Global Fleet Management Market Research Report – Segmentation by Solution Type (Vehicle Tracking and Monitoring, Fleet Maintenance and Diagnostics, Driver Behaviour and Performance Management, Fuel management, Route Optimization and navigation, Safety and Compliance management, Accident management, Leasing, Financing, and Insurance management, Others (Tire management, Toll management)); By Deployment Mode (On-Premises and Cloud-Based); By Fleet Type (Light Commercial Vehicles (LCVs), Medium and Heavy Commercial Vehicles (MHCVs), Construction and Mining Vehicles, Public Transport Vehicles, Others (Rental Fleets, Specialized Utility Vehicles)); By Component (Hardware- (GPS Tracking Devices, Dash cameras, Sensors (Fuel, Tire Pressure, etc.), Electronics Logging Devices (ELDs), Others (OBD Devices, RFID)), Software- (Fleet Management Platforms, Analytics and Reporting Software), Services- (Consulting and Deployment Services, Managed Services, Support and Maintenance)); By Communication Technology (Cellular- (2G, 3G, 4G/LTE, 5G), Satellite); By End-Use Industry (Transportation & Logistics, Retail & E-commerce, Oil & Gas, Construction, Mining, Utilities, Waste management, Healthcare & Pharmaceuticals, Others (Education, hospitality, Municipal Services)); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-2209

Format:

Region: Global

Market Size and Overview:

The Global Fleet Management Market was valued at USD 23.4 billion in 2024 and is projected to reach a market size of USD 52.50 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 17.54%.

The Fleet Management Market is rapidly gaining prominence as businesses across industries seek smarter, more efficient ways to manage their vehicle operations. This market revolves around solutions and services that enable organizations to track, monitor, and optimize their fleets in real time. With growing pressure to reduce operational costs, improve driver safety, enhance fuel efficiency, and comply with strict regulatory standards, companies are increasingly investing in advanced telematics, GPS tracking, and predictive maintenance systems. Additionally, the integration of technologies like AI, IoT, and cloud computing is transforming fleet operations from reactive to proactive, allowing for better route planning, vehicle utilization, and overall performance. As demand for connected vehicles and automated fleet processes grows, the fleet management market continues to expand across commercial logistics, public transport, delivery services, and more.

Key Market Insights:

The fleet management market is witnessing substantial growth driven by the increasing adoption of IoT and AI technologies, which enable better fleet monitoring and data-driven decision-making. The demand for telematics solutions has surged, as these systems provide real-time tracking, improved route optimization, and predictive maintenance, leading to a reduction in operational costs. In fact, the integration of telematics has been shown to reduce fuel consumption by up to 10%, significantly enhancing operational efficiency for fleet operators.

The growth in e-commerce and logistics sectors is further fueling the fleet management market. With the rise of on-demand deliveries, companies are focusing on fleet optimization to handle increased transportation needs. A recent study found that logistics companies utilizing fleet management systems experienced a 15% reduction in delivery times and a 20% improvement in customer satisfaction.

In addition, the need for regulatory compliance and enhanced vehicle safety is pushing the adoption of fleet management systems across various industries. Fleet operators are turning to these solutions to ensure compliance with environmental regulations, such as emissions standards, and improve driver safety by monitoring behavior. The global focus on reducing carbon footprints and increasing sustainability is anticipated to continue driving growth in the fleet management market as companies seek eco-friendly solutions while optimizing their vehicle fleets.

Fleet Management Market Drivers:

Growing Demand for Fleet Efficiency and Cost Optimization

The rising demand for businesses to streamline their operations and reduce operational costs is driving the adoption of fleet management solutions. Companies are focusing on improving the efficiency of their fleet operations, reducing fuel consumption, minimizing maintenance costs, and enhancing productivity. With the help of advanced fleet management tools, organizations can gain real-time insights into fleet performance, identify inefficiencies, and optimize routes and schedules, all of which contribute to significant cost savings and operational improvements.

Technological Advancements Driving Fleet Management Solutions

Technological advancements in areas such as Internet of Things (IoT), artificial intelligence (AI), and telematics are fueling the growth of the fleet management market. The integration of IoT-enabled devices in vehicles helps fleet operators monitor vehicle health, track real-time locations, and capture critical performance data. AI-driven algorithms further enhance route optimization, predictive maintenance, and driver safety. As these technologies continue to evolve, fleet management solutions are becoming more efficient and reliable, providing companies with powerful tools to optimize their operations.

Rising Focus on Driver Safety and Compliance Regulations

With an growing emphasis on ensuring the safety of drivers and meeting regulatory requirements, fleet management systems are becoming essential for businesses in various industries. Fleet operators are using advanced solutions to monitor driver behavior, ensure compliance with safety regulations, and reduce accidents. Features like real-time alerts, driver scorecards, and automated reporting help ensure that fleet drivers adhere to best safety practices while complying with governmental regulations, reducing the risk of accidents and legal liabilities.

Demand for Sustainable and Environmentally-Friendly Fleet Operations

The growing global concern about environmental sustainability and the push for greener initiatives are encouraging fleet operators to adopt eco-friendly solutions. Fleet management systems help businesses reduce their carbon footprint by optimizing routes, improving fuel efficiency, and managing electric vehicle fleets. The shift towards electric vehicles (EVs) and hybrid models is also driving the market as organizations strive to meet environmental standards and reduce emissions. This growing focus on sustainability is propelling the demand for fleet management solutions that support eco-friendly practices.

Fleet Management Market Restraints and Challenges:

High Initial Investment and Integration Complexities

One of the primary challenges hindering the growth of the fleet management market is the high initial investment required for implementing advanced fleet management solutions. Small and medium-sized businesses may find it difficult to afford the upfront costs of purchasing and integrating technology such as telematics, sensors, and software systems into their fleets. Additionally, integrating new fleet management systems with existing infrastructure can be complex and time-consuming, requiring significant effort in terms of training and system customization. These factors may deter some businesses from adopting fleet management solutions, especially in regions with budget constraints.

Fleet Management Market Opportunities:

The fleet management market presents significant opportunities driven by the rising demand for automation and real-time data analytics. As industries focus on improving operational efficiency, there is a growing need for intelligent fleet management solutions that can optimize route planning, reduce fuel consumption, and enhance vehicle maintenance scheduling. Additionally, the rise of electric vehicles (EVs) and the need for sustainable fleet operations create opportunities for advanced fleet management systems that incorporate EV charging stations, energy consumption tracking, and carbon footprint management. With technological advancements such as AI, machine learning, and IoT, businesses can leverage these innovations to enhance safety, reduce costs, and ensure regulatory compliance, opening new avenues for market growth.

Fleet Management Market Segmentation:

Market Segmentation: By Solution Type:

o Vehicle Tracking and Monitoring

o Fleet Maintenance and Diagnostics

o Driver Behavior and Performance Management

o Fuel Management

o Route Optimization and Navigation

o Safety and Compliance Management

o Accident Management

o Leasing, Financing, and Insurance Management

o Others (Tire Management, Toll Management)

The dominant solution type in the fleet management market is vehicle tracking and monitoring, which has established itself as the primary focus for businesses aiming to optimize fleet operations. This solution provides real-time visibility into vehicle location, performance, and maintenance needs, leading to improved efficiency, reduced operational costs, and enhanced safety. The widespread adoption of GPS tracking systems, coupled with the growing emphasis on fleet optimization, drives the popularity of this solution type across various industries, making it a dominant player in the market.

The fastest-growing solution type is route optimization and navigation, driven by advancements in AI and machine learning technologies. As businesses seek to minimize fuel consumption and travel time while enhancing overall fleet productivity, route optimization tools have become essential. These solutions leverage real-time traffic data, predictive analytics, and smart algorithms to determine the most efficient routes, leading to cost savings, improved service levels, and greater operational efficiency. As a result, the demand for route optimization and navigation is expected to grow rapidly in the coming years.

Market Segmentation: By Deployment Mode:

o On-Premise

o Cloud-Based

The dominant deployment mode in the fleet management market is cloud-based solutions. As businesses increasingly move towards digital transformation, cloud-based solutions have gained traction due to their scalability, flexibility, and cost-effectiveness. These solutions allow for centralized data storage, remote accessibility, and real-time updates, making them highly attractive to fleet operators. The cloud-based deployment also facilitates easy integration with other technologies such as IoT, AI, and big data analytics, further enhancing fleet management capabilities.

The fastest-growing deployment mode is on-premise solutions, which cater to organizations with stringent data security and privacy requirements. While cloud-based solutions are more commonly adopted, some businesses in highly regulated industries prefer on-premise deployment to retain full control over their data and infrastructure. With the increasing focus on data security and compliance, the demand for on-premise solutions is expected to increase in specific sectors, such as government and defense, where strict security protocols are essential.

Market Segmentation: By Fleet Type:

o Light Commercial Vehicles (LCVs)

o Medium and Heavy Commercial Vehicles (MHCVs)

o Construction and Mining Vehicles

o Public Transport Vehicles

o Others (Rental Fleets, Specialized Utility Vehicles)

The dominant fleet type in the market is Light Commercial Vehicles (LCVs). These vehicles are highly favored due to their affordability and versatility in a wide range of industries. LCVs play a significant role in last-mile delivery, especially as e-commerce and logistics services grow rapidly worldwide. They are also extensively used by small businesses for various transportation needs, making them essential for cost-effective operations. Their ability to balance operational costs with high utility has made them a primary choice for many businesses, particularly in urban environments where smaller vehicles are preferred for maneuvering through congested streets.

The fastest-growing fleet type is Medium and Heavy Commercial Vehicles (MHCVs), driven by the booming need for large-scale logistics and freight transportation. These vehicles are crucial for industries that require the movement of bulk goods, such as construction, manufacturing, and wholesale distribution. The ongoing expansion of supply chains, especially with international trade increasing, has led to the growth of MHCV fleets. Additionally, advancements in fuel management, telematics, and route optimization technologies are improving the operational efficiency of MHCVs, making them an increasingly attractive option for businesses looking to enhance their logistics capabilities.

Market Segmentation: By Component:

o Hardware

GPS Tracking Devices

Dash Cameras

Sensors (Fuel, Tire Pressure, etc.)

Electronic Logging Devices (ELDs)

Others (OBD Devices, RFID)

o Software

Fleet Management Platforms

Analytics and Reporting Software

o Services

Consulting and Deployment Services

Managed Services

Support and Maintenance

The dominant component in the fleet management market is Hardware, particularly GPS tracking devices and dash cameras. These devices have become indispensable in fleet operations as they ensure real-time location tracking, provide enhanced security, and support efficient route planning. GPS tracking devices are crucial for fleet operators, offering features like geofencing and route optimization, which enhance operational efficiency and reduce fuel consumption. Meanwhile, dash cameras are valuable for monitoring driver behavior and ensuring safety standards, becoming a necessity for fleet management, particularly in industries focused on safety and risk management.

The fastest-growing component is Software, especially Fleet Management Platforms and Analytics and Reporting Software. The rising demand for data-driven decision-making and optimized fleet operations has spurred the growth of software solutions. Fleet management platforms are essential for managing complex fleet operations, offering integrated solutions that combine route optimization, maintenance scheduling, and real-time data analytics. Additionally, analytics and reporting software is gaining traction as businesses seek more insights into fuel consumption, driver behavior, and vehicle performance to improve efficiency and reduce costs. These software solutions are increasingly critical for companies looking to streamline operations and leverage big data to drive smarter business decisions.

Market Segmentation: By Communication Technology:

o Cellular (2G, 3G, 4G/LTE, 5G)

o Satellite

The dominant communication technology in the fleet management market is Cellular, particularly 4G/LTE and 5G networks. These technologies are widely adopted due to their high-speed, low-latency, and reliable communication, which are crucial for real-time tracking and monitoring of fleet vehicles. 4G/LTE provides seamless connectivity across large areas, while 5G is emerging as a game-changer because of its ultra-fast speeds and its ability to handle a massive volume of connected devices simultaneously. This makes cellular technology the backbone of modern fleet management solutions, enabling efficient route optimization, real-time vehicle diagnostics, and instant communication.

The fastest-growing communication technology is Satellite, driven by the demand for global coverage in remote areas where cellular networks are not available. Satellite communication offers fleet operators the ability to track vehicles in isolated or hard-to-reach regions, ensuring that no vehicle is left unmonitored. As companies expand their operations into more remote or rural regions, satellite communication plays a crucial role in enhancing the reach and reliability of fleet management solutions. This growth is particularly evident in industries like logistics, mining, and construction, where vehicles often operate in off-the-grid locations.

Market Segmentation: By End-User Industry:

o Transportation and Logistics

o Retail and E-commerce

o Oil and Gas

o Construction

o Mining

o Utilities

o Waste Management

o Healthcare and Pharmaceuticals

o Others (Education, Hospitality, Municipal Services)

The dominant end-user industry in the fleet management market is Transportation and Logistics, which accounts for the largest share of fleet management technology adoption. This sector relies heavily on fleet management solutions to optimize delivery routes, monitor fuel consumption, track vehicle performance, and ensure regulatory compliance. The growing demand for quick and efficient deliveries, especially with the surge in e-commerce and on-demand services, has led to a significant increase in fleet management technology investments. These solutions enhance operational efficiency, reduce costs, improve driver safety, and provide real-time tracking capabilities, making them vital for transportation and logistics companies to maintain a competitive edge in the market.

On the other hand, the fastest-growing end-user industry in the fleet management market is Healthcare and Pharmaceuticals, driven by the growing demand for safe, timely, and temperature-sensitive deliveries of medical supplies and pharmaceuticals. Fleet management solutions in this sector are used to ensure the efficient transportation of goods such as vaccines, medicines, and medical equipment, which require strict temperature control and timely delivery. The rapid expansion of home healthcare services, coupled with the rise in e-commerce pharmaceutical sales and stricter regulatory requirements, has led to a significant adoption of fleet management technologies. Companies in the healthcare sector are focusing on increasing fleet efficiency, ensuring real-time monitoring of deliveries, and improving compliance with regulatory standards, making this a fast-growing segment in the fleet management market.

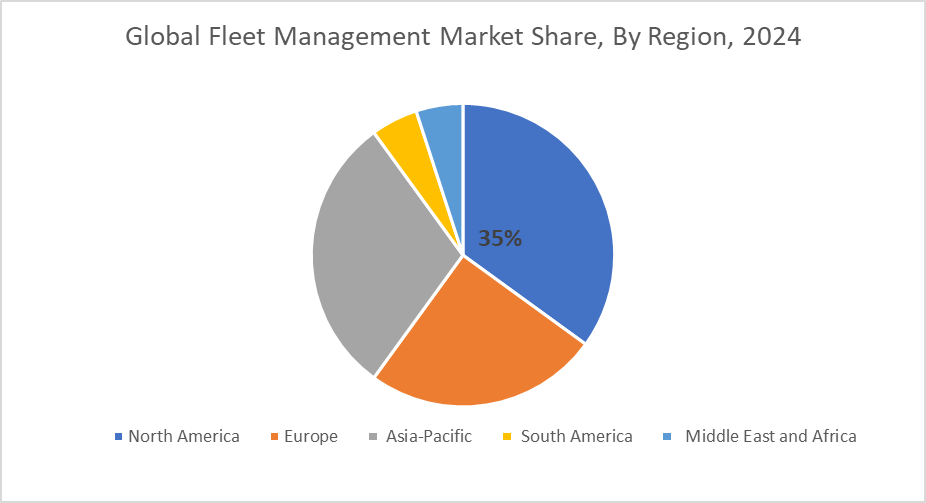

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

The dominant region in the fleet management market is North America, which holds the largest share. This dominance is largely because of the region's advanced technological infrastructure, high adoption rates of fleet management solutions, and a substantial number of commercial fleets operating across various industries. The presence of key market players, strong government regulations on fleet safety and compliance, and the growing trend of integrating IoT, GPS tracking, and telematics technologies further solidify North America’s leadership in the fleet management space. Additionally, industries such as transportation, logistics, and retail heavily rely on fleet management systems, contributing to the region’s high market share.

On the other hand, the fastest-growing region is Asia-Pacific, which is experiencing rapid growth in the fleet management market. This growth can be attributed to the region's increasing industrialization, expanding transportation and logistics sectors, and a significant rise in e-commerce activities, particularly in countries like China and India. With the growing need for efficient fleet operations and cost management in emerging economies, the adoption of fleet management systems is accelerating. The rapid development of infrastructure, government initiatives promoting smart cities, and a rising focus on sustainability also drive the market's growth in this region. The demand for advanced technologies such as AI, IoT, and data analytics in fleet management solutions is expected to continue propelling this growth.

COVID-19 Impact Analysis on the Global Fleet Management Market:

The COVID-19 pandemic significantly impacted the global fleet management market, initially leading to a slowdown in demand as industries faced disruptions in supply chains and transportation. Lockdowns, reduced economic activities, and restrictions on movement caused a temporary decline in fleet utilization. However, the market quickly rebounded as companies adapted to new challenges by leveraging digital fleet management solutions to ensure safety, optimize operations, and reduce costs. The pandemic also accelerated the adoption of contactless and remote monitoring technologies, such as GPS tracking and telematics, to enhance fleet efficiency and comply with health protocols.

Latest Trends/ Developments:

Fleet management is undergoing a transformative shift with the increasing adoption of cutting-edge technologies that drive efficiency and sustainability. The integration of AI and machine learning is enhancing predictive maintenance, helping fleet operators identify potential issues before they lead to breakdowns, which ultimately reduces costs and extends the life of vehicles. Additionally, the Internet of Things (IoT) is playing a crucial role in real-time vehicle tracking, offering valuable data insights that improve decision-making and optimize operations.

Moreover, the rise of Mobility-as-a-Service (MaaS) is reshaping the fleet management landscape by offering on-demand, flexible transportation solutions that cater to both consumer and business needs. The emergence of 5G connectivity and cloud computing is also revolutionizing fleet operations by enabling seamless data exchange and communication between vehicles, making real-time monitoring and coordination more efficient than ever. These advancements are laying the foundation for a future where fleet management is not only smarter and more efficient but also more adaptable to the growing need for sustainable practices and consumer-centric solutions. As the industry continues to evolve, these technological innovations promise to shape the future of mobility in unprecedented ways.

Key Players:

• Geotab

• Samsara

• Fleet Complete

• Trimble Inc.

• Daimler AG

• Verizon Connect

• Zonar Systems

• Wheels, Inc.

• MiX Telematics

• Teletrac Navman

Chapter 1. Global Fleet Management Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Fleet Management Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Fleet Management Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Fleet Management Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Fleet Management Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Fleet Management Market – By Solution Type

6.1 Vehicle Tracking and Monitoring

6.2 Fleet Maintenance and Diagnostics

6.3 Driver Behavior and Performance Management

6.4 Fuel Management

6.5 Route Optimization and Navigation

6.6 Safety and Compliance Management

6.7 Accident Management

6.8 Leasing, Financing, and Insurance Management

6.9 Others (Tire Management, Toll Management)

6.10. Y-O-Y Growth trend Analysis By Solution Type

6.11. Absolute $ Opportunity Analysis By Solution Type, 2025-2030

Chapter 7. Global Fleet Management Market – By Deployment Mode

7.1 On-Premise

7.2 Cloud-Based

7.3. Y-O-Y Growth trend Analysis By Deployment Mode

7.4. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global Fleet Management Market – By Fleet Type

8.1 Light Commercial Vehicles (LCVs)

8.2 Medium and Heavy Commercial Vehicles (MHCVs)

8.3 Construction and Mining Vehicles

8.4 Public Transport Vehicles

8.5 Others (Rental Fleets, Specialized Utility Vehicles)

8.6. Y-O-Y Growth trend Analysis By Fleet Type

8.7. Absolute $ Opportunity Analysis By Fleet Type, 2025-2030

Chapter 9. Global Fleet Management Market – By Component

9.1 Hardware

9.1.1 GPS Tracking Devices

9.1.2 Dash Cameras

9.1.3 Sensors (Fuel, Tire Pressure, etc.)

9.1.4 Electronic Logging Devices (ELDs)

9.1.5 Others (OBD Devices, RFID)

9.2 Software

9.2.1 Fleet Management Platforms

9.2.2 Analytics and Reporting Software

9.3 Services

9.3.1 Consulting and Deployment Services

9.3.2 Managed Services

9.3.3 Support and Maintenance

9.4. Y-O-Y Growth trend Analysis By Component

9.5. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 10. Global Fleet Management Market – By Communication Technology

10.1 Cellular (2G, 3G, 4G/LTE, 5G)

10.2 Satellite

10.3. Y-O-Y Growth trend Analysis By Communication Technology

10.4. Absolute $ Opportunity Analysis By Communication Technology, 2025-2030

Chapter 11. Global Fleet Management Market – By End-Use Industry

11.1 Transportation and Logistics

11.2 Retail and E-commerce

11.3 Oil and Gas

11.4 Construction

11.5 Mining

11.6 Utilities

11.7 Waste Management

11.8 Healthcare and Pharmaceuticals

11.9 Others (Education, Hospitality, Municipal Services)

11.10. Y-O-Y Growth trend Analysis By End-Use Industry

11.11. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 12. Global Fleet Management Market, By Geography – Market Size, Forecast, Trends & Insights

12.1. North America

12.1.1. By Country

12.1.1.1. U.S.A.

12.1.1.2. Canada

12.1.3. Mexico

12.1.2. By Solution Type

12.1.3. By Deployment Mode

12.1.4. By Fleet Type

12.1.5. By Component

12.1.6. By Communication Technology

12.1.7. By End-Use Industry

12.1.8. Countries & Segments – Market Attractiveness Analysis

12.2. Europe

12.2.1. By Country

12.2.1.1. U.K.

12.2.1.2. Germany

12.2.1.3. France

12.2.1.4. Italy

12.2.1.5. Spain

12.2.1.6. Rest of Europe

12.2.2. By Solution Type

12.2.3. By Deployment Mode

12.2.4. By Fleet Type

12.2.5. By Component

12.2.6. By Communication Technology

12.2.7. By End-Use Industry

12.2.8. Countries & Segments – Market Attractiveness Analysis

12.3. Asia Pacific

12.3.1. By Country

12.3.1.1. China

12.3.1.2. Japan

12.3.1.3. South Korea

12.3.1.4. India

12.3.1.5. Australia & New Zealand

12.3.1.6. Rest of Asia-Pacific

12.3.2. By Solution Type

12.3.3. By Deployment Mode

12.3.4. By Fleet Type

12.3.5. By Component

12.3.6. By Communication Technology

12.3.7. By End-Use Industry

12.3.8. Countries & Segments – Market Attractiveness Analysis

12.4. South America

12.4.1. By Country

12.4.1.1. Brazil

12.4.1.2. Argentina

12.4.1.3. Colombia

12.4.1.4. Chile

12.4.1.5. Rest of South America

12.4.2. By Solution Type

12.4.3. By Deployment Mode

12.4.4. By Fleet Type

12.4.5. By Component

12.4.6. By Communication Technology

12.4.7. By End-Use Industry

12.4.8. Countries & Segments – Market Attractiveness Analysis

12.5. Middle East & Africa

12.5.1. By Country

12.5.1.1. United Arab Emirates (UAE)

12.5.1.2. Saudi Arabia

12.5.1.3. Qatar

12.5.1.4. Israel

12.5.1.5. South Africa

12.5.1.6. Nigeria

12.5.1.7. Kenya

12.5.1.8. Egypt

12.5.1.9. Rest of MEA

12.5.2. By Solution Type

12.5.3. By Deployment Mode

12.5.4. By Fleet Type

12.5.5. By Component

12.5.6. By Communication Technology

12.5.7. By End-Use Industry

12.5.8. Countries & Segments – Market Attractiveness Analysis

Chapter 13. Global Fleet Management Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

13.1 Geotab

13.2 Samsara

13.3 Fleet Complete

13.4 Trimble Inc.

13.5 Daimler AG

13.6 Verizon Connect

13.7 Zonar Systems

13.8 Wheels, Inc.

13.9 MiX Telematics

13.10 Teletrac Navman

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Fleet Management Market was valued at USD 23.4 billion in 2024 and is projected to reach a market size of USD 52.50 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 17.54%.

The global fleet management market is driven by the increasing demand for operational efficiency, cost reduction, and real-time vehicle tracking.

Based on deployment Mode, the Global Fleet Management Market is segmented into On-premise and Cloud-based.

North America is the most dominant region for the Global Fleet Management Market.

Geotab, Samsara, Fleet Complete, Trimble Inc. are the leading players in the Global Fleet Management Market.