Hyper-Converged Infrastructure Market Research Report -- Segmentation by Component (Hardware, Software); By Organization Size (Small and Medium Enterprises, Large Enterprises); By Application (Data Centre Consolidation, Virtualization, Remote Office/Branch Office, Virtual Desktop Infrastructure, Backup and Disaster Recovery, Others); By End-User (IT & Telecom, Healthcare, Government, Manufacturing, Education, Others); Region - Forecast (2025 - 2030)

Published: 2024 - January

Report Code: IM-1022

Format:

Region: Global

Market Size and Overview:

The Global Hyper-Converged Infrastructure Market was valued at USD 15.73 billion in 2024 and is projected to reach a market size of USD 44.47 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.1%.

Hyper-Converged Infrastructure (HCI) is a software-defined IT infrastructure that virtualizes all elements of conventional hardware-defined systems including storage, compute, and networking. This revolutionary approach to data center architecture has gained significant momentum in the 21st century as organizations seek to simplify IT management while reducing costs and improving scalability. With the continuous evolution of digital transformation initiatives, the demand for simplified, software-defined infrastructure solutions is rapidly increasing and is anticipated to create substantial opportunities across various industries including healthcare, education, government, and enterprise sectors.

Key Market Insights:

According to a comprehensive survey conducted by Gartner in 2022, approximately 73% of IT leaders reported that HCI solutions reduced their infrastructure management time by an average of 47%, leading to significant operational cost savings.

Research from IDC reveals that enterprises deploying hyper-converged infrastructure solutions achieved an average ROI of 269% within three years of implementation. The study also indicated that 68% of organizations experienced deployment times of less than 30 minutes for new virtual machines, compared to several hours with traditional infrastructure approaches, demonstrating substantial improvements in operational agility and time-to-market capabilities.

A 2023 industry analysis involving 1,200 enterprise IT executives found that 81% of organizations using HCI reported improved disaster recovery capabilities, with average recovery time objectives decreasing by 65%.

Market intelligence data from Dell Technologies indicates that the average HCI deployment supports approximately 150% more virtual machines per physical node compared to traditional infrastructure configurations. This increased density translates to significant capital expenditure savings, with organizations reporting an average 42% reduction in hardware acquisition costs when transitioning from legacy infrastructure to hyper-converged solutions for equivalent workload capacities.

Hyper-Converged Infrastructure Market Drivers:

The growing complexity of traditional IT infrastructure management and the increasing demand for simplified, scalable solutions are fundamentally driving the adoption of hyper-converged infrastructure across diverse organizational environments.

Traditional IT infrastructure architectures require specialized expertise across multiple domains including storage area networks, server administration, and network configuration, creating substantial operational complexity and resource requirements. Organizations typically employ dedicated teams for each infrastructure component, resulting in siloed operations, increased staffing costs, and potential integration challenges between different system components. Hyper-converged infrastructure addresses these challenges by consolidating compute, storage, and networking into a single, software-defined platform that can be managed through unified interfaces. The software-defined nature of HCI platforms also enables policy-based automation that reduces manual configuration errors by approximately 67% compared to traditional infrastructure approaches. Additionally, the modular architecture of HCI solutions allows organizations to scale infrastructure resources incrementally based on actual demand rather than over-provisioning for peak capacity requirements. This approach to capacity planning has enabled organizations to reduce initial capital expenditures by an average of 35% while maintaining the flexibility to expand as business requirements evolve. Furthermore, the standardized architecture of HCI platforms reduces vendor dependency and enables organizations to implement consistent operational procedures across multiple data centre locations, improving operational consistency and reducing training requirements for IT staff.

The accelerating digital transformation initiatives and the increasing adoption of edge computing architectures are propelling significant growth in the hyper-converged infrastructure market.

Digital transformation projects require agile, scalable infrastructure that can rapidly adapt to changing business requirements and support modern application architectures including containerized workloads and microservices implementations. HCI platforms provide the flexibility and performance characteristics necessary to support these dynamic environments while maintaining operational simplicity. Research indicates that organizations implementing digital transformation initiatives experience 43% faster application deployment cycles when utilizing HCI compared to traditional infrastructure approaches. The distributed nature of modern business operations, accelerated by remote work trends, has also created substantial demand for edge computing capabilities that can deliver consistent performance and management experiences across geographically dispersed locations. HCI solutions excel in these scenarios by providing standardized infrastructure building blocks that can be deployed and managed centrally while delivering local computing resources.

Hyper-Converged Infrastructure Market Restraints and Challenges:

Despite its compelling advantages, the hyper-converged infrastructure market faces several significant challenges that could impact its growth trajectory. Vendor lock-in concerns remain a primary barrier, as organizations worry about becoming dependent on single-vendor solutions that may limit future flexibility and negotiating power. Technical integration challenges persist when connecting HCI platforms with existing legacy systems, often requiring substantial migration efforts and potential application modifications. Performance limitations can occur in highly specialized workloads, particularly those requiring extreme compute density or specialized hardware accelerators that may not be available in standard HCI configurations. Additionally, the initial learning curve associated with software-defined infrastructure management can be steep for organizations with traditional infrastructure expertise, necessitating significant training investments and potentially temporary productivity impacts during transition periods.

Hyper-Converged Infrastructure Market Opportunities:

The hyper-converged infrastructure market presents substantial growth opportunities across multiple dimensions as organizations continue their digital transformation journeys. Edge computing applications represent a particularly promising area, with 5G network deployments and IoT proliferation creating demand for distributed computing resources that can be managed centrally while operating autonomously. The growing adoption of artificial intelligence and machine learning workloads creates opportunities for HCI vendors to develop specialized solutions optimized for these compute-intensive applications. Small and medium enterprises represent a largely untapped market segment, with cloud-like consumption models and managed services making HCI solutions increasingly accessible to organizations with limited IT resources. Industry-specific solutions present additional opportunities, particularly in healthcare where regulatory compliance requirements and data sovereignty concerns favor on-premises infrastructure with cloud-like operational characteristics.

Hyper-Converged Infrastructure Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

The software segment dominated the global hyper-converged infrastructure market with approximately 64.2% revenue share. This dominance reflects the software-defined nature of HCI solutions, where the majority of value and differentiation comes from the management, orchestration, and virtualization software layers rather than the underlying hardware components. Leading HCI vendors have focused their development efforts on creating comprehensive software platforms that can operate across diverse hardware configurations, enabling greater flexibility and reduced vendor dependence for customers.

The hardware segment, while smaller in terms of revenue percentage, remains critical to HCI deployments and is projected to grow at a steady CAGR of 19.8% during the forecast period. This growth is driven by increasing performance requirements for modern workloads, the adoption of NVMe storage technologies, and the integration of specialized processors such as GPUs for AI and machine learning applications. Appliance-based HCI solutions, which bundle optimized hardware with software, continue to be popular among organizations seeking turnkey solutions with vendor-supported hardware configurations.

Market Segmentation: By Organization Size

• Small and Medium Enterprises (SMEs)

• Large Enterprises

Large enterprises accounted for approximately 71.3% of the hyper-converged infrastructure market share in 2022, driven by their complex IT environments, substantial infrastructure investments, and early adoption of emerging technologies. These organizations typically deploy HCI solutions for data center consolidation, disaster recovery, and remote office applications, with average deployment sizes significantly larger than SME implementations. Large enterprises also drive demand for advanced features such as multi-site management, integrated backup solutions, and enterprise-grade security capabilities.

The SME segment is projected to experience the highest growth rate during the forecast period, with a CAGR of 26.7%. This accelerated growth is attributed to the increasing availability of entry-level HCI solutions with simplified management interfaces and consumption-based pricing models that make advanced infrastructure capabilities accessible to smaller organizations. Cloud-like operational models and managed services are particularly appealing to SMEs that lack dedicated infrastructure expertise, enabling them to achieve enterprise-grade capabilities without substantial internal resource investments.

Market Segmentation: By Application

• Data Center Consolidation

• Virtualization

• Remote Office/Branch Office (ROBO)

• Virtual Desktop Infrastructure (VDI)

• Backup and Disaster Recovery

• Others

Data center consolidation emerged as the largest application segment, accounting for 28.6% of the market share. Organizations are leveraging HCI solutions to reduce their physical data center footprint while maintaining or improving application performance and availability. This consolidation enables significant cost savings in real estate, power consumption, and cooling requirements while simplifying infrastructure management through unified platforms.

The Remote Office/Branch Office segment is projected to grow at the fastest CAGR of 27.4% during the forecast period. This growth is driven by the distributed nature of modern business operations and the need for consistent IT services across multiple locations. HCI solutions excel in ROBO deployments by providing enterprise-grade capabilities in compact form factors that can be managed remotely, reducing the need for local IT expertise while ensuring reliable operations across geographically dispersed sites.

Market Segmentation: By End-User

• IT & Telecom

• Healthcare

• Government

• Manufacturing

• Education

• Others

The IT & Telecom sector dominated the hyper-converged infrastructure market in 2022 with a 31.7% share, reflecting these organizations' sophisticated infrastructure requirements and early adoption of software-defined technologies. Telecom companies, in particular, are deploying HCI solutions to support network function virtualization initiatives and edge computing applications that require distributed infrastructure with centralized management capabilities.

Healthcare represents the fastest-growing end-user segment with a projected CAGR of 28.9% during the forecast period. This growth is driven by increasing digitization of healthcare records, the adoption of medical imaging systems that require high-performance storage, and regulatory requirements that favor on-premises infrastructure with robust security and compliance capabilities. Healthcare organizations also benefit from HCI's simplified management model, which reduces the IT expertise required to maintain critical healthcare applications and systems.

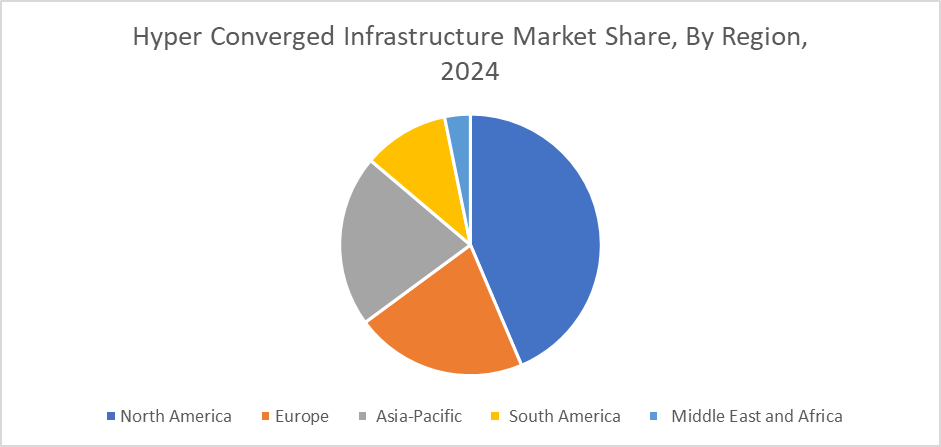

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America maintained its leadership position in the global hyper-converged infrastructure market in 2024, accounting for 41.8% of the total market share. This dominance is attributed to the region's advanced IT infrastructure, high adoption rates of emerging technologies, and the presence of major HCI solution providers. The United States, in particular, has seen strong adoption across multiple sectors including healthcare, education, and government, with federal agencies increasingly standardizing on HCI platforms for their infrastructure modernization initiatives.

The Asia-Pacific region is anticipated to witness the highest growth rate during the forecast period, with a CAGR of 26.3%. This accelerated growth is driven by rapid digital transformation initiatives across emerging economies, substantial investments in data center infrastructure, and increasing adoption of cloud-like technologies among enterprises. Countries such as China, India, and Japan are experiencing particularly strong demand for HCI solutions as organizations seek to modernize their IT infrastructure while maintaining local data sovereignty and control

COVID-19 Impact Analysis on the Global Hyper-Converged Infrastructure Market:

The COVID-19 pandemic initially created uncertainty in IT infrastructure spending as organizations focused on immediate operational continuity challenges. However, the crisis ultimately accelerated HCI adoption as organizations recognized the importance of agile, easily manageable infrastructure for supporting remote work and distributed operations. The pandemic highlighted the limitations of traditional infrastructure approaches that required on-site management and complex maintenance procedures, making the remote management capabilities of HCI solutions particularly valuable. Healthcare organizations, in particular, accelerated their HCI deployments to support telemedicine initiatives, remote patient monitoring, and the rapid scaling of digital health services.

Latest Trends/ Developments:

The integration of artificial intelligence and machine learning capabilities directly into HCI platforms is transforming infrastructure management through predictive analytics, automated optimization, and intelligent resource allocation.

Leading vendors are incorporating AI-driven features that can automatically detect performance anomalies, predict hardware failures, and optimize resource utilization without human intervention, significantly reducing operational overhead and improving system reliability.

Container orchestration and Kubernetes integration have become standard features in modern HCI platforms, enabling organizations to support cloud-native applications alongside traditional virtualized workloads.

Key Players:

• Nutanix, Inc.

• VMware, Inc. (Broadcom)

• Dell Technologies Inc.

• Hewlett Packard Enterprise

• Cisco Systems, Inc.

• Lenovo Group Limited

• Huawei Technologies Co., Ltd.

• NetApp, Inc.

• Hitachi Vantara

• Scale Computing

Chapter 1. Hyper-Converged Infrastructure Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Hyper-Converged Infrastructure Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Hyper-Converged Infrastructure Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Hyper-Converged Infrastructure Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Hyper-Converged Infrastructure Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Hyper-Converged Infrastructure Market – By Component

6.1. Hardware

6.2. Software

Chapter 7. Hyper-Converged Infrastructure Market – By Organization Size

7.1. Small and Medium Sized Enterprises (SME)

7.2. Large Enterprises

Chapter 8. Hyper-Converged Infrastructure Market – By Application

8.1. Data Centre Consolidation

8.2. Virtualization

8.3. Remote Office/Branch Office

8.4. Virtual Desktop Infrastructure

8.5. Backup and Disaster Recovery

8.6. Absolute $ Opportunity Analysis By Size, 2024-2030

Chapter 9. Hyper-Converged Infrastructure Market – By End User

9.1. Telecom

9.2. Healthcare

9.3. Government

9.4. Manufacturing

9.5. Education

9.6. Others

Chapter 10. Hyper-Converged Infrastructure Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Organization Size

10.1.4. By Application

10.1.5 By End user

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Organization Size

10.2.4. By Application

10.2.5 By End user

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Organization Size

10.3.4. By Application

10.3.5 By End user

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Organization Size

10.4.4. By Application

10.4.5 By End user

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Organization Size

10.5.4. By Application

10.5.5 By End user

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Hyper-Converged Infrastructure Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Nutanix, Inc.

11.2. VMware, Inc. (Broadcom)

11.3. Dell Technologies Inc.

11.4. Hewlett Packard Enterprise

11.5. Cisco Systems, Inc.

11.6. Lenovo Group Limited

11.7. Huawei Technologies Co., Ltd.

11.8. NetApp, Inc.

11.9. Hitachi Vantara

11.10. Scale Computing

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Hyper-Converged Infrastructure Market was valued at USD 15.73 billion in 2024 and is projected to reach a market size of USD 44.47 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.1%.

The growing complexity of traditional IT infrastructure management and the increasing demand for simplified, scalable solutions are the primary drivers propelling the global hyper-converged infrastructure market.

Based on Component, the Global Hyper-Converged Infrastructure Market is segmented into Hardware and Software.

North America is the most dominant region for the Global Hyper-Converged Infrastructure Market.

Nutanix Inc., VMware Inc., Dell Technologies Inc., and Hewlett Packard Enterprise are the key players operating in the Global Hyper-Converged Infrastructure Market.