave component shipments during the year.

In the 5G domain, it was estimated that 18% of newly deployed urban base stations in 2024 were equipped with mmWave capabilities to handle high-density data traffic.

Furthermore, over 30% of all new vehicles manufactured in 2024 were equipped with at least one mmWave-based ADAS sensor.

Investment in the sector remained robust, with venture capital funding for mmWave startups exceeding $500 million in 2024.

On the consumer side, an estimated 90 million smartphone units shipped in 2024 featured mmWave antenna modules.

In aerospace and defense, spending on mmWave-based satellite communication terminals reached nearly $600 million.

The E-band (71-76 GHz and 81-86 GHz) constituted roughly 40% of the frequency band market share due to its balanced performance for backhaul. Meanwhile, sales of gallium nitride (GaN)-based mmWave amplifiers grew by 25% in 2024.

The industrial sector saw over 15,000 mmWave sensors deployed for process monitoring and robotics.

Market Drivers:

Exponential Growth of 5G and Future Wireless Standards

The primary engine propelling the mmWave market forward is the global deployment of 5G networks and the concurrent research into 6G. Millimeter wave frequencies are fundamental to achieving the gigabit-per-second speeds and ultra-low latency that define the true 5G experience. As mobile data consumption continues to explode, driven by high-definition video streaming, online gaming, and AR/VR applications, network carriers are compelled to leverage the massive bandwidth available in the mmWave spectrum to alleviate congestion in traditional sub-6 GHz bands. This driver extends beyond consumer mobile to fixed wireless access (FWA), providing fiber-like internet speeds in areas where laying physical cables is impractical.

Advancements in Automotive Radar and Autonomous Systems

The automotive industry's relentless pursuit of enhanced safety and full autonomy serves as a powerful, independent driver for the mmWave market. Millimeter wave radar is the sensory backbone of modern ADAS, enabling critical functions like adaptive cruise control, automatic emergency braking, and blind-spot detection. Its ability to provide precise velocity, range, and angle measurements, even in adverse weather conditions, makes it superior to other sensing modalities like cameras or LiDAR for certain functions. As vehicles progress towards higher levels of autonomy (L3 and beyond), the number and sophistication of mmWave sensors per vehicle are set to increase dramatically.

Market Restraints and Challenges:

The widespread adoption of millimeter wave technology is principally constrained by its inherent physical properties. These high-frequency signals suffer from significant propagation loss and are easily obstructed by physical objects like buildings, foliage, and even heavy rain, severely limiting their effective range and requiring a direct or near-direct line of sight. This necessitates the deployment of a much denser network of base stations, which elevates infrastructure costs and complicates network planning, thereby posing a significant barrier to achieving ubiquitous coverage, especially in suburban and rural environments.

Market Opportunities:

Substantial market opportunities are emerging from the application of mmWave technology in satellite communications and non-terrestrial networks. Constellations of low Earth orbit (LEO) satellites can utilize mmWave for high capacity backhaul and to deliver broadband services to remote and underserved regions globally. Another significant opportunity lies in the industrial sector, where mmWave sensors can enable high-precision robotics, asset tracking, and process control in smart factories. The development of low-cost, integrated mmWave modules will unlock further use cases in consumer electronics and smart home devices.

Market Segmentation:

Segmentation by Component:

• Antennas & Transceivers

• Amplifiers & Radio-Frequency Integrated Circuits (RFICs)

• Oscillators & Frequency Converters

• Control Devices & Filters

This segment is experiencing the most rapid growth, driven by the increasing integration of mmWave capabilities into compact devices like smartphones and customer-premises equipment. Advances in semiconductor materials like GaN and SiGe are enabling the production of smaller, more power-efficient, and cost-effective RFICs and amplifiers, which are critical for overcoming the technology's inherent power consumption and thermal challenges.

Antennas and transceivers remain the most dominant component segment, as they are the fundamental hardware interface in every mmWave system. The development of advanced antenna-in-package (AiP) and phased-array antenna designs is critical for implementing the complex beamforming techniques required for mmWave communication, making this segment an indispensable part of both the infrastructure and user equipment markets.

Segmentation by Application:

• Telecommunications

• Automotive & Transport

• Aerospace & Defense

• Consumer Electronics & Industrial

The automotive and transport sector represents the fastest-growing application area. This growth is fueled by the escalating integration of ADAS in mainstream vehicles and the industry-wide push towards higher levels of autonomous driving. Each step up in autonomy requires a more extensive and sophisticated suite of sensors, with mmWave radar being a cornerstone technology for reliable environmental perception.

Telecommunications continue to be the most dominant application, commanding the largest share of the market. This dominance is due to the massive global investment in 5G infrastructure, where mmWave is essential for delivering headline multi-gigabit speeds in dense urban areas, stadiums, and for fixed wireless access. The sheer scale of network deployments solidifies this segment's leading position.

Segmentation by Frequency Band:

• E-Band (71-76 GHz and 81-86 GHz)

• V-Band (57-64 GHz)

• D-Band (130-174.8 GHz)

• Other Bands (including 24/28/39 GHz for 5G)

The D-Band is emerging as the fastest-growing frequency segment, primarily driven by research and development into future automotive radar and 6G communication systems. While not yet in widespread commercial use, its potential for extremely high-resolution sensing and massive data throughput is attracting significant investment, positioning it as a key band for next-generation applications beyond 2025.

The E-Band is currently the most dominant frequency band in terms of revenue, largely due to its widespread use in wireless backhaul and fronthaul for cellular networks. Its licensed nature and favorable propagation characteristics compared to other mmWave bands make it the go-to solution for carriers needing to establish high-capacity, point-to-point links to connect their cell towers.

Segmentation by Product Type:

• Scanner & Imaging Systems

• Radar & Satellite Communication Systems

• Telecommunication Equipment

This product category is the fastest growing, propelled by dual engines of growth in the automotive sector's demand for advanced radar and the burgeoning market for LEO satellite broadband services. As both autonomous driving and space-based internet technologies mature, the demand for sophisticated radar and satcom systems operating in the mmWave spectrum is accelerating rapidly.

Telecommunication equipment, including 5G base stations (gNodeB), small cells, and fixed wireless access points, remains the most dominant product type. The global imperative to build out 5G networks ensures a massive and sustained demand for this equipment, making it the largest segment by a significant margin as network operators continue to densify their mmWave deployments.

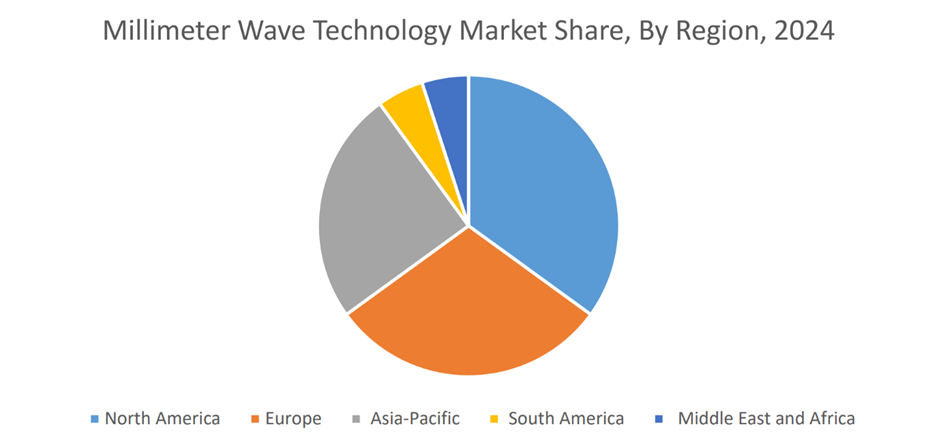

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

North America maintains its dominance in the mmWave market due to aggressive 5G deployments by major carriers, particularly in the United States, and its leadership in the aerospace and defense sectors. The region's strong R&D ecosystem and early adoption of mmWave-enabled consumer devices further cement its leading position in both consumption and innovation.

The Asia-Pacific region is the fastest-growing market for mmWave technology. This rapid expansion is driven by significant government-backed 5G rollouts in countries like South Korea, Japan, and China, coupled with a massive and tech-savvy consumer base and a burgeoning automotive manufacturing industry that is rapidly adopting advanced sensor technologies.

COVID-19 Impact Analysis:

The COVID-19 pandemic acted as an unexpected catalyst for the millimeter wave market. The global shift to remote work, virtual learning, and telehealth created an unprecedented strain on existing network infrastructure, highlighting the urgent need for greater bandwidth and more reliable connectivity. This accelerated investment timelines for 5G and fixed wireless access deployments, boosting demand for mmWave equipment. While the pandemic initially caused supply chain disruptions for some components, the long-term effect has been a reinforced strategic imperative for building next-generation wireless infrastructure.

Latest Trends and Developments:

A key trend shaping the market is the development of fully integrated antenna-in-package (AiP) solutions, which combine antennas, transceivers, and other RF components into a single, compact module. This integration is crucial for reducing the size, cost, and power consumption of mmWave systems, enabling their use in smartphones and other portable devices. Another significant development is the increasing use of artificial intelligence and machine learning to optimize complex beamforming and beam-steering algorithms, enhancing signal reliability and network efficiency in challenging environments.

Key Players in the Market:

• Axxcss Wireless Solutions (US)

• NEC Corporation (Japan)

• Ceragon (Israel)

• L3Harris Technologies, Inc. (US)

• Aviat Networks (US)

• Smiths Group plc (UK)

• Eravant (US)

• Farran (Ireland)

• Keysight Technologies (US)

• Ducommun Incorporated (US)

Chapter 1. Global Millimeter Wave Technology Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Millimeter Wave Technology Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Millimeter Wave Technology Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Millimeter Wave Technology Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Millimeter Wave Technology Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Millimeter Wave Technology Market – By Component

6.1. Introduction/Key Findings

6.2. Antennas & Transceivers

6.3. Amplifiers & Radio-Frequency Integrated Circuits (RFICs)

6.4. Oscillators & Frequency Converters

6.5. Control Devices & Filters

6.6. Y-O-Y Growth trend Analysis By Component

6.7. Absolute $ Opportunity Analysis By Component, 2024-2030

Chapter 7. Global Millimeter Wave Technology Market – By Application

7.1. Introduction/Key Findings

7.2. Telecommunications

7.3. Automotive & Transport

7.4. Aerospace & Defense

7.5. Consumer Electronics

7.6. Industrial

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2024-2030

Chapter 8. Global Millimeter Wave Technology Market – By Frequency Band

8.1. Introduction/Key Findings

8.2. E-Band

8.3. V-Band

8.4. D-Band

8.5. Other Bands

8.6. Y-O-Y Growth trend Analysis By Frequency Band

8.7. Absolute $ Opportunity Analysis By Frequency Band, 2024-2030

Chapter 9. Global Millimeter Wave Technology Market – By Product Type

9.1. Introduction/Key Findings

9.2. Scanner & Imaging Systems

9.3. Radar & Satellite Communication Systems

9.4. Telecommunication Equipment

9.5. Y-O-Y Growth trend Analysis By Product Type

9.6. Absolute $ Opportunity Analysis By Product Type, 2024-2030

Chapter 10. Global Millimeter Wave Technology Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Application

10.1.4. By Frequency Band

10.1.5. By Product Type

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Application

10.2.4. By Frequency Band

10.2.5. By Product Type

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Component

10.3.3. By Application

10.3.4. By Frequency Band

10.3.5. By Product Type

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Application

10.4.4. By Frequency Band

10.4.5. By Product Type

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Application

10.5.4. By Frequency Band

10.5.5. By Product Type

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Millimeter Wave Technology Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Axxcss Wireless Solutions (US)

11.2. NEC Corporation (Japan)

11.3. Ceragon (Israel)

11.4. L3Harris Technologies, Inc. (US)

11.5. Aviat Networks (US)

11.6. Smiths Group plc (UK)

11.7. Eravant (US)

11.8. Farran (Ireland)

11.9. Keysight Technologies (US)

11.10. Ducommun Incorporated (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary growth drivers are the massive bandwidth requirements for 5G and future wireless standards, which are essential for applications like high-definition streaming and AR/VR, and the critical role of high-resolution mmWave radar in enabling advanced driver-assistance systems (ADAS) and the development of autonomous vehicles.

The main challenges stem from the physical properties of high-frequency signals, including limited range, susceptibility to physical obstructions (requiring line-of-sight), and higher signal attenuation. These factors lead to increased infrastructure density and higher deployment costs compared to lower-frequency bands, hindering widespread coverage.

Key players include Qualcomm, Samsung, Nokia, Ericsson, Huawei, Analog Devices, Keysight Technologies, NXP Semiconductors, Infineon Technologies, Texas Instruments, MACOM, Qorvo, Sivers Semiconductors, Anritsu, and Rohde & Schwarz.

North America currently holds the largest market share, estimated at around 38%, driven by early and aggressive 5G network deployments and a strong aerospace and defense industry.

The automotive and transport application is expanding at the highest rate, fueled by the rapid integration of mmWave radar sensors into vehicles for ADAS and the ongoing development of fully autonomous driving systems.