Global Edge Data Center Market Research Report – Segmentation by Component (Solutions and Services); By Size (Micro Data centers, Hyperscale/enterprise Data Center, Others); By Application (BFSI, Colocation, Energy, Government, Healthcare, Manufacturing, IT & Telecom, Others); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16561

Format:

Region: Global

Market Size and Overview:

The Global Edge Data Center Market was valued at USD 13.83 billion in 2024 and is projected to reach a market size of USD 41.53 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 24.6%.

The Edge Data Center Market refers to a growing segment of the data center industry focused on deploying smaller, decentralized facilities closer to end users and devices. Unlike traditional centralized data centers, edge data centers are strategically located to reduce latency, enhance real-time data processing, and improve user experiences in applications such as IoT, 5G, autonomous systems, streaming, and smart cities. These centers support rapid data exchange by minimizing the distance data must travel, thereby enabling faster decision-making and more efficient network performance. As digital transformation accelerates and demand for low-latency services rises, edge data centers are becoming critical infrastructure for enabling next-generation technologies and delivering scalable, distributed computing capabilities across various industries.

Key Market Insights:

Over 65% of telecom providers worldwide have started integrating edge data centers to support expanding 5G networks and deliver faster, localized services. These deployments are aimed at reducing latency and improving network performance for data-heavy applications like autonomous vehicles, gaming, and industrial automation.

More than 50% of enterprises are shifting toward hybrid infrastructure models, combining centralized and edge computing to manage workloads more efficiently. This allows businesses to process critical data at the edge while relying on core data centers for storage and analytics, improving operational speed and responsiveness.

By 2026, over 70% of IoT-generated data is expected to be processed at the edge rather than centralized cloud platforms. This shift is being driven by the demand for real-time data handling in applications such as smart factories, healthcare monitoring, and connected retail, all of which rely on immediate insights and minimal data transfer delays.

Edge Data Center Market Drivers:

Explosive Growth of IoT Devices Is Creating Unprecedented Demand for Localized Data Processing

The rapid proliferation of IoT devices across industries—ranging from smart homes and wearables to industrial sensors and autonomous machinery—is generating enormous volumes of data that require real-time analysis and response. Traditional centralized data centers are often unable to handle the low-latency demands of these devices due to physical distance and network congestion. Edge data centers resolve this challenge by bringing processing capabilities closer to the source, reducing latency and enabling faster decision-making. This is especially critical in use cases like healthcare monitoring, connected vehicles, and smart factories where milliseconds can make a significant difference. As IoT continues to scale, the need for localized, responsive infrastructure is becoming an essential driver of the edge data center market.

Rollout of 5G Networks Is Accelerating the Need for Distributed Infrastructure

The global expansion of 5G technology is fueling massive demand for edge data centers to support the ultra-low-latency and high-bandwidth requirements of next-generation applications. Unlike previous network generations, 5G is designed to enable real-time communication between devices, making centralized processing models inefficient for many emerging use cases. Edge data centers act as key enablers of 5G, providing localized computing resources to offload data from the core network and support services such as augmented reality, autonomous vehicles, and smart city infrastructure. The closer proximity of edge facilities to users enhances the performance of 5G applications, making edge deployment a foundational element in the success of this transformative technology.

Rising Demand for Real-Time Analytics and Instantaneous Decision-Making Across Industries

Industries such as manufacturing, logistics, healthcare, and retail are increasingly dependent on real-time analytics to fuel efficiency, reduce downtime, and personalize services. Edge data centers allow companies to analyze data at or near the source, eliminating the delay associated with transferring information to distant cloud servers. This is especially beneficial in critical environments like production lines, emergency care, and financial transactions, where immediate data processing is essential. The ability to make split-second decisions based on localized data not only improves responsiveness but also strengthens security by limiting unnecessary data transmission. This shift in data strategy is encouraging more organizations to embrace edge computing as a core operational model.

Increased Adoption of AI and Machine Learning Is Driving the Need for Decentralized Processing Power

Artificial intelligence and machine learning technologies require rapid, high-volume data processing to function effectively, especially when applied in real-time environments like predictive maintenance, facial recognition, and smart surveillance. While traditional data centers provide the necessary computing power, they often introduce latency and bandwidth limitations due to distance and traffic. Edge data centers solve this problem by bringing AI processing closer to the endpoint, enabling faster insights and immediate actions. Additionally, the growth of AI at the edge—where devices make independent decisions without relying on the cloud—is further accelerating the need for scalable, decentralized infrastructure.

Edge Data Center Market Restraints and Challenges:

High Infrastructure Costs, Limited Standardization, and Security Concerns Pose Significant Barriers to Edge Data Center Expansion

While the demand for edge data centers is rapidly increasing, several key challenges are hindering widespread deployment. One of the most prominent restraints is the high cost of setting up and maintaining multiple decentralized facilities, including investments in hardware, connectivity, energy management, and security. Unlike centralized data centers, edge sites often operate in remote or underserved areas, requiring additional expenses for environmental control, physical protection, and reliable power sources. Furthermore, the lack of standardized frameworks for edge infrastructure makes integration and scalability complex for service providers. Security and data privacy also remain critical concerns, as edge locations may be more vulnerable to physical and cyber threats because of their distributed nature. These factors collectively slow down adoption, especially among smaller organizations with limited IT budgets.

Edge Data Center Market Opportunities:

The Edge Data Center Market is poised for significant growth as emerging technologies such as autonomous vehicles, smart cities, augmented reality, and industrial IoT increasingly require ultra-low-latency processing closer to data sources. One of the biggest opportunities lies in expanding digital infrastructure into rural and underserved regions, where edge data centers can enable localized computing, bridge connectivity gaps, and support remote healthcare, education, and agricultural solutions. Additionally, industries like retail, manufacturing, and logistics are exploring edge applications to enhance customer experiences, enable real-time supply chain tracking, and automate operations. With rising enterprise interest in decentralized architecture, combined with ongoing advancements in AI, 5G, and micro data center designs, the edge landscape is rapidly expanding, offering new avenues for innovation and investment.

Edge Data Center Market Segmentation:

Market Segmentation: By Component:

• Solution

• Services

In the Edge Data Center Market, solutions form the dominant segment as they include the essential hardware, software, and infrastructure needed to build and operate edge facilities. These solutions cover power and cooling systems, racks, networking equipment, monitoring software, and physical security—everything required to deploy and manage decentralized data centers effectively. As businesses increasingly seek to reduce latency and bring computing closer to the source of data generation, need for complete, scalable, and energy-efficient edge solutions has surged. Enterprises and telecom operators prioritize robust solutions that can support real-time applications, environmental variability, and remote operability, making this segment the backbone of the market.

ervices, on the other hand, are the fastest-growing segment, driven by the increasing demand for consulting, system integration, deployment support, and managed services. With many organizations lacking the internal expertise to design, install, and operate edge environments, service providers are playing a critical role in enabling seamless adoption. Additionally, as edge facilities are often distributed across multiple locations, ongoing maintenance, remote monitoring, and technical support have become vital for ensuring consistent uptime and performance. This growing reliance on professional and managed services is fueling rapid expansion in this segment, especially among enterprises scaling their edge strategies across regions and industries.

Market Segmentation: By Size:

• Micro Data centers

• Hyperscale/Enterprise Data Center

• Other

In the Edge Data Center Market, micro data centers are the dominant segment, as they are specifically designed to deliver localized computing power with low latency in compact, modular formats. These small-scale facilities are ideal for deployment in remote locations, closer to end users and data sources, supporting real-time processing for IoT, 5G, and smart applications. Their ability to function independently with integrated power, cooling, and security systems makes them highly suitable for industries such as retail, healthcare, telecom, and manufacturing. As edge computing continues to expand, micro data centers are increasingly favored for their flexibility, ease of deployment, and cost-effectiveness in delivering decentralized infrastructure.

Hyperscale/enterprise data centers, while traditionally associated with centralized cloud processing, are emerging as the fastest-growing segment in the edge ecosystem due to their evolving role in hybrid infrastructure models. Large enterprises are now adapting hyperscale architectures to support edge operations by deploying smaller, modular versions of their centralized data centers closer to specific regions or operational zones. These facilities handle more complex processing tasks while working in conjunction with micro edge units, creating a distributed yet scalable framework. This trend is gaining traction among technology giants and cloud service providers aiming to improve global coverage and reduce data latency across user bases.

Market Segmentation: By Application:

• BFSI

• Colocation

• Energy

• Government

• Healthcare

• Manufacturing

• IT & Telecom

• Others

In the Edge Data Center Market, IT & Telecom is the dominant application segment, driven by the sector’s demand for ultra-low latency, high-bandwidth data processing to support technologies like 5G, IoT, and cloud computing. Telecom providers and tech companies are rapidly deploying edge data centers to enhance network performance, reduce backhaul traffic, and deliver faster digital services to end users. With rising mobile data usage and the global expansion of 5G networks, edge infrastructure has become essential for enabling seamless connectivity, real-time content delivery, and distributed computing environments across urban and remote areas alike.

Healthcare is emerging as the fastest-growing application segment, fueled by the rising demand for real-time patient monitoring, connected medical devices, and telemedicine services. Edge data centers enable local data processing near healthcare facilities, ensuring faster diagnostics, minimal latency, and secure handling of sensitive medical records. This localized approach supports mission-critical applications such as AI-based imaging, emergency response, and remote surgeries, where every millisecond counts. The healthcare sector’s push for digital transformation and data-driven care is accelerating the adoption of edge computing solutions, especially in both urban hospitals and rural clinics.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

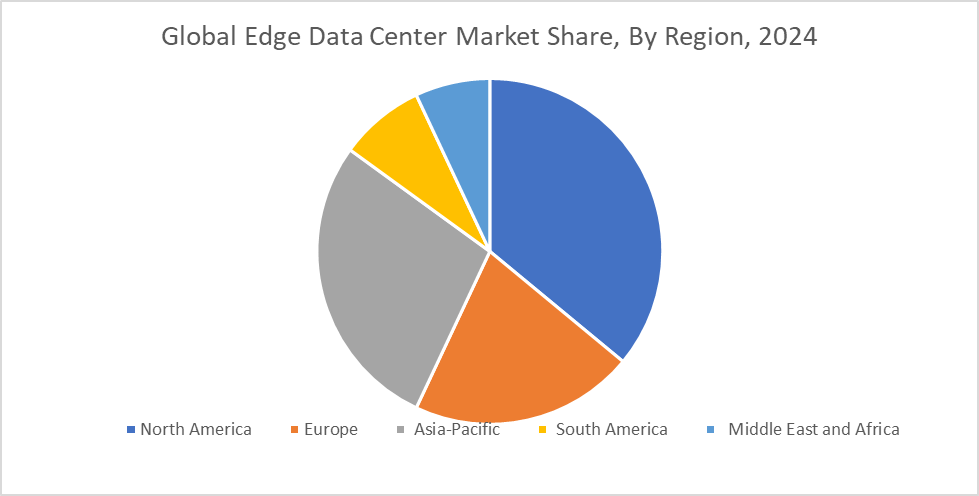

North America holds the dominant position in the Edge Data Center Market, contributing the largest share because of its mature IT infrastructure, early adoption of advanced technologies, and the strong presence of key cloud service providers and telecom giants. The U.S., in particular, has seen widespread deployment of edge facilities to support growing data demands from industries like autonomous transportation, smart cities, and streaming services. In addition, North America’s aggressive rollout of 5G networks and investments in IoT ecosystems are further accelerating edge expansion. The region’s technological readiness, along with regulatory support and high internet penetration, continues to fuel its leadership in the global edge data center landscape.

Asia-Pacific is the fastest-growing region, driven by rapid digital transformation, rising internet usage, and expanding urban infrastructure across countries like China, India, Japan, and South Korea. With a booming population and increasing adoption of mobile devices, the region is experiencing a surge in data traffic, which is pushing telecom providers and enterprises to adopt edge computing for low-latency and real-time processing. Government initiatives supporting smart city development, Industry 4.0, and rural digital connectivity are also contributing to the fast-paced growth. As Asia-Pacific continues to scale its 5G networks and IoT applications, the demand for localized edge data centers is accelerating faster than any other region globally.

COVID-19 Impact Analysis on the Global Edge Data Center Market:

The COVID-19 pandemic significantly accelerated the growth of the Edge Data Center Market by increasing reliance on digital infrastructure and remote connectivity. As remote work, online education, telemedicine, and streaming services surged, so did the demand for low-latency, high-speed data processing closer to end users. This shift exposed the limitations of centralized data centers and emphasized the need for decentralized edge facilities that could handle real-time data traffic efficiently. Enterprises and service providers began fast-tracking edge deployments to support growing bandwidth needs and ensure seamless digital experiences, laying the foundation for long-term growth in distributed computing.

Latest Trends/ Developments:

A major trend shaping the Edge Data Center Market is the rapid integration of AI and automation to manage and optimize operations across decentralized facilities. As edge sites are often deployed in remote or distributed locations, operators are leveraging AI for real-time monitoring, predictive maintenance, and autonomous performance tuning. Intelligent systems can detect and resolve issues before they escalate, reducing downtime and operational costs. Automation is also enabling lights-out data centers—facilities that run without human intervention—allowing for scalable edge deployments with minimal physical oversight.

Another significant development is the growing adoption of modular and prefabricated edge data centers that offer quick deployment, scalability, and adaptability. These containerized solutions are being used across various industries to bring computing power closer to users without the need for large infrastructure investments. At the same time, companies are focusing on energy efficiency and sustainability by incorporating advanced cooling systems, renewable energy sources, and compact designs. Additionally, telecom operators are integrating edge data centers into their 5G infrastructure to support real-time applications such as autonomous vehicles, smart cities, and immersive media. Together, these innovations are driving faster, more efficient, and more sustainable edge computing ecosystems.

Key Players:

• ATC IP LLC

• Cisco Systems Inc

• Dell Inc.; Eaton

• EdgeConneX Inc.

• Endeavor Business Media, LLC

• Fujitsu

• Hewlett Packard Enterprise Development LP

• Huawei Technologies Co., Ltd.

• IBM

• NVIDIA Corporation

Chapter 1. Global Edge Data Center Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Edge Data Center Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Edge Data Center Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Edge Data Center Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Edge Data Center Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Edge Data Center Market – By Component

6.1. Solution

6.2. Services

6.3. Y-O-Y Growth trend Analysis By Component

6.4. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global Edge Data Center Market – By Size

7.1. Micro Data Center

7.2. Hyperscale/Enterprise Data Center

7.3. Others

7.4. Y-O-Y Growth trend Analysis By Size

7.5. Absolute $ Opportunity Analysis By Size, 2025-2030

Chapter 8. Global Edge Data Center Market – By Application

8.1. BFSI

8.2. Colocation

8.3. Energy

8.4. Government

8.5. Healthcare

8.6. Manufacturing

8.7. IT & Telecom

8.8. Others

8.9. Y-O-Y Growth trend Analysis By Application

8.10. Absolute $ Opportunity Analysis By Application, 2024-2030

Chapter 9. Global Edge Data Center Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Component

9.1.3. By Size

9.1.4. By Application

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Component

9.2.3. By Size

9.2.4. By Application

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Component

9.3.3. By Size

9.3.4. By Application

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Component

9.4.3. By Size

9.4.4. By Application

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Component

9.5.3. By Size

9.5.4. By Application

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Edge Data Center Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1 ATC IP LL

10.2 Cisco Systems Inc

10.3 Dell Inc.; Eaton

10.4 EdgeConneX Inc.

10.5 Endeavor Business Media, LLC

10.6 Fujitsu

10.7 Hewlett Packard Enterprise Development LP

10.8 Huawei Technologies Co., Ltd.

10.9 IBM

10.10 NVIDIA Corporation

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Edge Data Center Market was valued at USD 13.83 billion in 2024 and is projected to reach a market size of USD 41.53 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 24.6%.

Rising demand for low-latency processing, 5G deployment, and real-time data handling.

Based on Size, the Global Edge Data Center Market is segmented into Micro and Hyperscale.

North America is the most dominant region for the Global Edge Data Center Market.

ATC IP LLC, Cisco Systems Inc, Dell Inc., Eaton are the leading players in the Global Edge Data Center Market.