Healthcare IT Market Research Report – Segmentation by Product Type (Healthcare Provider Solutions, Healthcare Payer Solutions, HCIT Outsourcing Services); By End-User (Healthcare Providers, Healthcare Payers); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-2536

Format:

Region: Global

Market Size and Overview:

The Healthcare IT Market was valued at USD 334.22 billion and is projected to reach a market size of USD 701.8 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 15.9%.

Healthcare Information Technology (IT) represents a rapidly evolving industry that has witnessed transformative advancements in the 21st Century. With the rising need for efficient healthcare delivery systems and the increasing digitization of medical records and procedures, healthcare IT has become indispensable for modern healthcare operations. The continuous development of technological solutions has attracted both academic and professional communities, creating unprecedented opportunities for innovation and improvement in healthcare delivery while addressing critical challenges related to patient care, operational efficiency, and cost management.

Key Market Insights:

According to the Healthcare Information and Management Systems Society (HIMSS) survey, approximately 76% of healthcare providers have invested significantly in electronic health record (EHR) systems, representing a 15% increase from 2019, indicating growing confidence in digital transformation despite implementation challenges.

The North American region currently accounts for 38% of global healthcare IT expenditure, with the United States and Canada collectively representing 31% of the global market share, attributed to favorable governmental regulations, advanced healthcare infrastructure, and early technology adoption among healthcare providers.

Implementation of artificial intelligence and machine learning solutions in healthcare diagnostics has demonstrated accuracy improvements of 22% in early disease detection and reduced diagnostic time by 35% according to the American Medical Informatics Association's 2022 report, driving increased investment in these technologies.

Cloud-based healthcare solutions have shown operational cost reductions of 26% and data accessibility improvements of 41% in comparative studies across 230 healthcare facilities, making them increasingly attractive alternatives to traditional on-premise systems for both large hospital networks and smaller independent practices.

Healthcare IT Market Drivers:

The increasing demand for improved patient outcomes, enhanced operational efficiency, and regulatory compliance requirements are driving unprecedented investments in healthcare IT solutions across global markets.

Healthcare providers worldwide are experiencing mounting pressure to deliver superior patient care while simultaneously reducing operational costs, a challenge that has catalyzed the adoption of comprehensive IT solutions. According to the Institute for Healthcare Improvement, healthcare organizations implementing integrated IT systems have reported average patient satisfaction improvements of 31% alongside administrative efficiency gains of 27%. The proliferation of chronic diseases, which now affect approximately 45% of the global population according to WHO estimates, necessitates more sophisticated disease management tools capable of tracking long-term patient conditions and treatment efficacy. Electronic health record adoption has reached critical mass in developed markets with implementation rates exceeding 89% in the United States and 84% across Western Europe, creating robust digital ecosystems that can support increasingly advanced applications. Regulatory mandates for data security, patient privacy, and standardized reporting have compelled healthcare organizations to invest approximately $36.5 billion annually in compliance-related IT infrastructure, representing 17% of total healthcare IT expenditure. The integration of artificial intelligence with clinical decision support systems has demonstrated diagnostic accuracy improvements of 19-27% across multiple specialties while reducing clinical decision time by an average of 31%, compelling forward-thinking healthcare providers to accelerate technological adoption.

The growing emphasis on interoperability, data analytics, and personalized healthcare is revolutionizing healthcare IT investment priorities across the provider landscape.

Healthcare data generation has increased exponentially, with the average hospital now producing 50 petabytes of data annually according to the Healthcare Information and Management Systems Society, creating unprecedented opportunities for organizations capable of effectively analyzing and utilizing this information. Interoperability challenges between disparate healthcare systems result in approximately $77.8 billion in unnecessary healthcare expenditure annually through duplicated tests, delayed treatments, and administrative inefficiencies, making integration solutions one of the fastest-growing segments within healthcare IT. Personalized medicine approaches, which leverage genomic information and comprehensive patient histories to tailor treatment plans, have demonstrated treatment efficacy improvements of 28-42% across multiple therapeutic areas, driving investment in IT systems capable of supporting precision healthcare initiatives.

Healthcare IT Market Restraints and Challenges:

Despite substantial growth potential, the healthcare IT market faces significant challenges that impact adoption rates and implementation success. The substantial initial investment required for comprehensive healthcare IT systems represents a major barrier, particularly for smaller healthcare providers and facilities in developing regions, with enterprise-level EHR implementations averaging $14.5 million for mid-sized hospitals. Integration complexity with legacy systems presents another substantial challenge, with 61% of healthcare CIOs reporting significant technical difficulties when attempting to connect modern solutions with established infrastructure. Data security and privacy concerns have intensified as healthcare data breaches increased by 42% in 2022, with the average breach costing healthcare organizations $10.1 million according to IBM Security reports. Clinician resistance to technological change remains problematic, with 47% of physicians reporting EHR-related professional dissatisfaction and 38% attributing burnout partially to documentation requirements.

Healthcare IT Market Opportunities:

The integration of emerging technologies like artificial intelligence, blockchain, and Internet of Medical Things (IoMT) presents unprecedented growth opportunities, with the AI healthcare segment alone projected to reach $188.4 billion by 2030. Developing economies offer substantial untapped markets, with digital health adoption rates below 30% in many regions compared to over 75% in developed nations, creating significant expansion potential as healthcare infrastructure modernizes. Government initiatives promoting healthcare digitization have allocated approximately $27.6 billion globally in 2022, creating favorable conditions for market expansion across both public and private healthcare sectors. Remote patient monitoring technologies demonstrated clinical efficacy through 22% reductions in hospital readmissions and 31% decreases in emergency department visits, driving accelerated adoption across chronic disease management programs. The emergence of value-based care models, implemented in various forms across 37 countries, necessitates sophisticated analytics capabilities to track and optimize performance metrics, creating sustained demand for advanced healthcare IT solutions.

Healthcare IT Market Segmentation:

Market Segmentation: By Product Type:

• Healthcare Provider Solutions

• Healthcare Payer Solutions

• HCIT Outsourcing Services

Based on product type, the Healthcare Provider Solutions segment dominated the market with approximately 46.3% revenue share. This dominance stems from the essential role these solutions play in direct patient care delivery, clinical documentation, and operational management across healthcare facilities of all sizes. Electronic Health Record (EHR) systems, which form the foundation of provider solutions, have reached implementation rates exceeding 89% in developed markets, while clinical decision support systems demonstrated diagnostic accuracy improvements of 22% and treatment protocol adherence increases of 17.5% in comparative studies across multiple specialties.

The HCIT Outsourcing Services segment is projected to grow at the highest CAGR of 21.7% during the forecast period. This accelerated growth is driven by healthcare organizations increasingly focusing on core clinical activities while delegating specialized IT functions to dedicated service providers. Outsourcing arrangements have demonstrated average operational cost reductions of 31% compared to in-house IT management while providing access to specialized expertise that would be prohibitively expensive to maintain internally. Cloud-based service models, which constitute approximately 64% of healthcare IT outsourcing arrangements, offer scalability and flexibility that internal IT departments often struggle to provide, further accelerating adoption across healthcare organizations seeking to optimize resource allocation.

Market Segmentation: By End-User

• Healthcare Providers

• Healthcare Payers

The Healthcare Providers segment held the largest market share at 58.7% in 2022, reflecting the comprehensive technology requirements of hospitals, clinics, physician practices, and other direct care delivery organizations. Provider organizations face complex challenges related to clinical documentation, regulatory compliance, patient engagement, and operational efficiency that necessitate substantial IT investments across multiple functional areas. Hospitals implementing comprehensive healthcare IT systems reported average operational efficiency improvements of 26% and clinical outcome enhancements of 19% according to a 2022 American Hospital Association analysis, establishing clear return-on-investment metrics that support continued technology adoption.

The Healthcare Payers segment is anticipated to witness significant growth during the forecast period, with a projected CAGR of 18.9%. Insurance companies and managed care organizations face intensifying pressure to improve administrative efficiency, enhance member engagement, reduce fraud, and optimize claims processing through technological innovation. Advanced analytics solutions deployed by payer organizations have demonstrated fraud detection improvements of 33% while reducing administrative costs by an average of 22% according to the Healthcare Financial Management Association. The growing prevalence of value-based care arrangements, which now impact approximately 63% of insured lives in developed markets, requires sophisticated data exchange and analytics capabilities between payers and providers, driving increased investment in interoperability solutions and shared analytical platforms.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

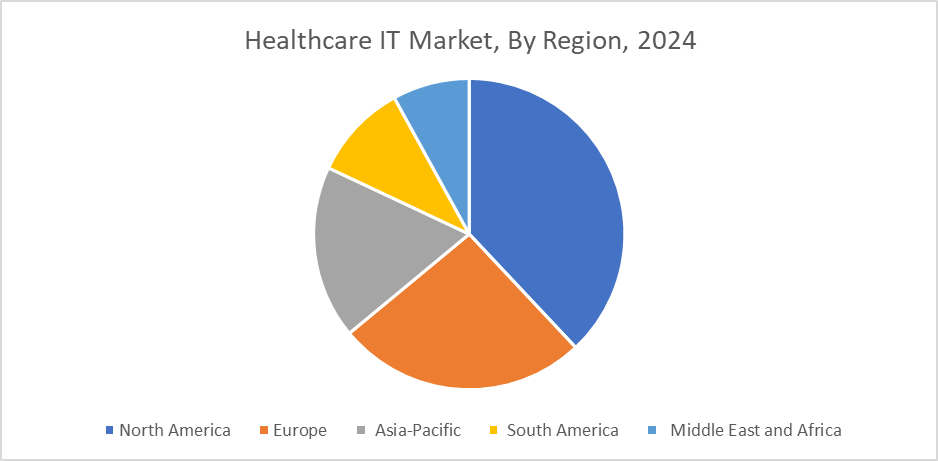

North America dominated the global healthcare IT market with a revenue share of 38.4%. This dominance is attributed to advanced healthcare infrastructure, substantial technology investments, and favorable regulatory environments that promote digital health adoption. The United States accounts for approximately 84% of regional healthcare IT expenditure, with implementation rates for critical technologies such as EHR systems reaching 92% among hospitals and 78% among independent physician practices. Additionally, federal initiatives including the 21st Century Cures Act and HITECH Act have allocated over $35 billion toward healthcare digitization efforts, creating robust incentives for continued technology adoption.

The Asia-Pacific region is projected to experience the highest growth rate during the forecast period, with an anticipated CAGR of 24.6%. Rapidly developing healthcare infrastructure, increasing government investments in digital health initiatives, and the expansion of private healthcare systems are driving accelerated technology adoption across the region. Countries including China, India, Japan, and South Korea have established national healthcare digitization strategies with collective investments exceeding $17.5 billion between 2022-2025. Rising healthcare expenditure, which increased at an average annual rate of 9.7% across the region over the past five years, provides the financial foundation for sustained technology investment. Additionally, the region's large population base and growing middle class are creating unprecedented demand for improved healthcare services that can only be efficiently delivered through technology-enabled systems.

COVID-19 Impact Analysis on the Global Healthcare IT Market:

The COVID-19 pandemic triggered unprecedented acceleration in healthcare IT adoption across all market segments, with telehealth utilization increasing by over 4,300% during peak pandemic periods according to the American Medical Association. Healthcare organizations rapidly deployed remote care technologies, with 78% of providers implementing or expanding telehealth solutions within the first six months of the pandemic. Regulatory barriers to digital health adoption were temporarily removed or permanently modified in 93% of developed markets, creating favorable conditions for technology experimentation and implementation that have largely persisted beyond the acute crisis phase.

The pandemic simultaneously exposed critical weaknesses in existing healthcare information systems, particularly related to interoperability, data analytics, and public health surveillance capabilities. Approximately 67% of healthcare executives reported significant challenges sharing clinical information between organizations during the pandemic according to a 2022 Black Book Research survey.

Latest Trends/ Developments:

The integration of artificial intelligence across healthcare applications has accelerated dramatically, with 76% of healthcare organizations now utilizing AI in at least one clinical or administrative function according to KLAS Research, representing a 32% increase from 2021 and creating unprecedented demand for advanced analytics platforms capable of supporting increasingly sophisticated AI applications.

Epic Systems' 2022 partnership with Microsoft to integrate Azure-based AI capabilities into its widely-used EHR platform exemplifies the accelerating convergence between established healthcare IT vendors and technology giants, creating comprehensive ecosystems that combine clinical expertise with advanced technical capabilities while significantly expanding the practical applications of artificial intelligence in routine healthcare operations.

The rapid evolution of remote patient monitoring technologies has established a dynamic market segment growing at 28.9% annually, with solutions incorporating IoT sensors, mobile applications, and predictive analytics demonstrating clinical outcome improvements of 31%.

Key Players:

• Cerner Corporation (Oracle)

• Epic Systems Corporation

• Allscripts Healthcare Solutions

• McKesson Corporation

• Philips Healthcare

• GE Healthcare

• Siemens Healthineers

• Athenahealth

• InterSystems Corporation

• NextGen Healthcare

• eClinicalWorks

• Medtronic

• IBM Watson Health

Chapter 1. HEALTHCARE IT MARKET – Scope & Methodology

1.1. Market Segmentation

1.2. Assumptions

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. HEALTHCARE IT MARKET – Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.3. COVID-19 Impact Analysis

2.3.1. Impact during 2023 – 2030

2.3.2. Impact on Supply – Demand

Chapter 3. HEALTHCARE IT MARKET – Competition Scenario

3.1. Market Share Analysis

3.2. Product Benchmarking

3.3. Competitive Strategy & Development Scenario

3.4. Competitive Pricing Analysis

3.5. Supplier - Distributor Analysis

Chapter 4. HEALTHCARE IT MARK ET - Entry Scenario

4.1. Case Studies – Start-up/Thriving Companies

4.2. Regulatory Scenario - By Region

4.3 Customer Analysis

4.4. Porter's Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. HEALTHCARE IT MARKET - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. HEALTHCARE IT MARKET – By Business Segment

6.1 Laboratory Information Systems (LIS)

6.2. Picture Archiving and Communication System (PACS) and Vendor Neutral Archive (VNA)

6.3. Radiology Information Systems (RIS)

6.4. Electronic Health Records (EHR)

6.5. Telemedicine

6.6. Clinical Decision Support System (CDSS)

6.7. Claims Management Solutions

6.8. Population Health Management Solutions

6.9. Fraud Analytics

6.10. Provider Management Services

6.11. Billing and Accounts Management Services

6.12. Other Business Segments

Chapter 7. HEALTHCARE IT MARKET – By Component

7.1. Software

7.2. Hardware

7.3. Services

Chapter 8. HEALTHCARE IT MARKET – By Delivery Mode

8.1 On-premise

8.2. Cloud-based

Chapter 9. HEALTHCARE IT MARKET –By End User

9.1 Payers

9.2. Providers

Chapter 10. HEALTHCARE IT MARKET – By Region

10.1. North America

10.2. Europe

10.3.The Asia Pacific

10.4.Latin America

10.5. Middle-East and Africa

Chapter 11. HEALTHCARE IT MARKET– Company Profiles – (Overview, Product Portfolio, Financials, Developments)

11.1. Company 1

11.2. Company 2

11.3. Company 3

11.4. Company 4

11.5. Company 5

11.6. Company 6

11.7. Company 7

11.8. Company 8

11.9. Company 9

11.10. Company 10

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

It includes digital technologies, software, and systems that support healthcare services, data management, and patient care delivery.

Major components include electronic health records (EHR), telemedicine, healthcare analytics, cybersecurity, and patient engagement tools.

It improves efficiency, enhances patient outcomes, enables remote care, reduces costs, and ensures better data accuracy and accessibility.

Trends include AI integration, cloud-based health solutions, wearable tech, data interoperability, and blockchain for secure records.

Leading companies include Cerner, Epic Systems, Allscripts, Oracle Health, and GE Healthcare.