Global Flexible Substrates Market Research Report – Segmentation By Material Type (Plastic Substrates, Metal Substrates, Flexible Glass); By Technology (Roll-to-Roll Processing, Printed Electronics, Thin-Film Transistor Technology, Microelectromechanical Systems Integration); By End User (Consumer Goods Manufacturers, Medical Device Companies, Automotive OEMs, Electronics & Semiconductor Firms); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-5550

Format:

Region: Global

Market Size and Overview:

The Flexible Substrates Market was valued at USD 0.78 billion in 2024 and is projected to reach a market size of USD 1.6 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 15.45%.

With a prolific evolution in the Flexible Substrates Market, it becomes a strong enabler for next-generation electronic devices and consumer industries such as healthcare, automotive, consumer electronics, and energy. Flexible substrates like films made from plastic, metal foil, or flexible glass can thus deliver lightweight, strong, and space-saving designs for embedded applications, ranging from foldable displays and wearable sensors to flexible solar panels and printed circuits. With the increasing demand for compact, portable, and high-performance electronic products, manufacturers have shifted their investments toward flexible materials that support innovative form factors and enhanced functionality. Material advances, roll-to-roll manufacturing, and the proliferation of flexible and printed electronics will propel this market into one of the fundamental blocks in the future of smart technology.

Key Market Insights:

Printed electronics using flexible substrates grew by 40% in two years. Applications include smart packaging, flexible sensors, and RFID tags. This trend is supported by low-cost roll-to-roll printing techniques and increasing demand for compact electronics.

Flexible substrates reduce device weight by up to 60%. This advantage is crucial in sectors like aerospace and healthcare, where lightweight design improves performance and usability. Medical patches and diagnostic wearables benefit significantly from this feature.

Flexible Substrates Market Drivers:

One of the key drivers of the Flexible Substrates Market is the rising demand for flexible electronics in consumer devices such as smartphones, tablets, smartwatches, and foldable displays.

The rising consumer demand for the application of flexible electronics is one of the primary drivers for the Flexible Substrates Market. Such applications include consumer electronics, smartphones, tablets, smartwatches, and foldable displays. As consumers increasingly demand thinner, lighter, and more adaptable devices, manufacturers are using flexible substrates, including polyimide, PET, and flexible glass, to enable the compact, bendable, and durable components needed for such devices. The burgeoning applications of foldable and rollable OLED screens, flexible batteries, and wearable sensors have placed flexible substrates at the center of electronics innovation. Giants among electronics manufacturers, such as Samsung, Huawei, and Apple, have heavily invested in flexible display technologies, relying on these materials. In addition, flexible circuits' advantages, such as lower interconnection points, lower weight, and better heat dissipation, increase their attractiveness and desirability in product design. As expansion in the fields of 5G and IoT applications increases, so does the need for high-density, high-performance flexible components. Flexible substrates also facilitate the fabrication of next-generation printed electronics with roll-to-roll and inkjet processes to ensure affordable mass production. This scalability is important to match the ever-growing demand while controlling production costs. The flexible substrate is expected to interface with the consumer electronics market, which is in a constant evolution pattern, and thus, would become a standard application for future devices. Their flexibility, strength, and compatibility with all upcoming technology make them the vital drivers toward innovation.

Another major driver accelerating the Flexible Substrates Market is the increasing need for lightweight, compact, and flexible components in the automotive and healthcare industries.

One of the predominant factors driving the flexible substrate market is the demand for lightweight, compact, and flexible component assembly in the automotive and healthcare sectors. In the automotive segment, flexible substrates are nowadays widely employed in infotainment systems, head-up displays, flexible lighting panels, and touch-sensitive dashboards. As this sector becomes more digitally integrated and design-centric, it has created the need for flexible substrates that allow for curved, space-efficient components, enhancing aesthetics and functionality. With the trend towards electric and autonomous vehicles, space optimization and weight reduction become critical advantages that flexible substrates have to offer. These flexible substrates, meanwhile, find applications in the healthcare industry for wearable biosensors or flexible medical patches, even diagnostic devices, most likely adhering to the human body, improving patient comfort and real-time health monitoring. Flexible substrates will provide the solution to creating noninvasive skin-contact electronics that are robust, lightweight, and offer easy manufacturing in complex shapes and sizes. Excellent for smart medical textiles and drug delivery systems, as these are compatible with printed and stretchable electronics, they continue to be the most used materials. Growing demand for remote health monitoring and portable diagnostics, especially in the wake of COVID-19, further drives innovation in flexible medical electronics. As both industries move further toward miniaturization and intelligent integration, flexible substrates become essential for achieving the desired technological objectives.

Flexible Substrates Market Restraints and Challenges:

One of the primary restraints in the Flexible Substrates Market is the high cost of manufacturing and material limitations, which can hinder widespread adoption, especially among small to mid-sized companies.

The widest restraints in the flexible substrates market are the high cost of manufacture and material restrictions, which can hold back their wider dissemination, especially to small and medium companies. Flexible substrates are manufactured by special fabrication techniques such as roll-to-roll printing, vacuum deposition, and precise thermal processing, which require sophisticated equipment and a good skillset. For instance, polyimide and flexible glass are efficient materials; however, they are consistently more expensive than conventional rigid substrates. In addition, it is technically difficult to consistently maintain performance under flexible conditions such as conductivity, durability, and resistance to environmental stress. Some flexible materials are moisture, heat, and mechanical fatigue, sensitive to long-term reliability. Increased defect rate and cost-in-microbiological quality can arise from high-volume production. Furthermore, hybrid systems with integrated existing rigid components complicate design and level assembly. Flexibility has been accompanied by affordability in premium product segments or experimental uses, although, with clear advantages, flexibility in product use is mostly limited. For further commercial potential, innovations must continue in low-cost materials, scalable production methods, and durability standards. High-Cost Manufacturing, Material Limitations Are Major Obstructions to the Flexible Substrates Market. However, these features can limit their wider dissemination, especially to small- and medium-sized companies. The flexible substrates are manufactured through special fabrication techniques such as roll-to-roll printing, vacuum deposition, and precise thermal processing, demanding sophisticated equipment and a good skillset for production. For example, polyimide and flexible glass are both efficient materials, but much more expensive compared to conventional rigid substrates. Consistent performance under flexible conditions like conductivity, durability, and environmental stress resistance is technically difficult to maintain.

Flexible Substrates Market Opportunities:

The Flexible Substrates Market is teeming with potential, especially now that new technologies such as printed electronics and IoT, as well as personal communication devices, are on the rise. Flexible substrates play an enabling role in creating ultra-thin, lightweight, and bendable components for future applications. The need for cost-effective, scalable, and customizable substrates is increasing, as the adoption of printed sensors, RFID tags, flexible displays, and smart textiles continues to rise. The roll-to-roll production process makes mass production accessible and opens up opportunities for flexible electronics in healthcare, logistics, and retail applications. In the healthcare sector, flexible substrates enable skin-mounted diagnostics as well as intelligent drug delivery systems, while in automobiles, they support curved infotainment systems and lightweight control modules. The transition toward sustainable and energy-efficient materials is also opening up new avenues to use eco-friendly substrates in flexible solar panels and energy-harvesting systems. There will also be innovations such as biodegradable substrates and stretchable electronics by start-ups and research institutes, which will have high market potential. As 5G spreads its wings and smart connected devices become more ubiquitous, the demand for embedded, space-saving electronics will also go up, making flexible substrates a cornerstone material in the techno-economics of the future.

Flexible Substrates Market Segmentation:

Market Segmentation: By Material Type

• Plastic Substrates

• Metal Substrates

• Flexible Glass

The Flexible Substrates Market is mainly segmented based on the material type: it includes plastic substrates, metal substrates, and flexible glass. Plastic substrates dominate the segment and attach several types: polyimide (PI), PET, and PEN. They are cost-efficient, lightweight, and highly thermally flexible, which renders them suitable for use in displays, RFID tags, and wearables. Metal substrates such as stainless-steel foils and aluminum foils provide the best conductivity and thermal stability under extreme performance or environmentally rigorous usages such as automotive electronics and industrial sensors. Flexible glass is being extensively adopted in high-end electronics-related products such as bendable displays and OLED screens since it proves to have excellent barrier properties and transparency. Though costly, its longevity and clarity in the vision make it attractive for use in premium products. Each material type lends advantages specific to the device design and performance requirements, as well as the atmosphere in which the device will be used. Moreover, numbers will continue to grow in the field of hybrid material design where electrical performance, flexibility, and strength coalesce.

Market Segmentation: By Technology

• Roll-to-Roll Processing

• Printed Electronics

• Thin-Film Transistor Technology

• Microelectromechanical Systems Integration

Roll-to-Roll, Printed Electronics, Thin-Film Transistor (TFT) Technology, and MEMS Integration are categorized under flexible substrates technology segmentation in the Flexible Substrates Market. Among these technologies, Roll-to-Roll processing enables high-volume, low-cost production in a continuous processing line of flexible films. Thus, it is very useful for printed sensors and modules of solar cells. Printed electronics employ conductive inks, which are the main design drivers for smart labels, wearables, and disposable sensors, and allow greater design flexibility and savings on material. TFT technology powers flexible OLED displays and e-paper, allowing devices to continue functioning even if bent or folded. MEMS integration supports very tiny, flexibly combined mechanical-electronic systems, such as those utilized in diagnostics for medical purposes or sensing in automotive applications. Collectively, these technologies are all about performance and miniaturization in flexible electronics. There are endless innovative developments in precision of processing as well as in compatibility with materials to enhance reliability and minimize the cost of production.

Market Segmentation: By End User

• Consumer Goods Manufacturers

• Medical Device Companies

• Automotive OEMs

• Electronics & Semiconductor Firms

The market operates based on end-user classifications, which serve the following industries: consumer goods manufacturers, medical devices, automotive OEMs, and electronics and semiconductor users. Other than that, consumer electronics applications, such as foldable phones, smartwatches, and new wearables sensors for applications that require design versatility and portability, create a very high consumption for flexible substrates. These flexible substrates that are biocompatible are used by companies that operate in the field of medical devices in remote monitoring diagnostics, smart patches, and wearable monitors for real-time patient tracking. OEMs from the automotive sector are apt among others to adopt these for their application in curved entertainment systems, touch-sensitive dashboards, and flexible lighting sources in electric and autonomous vehicles. In the electronics and semiconductor industries, it is used for the next generation of printed circuit testing and energy devices with microchips in ultra-compact form factors. The high demand for durability, performance, and versatility from each segment will drive customization in the market even further. Diversification for end-users will continue to grow through other industries pursuing smart, lightweight, and connected devices.

Market Segmentation: Regional Analysis:

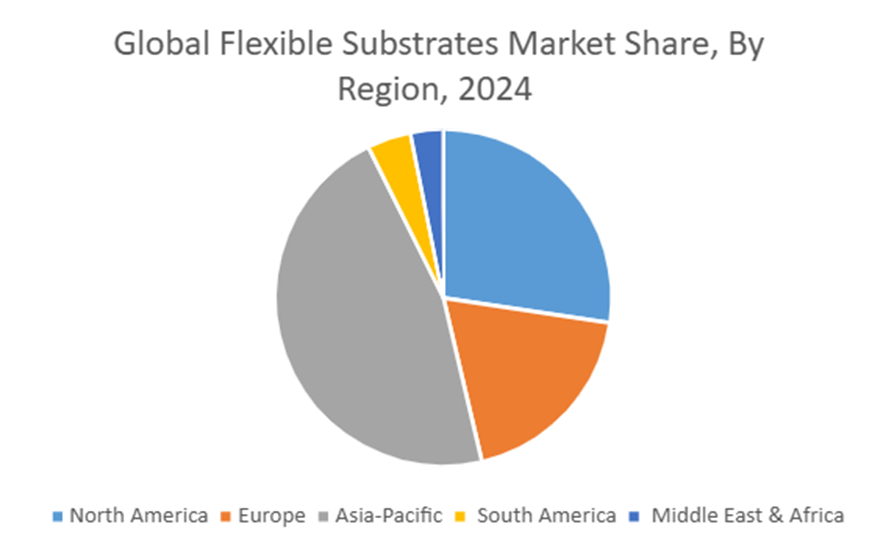

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

The Asian region has acquired strong dominance in the Flexible Substrates Market, led by the manufacturing giants of China, Japan, and South Korea. The electronics supply chain is well established in this region, along with R&D resources and high-volume production of flexible displays, sensors, and semiconductors. Following closely is the North American region, where demand is driven by innovative products in OLED screens, solar energy applications, and wearable technology in the USA. In Europe, the market steadily expands, supported by escalated integration of flexible substrates in medical devices and automotive electronics, along with the increasing focus on sustainable and lightweight materials. An emerging player is South America, where increased flexible technology adoption in solar and consumer electronics can be seen in Brazil and Argentina. Gradual uptake is being witnessed in the Middle East and Africa, primarily in healthcare wearables and defense electronics, with the digitization and smart technology initiatives being led by the GCC countries. Each region is uniquely contributing to the development of global demand for flexible substrates based on its strengths in respective industries and innovation priorities.

COVID-19 Impact Analysis on the Flexible Substrates Market:

While providing demand mitigation through increasing demand for flexible substrates from application segments such as healthcare devices, biosensors, and remote monitoring tools, the COVID-19 pandemic had mixed effects on the flexible substrates market. The pandemic caused a decline in demand for flexible components due to unexpected temporary shutdowns in key sectors such as consumer electronics and automotive manufacturing, delayed product launches, and, in general, disrupted global supply chains by halting production due to statewide lockdowns and workforce shortages. The healthcare sector saw increasing demand for wearable medical devices, biosensors, and remote monitoring tools, the designs for most of which are very much dependent on lightweight and skin-conforming flexible substrates. Therefore, some of the downturn in demand from the segments mentioned was blamed on the rise in demand for flexible substrates for the healthcare sector. Digitization, telemedicine, and smart healthcare on a global scale opened up new horizons for flexible electronics during the pandemic. From a manufacturing perspective, a more localized and automated production method(concentrating on roll-to-roll fabrication) is picking up for the industry to minimize dependency areas in global supply chains. The short-term problems posed by the initial shock nurtured an accelerated innovative process in the industry and showcased the strategic importance of flexible, mobile, and connected devices, resulting in renewed investments and long-term growth potential in the flexible substrates market.

Latest Trends/ Developments:

The Flexible Substrates Market is rapidly transforming due to advanced manufacturing processes, sustainable material development, and diverse applications. One of the most noteworthy innovations has been in roll-to-roll (R2R) printing means of manufacturing flexible electronics with continuous, high accuracy, and low cost. The field of printed electronics is gaining acceptance as techniques like inkjet and screen printing provide a scalable means for manufacturing RFID tags, biosensors, and wearable patches.

Manufacturers are incorporating biodegradable polymers and the use of solvent-free inks in substrate manufacturing towards environmental sustainability and reduction of carbon footprint. Their current trends show that manufacturers want ultrathin stretchable flexible glass that has gained attention for foldable smartphone displays, AR/VR devices, and medical electronics due to its durability and transparency. Meanwhile, these hybrid techniques are able to manufacture high-density, multifunctional circuits by layering ink and embedding electronics. Smart textiles and biocompatible substrates are under development for healthcare and wearables that will be able to physically monitor conditions utilizing sensors embedded in their fabrics. Such innovations contribute to the industry-wide shift toward lighter, more adaptable, and environmentally friendly electronics.

Key Players:

• DuPont (US)

• LG Chem (South Korea)

• 3M Company (US)

• Sumitomo Electric Industries, Ltd. (Japan)

• Kolon Industries, Inc. (South Korea)

• Schott AG (Germany)

• Arkema Group (France)

• Fujikura Ltd. (Japan)

• BenQ Materials Corporation (Taiwan)

• Teijin Limited (Japan)

Chapter 1. Global Flexible Substrates Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Flexible Substrates Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Flexible Substrates Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Flexible Substrates Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Flexible Substrates Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Flexible Substrates Market – By Material Type

6.1. Introduction/Key Findings

6.2. Plastic Substrates

6.3. Metal Substrates

6.4. Flexible Glass

6.5. Y-O-Y Growth trend Analysis By Material Type

6.6. Absolute $ Opportunity Analysis By Material Type, 2025-2030

Chapter 7. Global Flexible Substrates Market – By Technology

7.1. Introduction/Key Findings

7.2. Roll-to-Roll Processing

7.3. Printed Electronics

7.4. Thin-Film Transistor Technology

7.5. Microelectromechanical Systems Integration

7.6. Y-O-Y Growth trend Analysis By Technology

7.7. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 8. Global Flexible Substrates Market – By End User

8.1. Introduction/Key Findings

8.2. Consumer Goods Manufacturers

8.3. Medical Device Companies

8.4. Automotive OEMs

8.5. Electronics & Semiconductor Firms

8.6. Y-O-Y Growth trend Analysis By End User

8.7. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 9. Global Flexible Substrates Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Material Type

9.1.3. By Technology

9.1.4. By End User

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Material Type

9.2.3. By Technology

9.2.4. By End User

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Material Type

9.3.3. By Technology

9.3.4. By End User

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Material Type

9.4.3. By Technology

9.4.4. By End User

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Material Type

9.5.3. By Technology

9.5.4. By End User

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Flexible Substrates Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. DuPont

10.2. LG Chem

10.3. 3M Company

10.4. Sumitomo Electric Industries, Ltd.

10.5. Kolon Industries, Inc.

10.6. Schott AG

10.7. Arkema Group

10.8. Fujikura Ltd.

10.9. BenQ Materials Corporation

10.10. Teijin Limited

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Flexible Substrates Market was valued at USD 0.78 billion in 2024 and is projected to reach a market size of USD 1.6 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 15.45%.

The Flexible Substrates Market is driven by the growing demand for lightweight, bendable electronics and the expansion of wearable devices, foldable displays, and printed sensors. Advancements in materials and roll-to-roll manufacturing further fuel scalability and cost-efficiency.

The Flexible Substrates Market segments by technology include Roll-to-Roll Processing, Printed Electronics, Thin-Film Transistor (TFT) Technology, and Microelectromechanical Systems (MEMS) Integration.

Asia-Pacific is the most dominant region for the Flexible Substrates Market.

DuPont, LG Chem, 3M Company, Sumitomo Electric Industries, Kolon Industries, Schott AG, Arkema Group, Fujikura, BenQ Materials, Teijin, FlexEnable, Taimide Tech, Polyonics, and Cymbet Corporation are the key players in the Flexible Substrates Market.