Global Distributed Cloud Market Research Report – Segmentation by Application (Edge Computing, Content-Delivery, IoT, Others); By Service (Data Security, Data Storage, Networking, Others); By Enterprise (Large Enterprise, SMEs); By End-Use (BFSI, IT & Telecom, Retail & Commerce, Healthcare, Government & Defense, Manufacturing, Energy & Utilities, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9967

Format:

Region: Global

Market Size and Overview:

The Global Distributed Cloud Market was valued at USD 4.07 billion in 2024 and is projected to reach a market size of USD 16.19 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 31.8%.

The distributed cloud market refers to a computing model where cloud services are deployed across multiple geographically dispersed locations while remaining centrally managed by a public cloud provider. This approach brings cloud resources closer to end users and devices, enabling lower latency, improved compliance with local regulations, and enhanced performance for edge computing and hybrid cloud environments. Influenced by the rapid growth of IoT, 5G, and real-time analytics, the distributed cloud market is gaining traction across industries such as healthcare, manufacturing, retail, and finance. As organizations seek more agile, scalable, and secure infrastructure, distributed cloud solutions are becoming essential for digital transformation.

Key Market Insights:

The adoption of distributed cloud solutions is accelerating as organizations prioritize latency reduction and regulatory compliance. According to Gartner, by 2025, over 50% of enterprise-generated data will be created and processed outside traditional centralized data centers or cloud environments. This shift is pushing companies to deploy cloud services closer to data sources, enhancing speed and responsiveness in areas such as manufacturing automation, smart cities, and autonomous systems.

Enterprises are increasingly leveraging distributed cloud models to optimize performance and cost-efficiency. A report by IDC indicates that 75% of large enterprises will adopt hybrid or multi-cloud infrastructures by 2026, many of which will include distributed cloud components. This trend is fueled by the demand for localized data processing and real-time analytics, especially in sectors such as healthcare and finance where data sensitivity and latency are critical.

Edge computing plays a significant role in driving distributed cloud demand. The number of connected devices is projected to reach 29.3 billion by 2030, creating a vast network of endpoints generating continuous streams of data. Distributed cloud enables these devices to process information closer to the source, reducing bandwidth use and improving decision-making speed, which is crucial for IoT applications and immersive technologies like AR and VR.

Distributed Cloud Market Drivers:

Rising Demand for Low Latency and Real-Time Data Processing

One of the primary drivers of the distributed cloud market is the growing demand for low latency and real-time data processing. As industries like autonomous vehicles, smart manufacturing, and financial services require instant data-driven decisions, centralized cloud models often fall short in delivering the required speed and responsiveness. Distributed cloud architecture brings computation and storage closer to the data source, significantly reducing latency and enabling real-time insights. This capability is critical for applications such as predictive maintenance, video surveillance, and edge AI, where even milliseconds of delay can lead to inefficiencies or failures.

Growing Need for Regulatory Compliance and Data Sovereignty

With stricter data protection regulations such as GDPR in Europe and similar laws in other regions, organizations are under increasing pressure to store and process data within national or regional boundaries. Distributed cloud allows companies to deploy cloud services in specific geographic locations, helping them comply with local data residency and privacy laws without compromising on performance or scalability. This flexibility is particularly important for global enterprises operating across multiple jurisdictions, as it ensures they meet legal requirements while maintaining a unified cloud management experience.

Expansion of Internet of Things (IoT) and Edge Devices

The rapid growth of IoT devices is another major driver for the distributed cloud market. As billions of sensors, cameras, and smart devices generate continuous streams of data, the traditional cloud model becomes inefficient for handling the volume and speed of information. Distributed cloud enables edge computing capabilities by allowing data to be processed closer to the devices, reducing bandwidth consumption and improving response time. This architecture supports a wide range of use cases such as smart cities, connected healthcare, and industrial automation, where immediate data analysis is essential for operational efficiency.

Increased Adoption of Hybrid and Multi-Cloud Strategies

Businesses are increasingly moving towards hybrid and multi-cloud environments to avoid vendor lock-in and to improve resiliency. Distributed cloud supports these strategies by offering a consistent infrastructure and service delivery model across on-premises, public, and edge locations. This flexibility allows organizations to run workloads wherever it makes the most sense—whether because of cost, performance, or compliance considerations—while maintaining centralized control. As more enterprises seek agile, scalable solutions that support digital transformation, distributed cloud becomes a vital component in achieving these goals.

Distributed Cloud Market Restraints and Challenges:

Security Complexities and Integration Challenges Restrain Widespread Adoption

Despite its advantages, the distributed cloud market faces significant restraints and challenges that can hinder its growth. One of the primary concerns is the increased complexity of securing data and applications spread across multiple locations. With more endpoints and edge nodes, the risk of cyberattacks, data breaches, and unauthorized access rises, requiring advanced and often costly security solutions. Additionally, integrating distributed cloud infrastructure with existing legacy systems and ensuring seamless interoperability across diverse platforms can be technically demanding. Organizations may also face difficulties in managing distributed resources, maintaining consistent performance, and ensuring compliance across all regions, especially when skilled IT professionals are limited.

Distributed Cloud Market Opportunities:

The distributed cloud market presents vast opportunities as emerging technologies and evolving business demands continue to reshape IT infrastructure. Advancements in 5G, AI, and machine learning are enabling new applications that thrive on distributed computing, such as autonomous systems, immersive experiences, and advanced analytics at the edge. Industries like healthcare, retail, logistics, and telecommunications are increasingly adopting distributed cloud to enhance operational efficiency, deliver personalized services, and support real-time decision-making. Additionally, as small and medium-sized enterprises (SMEs) pursue digital transformation, scalable and location-flexible distributed cloud solutions offer them a cost-effective path to innovation and global reach.

Distributed Cloud Market Segmentation:

Market Segmentation: By Application:

• Edge Computing

• Content Delivery

• Internet of Things (IoT)

• Others

Edge computing is the dominant application segment within the distributed cloud market because of its critical role in processing data closer to the source for faster response times and reduced latency. Many industries, including manufacturing, automotive, and healthcare, rely heavily on edge computing to support real-time analytics, automation, and AI-driven processes. Its ability to handle massive amounts of data locally while maintaining connectivity with the central cloud infrastructure makes it indispensable for applications requiring immediate insights and low latency, driving widespread adoption.

The fastest-growing application segment in the distributed cloud market is the Internet of Things (IoT). With billions of connected devices generating continuous streams of data, IoT demands localized processing to manage bandwidth efficiently and enable rapid decision-making. Distributed cloud solutions support IoT deployments by offering scalable, secure, and flexible infrastructure at the edge, making it easier for businesses to implement smart environments such as connected homes, smart cities, and industrial IoT networks. The exponential growth of IoT devices and their increasing complexity drive the rapid expansion of this segment.

Market Segmentation: By Service:

• Data Security

• Data Storage

• Networking

• Other

Data security is the dominant service segment in the distributed cloud market, driven by the increasing demand to protect sensitive information across multiple, geographically dispersed locations. As data flows between edge nodes and central cloud environments, robust security measures like encryption, identity management, and threat detection become critical to prevent breaches and ensure compliance with regulations. Organizations prioritize security services to build trust and safeguard their distributed infrastructure from evolving cyber threats.

Networking services are experiencing the fastest growth in the distributed cloud market due to the growing demand for seamless connectivity between distributed nodes, edge devices, and central cloud systems. Advanced networking solutions, including software-defined networking (SDN) and network function virtualization (NFV), enable efficient traffic management, reduced latency, and enhanced bandwidth optimization. This growth is propelled by the expansion of 5G networks and the increasing number of connected devices requiring reliable, high-speed communication.

Market Segmentation: By Enterprise:

• Large Enterprise

• Small and Medium Enterprise (SMEs)

Large enterprises dominate the distributed cloud market because of their extensive IT infrastructure needs, global operations, and greater resources to invest in advanced cloud solutions. These organizations benefit from distributed cloud by improving performance across multiple locations, ensuring compliance with various regional regulations, and enabling real-time data processing at the edge. Their complex workflows and high demand for scalability drive widespread adoption and continuous innovation within this segment.

Small and medium enterprises (SMEs) represent the fastest-growing segment in the distributed cloud market as they increasingly adopt cloud technologies to enhance agility, reduce costs, and compete more effectively. Distributed cloud offers SMEs flexible, scalable infrastructure without the heavy upfront investment typical of traditional data centers. With rising digital transformation initiatives, SMEs are leveraging distributed cloud services to support remote work, IoT applications, and localized data processing, fueling rapid growth in this sector.

Market Segmentation: By End-Use:

• BFSI

• IT & Telecom

• Retail & Commerce

• Healthcare

• Government & Defense

• Manufacturing

• Energy & Utilities

• Others

The BFSI (Banking, Financial Services, and Insurance) sector is a dominant end-use segment in the distributed cloud market, driven by its critical need for secure, low-latency data processing and compliance with stringent regulatory requirements. Distributed cloud enables BFSI organizations to enhance fraud detection, risk management, and customer experience by processing sensitive transactions closer to the source while maintaining robust security measures. Its adoption helps financial institutions accelerate innovation while safeguarding data integrity.

The IT & Telecom sector is the fastest-growing end-use segment due to the rapid expansion of 5G networks and increasing demand for edge computing capabilities. Telecom companies leverage distributed cloud to improve network performance, manage vast amounts of data generated by connected devices, and deliver new services like immersive media and smart city applications. The sector’s continuous investment in infrastructure modernization fuels rapid adoption of distributed cloud technologies.

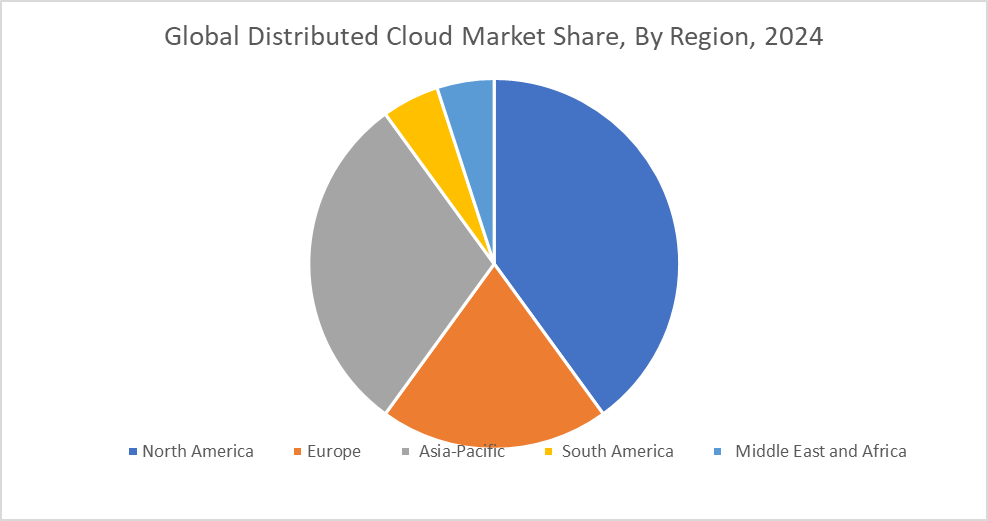

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is the dominant region in the distributed cloud market, accounting for the largest share due to its advanced technological infrastructure, early adoption of cloud innovations, and the presence of major cloud service providers. The region’s strong focus on digital transformation across industries such as BFSI, healthcare, and government drives substantial investment in distributed cloud solutions. Additionally, stringent data privacy regulations and the growing demand for edge computing to support applications like autonomous vehicles and smart cities further reinforce North America’s leadership.

Asia-Pacific is the fastest-growing region in the distributed cloud market, fueled by rapid digitization, increasing adoption of IoT and 5G technologies, and expanding enterprise cloud initiatives across emerging economies. Countries like China, India, Japan, and South Korea are investing heavily in upgrading their digital infrastructure and deploying distributed cloud services to support manufacturing automation, smart city projects, and e-commerce expansion. The region’s large population and growing middle class are driving demand for real-time data processing and localized cloud services.

COVID-19 Impact Analysis on the Global Distributed Cloud Market:

The COVID-19 pandemic accelerated the adoption of distributed cloud technologies as businesses rapidly shifted to remote work and digital operations. The sudden growth in data traffic and the need for seamless connectivity across dispersed locations highlighted the limitations of traditional centralized cloud models. Distributed cloud enabled organizations to process data closer to users, ensuring better performance, security, and reliability during a time of unprecedented demand. Additionally, industries such as healthcare and retail leveraged distributed cloud to support telemedicine and e-commerce growth, further driving market expansion despite pandemic-related challenges.

Latest Trends/ Developments:

One of the latest trends in the distributed cloud market is the integration of artificial intelligence (AI) and machine learning (ML) at the edge. By embedding AI/ML capabilities directly within distributed cloud infrastructure, organizations can perform real-time analytics and make faster, smarter decisions without relying on centralized data centers. Additionally, the rollout of 5G networks is enhancing distributed cloud performance by providing faster, more reliable connectivity, enabling seamless communication between edge devices and central cloud platforms.

Another significant development is the increasing focus on enhanced security frameworks tailored specifically for distributed cloud environments. As workloads become more decentralized, providers are investing in zero-trust architectures, advanced encryption methods, and automated threat detection systems to safeguard data across multiple edge locations. Furthermore, cloud vendors are offering more flexible hybrid and multi-cloud management tools, enabling businesses to orchestrate workloads seamlessly across on-premises, public, and edge clouds. This improved interoperability and security are helping organizations accelerate their digital transformation while managing risks effectively.

Key Players:

• Google (US)

• IBM (US)

• Microsoft (US)

• AWS (US)

• VMware (US)

• Alibaba Cloud (China)

• Teradata (US), F5 (US)

• Cohesity (US)

• Oracle (US) Commvault (US)

• SCC (UK) Wind River Systems (US)

Chapter 1. Global Distributed Cloud Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Distributed Cloud Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Distributed Cloud Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Distributed Cloud Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Distributed Cloud Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Distributed Cloud Market – By Application

6.1. Edge Computing

6.2. Content Delivery

6.3. Internet of Things (IoT)

6.4. Y-O-Y Growth trend Analysis By Application

6.5. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 7. Global Distributed Cloud Market – By Service

7.1. Data Security

7.2. Data Storage

7.3. Networking

7.4. Others

7.5. Y-O-Y Growth trend Analysis By Service

7.6. Absolute $ Opportunity Analysis By Service, 2025-2030

Chapter 8. Global Distributed Cloud Market – By Enterprise

8.1. Large Enterprise

8.2. Small and Medium Enterprise (SMEs)

8.3. Y-O-Y Growth trend Analysis By Enterprise

8.4. Absolute $ Opportunity Analysis By Enterprise, 2025-2030

Chapter 9. Global Distributed Cloud Market – By End-Use

9.1. BFSI

9.2. IT & Telecom

9.3. Retail & Commerce

9.4. Healthcare

9.5. Government & Defense

9.6. Manufacturing

9.7. Energy & Utilities

9.7. Others

9.8. Y-O-Y Growth trend Analysis By End-Use

9.9. Absolute $ Opportunity Analysis By End-Use, 2025-2030

Chapter 10. Global Distributed Cloud Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Application

10.1.3. By Service

10.1.4. By Enterprise

10.1.5. By End-use

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Application

10.2.3. By Service

10.2.4. By Enterprise

10.2.5. By End-use

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Application

10.3.3. By Service

10.3.4. By Enterprise

10.3.5. By End-use

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Application

10.4.3. By Service

10.4.4. By Enterprise

10.4.5. By End-use

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Application

10.5.3. By Service

10.5.4. By Enterprise

10.5.5. By End-use

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Distributed Cloud Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1 Google (US)

11.2 IBM (US)

11.3 Microsoft (US)

11.4 AWS (US)

11.5 VMware (US)

11.6 Alibaba Cloud (China)

11.7 Teradata (US), F5 (US)

11.8 Cohesity (US)

11.9 Oracle (US) Commvault (US)

11.10 SCC (UK) Wind River Systems (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Distributed Cloud Market was valued at USD 4.07 billion in 2024 and is projected to reach a market size of USD 16.19 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 31.8%.

The global distributed cloud market is driven by the growing demand for low latency and real-time data processing, stricter regulatory compliance, rapid expansion of IoT devices, and increasing adoption of hybrid and multi-cloud strategies.

Based on Service, the Global Distributed Cloud Market is segmented into Data Security, Data Storage, Networking, Others.

North America is the most dominant region for the Global Distributed Cloud Market.

Google (US), IBM (US), Microsoft (US), AWS (US) are the leading players in the Global Distributed Cloud Market.