Global Fintech Technologies Market Research Report – Segmentation By Technology (Blockchain, Artificial Intelligence & Machine Learning, Big Data Analytics, Mobile Payments, Digital Banking), By Application (Lending & Credit, Payments, Wealth Tech, Insurtech, Regtech, Others), By Deployment Mode (Cloud, On-premises, Hybrid), By Enterprise Size (SMEs, Large Enterprises), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16582

Format:

Region: Global

Market Size and Overview:

The Global Fintech Technologies Market was valued at USD 356.73 billion and is projected to reach a market size of USD 686.85 billion by the end of 2030. Over the forecast period of 2023-2030, the market is projected to grow at a CAGR of 14%.

Digital banking platforms, mobile wallets, blockchain networks, artificial intelligence-powered risk engines, and big-data analytics automating and improving financial services across banking, insurance, wealth management, and payments define fintech. Spurred by digital transformation projects, open-banking rules, and changing consumer preferences toward mobile and contactless transactions, fintech is revolutionizing the world financial services scene. Established incumbents and startups are pouring significant money into grabbing markets, including Buy Now, Pay Later (BNPL), predicted to reach USD 3.7 trillion by 2030, and embedded finance (projected to hit USD 7.2 trillion by 2030).

Key Market Insights:

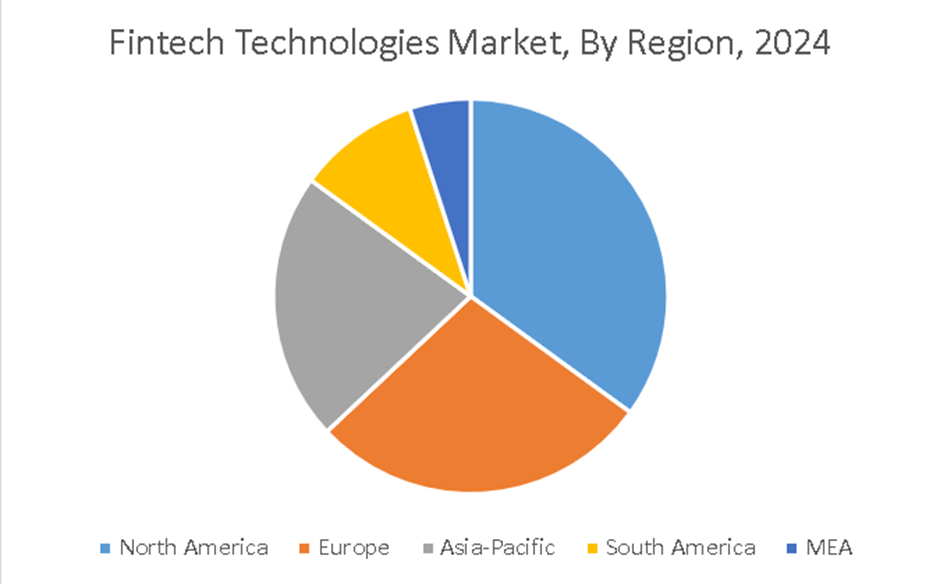

At about 35% in 2024, driven by Silicon Valley innovation and regulatory sandboxes, North America controls the market; Asia Pacific is the fastest-growing at approximately 22% CAGR, powered by digital-banking adoption in China and India.

Payments (including mobile and cross-border remittances) comprise around 30% of revenues, while Lending and Credit (digital personal and SME loans) are growing at around 20% CAGR, fueled by alternative data scoring algorithms.

Driving technological spending with nearly 25% share, artificial intelligence and machine learning systems underpin personalized advice and fraud detection; blockchain is the fastest-growing technology category at about 28% CAGR, aiding DeFi and smart-contract solutions.

Using cloud-based SaaS billing, accounting, and lending tools that cut operational complexity and hasten time-to-market for digital financial services, SMEs make up around 40% of fintech adoption.

Fintech Technologies Market Drivers:

The recent digital transformation and modernization of banking are driving the growth of this market.

The primary driver for fintech technology acceptance is the need to modernize aging core-banking and insurance systems. 65% of financial-services CIOs have larger budgets for fintech-XaaS solutions to support omnichannel banking, real-time payments, and embedded-finance partnerships. Leading institutions are phasing out old mainframes for cloud-native microservices architectures, therefore speeding feature deployment cycles from months to weeks. This change supports cutting-edge applications including real-time fraud detection, AI-driven credit scoring, and customized wealth-management dashboards. Over 70% of world banks will operate key workloads on XaaS platforms by 2025 to satisfy 99.99% uptime SLAs and enable 24/7 digital channels. Moreover, alliances between incumbents and fintech companies, arranged via API marketplaces, are multiplying, which enables banks to swiftly incorporate best-of-breed services without significant in-house development. The outcome is a more resilient, flexible financial services ecosystem able to react fast to legislative changes and changing customer demands.

The surge in mobile and contactless payment methods is helping the market to grow rapidly.

Driven by QR-code systems in China, UPI in India, and tap-to-pay NFC solutions in the West, global mobile-payment values are expected to reach USD 13 trillion by 2025. COVID-19 sped contactless adoption, with 89% of consumers now preferring touch-free in-store payments and P2P transactions via mobile apps. Both fintechs and banks are putting resources into cloud-hosted wallet systems and real-time transaction-monitoring engines so that millions of daily payments may be handled safely and at scale. While guaranteeing PCI-DSS compliance, innovations like tokenization and biometric authentication further lower fraud rates, now under 0.01% for big wallets. As underbanked people leapfrog conventional POS infrastructure, digital wallet adoption in Latin America increased 45% alone in 2024. Cloud-native payment gateways also allow easy cross-border remittances with fees as little as 1%, hence establishing mobile payments as a foundation of worldwide financial inclusion.

The use of open banking is also considered a major market growth driver.

Open-banking requirements, including the U.K.'s Open Banking system, Australia's Consumer Data Right, and PSD2 in the EU, compel banks to expose customer data through standardized APIs, therefore promoting a lively fintech environment of data aggregators and personal-finance applications. EU fintechs have produced over €50 billion more in revenue by providing account-aggregation solutions, payment initiation, and smart-saving tools since PSD2's release in 2018. 75% of current-account holders in the U.K. have approved at least one third-party provider, demonstrating strong consumer trust in secure API-based data exchange. Open-banking also underpins embedded-finance models, where non-financial platforms offer white-label payment and lending services, creating new revenue streams and enhancing stickiness. Further accelerating live-market testing of innovative fintech solutions under lessened compliance burdens, regulatory sandboxes in Singapore, Dubai, and the U.K. help to foster innovation while maintaining consumer protections.

The adoption of BNPL and alternative lending is driving the growth of this market.

As Gen Z and millennials prefer short-term, interest-free installment plans over conventional credit cards, buy now, pay later (BNPL) has grown into a USD 3.7 trillion worldwide market by 2030. To underwrite credit for underbanked customers and SMEs in areas without sufficient credit-bureau coverage, leading fintech lenders use AI-driven alternative-data models that include social-graph indicators, utility-payment history, and mobile phone use. Compared to traditional scoring, this method lowers default rates by 25% and broadens loan penetration into new populations. Mobile-first micro-loan apps in developing countries like Southeast Asia and Africa give small merchants working-capital lines within minutes, therefore stimulating local economic activity. Though fintechs keep innovating with risk-sharing alliances and real-time portfolio analysis to preserve credit quality and compliance, regulatory frameworks are changing to manage BNPL's fast expansion, Australia's 2024 lending-code revisions, and the EU's Consumer Credit Directive amendments.

Fintech Technologies Market Restraints and Challenges:

The rising risk of cybersecurity fraud is a huge challenge being faced by this market.

Growing cyberattacks directed at fintechs as they manage more and more digital payments and customer data can halt operations and undermine confidence. Driven by sophisticated ransomware, credential-stuffing, and API-based attacks, the average cost of a data breach in the financial sector reached USD 5.9 million per incident in 2024. Real-time fraud-detection systems using artificial intelligence/machine learning are now required, scanning transaction patterns and device-fingerprint anomalies to prevent unlawful activity before finalization. While multi-factor authentication (MFA) has become commonplace, implementation complexity, that is, balancing security with frictionless UX, continues to be a barrier for conversion rates. Expectations of regulation (e.g., FFIEC in the U.S., EBA guidelines in Europe) necessitate continuous monitoring and quick incident reporting, thus encouraging fintechs to spend 15–20% of their IT budgets on managed-security services and security operations centers (SOCs). Furthermore, rising cyber-liability insurance premiums by 12% yearly mirror underwriters' concerns over systemic financial-sector exposures. This increased risk environment calls for continual security-by-design methods, zero-trust architectures, and strong third-party vendor due diligence to protect fintech ecosystems.

The market faces a great challenge from the fragmentation of rules and regulations, making it complex.

Multinational fintech companies fight with a patchwork of overlapping and frequently contradictory rules governing data privacy, licensing, anti-money-laundering (AML), and capital adequacy. Each of the GDPR of the European Union, the CCPA of California, the forthcoming DPDP of India, and Brazil's LGPD demands different data-handling and consent, therefore, companies must set up regional data-residency controls and consent-management processes. Cross-border payments have to adhere to changing AML/KYC requirements and sanction-screening policies, which add complexity and delay product debuts by 3–6 months for international rollouts. Regulatory sandboxes, while helpful in some regions, have different ranges and durations, which creates uncertainty for scalability and investment planning. Maintaining compliance calls for continuous investment in RegTech solutions like automated-reporting, transaction-monitoring-engines, and policy-as-code-frameworks that can account for dynamic rule changes, which cumulatively can consume 10–15% of fintech-operational budgets. Legal and operational risks are raised, time-to-market is slowed, and expansion costs are increased with this fragmentation.

The integration of this system with the existing ones is quite complex, making it difficult for this market to advance.

Although modernization is encouraged, many current banks and insurers still use decades-old core systems based on monolithic codebases and mainframes. Incorporating open-API gateways, digital-wallet services, and real-time payment rails, among other Fintech breakthroughs, into these historic settings calls for considerable middleware, custom adapters, and professional-services projects. According to survey findings, 62% of financial institutions have reported project delays of six to twelve months brought on by challenges in data mapping, stateful transaction reconciliation, and orchestration across heterogeneous platforms. Usually requiring dual-run periods, whereby new fintech modules run alongside traditional processes to guarantee continuous service, such integrations increase costs and human resource needs. Furthermore, aggravating factors are the shortage of qualified mainframe engineers and institutional knowledge gaps, which cause extended testing cycles and greater reliance on outside system integrators.

The market suffers from a shortage of a talented workforce, which hampers its operational efficiency.

With 54% of fintech companies claiming challenges in recruiting certified cloud architects, blockchain developers, data scientists, and compliance experts, the quick growth of fintech has surpassed the supply of specialized talent. This abilities gap raises wage expectations, experienced fintech engineers earn > USD 200000 annually in developed economies, and compels many startups to outsource essential activities to managed-service providers or consultants, which could increase O&M expenditures by 15–20%. Only 28% of colleges worldwide have committed fintech programs or collaborations with financial-services businesses; therefore, educational and training pipelines lag behind business demands. Fintech firms thus invest in internal upskilling through boot camps, vendor-sponsored certification programs, and collaborations with coding academies, but these projects take months to start bearing fruit. Relying too much on a small pool of specialists for business-critical infrastructure and security activities not only stifles product development and innovation but also exposes operational hazards.

Fintech Technologies Market Opportunities:

The increasing use of embedded finance and super-app models is said to be a major market growth opportunity.

By directly incorporating financial services into non-financial platforms, including e-commerce sites, ride-hail apps, and social media networks, embedded finance is changing customer journeys. From almost USD 0.5 trillion, The Paypers forecasts that the embedded finance and Banking-as-a-Service (BaaS) market will reach USD 7.2 trillion by 2030. Consumer demand for smooth checkout experiences, BNPL, and in-app wallets, as well as companies looking for fresh revenue streams through "banking without banks," propel this development. Incorporating lending, payments, and insurance services into company software can boost consumer lifetime value by 20–30% while lowering acquisition expenses by 15%, thanks to contextual offers and less friction, notes Deloitte. Modifiable APIs for KYC, payment processing, and risk-scoring provided by leading BaaS platforms let partners debut financial solutions in weeks rather than years. The super-app phenomenon, where a single app offers ride-hailing, food delivery, digital wallets, and microloans, has seen platforms like Grab and Gojek lock in billions of users across Southeast Asia, demonstrating the great financial possibility of embedded finance.

The use of DeFi and Tokenization is seen as a major market growth opportunity.

Using blockchain smart contracts, decentralized finance (DeFi) provides lending, borrowing, derivatives trading, and liquidity pooling devoid of central agencies. Following a decline, Total Value Locked (TVL) in DeFi protocols recovered past USD 100 billion in mid-2024, according to Bitcoin.com, indicating renewed faith in collateralized lending and yield-farming tactics. Major DeFi platforms are processing more than USD 10 billion in daily trading volume, and institutional entrants are experimenting with tokenized real-world assets, such as real estate and fine art, which widens applications beyond crypto-native markets. By allowing fractional ownership, tokenization lowers minimum investments and boosts liquidity, therefore freeing USD 16 trillion in global private-market assets over the following ten years, according to McKinsey. Regulatory transparency in countries like Switzerland and Singapore is even hastening DeFi invention as compliant on-ramps and custodial solutions appear, drawing established financial services companies to try authorized DeFi apps on corporate blockchains.

The new SME banking platforms are covering the underserved segments, helping the market to increase its reach.

Designed for small and medium-sized businesses (SMEs), cloud-native business-banking suites are grabbing a large, underserved market. According to Spherical Insights and Consulting, digital banking systems, which were valued at USD 21.2 billion in 2021, are projected to grow at a 29.7% CAGR to USD 220.1 billion by 2030. These all-in-one systems combine accounting, payroll, payments, and lending into a single dashboard that helps SMEs manage cash flow, automatically bill invoices, and access working-capital lines in minutes. The demand for locally based, mobile-first banking solutions in developing countries is highlighted by Tide's quick development in India, surpassing 700,000 SMEs in just three years. Integrating open APIs for tax filings, expense management, and e-invoicing helps these platforms to lower administrative expenses by 30–40% and increase financial transparency, therefore lowering default risk for lending partners. The addressable market for cloud-based SME banking is projected to grow at around 25% annual average through 2030 as regulatory authorities in APAC and LATAM start fintech sandboxes and SME lending programs.

The emergence of WealthTech platforms and AI-driven advisory platforms is opening up new opportunities for the market.

By 2027, WealthTech platforms are democratizing access to investment counseling via robo-advisors and AI-powered chatbots, bringing complex portfolio management to mass-affluent customers, according to PitchBook and Morningstar analysts. This represents a CAGR of around 14%, up from USD 1.1 trillion in 2023 to more than USD 2 trillion in assets under management (AUM). These solutions optimize asset allocation, rebalance portfolios in real time, and provide customized financial counsel via mobile apps using machine-learning models trained on past market data. Cost-effective fee structures, often 0.25–0.50% AUM compared to 1% for traditional advisors, are attracting younger generations; over 50% of Gen Y investors are now considering robo-advisors their main source of financial advice. Furthermore, hybrid models combining human and AI guidance are surfacing, providing “advice-as-a-service” subscriptions that combine algorithmic insights with human supervision, so broadening the market appeal and fostering continued growth in the WealthTech industry.

Fintech Technologies Market Segmentation:

Market Segmentation: By Technology

• Blockchain

• Artificial Intelligence & Machine Learning

• Big Data Analytics

• Mobile Payments

• Digital Banking

With its high share and widespread consumer transactions, the Mobile Payments segment is dominant. Encouraged by contactless adoption worldwide and connection with retail and social applications, mobile-payment technologies (wallets, NFC, QR codes) made up about 30% of the fintech market in 2024. With a 48% CAGR as DeFi and enterprise ledger usage skyrockets, blockchain is the fastest-growing sector. Blockchain supports smart contracts, cross-border transactions, and decentralized finance (DeFi). Driven by rising DeFi volumes and corporate acceptance of authorized ledgers, it accounted for about 10% of fintech technology spending in 2024.

Under the AI & ML segment, real-time risk analysis and customer insights enable AI/ML to drive fraud detection, credit scoring, and tailored advisory; it dominated roughly 25% of fintech technology budgets in 2024. With about 20% of technology spending, big-data platforms convert transaction streams and client data to drive lending decisions and marketing initiatives as businesses invest in scalable data lakes. As incumbent banks and challengers digitize account opening, loan processing, and branchless services, digital banking platforms (neo-banks, banking-as-a-service) accounted for around 15% of the technology stack.

Market Segmentation: By Application

• Lending & Credit

• Payments

• Wealth Tech

• Insurtech

• Regtech

• Others

The Payments segment dominates the market. Payments driven with nearly 30% of application spending reflect consumer and business needs for smooth transactions, encompassing mobile wallets, merchant acquiring, and remittances. Given its high transaction volume and revenue base, payments led with nearly 30% of application spending. The Regtech segment is the fastest-growing segment. RegTech, at almost 22% CAGR, is driven by rising compliance costs and regulatory complexity. Approximately 8% of application revenues are derived from compliance solutions, KYC, AML, and transaction monitoring, which is powered by stringent rules.

When it comes to the Lending & Credit segment, driven by artificial intelligence-based underwriting and rapid disbursement, digital personal, SME, and peer-to-peer lending platforms made up around 25% of fintech application income in 2024. Wealth tech consisted of about 15% of robo-advisors and algorithmic trading systems, as automated portfolio management becomes commonplace. Around 10% was made up of digital insurance distribution and use-based underwriting, which used telematics and artificial intelligence for risk evaluation. Together, making up the remaining around 12%, finance management apps, crowdfunding, and cryptocurrencies are among others.

Market Segmentation: By Deployment Mode

• Cloud

• On-premises

• Hybrid

Cloud segment dominates this market, given its cost benefits and versatility. Favored for scalability and quick delivery of new services, cloud deployments, both public and private, dominate with around 70% of fintech infrastructures. The Hybrid segment is said to be the fastest-growing one. At roughly 20% CAGR, hybrid is the fastest-growing as controlled entities combine legacy and cloud. With on-prem control and cloud agility, hybrid models have around a 10% share but are expanding at about 20% CAGR as companies look for best-of-both-worlds designs. When it comes to the On-premises segment, for total data and security control, legacy banks and major insurers keep about 20% of their systems on-premises.

Market Segmentation: By Enterprise Size

• SMEs

• Large Enterprises

The Large Enterprises segment is said to dominate the market, as big companies mirror their bigger budgets and regulatory demands. Large banks, insurance, and corporate treasuries contribute around 60% and use complex, multi-module fintech stacks on a large scale. The SMEs segment is said to be the fastest-growing segment. SMEs, at about 24% CAGR, as turnkey SaaS and DaaS products democratize access to sophisticated fintech capabilities. Employing plug-and-play solutions for payments, accounting, and lending with little IT overhead, small and medium-sized enterprises make up around 40% of fintech technology uptake.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America leads this market, for its mature market and tech leadership. Leads with about 35% market share in 2024 spurred by Silicon Valley invention and early fintech regulation. The Asia-Pacific region is said to be the fastest-growing region. Given its great unbanked population and mobile-centric payments expansion, Asia Pacific is the fastest-growing region at about 22% CAGR. This growth is driven by India's UPI real-time payments adoption and China's digital-wallet revolution.

Europe holds a 20% market share, as it is supported by open banking frameworks and PSD2. Whereas, both South America and the MEA regions are considered emerging markets. This is due to quick fintech absorption in Mexico and Brazil, fixing underbanking, growing through mobile-money systems and digital-banking efforts.

COVID-19 Impact Analysis on the Global Fintech Technologies Market:

Lockdowns and financial insecurity propelled customers and companies toward digital financial services, therefore accelerating the adoption of fintech. Global digital-payment volumes increased 30–40% in 2020–21, while digital-lending origin doubled in many countries. Quickly introducing contactless payments, remote-onboarding KYC, and SME assistance-loan systems, fintechs condensed multi-year digital transformation roadmaps into quarters. This change set fintech as vital infrastructure and forever changed consumer behavior, so supporting continuous development even post-pandemic.

Latest Trends/ Developments:

Under a single UX, platforms like Grab and WeChat combine payments, lending, insurance, and investments.

Real-time, low-cost foreign transfers made possible by ISO 20022 adoption upset existing correspondent-bank systems.

Providing regulated environments for live-market testing, jurisdictions (U.K., Singapore, UAE) speed fintech innovation.

Central bank digital currencies are under experimental trial (e.g., China's e-CNY; Nigeria's e-Naira), which could transform payment and settlement processes.

Key Players:

• NVIDIA Corporation

• Microsoft

• Goldman Sachs

• Cisco Systems Inc.

• Bankable

• Blockstream Corporation Inc.

• Circle Internet Financial Limited

• Tata Consultancy Services Limited

• ORACLE

• IBM Corporation

Chapter 1. Global Fintech Technologies Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Fintech Technologies Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Fintech Technologies Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Fintech Technologies Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Fintech Technologies Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Fintech Technologies Market- By Technology

6.1. Introduction/Key Findings

6.2. Blockchain

6.3. Artificial Intelligence & Machine Learning

6.4. Big Data Analytics

6.5. Mobile Payments

6.6. Digital Banking

6.7. Y-O-Y Growth trend Analysis By Technology

6.8. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 7. Global Fintech Technologies Market– By Application

7.1 Introduction/Key Findings

7.2. Lending & Credit

7.3. Payments

7.4. Wealth Tech

7.5. Insurtech

7.6. Regtech

7.7. Others

7.8. Y-O-Y Growth trend Analysis By Application

7.9. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Fintech Technologies Market– By Deployment Mode

8.1. Introduction/Key Findings

8.2. Cloud

8.3. On-premises

8.4. Hybrid

8.5. Y-O-Y Growth trend Analysis By Deployment Mode

8.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 9. Global Fintech Technologies Market– By Enterprise Size

9.1. Introduction/Key Findings

9.2. SMEs

9.3. Large Enterprises

9.4. Y-O-Y Growth trend Analysis By Enterprise Size

9.5. Absolute $ Opportunity Analysis By Enterprise Size, 2025-2030

Chapter 10. Global Fintech Technologies Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Technology

10.1.3. By Application

10.1.4. By Deployment Mode

10.1.5. By Enterprise Size

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Technology

10.2.3. By Application

10.2.4. By Deployment Mode

10.2.5. By Enterprise Size

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Technology

10.3.3. By Application

10.3.4. By Deployment Mode

10.3.5. By Enterprise Size

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Technology

10.4.3. By Application

10.4.4. By Deployment Mode

10.4.5. By Enterprise Size

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Technology

10.5.3. By Application

10.5.4. By Deployment Mode

10.5.5. By Enterprise Size

10.5.6. By Region

Chapter 11. Global Fintech Technologies Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. NVIDIA Corporation

11.2. Microsoft

11.3. Goldman Sachs

11.4. Cisco Systems Inc.

11.5. Bankable

11.6. Blockstream Corporation Inc.

11.7. Circle Internet Financial Limited

11.8. Tata Consultancy Services Limited

11.9. ORACLE

11.10. IBM Corporation

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Fintech Technologies Market was valued at USD 356.73 billion and is projected to reach a market size of USD 686.85 billion by the end of 2030 with a CAGR of 14%.

Led by consumer desire for smooth, real-time transactions, the payments segment including mobile wallets and cross-border remittances, contribute for around 30% of fintech income.

Open-banking laws (PSD2, U.K. Open Banking) and regulatory sandboxes offer API access to banking information and a regulated environment for live-market testing, therefore speeding product development and market penetration.

A 30–40% increase in digital-payment volumes and a doubling of digital-lending origination driven by the epidemic, confirmed fintech as necessary for contactless trade, SME relief loans, and remote banking.

Driven by large unbanked populations, smartphone proliferation, government digital-economy efforts, and rapid e-wallet adoption, Asia Pacific is fastest growing at around 22% CAGR.