Global Enterprise Communication Infrastructure Market Research Report – Segmentation By Component (Hardware, Software, Services), By Deployment (On-premises, Cloud-based), By Technology (SD-WAN, Unified Communication, Secured Access Service Edge, Optical Transport), By End-Use Industry (IT & Telecom, BFSI, Healthcare, Government, Retail & E-Commerce, Others), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-969

Format:

Region: Global

Market Size and Overview:

The Global Enterprise Communication Infrastructure Market was valued at USD 111.84 billion and is projected to reach a market size of USD 252.09 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 17.65%.

Extensive cloud migration, hybrid-work methods, and next-generation networking solutions introduce this expansion. Addressing demands for great bandwidth, low latency, security, and centrally managed orchestration across worldwide enterprise footprints, these solutions include hardware (routers, switches, optical transport) from both on-premise and cloud-based sources as well as software (SD-WAN controllers, UCaaS platforms) and managed services.

Key Market Insights:

Driven by operators outsourcing the complexity of multi-vendor settings and 24/7 monitoring, managed network and security solutions comprise 60% of all revenue.

As companies use agile, policy-driven overlays to replace ancient MPLS connections and provide safe remote access and branch connections, SD-WAN and SASE software solutions are expanding at a 20% CAGR.

Still 25% of hardware revenue, high-capacity optical DWDM systems reflect ongoing demand for backbone improvements to enable 5G backhaul and cloud-on-ramps.

Driven by national digital-economy plans, cloud adoption, and fast mobile broadband infrastructure development, APAC is the fastest rising area with an 18% CAGR.

Enterprise Communication Infrastructure Market Drivers:

The increasing popularity of remote work and Hybrid Workforce Models is driving the growth of this market.

Driven by the need for continuous security attitude and low-latency access irrespective of location, this migration decreases branch-to-cloud provisioning times by up to 60% in pilot deployments. Furthermore, businesses using SASE claim a 25% decrease in mean time to remediation (MTTR) for security incidents because of centralized analytics and automated policy enforcement. The demand for integrated communications infrastructure that smoothly enables remote-worker security and performance keeps driving market expansion as hybrid work becomes the norm.

The rollout of 5G networks and Edge Computing Systems is considered a major market growth driver.

Driven by demand for edge-optimized communication infrastructure, including on-premise micro-data centers and edge routers, to satisfy ultra-low-latency requirements, global 5G subscriptions reached over 1.5 billion connections by early 2025. Underlining applications like AR/VR cooperation, real-time IoT analytics, and Industry 4.0 automation, 5G connectivity is expected to reach 2 billion by end-2025. As a result, network operators and companies are pouring money into converged optical and IP-/MPLS backbones to provide deterministic performance from the edge to the core, hence increasing optical-transport revenues by 18% every year. Up to 35% of backhaul traffic is decreased, and application reaction times for distributed workforces are enhanced when edge compute installations co-located with 5G base stations enable packet inspection, caching, and AI inference at the network edge. Enterprises are giving top priority to communication architectures that combine high-bandwidth wireless access with edge computing for next-generation services as 5G infrastructure spreads.

The rapid migration towards cloud-managed services is helping the market to grow.

With public-cloud IaaS spending expected to expand at a 19.4% CAGR from 2024 to 2028, reaching USD 1.6 trillion, enterprises are fast transferring branch and campus networks to cloud-managed solutions, according to IDC. This rise in cloud adoption calls for integrated WAN-to-cloud connection solutions, including SD-WAN-as-a-Service and direct cloud on-ramps, to guarantee consistent QoS and security across multi-cloud deployments. Cloud-based orchestration platforms allow centralized management of network policies and fast deployment of new sites, therefore reducing provisioning cycles from weeks to days. Furthermore, the move to OPEX-based cloud models fits with more general IT trends and lowers hardware refresh capital costs by 25% while increasing agility to scale bandwidth up or down as needed. Software-driven, service-centric architectures are more and more used in the enterprise communication infrastructure market as CIOs adopt "cloud-first" directives.

The increasing adoption of Zero-Trust technology is driving the growth of this market.

Driven by a desire for constant verification of users, devices, and sessions in hybrid environments, Zero Trust frameworks, combining ZTNA, FWaaS, CASB, and micro-segmentation, are becoming the fastest-growing network-security paradigm. A recent research shows that 65% of companies intend to replace VPNs with ZTNA within 12 months, citing better threat containment and lower lateral-movement risk. Driven by demand for continuous verification of users, devices, and sessions in hybrid environments, Zero Trust adoption is projected to grow at a 19.6% CAGR through 2026. Combined SASE and Zero Trust deployments cut incident response times by 30% and reduce breach remediation costs by 25%, as policy enforcement is consistently applied across network edges and cloud resources. Cyber-resilience top-of-mind, businesses are deepening security into their communication infrastructure, so supporting the market’s expansion trajectory.

Enterprise Communication Infrastructure Market Restraints and Challenges:

The market faces a challenge due to the complexity involved in integrating with the existing legacy infrastructure.

Many businesses still depend on divided old networks, comprising MPLS circuits, legacy VPNs, and on-premises firewalls, that were never meant for cloud-centric, software-defined overlays. Often requiring phased "hybrid" designs where priority locations are moved and lower priority locations come next after compatibility problems are ironed out, incorporating SD-WAN and SASE solutions into these heterogeneous environments calls for integration. Every phase calls for customized middleware or connector creation to bridge old routing tables, QoS policies, and security devices with fresh controllers, thereby lengthening migration schedules by 6–12 months on average. As legacy equipment could lack APIs or sophisticated orchestration hooks, manual adjustments and thorough regression testing further complicate cut-over events and raise the danger of service interruptions during switchover. Network designers must conduct complete infrastructure audits, keep parallel operations of legacy and new overlays, and invest in personnel training to manage both environments in concert to lessen these pain points.

The high level of initial CapEx poses a significant challenge for this market.

Large campus networks and multi-site businesses can incur upwards of USD 1 million in initial CapEx in hardware licenses, rack space provisioning, power provisioning, and on-site installation labor in addition to costs for upgrades to next-generation optical transport systems (e.g., DWDM, ROADM). For smaller companies, these large-scale capital expenditures create major financial challenges, particularly when ROI is linked to marginal OPEX savings or better latency. Many businesses are bound by current capital-allocation procedures, even if cloud-based network-as-a-service models can move spending to OPEX, therefore postponing modernization projects. To reduce adoption obstacles, vendors and service providers must therefore provide phased purchase choices, flexible financing, or consumption-based pricing.

The market is challenged significantly by the problem of a shortage of skilled workers, which hampers market growth.

The design, deployment, and ongoing management of converged communication infrastructures is hampered by a chronic worldwide deficit of network-security and communication experts, estimated at 40% of required roles. LinkedIn statistics indicate that companies struggle to find candidates for network-automation experts, SASE architects, and SD-WAN engineers, jobs necessitating hybrid knowledge in routing, security, and cloud orchestration. This skill gap causes several companies to depend on managed service providers, which can raise continuous expenses and degrade institutional knowledge. Companies are investing in upskilling their internal teams through collaborations with vendors and colleges, as well as deploying low-code/AI-driven tools to lessen dependence on deep technical capabilities to address the scarcity.

The issues related to interoperability and standards are a major concern for the market.

The abundance of unique APIs, policy languages, and security systems among proprietary SD-WAN controllers presents interoperability problems when combining several vendor stacks or transferring workload across settings. Similarly, emerging SASE solutions bring SD-WAN, FWaaS, CASB, and ZTNA together under several architectures, making it difficult to establish uniform policy enforcement across branch offices and hybrid clouds. Development of unique connectors often results in longer integration timelines and greater professional-service costs for companies without industry-wide standards or conformance testing. Although efforts such as MEF's SD-WAN and SASE certification initiatives aim to promote standardization, widespread adoption is still in progress. Enterprises should design for vendor-agnostic processes—that is, employing abstract layers and consistent data models, in the meantime, to reduce lock-in and simplify multi-vendor orchestration.

Enterprise Communication Infrastructure Market Opportunities:

The adoption of AI-driven network automation is seen as a major market opportunity.

Early adopters using artificial intelligence-powered orchestration engines, which analyze telemetry from routers, switches, and security devices in real time to automate incident triage, predictive maintenance, and dynamic traffic routing, reduce mean time to resolution (MTTR) by up to 30%. Natural-language-driven chatbots and digital assistants automate basic support chores, such as ticket creation and status checks, freeing network engineers to concentrate on more valuable projects and boosting operational efficiency by 25%. The accuracy of AI models keeps getting better as businesses gather more data from cloud, edge, and IoT environments, therefore producing a virtuous cycle of automation and performance gains.

The use of converged 5 G networks and fixed infrastructure helps the market expand.

Private-5G's ultra-low latency (< 1 ms) and high bandwidth (up to 10 Gbps) add to fiber's dependability, therefore facilitating the deployment of converged-wireless-wired networks that support Industry 4.0 and IoT applications by companies. Integrated platforms from businesses like NTT and Schneider Electric now provide containerized edge-compute nodes co-located with 5 G radios and fiber backhaul, hence simplifying deployment and scaling across big campuses. Converged dashboards offer single-pane visibility into spectrum utilization, quality of service, and network slices, therefore allowing dynamic reallocation of resources to critical applications during peak loads.

The recent adoption of ZTNA and SASE is said to reduce incidents of security breaches, increasing efficiency.

Double-digit growth is expected for Secure Access Service Edge (SASE), which combines SD-WAN, FWaaS, CASB, and Zero Trust Network Access (ZTNA). The market is projected to grow from USD 15.5 billion in 2025 to USD 44.7 billion at a 23.6% CAGR by 2030. SASA adoption grows to protect dispersed users, branch offices, and cloud workloads under one policy framework as businesses embrace Zero Trust architectures, therefore lowering security breaches by 25% and streamlining operations. Managed-SASE solutions enable MSSPs, who can provide ready-to-use connection and protection without big upfront expenditures, to unlock fresh recurring revenue streams by combining network and security services. Constant authentication and micro-segmentation from integrating with identity providers and endpoint agents reduces lateral threat movement and guarantees compliance with data-protection rules.

The adoption of green networking solutions will reduce the carbon footprint of the market.

With ICT's carbon footprint estimated to reach up to 21% of global electricity consumption by 2030, sustainability requirements are driving demand for energy-efficient network equipment, so-called "green switches" and optical amplifiers designed for low-power operation and recyclability. AI-driven power-management capabilities dynamically power down dormant ports and line cards, lowering switch energy usage by 30% during non-peak hours. Vendors like Nvidia are embedding silicon-photonics directly into switch ASICs, eliminating external transceiver modules and reducing per-port power by over 50% in next-generation data-center fabrics. Studies emphasize incremental approaches like DC-power deployment and PoE-power-capping policies to reduce AC conversion losses even more and customize energy use to real-time consumption patterns. When businesses incorporate energy indicators onto network-management dashboards, green networking solutions are crucial for achieving ESG objectives while generating operational expense reductions.

Enterprise Communication Infrastructure Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

• Services

The Hardware segment dominates the market. Backed by expenditures in high-capacity optical DWDM and WAN-edge equipment to enable bandwidth-hungry workloads, hardware solutions generate roughly 40% of market income. The Software segment is the fastest-growing. At 20% CAGR, software-defined infrastructure is the fastest growing as businesses substitute cloud-native overlays, including security, routing, and collaboration for traditional MPLS and stand-alone UC. The Services segment is driven by the complexity of multi-vendor surroundings and the necessity of 24x7 monitoring, updates, and support; managed services control 60% of all spending.

Market Segmentation: By Deployment

• On-premises

• Cloud-based

The Cloud-based segment is both the dominant and the fastest-growing segment of the market, with over 55% share in 2024 and expanding at 15% CAGR. Cloud deployments offer rapid rollout, elastic scaling, and continuous feature updates, ideal for hybrid work and global operations. Though its relative share is gradually declining, the on-premises segment preferred by regulated sectors and large campuses for data sovereignty and extensive customization remains at about 45%.

Market Segmentation: By Technology

• SD-WAN

• Unified Communication

• Secured Access Service Edge

• Optical Transport

The SD-WAN segment dominates the market as it holds around 30% market share. It has replaced the WAN technology by routing the traffic over multiple links due to better policy and performance. The SASE segment is said to be the fastest-growing segment. Projected at 25% CAGR as companies embrace Zero Trust architectures that merge SD-WAN, FWaaS, CASB, and ZTNA for unified network-security policies.

The Unified Communications (UCaaS/Collaboration) segment accounts for around 25%; growth is driven by remote-work requirements and integration of voice, video, and messaging into unified systems. The Optical Transport (ROADM, DWDM) segment, making up around 25% of hardware costs, is backbone networks as they are upgraded to enable high-throughput data centers, cloud on-ramps, and 5G backhaul.

Market Segmentation: By End-Use Industry

• IT & Telecom

• BFSI

• Healthcare

• Government

• Retail & E-Commerce

• Others

The IT & Telecom segment dominates this market, with around 35% share, as service providers and major businesses continually update their underlying and edge networks to enable fresh offerings. The Healthcare segment is the fastest-growing segment of the market, driven by demanding latency and security needs for digital banking, trading systems, and payment networks.

BFSI has a share of around 20%. This market is defined by strict security requirements for digital banking, payment networks, and trading platforms. When it comes to the Government segment, under national digital agendas, the government supports e-government services, public-safety communications, and intelligent city networks. The Retail & E-commerce segment is driven by omnichannel convergence, POS connectivity, and supply-chain tracking requirements, about ten percent of the share. The Others segment has a 15% share employing private 5 G trials, IoT-enabled networks, and campus-network modernization for Industry 4.0 applications.

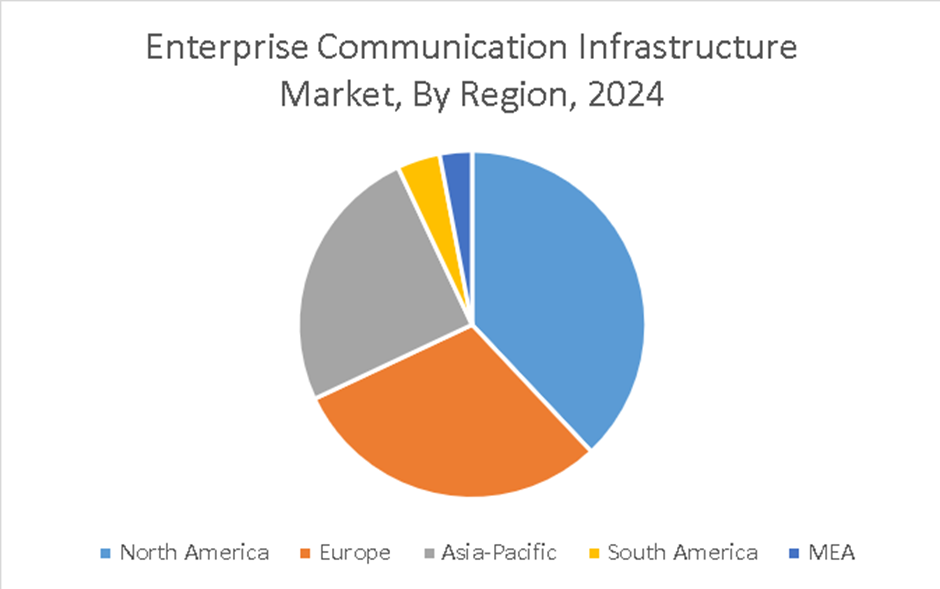

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America dominates this market, and the Asia-Pacific region is the fastest-growing one. North America is supported by high levels of budgets, strict laws regarding data security, and a large service-provider network. The Asia-Pacific region is defined by the rapid rollout of 5 G networks, a growing adoption rate of cloud-based technology, and better digital economy policies.

Driven by GDPR compliance requirements, robust SME digital initiatives, and pan-EU 5G corridors, Europe has roughly 25% of the market. South America and the MEA regions are considered emerging markets, with a combined share of about 20%, growing at a 10–12% CAGR as emerging-market operators enhance legacy MPLS and invest in cloud-managed WANs to seize digital transformation possibilities.

COVID-19 Impact Analysis on the Global Enterprise Communication Infrastructure Market:

As companies looked for safe, resilient connectivity for dispersed employees, remote work adoption accelerated a 30% rise in SD-WAN installations in 2020–2021. Demand for unified-communications solutions doubled to support digital-collaboration tools, while investment in cloud-managed WAN services increased 25%, therefore lowering dependence on on-site IT teams and allowing fast scaling during lockdowns. The change revealed shortcomings in conventional MPLS networks, spurring a rapid move to agile, software-defined overlays and fuelling long-run budgets for digital infrastructure upgrade.

Latest Trends/ Developments:

Reducing WAN latency and increasing SLAs, suppliers integrate artificial intelligence for dynamic path selection and anomaly detection.

Telecom companies use Open RAN designs to build hybrid enterprise-grade private-5G networks blended with central WAN overlays.

Providers' exposed RESTful APIs allow for easy integration with ITSM, SIEM, and orchestrating solutions, facilitating end-to-end automation.

As part of corporate ESG targets, energy-efficient switches and optics are gaining popularity with certain vendors promising carbon-neutral product lines by 2030.

Key Players:

• Microsoft Corporation

• AT&T Intellectual Property

• CISCO Systems

• Avaya LLC

• Orange Businesses

• ALE International

• Verizon

• DXC Technology Company

• NEC Corporation

• ALE USA Inc.

Chapter 1. Global Enterprise Communication Infrastructure Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Enterprise Communication Infrastructure Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Enterprise Communication Infrastructure Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Enterprise Communication Infrastructure Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Enterprise Communication Infrastructure Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Enterprise Communication Infrastructure Market– By Component

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global Enterprise Communication Infrastructure Market– By Deployment

7.1 Introduction/Key Findings

7.2 On-Premises

7.3 Cloud-Based

7.4. Y-O-Y Growth trend Analysis By Deployment

7.5. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 8. Global Enterprise Communication Infrastructure Market– By Technology

8.1. Introduction/Key Findings

8.2. SD-WAN

8.3. Unified Communication

8.4. Secured Access Service Edge

8.5. Optical Transport

8.6. Y-O-Y Growth trend Analysis By Technology

8.7. Absolute $ Opportunity Analysis By Technology, 2025-2030

Chapter 9. Global Enterprise Communication Infrastructure Market– By End-User

9.1. Introduction/Key Findings

9.2. IT & Telecom

9.3. BFSI

9.4. Healthcare

9.5. Government

9.6. Retail & E-commerce

9.7. Others

9.8. Y-O-Y Growth trend Analysis By End-User

9.9. Absolute $ Opportunity Analysis By End-User, 2025-2030

Chapter 10. Global Enterprise Communication Infrastructure Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Deployment

10.1.4. By Technology

10.1.5. By End-User

10.1.6 By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Deployment

10.2.4. By Technology

10.2.5. By End-User

10.2.6. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Deployment

10.3.4. By Technology

10.3.5. By End-User

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Deployment

10.4.4. By Technology

10.4.5. By End-User

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Deployment

10.5.4. By Technology

10.5.5. By End-User

10.5.6. By Region

Chapter 11. Global Enterprise Communication Infrastructure Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Microsoft Corporation

11.2. AT&T Intellectual Property

11.3. CISCO Systems

11.4. Avaya LLC

11.5. Orange Businesses

11.6. ALE International

11.7. Verizon

11.8. DXC Technology Company

11.9. NEC Corporation

11.10. ALE USA Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Enterprise Communication Infrastructure Market was valued at USD 111.84 billion and is projected to reach a market size of USD 252.09 billion by the end of 2030 with a CAGR of 17.65%.

The Software Segment is said to be the fastest-growing segment for this market due to the favoring of cloud-native, policy-driven overlays.

As companies moved to remote work and digital-collaboration models, the epidemic triggered a 30% rise in SD-WAN and a 25% increase in cloud-managed WAN service usage.

With an 18% CAGR, Asia Pacific is in front, driven by strong 5G deployments, digital-economy projects, and increasing corporate cloud adoption in China and India.

Look for Open RAN integrations for private-5G, API-first orchestration ecosystems, sustainability-focused hardware inventions, and AI-enabled network automation are some of the key trends related to the market.