Green Methanol Market Research Report – Segmentation by Production Technology (Bio-methanol, E-methanol, Waste-to-methanol, Mixed sources); By End-Use Application (Maritime fuel, Chemical production, Automotive fuel, Power generation, Industrial heating); By Purity Grade (Fuel grade, Chemical grade, Technical grade, Research grade); By Feedstock Source (Dedicated biomass crops, Agricultural/forestry residues, Municipal solid waste, Industrial waste gases, Direct air capture CO₂, Point source CO₂ capture); Region – Forecast (2025 – 2030)

Published: 2025 - April

Report Code: IM-16451

Format:

Region: Global

Green Methanol Market Size (2025 – 2030)

The Green Methanol Market was valued at USD 1.95 Billion in 2024 and is projected to reach a market size of USD 7.25 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 30.04%.

Market Size and Overview:

Green methanol represents a significant advancement in sustainable fuel alternatives, emerging as a crucial component in the global transition toward carbon neutrality. Unlike conventional methanol derived from fossil fuels, green methanol is produced using renewable feedstocks such as biomass, municipal waste, or through innovative power-to-X technologies that utilize renewable electricity, water, and captured carbon dioxide. This environmentally responsible production pathway positions green methanol as a vital solution for reducing greenhouse gas emissions across multiple industries, including maritime shipping, automotive, power generation, and chemical manufacturing. The green methanol market has witnessed remarkable expansion in 2024, driven primarily by stringent environmental regulations worldwide and increasing corporate commitments to decarbonization.

Key Market Insights:

Current global production capacity stands at 4.2 million metric tons annually, though actual production volumes hover around 2.8 million metric tons due to various operational factors. In maritime shipping, green methanol fuels over 75 vessels globally, with orders for an additional 130 methanol-capable ships placed this year. European manufacturers account for 42% of global green methanol production, establishing the region as the manufacturing epicenter. The average production cost of green methanol has decreased by 18% compared to 2023, now ranging between $670-800 per ton depending on the production pathway and location.

Market Drivers:

Stringent Maritime Emissions Regulations

The maritime industry faces unprecedented regulatory pressure to reduce its environmental footprint, catalyzing significant demand for green methanol as a compliant marine fuel. The International Maritime Organization's revised strategy aims to reduce greenhouse gas emissions from international shipping by at least 40% by 2030 and 70% by 2050 compared to 2008 levels, with aspirations to achieve net-zero emissions by approximately 2050. These ambitious targets have prompted major shipping companies to actively seek alternative fuels, with green methanol emerging as a preferred option due to its compatibility with existing infrastructure after minor modifications. Unlike other alternative fuels, green methanol can be stored in conventional tanks and requires less dramatic retrofitting of engines. Additionally, regional regulations such as the European Union's inclusion of maritime emissions in its Emissions Trading System (EU ETS) and the FuelEU Maritime Initiative have created immediate financial incentives for shipping companies to transition to lower-carbon fuels. The accessibility of green methanol and its demonstrable carbon reduction benefits have positioned it as an increasingly attractive solution for compliance with these multifaceted regulatory frameworks.

Expanding Industrial Decarbonization Commitments

Corporate sustainability commitments have evolved from optional initiatives to strategic imperatives, driving substantial interest in green methanol across diverse industries. Major chemical manufacturers have established science-based targets to reduce Scope 1 and 2 emissions, necessitating the adoption of low-carbon feedstocks like green methanol in their production processes. Similarly, consumer goods companies seeking to address Scope 3 emissions are pressuring their supply chains to incorporate renewable inputs, including materials derived from green methanol. This pressure extends to automotive manufacturers exploring alternative fuel options and power generation companies seeking cleaner methanol as a dispatchable generation resource that complements intermittent renewable sources. The financial implications of these commitments have intensified as investors increasingly incorporate ESG metrics into their assessment frameworks, making access to capital more favorable for companies demonstrating concrete decarbonization actions. This combination of customer expectations, investor pressure, and internal corporate targets has created robust demand signals that support the expansion of green methanol production capacity despite its current cost premium over conventional alternatives.

Market Restraints and Challenges:

The green methanol market continues to face significant cost barriers despite recent improvements, with production costs averaging 35-65% higher than conventional methanol depending on technology pathway. Limited availability of sustainable feedstocks, particularly for bio-methanol, constrains rapid capacity expansion in certain regions. Infrastructure adaptation requirements, including specialized storage and handling facilities, present additional financial hurdles. Competition from alternative low-carbon fuels and technologies, particularly in the transportation sector, creates market uncertainty that can delay investment decisions and slow adoption rates.

Market Opportunities:

Technological advancements in electrolysis and carbon capture are rapidly improving production economics, potentially enabling cost parity with fossil methanol in favorable regions within 3-5 years. Integration with existing industrial clusters that generate biogenic CO2 or hydrogen presents immediate deployment opportunities with reduced infrastructure requirements. Growing political support for carbon-neutral fuels has created favorable policy environments in major markets, including carbon pricing mechanisms that improve competitiveness. The versatility of green methanol across multiple applications (fuel, chemical feedstock, energy storage) allows producers to target premium markets while achieving scale economies.

Market Segmentation:

Segmentation by Production Technology:

• Bio-methanol (biomass gasification)

• E-methanol (renewable hydrogen with captured CO2)

• Waste-to-methanol

• Mixed sources

Bio-methanol dominates the current market with 63% share due to its relatively lower production costs and established technology pathway. Utilizing sustainable biomass feedstocks including agricultural residues, forest residues, and municipal solid waste, this production route benefits from existing gasification technologies that have been optimized over decades. Regional biomass availability strongly influences production distribution, with Scandinavian countries leveraging forestry resources particularly effectively.

E-methanol, produced by combining green hydrogen from renewable-powered electrolysis with captured carbon dioxide, represents the fastest-growing segment with 84% year-over-year capacity growth. This pathway benefits from rapidly declining renewable electricity and electrolyzer costs, while offering the advantage of precise carbon accounting. Recent technological breakthroughs in catalyst efficiency have significantly improved conversion rates, further enhancing economic viability in regions with abundant renewable energy resources.

Segmentation by End-Use Application:

• Maritime fuel

• Chemical production

• Automotive fuel

• Power generation

• Industrial heating

Chemical production applications dominate green methanol consumption, accounting for 46% of market volume. This dominance stems from the established position of methanol as an essential building block for numerous chemical derivatives, including formaldehyde, acetic acid, DME, and various plastics. Chemical producers have demonstrated willingness to absorb the green premium to reduce product carbon footprints, particularly for consumer-facing goods where sustainability marketing creates value.

Maritime fuel represents the fastest-growing application segment with 107% annual growth as shipping companies rapidly adopt green methanol to comply with emissions regulations. The IMO's carbon intensity targets have catalyzed major fleet conversion initiatives, with several container shipping giants placing substantial orders for methanol-capable vessels. The relative ease of adopting methanol compared to other alternative fuels—requiring only moderate engine and fuel system modifications—has accelerated this transition.

Segmentation by Purity Grade:

• Fuel grade (95-97%)

• Chemical grade (99%+)

• Technical grade (97-99%)

• Research grade (99.9%+)

Fuel grade green methanol commands 58% market share, dominating due to substantial volume requirements in maritime and automotive applications. This grade prioritizes energy content and combustion characteristics over absolute purity, allowing for cost-effective production processes that focus on carbon intensity reduction rather than removing final trace impurities. The broader specification tolerances enable producers to optimize production economics while maintaining performance characteristics necessary for fuel applications.

Chemical grade green methanol is expanding at 64% annually, driven by increasing demand for high-purity inputs for specialty chemical applications. This premium segment requires methanol exceeding 99% purity with strictly controlled impurity profiles suitable for pharmaceutical intermediates, advanced materials, and electronics applications. The substantial value-add in these downstream products enables manufacturers to absorb the combined premiums of both sustainability and higher purity specifications.

Segmentation by Feedstock Source:

• Dedicated biomass crops

• Agricultural/forestry residues

• Municipal solid waste

• Industrial waste gases

• Direct air capture CO2

• Point source CO2 capture

Agricultural and forestry residues constitute the primary feedstock for green methanol production, accounting for 47% of global capacity. This dominance reflects the established supply chains for collecting and processing these materials, particularly in regions with substantial forestry or agricultural operations. The utilization of these residues creates additional revenue streams for these sectors while avoiding sustainability concerns associated with dedicated energy crops competing with food production.

Industrial waste gases are experiencing the most rapid adoption growth at 92% annually, driven by the dual benefits of carbon circularity and economic efficiency. By capturing and converting CO2 streams from cement production, steel manufacturing, and other industrial processes, producers achieve lower input costs compared to direct air capture while helping these hard-to-abate sectors reduce their emissions profiles. Strategic co-location of methanol production with industrial facilities minimizes transportation requirements and creates operational synergies.

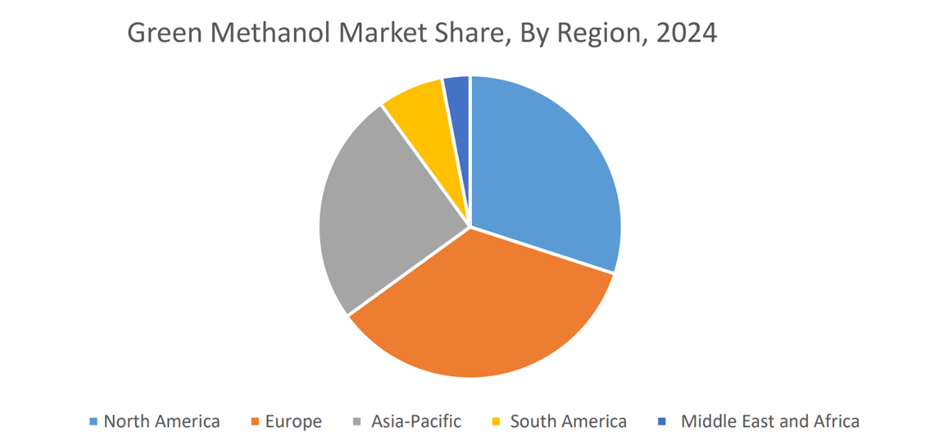

Segmentation by Regional Analysis:

• North America

• Europe

• Asia Pacific

• South America

• Middle East and Africa

The global green methanol market exhibits distinct regional characteristics, with Europe leading at 35% market share due to advanced regulatory frameworks and substantial public-private investment. North America follows at 27%, leveraging natural gas infrastructure transitioning to renewable gas and substantial biomass resources. Asia Pacific claims 23%, with remarkable growth in China and South Korea focusing on industrial applications. The Middle East (5%) and Latin America (3%) complete the market. Europe's dominance stems from ambitious climate targets, particularly in Scandinavian countries pioneering bio-methanol production. The fastest-growing region is Asia Pacific, expanding at 68% annually as maritime decarbonization initiatives accelerate in shipbuilding powerhouses like South Korea and Japan, complemented by China's push for cleaner chemical feedstocks.

COVID-19 Impact Analysis:

The pandemic initially disrupted green methanol projects through supply chain complications and financing uncertainties during 2020-2021. However, the subsequent economic recovery programs in major economies prioritized green investments, ultimately accelerating market development. Government stimulus packages frequently included specific provisions for clean fuel projects, including green methanol, while heightened awareness of supply chain vulnerabilities enhanced interest in domestically produced alternative fuels. By 2024, the market has fully recovered and expanded substantially beyond pre-pandemic projections.

Latest Trends and Developments:

Integration of green methanol production with comprehensive carbon capture utilization models is creating industrial symbiosis opportunities across sectors. Advanced catalysts that improve conversion efficiency while operating at lower temperatures have reduced energy requirements significantly. Digital twin technology implementation throughout production facilities has optimized operations and predictive maintenance. Multi-modal applications combining fuel, chemical feedstock, and energy storage functions are enhancing project economics through revenue diversification. The emergence of green methanol trading platforms is increasing market liquidity and price discovery, supporting further investment.

Key Players in the Market:

• Ørsted

• Carbon Recycling International

• OCI Global

• Proman

• Methanex Corporation

• Eni S.p.A.

• BASF SE

• Air Liquide

• Siemens Energy

• Equinor

• Mitsubishi Gas Chemical

• Shell

• A.P. Moller-Maersk

• Innogy

• Nordic Green

Segmentation by Feedstock Source:

• Dedicated biomass crops

• Agricultural/forestry residues

• Municipal solid waste

• Industrial waste gases

• Direct air capture CO2

• Point source CO2 capture

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary growth drivers for the green methanol market include increasingly stringent maritime emissions regulations, corporate decarbonization commitments across multiple industries, government support through favorable policy frameworks, declining production costs due to technological advancements, and growing consumer demand for products with reduced carbon footprints.

Key concerns surrounding the green methanol market include persistent cost premiums compared to conventional methanol, limited availability of sustainable feedstocks in certain regions, infrastructure adaptation requirements necessitating additional investment, competition from alternative low-carbon solutions, and geographic disparities in renewable electricity costs that affect production economics.

The green methanol market features a diverse mix of established energy companies, specialized producers, and technology innovators. Key players include Ørsted, Carbon Recycling International, OCI Global, Proman, Methanex Corporation, Eni S.p.A., BASF SE, Air Liquide, Siemens Energy, Equinor, Mitsubishi Gas Chemical, Shell, A.P. Moller-Maersk, Innogy, and Nordic Green.

Europe currently holds the largest market share, estimated around 35%.

Asia Pacific has shown significant room for growth in specific segments.