Logistics Automation Market Research Report – Segmentation by Component (Automated Storage and Retrieval Systems (AS/RS), Conveyor Systems, Sortation Systems, Palletizing and Depalletizing Systems, Robotic Picking and Packing Systems, Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs), Industrial Sensors, Barcode and RFID Scanners, Warehouse Management Systems (WMS), Transportation Management Systems (TMS), Yard Management Systems (YMS), Inventory Management Systems, Order Management Systems, Consulting, System Integration and Deployment, Support and Maintenance); By End-Use Industry (Retail and E-commerce, Manufacturing, Automotive, Healthcare and Pharmaceuticals, Food and Beverages, Aerospace and Defense, Consumer Electronics, Logistics and Transportation, Textiles, Chemicals, Oil & Gas); By Automation Type (Fixed Automation, Flexible Automation); By Enterprise Size (Large Enterprises, Small and Medium Enterprises (SMEs)); Region – Forecast (2024 – 2030)

Published: 2024 - January

Report Code: IM-4176

Format:

Region: Global

Market Size and Overview:

In 2024, the logistics automation market crossed USD 34 billion, with automated solutions cutting operational costs by an average of 28% across industries. Companies deploying end-to-end automation reported a 29.3% boost in warehouse productivity within the first year alone. Autonomous Mobile Robots (AMRs) surged by 34% year-on-year, reshaping warehouse layouts with flexible, scalable operations.

With e-commerce order volumes growing 5x faster than traditional retail and labor shortages driving logistics costs up by over 18%, automated systems have shifted from a "nice-to-have" to a "must-have" for competitive survival.

This report offers actionable segmentation by component, automation type, and end-user industry; uncovers pricing trends; analyzes deployment models; and provides country-specific insights including North America, Asia-Pacific, and Europe.

2025–2030 marks a critical window. Companies acting now can secure operational advantages, reduce risks, and achieve 3–5x faster returns on automation investments compared to late adopters.

The logistics automation market has experienced remarkable growth in 2024, revolutionizing supply chain operations across industries through advanced technological integration. This transformation is characterized by the increasing adoption of robotics, artificial intelligence, warehouse management systems, and autonomous vehicles designed to streamline logistics processes. Companies worldwide are recognizing the competitive advantages offered by automation technologies, including enhanced operational efficiency, reduced labor costs, and improved accuracy in inventory management. The market is witnessing a significant shift from traditional manual processes to sophisticated automated solutions that can handle complex logistics tasks with minimal human intervention. The current market landscape reflects a strong emphasis on end-to-end automation solutions that provide seamless connectivity between different stages of the supply chain. Major industry players are focusing on developing integrated platforms that combine various automation technologies to offer comprehensive logistics management capabilities. The rise of e-commerce has been a pivotal factor driving demand for logistics automation, as businesses strive to meet increasingly stringent customer expectations regarding delivery speed and accuracy. Additionally, the push toward sustainability has influenced market growth, with automated systems demonstrating superior energy efficiency and reduced environmental impact compared to conventional methods. In 2024, small and medium-sized enterprises (SMEs) have become more prominent participants in the logistics automation market, facilitated by the availability of scalable and cost-effective solutions. Cloud-based logistics automation platforms have gained substantial traction, enabling businesses of all sizes to access advanced capabilities without significant upfront investments.

Key Market Insights:

Studies indicate that companies implementing comprehensive logistics automation solutions report an average productivity increase of 29.3% within the first year of deployment.

The adoption rate of automated guided vehicles (AGVs) has surged by 47% in 2024 compared to the previous year, reflecting the growing preference for mobile robotics in warehouse environments.

Approximately 62% of logistics providers are currently utilizing some form of artificial intelligence to optimize route planning and inventory management.

Automated sortation systems have demonstrated an impressive 32.6% reduction in order processing time across industries.

The pharmaceutical sector has emerged as a significant adopter of logistics automation, with 71.5% of pharmaceutical companies investing in automated storage and retrieval systems.

Market Drivers:

Increasing E-commerce Demands

The explosive growth of e-commerce has fundamentally transformed consumer expectations around delivery speed, accuracy, and flexibility, creating unprecedented pressures on supply chain operations. Modern consumers demand same-day or next-day delivery options, accurate order fulfilment, and real-time tracking capabilities—requirements that are virtually impossible to meet consistently through manual processes alone. Logistics automation technologies address these challenges directly by enabling high-speed order processing, reducing picking errors through guided systems, and facilitating rapid sortation and dispatch operations. The ability to handle high-volume, high-variety order profiles efficiently has become essential for e-commerce success, particularly during peak seasons when order volumes can increase exponentially. Additionally, the rise of omnichannel retail strategies requires seamless integration between physical and online sales channels, necessitating sophisticated automated inventory management systems that maintain accurate stock visibility across all points of sale. Companies leveraging advanced logistics automation have demonstrated their ability to reduce order fulfilment times by up to 70% while simultaneously improving accuracy rates to over 99.9%, creating significant competitive advantages in the rapidly evolving e-commerce landscape.

Labor Shortages and Rising Costs

The logistics industry is facing severe workforce challenges characterized by persistent labor shortages, high turnover rates, and steadily increasing wage costs, creating compelling incentives for automation adoption. In many developed markets, logistics operations struggle to attract and retain qualified personnel for physically demanding roles in warehouses and distribution centers, particularly for night shifts and peak seasons. This workforce gap has been exacerbated by demographic shifts including aging populations and changing career preferences among younger workers. The financial implications are substantial, with labor typically representing 50-70% of operational costs in traditional logistics facilities. Automation technologies directly address these challenges by reducing dependence on manual labour while improving working conditions for remaining staff. Tasks that once required extensive human intervention—such as heavy lifting, repetitive picking, and long-distance walking within facilities—can now be performed by automated systems operating continuously without fatigue or performance variation. This transition allows human workers to be reallocated to higher-value roles requiring judgment and problem-solving skills, often resulting in increased job satisfaction and reduced turnover. The economic case for automation becomes increasingly compelling as labour costs rise, with many companies reporting that automation investments reach positive ROI significantly faster in regions with high labour costs.

Market Restraints and Challenges:

The logistics automation market faces significant barriers including high initial investment requirements and technical integration complexities. Many existing facilities require extensive structural modifications to accommodate automation systems, increasing implementation costs. Legacy IT systems often prove incompatible with modern automation platforms, necessitating additional investments in digital infrastructure. Furthermore, workforce resistance and training requirements can delay adoption and reduce projected returns, particularly in organizations with limited change management capabilities.

Market Opportunities:

Emerging technologies including artificial intelligence and machine learning present substantial opportunities for predictive logistics optimization. The growing middle class in developing regions is driving demand for efficient distribution networks, creating new markets for automation solutions. Sustainability initiatives provide openings for energy-efficient automation systems that reduce environmental impact while improving operational efficiency. Additionally, the increasing availability of automation-as-a-service models is making sophisticated technologies accessible to smaller organizations, significantly expanding the potential customer base for logistics automation providers.

Market Segmentation:

By Component:

Hardware:

• Automated Storage and Retrieval Systems (AS/RS)

• Conveyor Systems

• Sortation Systems

• Palletizing and Depalletizing Systems

• Robotic Picking and Packing Systems

• Automated Guided Vehicles (AGVs)

• Autonomous Mobile Robots (AMRs)

• Industrial Sensors

• Barcode and RFID Scanners

• Others (Cranes, Carousels, Shuttle Systems)

Software:

• Warehouse Management Systems (WMS)

• Transportation Management Systems (TMS)

• Yard Management Systems (YMS)

• Inventory Management Systems

• Order Management Systems

• Others (Fleet Management, Labor Management Software)

Services:

• Consulting

• System Integration and Deployment

• Support and Maintenance

Autonomous Mobile Robots represent the fastest-growing hardware component within logistics automation, experiencing 34% year-over-year growth. Unlike fixed automation or traditional AGVs, these flexible systems require minimal infrastructure modifications and can be rapidly deployed and reconfigured. AMRs leverage advanced navigation capabilities, machine learning, and sophisticated sensor arrays to navigate dynamic environments without predefined paths. Their modular design and scalable implementation allow organizations to start with limited deployments and expand incrementally, creating adoption advantages for operations with uncertain future requirements or space constraints.

Warehouse Management Systems maintain their position as the dominant software component within logistics automation, representing approximately 43% of total software expenditures. These systems serve as the central nervous system for automated operations, orchestrating workflows, resource allocation, and information flows across diverse automation technologies. WMS functionality has expanded beyond inventory control to incorporate sophisticated optimization algorithms, labor management, yard operations, and seamless integration with enterprise systems. Cloud-based deployment models have democratized access to enterprise-grade capabilities, accelerating adoption across organization sizes. The strategic importance of WMS continues to grow as automation complexity increases, requiring sophisticated coordination between human operators and diverse automated systems.

By End-Use Industry:

• Retail and E-commerce

• Manufacturing

• Automotive

• Healthcare and Pharmaceuticals

• Food and Beverages

• Aerospace and Defense

• Consumer Electronics

• Logistics and Transportation

• Others (Textiles, Chemicals, Oil & Gas)

The healthcare and pharmaceuticals sector has emerged as the fastest-growing vertical within logistics automation, experiencing 27% year-over-year implementation growth. This acceleration reflects unique industry pressures including regulatory compliance requirements, product traceability demands, temperature-controlled handling needs, and critical accuracy imperatives where errors carry significant consequences. The pandemic dramatically highlighted supply chain vulnerabilities within healthcare, catalyzing investment in automated systems that enhance resilience. Automation technologies address specialized requirements including clean room operations, precise environmental controls, expiration date management, and chain-of-custody documentation. The sector's high-value inventory profiles create compelling financial justifications for automation investments that reduce handling damage, improve inventory accuracy, and minimize spoilage rates.

Retail and e-commerce maintain their position as the dominant vertical within logistics automation, accounting for approximately 38% of total market expenditures. This dominance reflects the sector's massive scale, intense competitive pressures, and fundamental dependency on efficient logistics operations as a core competitive differentiator. E-commerce fulfillment requirements have driven innovation across the automation spectrum, from sophisticated goods-to-person systems to advanced sortation technologies optimized for parcel handling. The sector's demanding service level agreements, including same-day and next-day delivery, create compelling operational requirements that automation directly addresses. Additionally, the unpredictable demand patterns and seasonal volatility characteristic of retail operations create natural alignment with flexible automation systems that can scale capacity dynamically.

By Automation Type:

• Fixed Automation

• Flexible Automation

Flexible automation represents the fastest-growing category, experiencing 29% year-over-year growth as organizations prioritize adaptability within uncertain business environments. These systems, characterized by programmable capabilities and reconfigurable physical arrangements, allow operations to adjust to changing product mixes, volume fluctuations, and evolving business requirements without significant capital reinvestment. The category includes technologies such as autonomous mobile robots, collaborative robots, and modular conveyor systems designed for rapid reconfiguration. Flexible systems typically feature shorter implementation timelines and allow incremental deployment strategies that reduce initial capital requirements while maintaining expansion capabilities. Their inherent adaptability provides valuable insurance against forecast uncertainty and future process changes.

Fixed automation maintains its position as the dominant category by market share, representing approximately 64% of total automation expenditures. These systems, characterized by dedicated equipment designed for specific recurring tasks, deliver unmatched throughput capacity and efficiency for standardized, high-volume operations. The category includes technologies such as unit sortation systems, high-speed conveyor networks, and large-scale automated storage and retrieval systems. Fixed automation's established maturity provides reliability advantages and typically lower long-term operating costs at scale. Their dominance reflects the continued importance of core distribution center functions where process stability and maximum throughput efficiency justify dedicated infrastructure investments despite limited flexibility.

By Enterprise Size:

• Large Enterprises

• Small and Medium Enterprises (SMEs)

Small and Medium Enterprises represent the fastest-growing segment by enterprise size, experiencing 31% year-over-year adoption growth as automation technologies become increasingly accessible to operations beyond enterprise scale. This acceleration reflects several converging factors: the emergence of modular automation solutions designed for smaller footprints, the proliferation of robotics-as-a-service business models that convert capital expenditures to operating expenses, and the development of pre-configured systems requiring minimal customization. Cloud-based management systems have eliminated infrastructure barriers that previously limited SME adoption, while simplified implementation methodologies reduce deployment complexity and specialized expertise requirements. The compelling ROI metrics established in enterprise implementations have created confidence among smaller organizations previously hesitant to pioneer automation investments.

Large Enterprises maintain their dominant position by market share, representing approximately 72% of total automation expenditures. This dominance reflects several structural advantages: substantial capital resources enabling comprehensive system implementations, operational scales that magnify efficiency benefits, specialized technical expertise supporting complex implementations, and extensive operational data facilitating sophisticated ROI analysis. Enterprise operations typically maintain dedicated teams focused on continuous improvement initiatives, creating organizational structures well-aligned with automation implementation requirements. The complexity and scale of large enterprise logistics operations create natural alignment with sophisticated automation solutions capable of addressing multiple process challenges simultaneously. Their established technology governance frameworks and change management capabilities create supportive environments for successful automation adoption despite organizational complexity.

Segmentation by Regional Analysis:

• North America

• Europe

• Asia Pacific

• South America

• Middle East and Africa

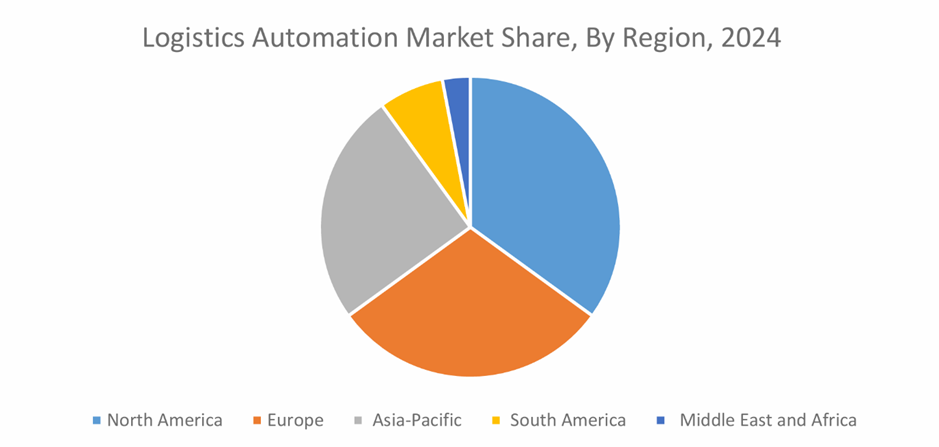

Asia-Pacific commands 27% but is growing fastest at 38% annually as manufacturing hubs modernize their distribution networks. Particularly strong growth is evident in China, India, and Southeast Asia where e-commerce expansion is driving logistics transformation. Latin America represents 8% with significant growth in Brazil and Mexico, while the Middle East and Africa account for 5% with concentrated development in advanced logistics hubs like Dubai and South Africa.

North America maintains its leadership position with 32% market share due to its mature logistics infrastructure, technological innovation capabilities, and acute labor challenges that create compelling automation incentives. The region's highly developed e-commerce market drives continuous investment in fulfillment automation, while the presence of leading technology providers and system integrators facilitates implementation. The concentration of early adopters has created network effects accelerating broader market acceptance as successful implementations demonstrate clear competitive advantages.

COVID-19 Impact Analysis:

The pandemic fundamentally accelerated logistics automation adoption by exposing vulnerabilities in labour-dependent operations and dramatically increasing e-commerce volumes. Health restrictions created unprecedented workforce disruptions while consumer purchasing shifted substantially online, creating dual pressures for greater automation. Organizations with automated systems demonstrated superior resilience, experiencing limited disruption compared to manual operations. This stark contrast prompted many companies to prioritize automation investments as essential for business continuity rather than merely efficiency improvements, permanently altering market growth trajectories and implementation timelines.

Latest Trends and Developments:

Micro-fulfilment centers utilizing dense automation in urban locations are revolutionizing last-mile logistics by positioning inventory closer to consumers. Collaborative robot implementations are expanding rapidly as safety improvements enable human-machine teamwork without physical barriers. Digital twins that create virtual representations of physical facilities allow predictive optimization and scenario testing before physical implementation. Open automation platforms emphasizing interoperability between different manufacturers' components are gaining traction, while subscription-based "automation-as-a-service" models are reducing capital barriers for smaller organizations seeking advanced capabilities without prohibitive upfront investments.

Key Players in the Market:

• Honeywell Intelligrated

• Daifuku Co. Ltd.

• Dematic (KION Group)

• Swisslog (KUKA AG)

• Knapp AG

• SSI Schaefer

• Vanderlande Industries

• Kardex Group

• Material Handling Systems (MHS)

• Bastian Solutions (Toyota Advanced Logistics)

• Murata Machinery

• Beumer Group

• Locus Robotics

• Fetch Robotics (now part of Zebra Technologies)

• Autostores

Chapter 1. Logistics Automation Market – Scope & Methodology

1.1. Market Segmentation

1.2. Assumptions

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Logistics Automation Market – Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.3. COVID-131 Impact Analysis

2.3.1. Impact during 2023 – 2030

2.3.2. Impact on Supply – Demand

Chapter 3. Logistics Automation Market – Competition Scenario

3.1. Market Share Analysis

3.2. Product Benchmarking

3.3. Competitive Strategy & Development Scenario

3.4. Competitive Pricing Analysis

3.5. Supplier - Distributor Analysis

Chapter 4. Logistics Automation Market - Entry Scenario

4.1. Case Studies – Start-up/Thriving Companies

4.2. Regulatory Scenario - By Region

4.3 Customer Analysis

4.4. Porter's Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. Logistics Automation Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Logistics Automation Market - By Component

6.1 Hardware

6.1.1. Automated Storage and Retrieval Systems (AS/RS)

6.1.2. Conveyor Systems

6.1.3. Sortation Systems

6.1.4. Palletizing and Depalletizing Systems

6.1.5. Robotic Picking and Packing Systems

6.1.6. Automated Guided Vehicles (AGVs)

6.1.7. Autonomous Mobile Robots (AMRs)

6.1.8. Industrial Sensors 6.1.9. Barcode and RFID Scanners

6.1.10. Others (Cranes, Carousels, Shuttle Systems)

6.2 Software

6.2.1. Warehouse Management Systems (WMS)

6.2.2. Transportation Management Systems (TMS)

6.2.3. Yard Management Systems (YMS)

6.2.4. Inventory Management Systems

6.2.5. Order Management Systems

6.2.6. Others (Fleet Management, Labor Management Software)

6.3 Services

6.3.1. Consulting

6.3.2. System Integration and Deployment

6.3.3. Support and Maintenance

Chapter 7. Logistics Automation Market - By End-Use Industry

7.1. Retail and E-commerce

7.2. Manufacturing

7.3. Automotive

7.4. Healthcare and Pharmaceuticals

7.5. Food and Beverages

7.6. Aerospace and Defense

7.7. Consumer Electronics

7.8. Logistics and Transportation

7.9. Others (Textiles, Chemicals, Oil & Gas)

Chapter 8. Logistics Automation Market - By Automation Type

8.1. Fixed Automation

8.2. Flexible Automation

Chapter 9. Logistics Automation Market - By Enterprise Size

9.1. Large Enterprises

9.2. Small and Medium Enterprises (SMEs)

Chapter 10. Logistics Automation Market – By Region

10.1. North America

10.2. Europe

10.3. The Asia Pacific

10.4. Latin America

10.5. Middle East and Africa

Chapter 11. Logistics Automation Market – Company Profiles – (Overview, Product Portfolio, Financials, Developments)

11.1. Honeywell Intelligrated

11.2. Daifuku Co. Ltd.

11.3. Dematic (KION Group)

11.4. Swisslog (KUKA AG)

11.5. Knapp AG

11.6. SSI Schaefer

11.7. Vanderlande Industries

11.8. Kardex Group

11.9. Material Handling Systems (MHS)

11.10. Bastian Solutions (Toyota Advanced Logistics)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Surging e-commerce demand, rising labor shortages, and the need for faster, more accurate fulfillment are pushing companies to automate supply chains rapidly.

High initial costs, integration complexity with legacy systems, and workforce resistance to change are the major hurdles.

Companies like Honeywell Intelligrated, Daifuku Co., Dematic, Swisslog, Knapp AG, and SSI Schaefer lead the market with advanced automation technologies.

North America currently leads, backed by a mature logistics infrastructure and early adoption of automation technologies.

Asia-Pacific is expanding rapidly, driven by booming e-commerce in countries like China, India, and Southeast Asia.