E-Commerce Packaging Market Research Report – Segmentation by Type (Corrugated Boxes, Protective Packaging Materials, Poly Mailers, Paperboard Packaging, Rigid Boxes, Padded Envelopes, Plastic Packaging Films, Packaging Inserts and Dividers, Tape and Labels, Other Specialty Packaging); By Distribution Channel (Manufacturers/Converters, Distributors, Retail/E-tail, Online Marketplaces, Third-Party Logistics Providers, Direct Sales); By Material (Paper and Paperboard, Plastic Materials, Biodegradable Plastics, Molded Fiber, Foam Materials, Metal, Glass, Textile-Based Materials, Composite Materials, Wood and Bamboo); By End-Use Application (Fashion and Apparel, Electronics and Technology, Health and Beauty, Food and Beverage, Home Goods and Furnishings, Books and Media, Toys and Baby Products, Pet Supplies, Subscription Boxes, Industrial and Automotive Parts); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16559

Format:

Region: Global

Market Size and Overview:

The E-Commerce Packaging Market was valued at USD 77.4 Billion in 2024 and is projected to reach a market size of USD 124.65 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 10%.

The E-Commerce Packaging Market continues to experience remarkable growth in 2024, propelled by the sustained momentum of online shopping behaviors that became deeply entrenched during the pandemic years and have since evolved into permanent consumer preferences. This dynamic market encompasses a diverse range of packaging solutions specifically engineered to withstand the rigors of direct-to-consumer delivery channels, including corrugated boxes, protective cushioning materials, poly mailers, and increasingly innovative sustainable alternatives. As digital commerce penetrates previously untapped demographics and geographical regions, packaging manufacturers are racing to develop solutions that balance protection, presentation, and environmental responsibility—the three critical pillars that now define success in this sector.

Key Market Insights:

Currently, corrugated packaging dominates with a commanding 43% share of the overall market value, while plastic protective packaging materials account for approximately 28% of total market revenue.

Notably, 67% of online shoppers report making purchasing decisions influenced by packaging sustainability claims, up from 52% just two years ago.

Approximately 38% of e-commerce packaging now incorporates some form of recycled content, with leading brands achieving averages of 72% recycled material content.

Returns-related packaging waste has emerged as a significant concern, with an estimated 5.6 billion packaging units used solely for product returns in 2024.

Packaging customization services have experienced explosive growth, with 84% of medium to large e-commerce operations now offering some form of branded packaging experience.

The average cost of packaging now represents 8.7% of total product delivery costs, a slight decrease from previous years due to design optimization and material efficiencies.

Market Drivers:

Explosive Growth in Direct-to-Consumer Brands

The remarkable proliferation of direct-to-consumer (D2C) brands has fundamentally transformed the e-commerce packaging landscape in 2024. These digitally-native brands, unencumbered by traditional retail paradigms, approach packaging as a critical brand touchpoint rather than mere functional necessity. Their emphasis on creating memorable unboxing experiences has elevated consumer expectations across the entire e-commerce ecosystem, driving demand for premium, customized packaging solutions even among established retailers. D2C brands typically allocate 2-3 times more budget toward packaging innovation compared to traditional retailers, recognizing its intrinsic connection to customer satisfaction and retention metrics. This shift has catalyzed a broader transformation whereby packaging has evolved from cost center to strategic investment, with brands leveraging distinctive packaging to establish competitive differentiation in crowded digital marketplaces. The spillover effect extends beyond purely aesthetic considerations, with D2C brands also pioneering sustainable packaging approaches that larger market participants subsequently adopt at scale, accelerating industry-wide innovation cycles.

Sustainability Mandates and Consumer Awareness

Environmental sustainability has transcended its previous positioning as a value-added feature to become an essential requirement driving packaging decision-making across the e-commerce landscape. This transformation stems from converging pressures: heightened consumer awareness regarding packaging waste, increasingly stringent regulatory frameworks in key markets, and corporate sustainability commitments that now encompass scope 3 emissions including packaging materials. Particularly influential are the 78% of consumers who report willingness to pay premiums for products utilizing environmentally responsible packaging solutions, creating direct economic incentives for sustainable innovation. Major e-commerce platforms have responded by implementing packaging sustainability metrics that influence product visibility and search rankings, effectively making sustainable packaging a prerequisite for marketplace success. The movement toward circular economy principles has similarly gained momentum, with packaging increasingly designed for multiple use cycles or straightforward recyclability from inception. These combined factors have catalysed unprecedented investment in alternative materials research, with bioplastics derived from agricultural waste streams, mycelium-based cushioning materials, and advanced paper-based protective solutions experiencing particular growth.

Market Restraints and Challenges:

The e-commerce packaging market faces significant challenges including volatile raw material costs that have increased by an average of 23% over the past eighteen months, creating margin pressures throughout the value chain. Fragmented recycling infrastructure continues to undermine circular economy aspirations, with only 47% of e-commerce packaging materials effectively recaptured through existing systems. Consumer expectations for both premium unboxing experiences and minimal environmental impact create contradictory design requirements that increase development complexity. Additionally, counterfeit protection features add cost layers while supply chain disruptions persist, hampering consistent material availability and complicating long-term planning efforts.

Market Opportunities:

Significant opportunities exist in compostable packaging solutions that decompose in home environments without industrial processing requirements, addressing consumer frustration with limited recycling infrastructure. Packaging designed specifically for recommerce (refurbished products) represents an emerging frontier with 32% annual growth as circular business models gain momentum. AI-driven right-sizing technology that creates custom packaging for each order is reducing material usage by up to 40% while improving protection. Reusable packaging systems with incentivized return mechanisms show promise in high-frequency purchase categories, potentially eliminating single-use packaging entirely for loyal customer segments. The integration of augmented reality experiences into packaging creates new marketing opportunities that extend customer engagement beyond delivery.

Market Segmentation:

Segmentation by Type:

• Corrugated Boxes

• Protective Packaging Materials

• Poly Mailers

• Paperboard Packaging

• Rigid Boxes

• Padded Envelopes

• Plastic Packaging Films

• Packaging Inserts and Dividers

• Tape and Labels

• Other Specialty Packaging

Corrugated boxes maintain dominance with 43% market share due to their unmatched versatility across product categories and dimensional customization capabilities. Their established recycling streams and consumer familiarity provide competitive advantages despite emerging alternatives. Recent innovations focus on reduced material usage through engineering advancements that maintain structural integrity while decreasing weight. Major retailers have implemented automated box-sizing systems that reduce excess space by 29%, optimizing both material consumption and shipping costs while maintaining protection performance.

Protective packaging materials represent the fastest-growing segment, expanding at 24.3% annually as fragile and high-value product categories increasingly transition to direct-to-consumer models. Innovation flourishes in this category, with biodegradable alternatives to traditional bubble wrap and polystyrene witnessing particularly strong adoption. Paper-based honeycomb structures, cornstarch-derived packing peanuts, and mushroom-based protective moldings exemplify the segment's sustainability evolution. The category benefits from dual optimization priorities: maximizing protection while minimizing environmental impact, driving continuous material science advancements and design innovation.

Segmentation by Distribution Channel:

• Manufacturers/Converters

• Distributors

• Retail/E-tail

• Online Marketplaces

• Third-Party Logistics Providers

• Direct Sales

Manufacturers/converters maintain market channel dominance with 47% share, leveraging their ability to provide customized solutions at scale while integrating directly into clients' supply chains. Their competitive advantage stems from vertical integration capabilities that encompass material production through conversion, enabling cost efficiencies unavailable to intermediaries. This channel has invested heavily in digital design interfaces that allow clients to visualize packaging solutions before production, reducing development cycles by an average of 38%. Long-term contracts with volume commitments characterize this channel, with manufacturers increasingly offering sustainability consulting services as value-added differentiators.

Online marketplaces for packaging materials represent the fastest-growing distribution channel at 28.7% annual growth, democratizing access to premium and sustainable options previously available only to large-volume purchasers. These platforms have disrupted traditional distribution by providing small and medium e-commerce operators with unprecedented variety and competitive pricing through aggregated purchasing power. The channel's success derives from sophisticated recommendation engines that match packaging solutions to specific product requirements based on dimensional data and fragility ratings. Transparent sustainability metrics and user reviews have created accountability mechanisms that accelerate innovation adoption.

Segmentation by End-Use Application:

• Fashion and Apparel

• Electronics and Technology

• Health and Beauty

• Food and Beverage

• Home Goods and Furnishings

• Books and Media

• Toys and Baby Products

• Pet Supplies

• Subscription Boxes

• Industrial and Automotive Parts

Electronics and technology products command 29% of the e-commerce packaging market value due to their combination of high average selling prices and specific protection requirements. The category demands sophisticated packaging solutions incorporating anti-static properties, precise dimensional tolerances, and superior impact resistance. Packaging for this segment increasingly incorporates suspended design techniques that create protective buffer zones using minimal materials. Consumer expectations for premium unboxing experiences are particularly pronounced in this category, with 73% of high-value electronics purchases incorporating distinctive visual design elements and staged reveal sequences.

Food and beverage represents the fastest-growing application segment at 31.2% annual growth, driven by rapid consumer adoption of direct-to-consumer specialty food products and meal kit subscription services. This category presents unique challenges requiring solutions that address temperature control, moisture regulation, and shelf-life extension while maintaining food safety compliance. Innovative insulation materials derived from recycled textile waste and biodegradable temperature-control elements exemplify the category's focus on responsible performance. The segment has pioneered sophisticated multi-compartment designs that enable mixed-temperature products to travel in single shipments, reducing delivery emissions.

Segmentation by Material:

• Paper and Paperboard

• Plastic Materials

• Biodegradable Plastics

• Molded Fiber

• Foam Materials

• Metal

• Glass

• Textile-Based Materials

• Composite Materials

• Wood and Bamboo

Paper and paperboard materials maintain decisive market leadership with 58% share, benefiting from their established recyclability credentials and consumer perception as environmentally responsible choices. The material category has evolved beyond basic brown boxes to encompass sophisticated engineered structures with performance characteristics rivaling synthetic alternatives. Advanced coating technologies have expanded paper-based applications into moisture-sensitive categories previously requiring plastic protection. Brand preference for paper stems from both sustainability advantages and superior printability, enabling high-impact graphics that enhance brand recognition.

Biodegradable plastics represent the fastest-growing material category with 36.8% annual expansion, addressing market demand for flexible packaging with reduced environmental impact. These materials offer performance characteristics comparable to conventional plastics while decomposing under specific conditions, addressing end-of-life concerns. Innovation centers on developing variants that decompose in home composting environments rather than requiring industrial facilities. The category includes both plant-derived bioplastics and enhanced conventional polymers with accelerated degradation properties, providing options across price points and performance requirements.

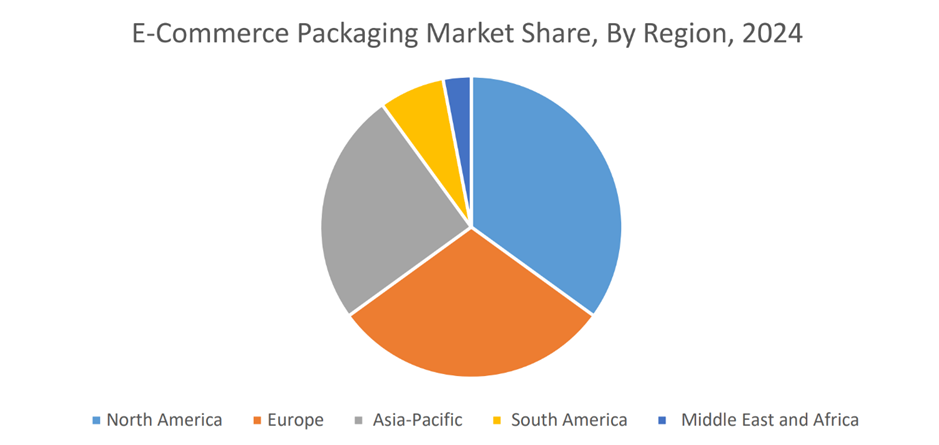

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

North America's market leadership stems from its sophisticated e-commerce ecosystem and consumer willingness to pay premiums for enhanced packaging experiences. The region leads in sustainable packaging innovation, with 72% of new packaging patents originating from North American companies. Its dominant position is reinforced by concentration of global e-commerce platforms headquartered in the region, which standardize packaging requirements across their marketplaces worldwide. North America demonstrates the highest rate of smart packaging adoption, with interactive elements incorporated into 34% of premium product deliveries compared to global averages of 21%.

Asia-Pacific's exceptional growth trajectory is driven by rapid e-commerce adoption across previously untapped consumer segments, particularly in second and third-tier cities throughout China, India, and Southeast Asia. The region benefits from substantial manufacturing capacity that enables rapid scaling of packaging production to meet explosive demand. Local innovation focuses on cost-efficient sustainable solutions appropriate for emerging market price sensitivities. Unique regional dynamics include significantly higher mobile commerce penetration, influencing packaging designs optimized for smaller average order sizes but higher purchase frequency compared to Western markets.

COVID-19 Impact Analysis:

The pandemic fundamentally transformed the e-commerce packaging market beyond temporary disruptions, permanently accelerating digital shopping adoption across previously resistant demographics and product categories. This structural shift expanded market requirements beyond traditional parcels to include specialized food delivery, pharmaceutical packaging, and contactless delivery solutions. Supply chain vulnerabilities exposed during the crisis prompted strategic regionalization of packaging production capacities, reducing dependency on concentrated manufacturing hubs. Additionally, heightened consumer awareness regarding package handling safety has sustained demand for antimicrobial surface treatments and tamper-evident features well beyond the acute pandemic period, representing enduring market changes.

Latest Trends and Developments:

Augmented reality packaging that links physical products with digital experiences represents a rapidly emerging trend, with brands incorporating AR markers that unlock exclusive content, product authentication, and usage tutorials. Packaging designed explicitly for reverse logistics has gained prominence as return volumes increase, with reusable packaging systems incorporating pre-paid return labeling and structural designs that facilitate multiple transit cycles. Voice-activated unboxing experiences for vision-impaired consumers exemplify inclusive design principles gaining traction among leading brands. Temperature-monitoring indicators integrated directly into packaging provide quality assurance for sensitive products while generating valuable supply chain data. The convergence of automation, robotics, and packaging design is accelerating, with packages increasingly engineered specifically for compatibility with automated fulfillment systems.

Key Players in the Market:

• DS Smith

• Smurfit Kappa

• International Paper

• Amcor

• Mondi Group

Chapter 1. Global E-Commerce Packaging Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global E-Commerce Packaging Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global E-Commerce Packaging Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global E-Commerce Packaging Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global E-Commerce Packaging Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global E-Commerce Packaging Market – By Type

6.1. Introduction/Key Findings

6.2. Corrugated Boxes

6.3. Protective Packaging Materials

6.4. Poly Mailers

6.5. Paperboard Packaging

6.6. Rigid Boxes

6.7. Padded Envelopes

6.8. Plastic Packaging Films

6.9. Packaging Inserts and Dividers

6.10. Tape and Labels

6.11. Other Specialty Packaging

6.12. Y-O-Y Growth trend Analysis By Type

6.13. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global E-Commerce Packaging Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Manufacturers/Converters

7.3. Distributors

7.4. Retail/E-tail

7.5. Online Marketplaces

7.6. Third-Party Logistics Providers

7.7. Direct Sales

7.8. Y-O-Y Growth trend Analysis By Distribution Channel

7.9. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global E-Commerce Packaging Market – By Material

8.1. Introduction/Key Findings

8.2. Paper and Paperboard

8.3. Plastic Materials

8.4. Biodegradable Plastics

8.5. Molded Fiber

8.6. Foam Materials

8.7. Metal

8.8. Glass

8.9. Textile-Based Materials

8.10. Composite Materials

8.11. Wood and Bamboo

8.12. Y-O-Y Growth trend Analysis By Material

8.13. Absolute $ Opportunity Analysis By Material, 2024-2030

Chapter 9. Global E-Commerce Packaging Market – By End-Use Application

9.1. Introduction/Key Findings

9.2. Fashion and Apparel

9.3. Electronics and Technology

9.4. Health and Beauty

9.5. Food and Beverage

9.6. Home Goods and Furnishings

9.7. Books and Media

9.8. Toys and Baby Products

9.9. Pet Supplies

9.10. Subscription Boxes

9.11. Industrial and Automotive Parts

9.12. Y-O-Y Growth trend Analysis By End-Use Application

9.13. Absolute $ Opportunity Analysis By End-Use Application, 2024-2030

Chapter 10. Global E-Commerce Packaging Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Distribution Channel

10.1.4. By Material

10.1.5. By End-Use Application

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Distribution Channel

10.2.4. By Material

10.2.5. By End-Use Application

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Type

10.3.3. By Distribution Channel

10.3.4. By Material

10.3.5. By End-Use Application

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Distribution Channel

10.4.4. By Material

10.4.5. By End-Use Application

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Distribution Channel

10.5.4. By Material

10.5.5. By End-Use Application

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global E-Commerce Packaging Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. DS Smith

11.2. Smurfit Kappa

11.3. International Paper

11.4. Amcor

11.5. Mondi Group

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The remarkable proliferation of D2C brands has transformed the packaging landscape, as they approach packaging as a critical brand touchpoint rather than merely functional. These brands typically allocate 2-3 times more budget toward packaging innovation than traditional retailers.

Price fluctuations have increased by an average of 23% over the past eighteen months, creating margin pressures throughout the value chain.

Key players include International Paper Company, DS Smith Plc, Mondi Group.

North America currently holds the largest market share, estimated around 35%.

Asia-Pacific has shown significant room for growth in specific segments.