Global Data Center Virtualization Market Research Report – Segmentation By Component (Hardware, Software, Services); By Type (Server Virtualization, Storage Virtualization, Network Virtualization, Desktop Virtualization, Application Virtualization); By End User (IT & Telecom, BFSI, Heathcare, Retails, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9904

Format:

Region: Global

Market Size and Overview:

The Data Center Virtualization Market was valued at USD 7.69 billion in 2024 and is projected to reach a market size of USD 21.09 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.36%.

The Data Center Virtualization Market is reshaping conventional IT infrastructures so organizations can optimize hardware resources, minimize operational costs, and increase scalability through software-defined technologies. Virtualization allows several virtual machines (VMs) to run on a single physical server by decoupling the underlying physical hardware from the services it supports, raising resource utilization and energy effectiveness. This way, faster deployment, better disaster recovery, and easier maintenance become possible; hence, it has become an indispensable part of any modern enterprise IT environment. As enterprises start their passage through the cloud, DevOps, and digital-first strategy focus, data center virtualization has become an enabler of agility, automation, and infrastructure flexibility. Organizations around the globe, from small enterprises to hyperscale providers, are leveraging virtualization technologies to future-proof their data centers against a fast-changing digital landscape that demands dynamic and on-demand workloads.

Key Market Insights:

Over 75% of global enterprises have implemented data center virtualization to improve scalability and reduce infrastructure complexity. This adoption is accelerating as businesses prioritize hybrid and multi-cloud environments.

Virtualized environments enable server provisioning up to 90% faster than traditional setups. This agility supports DevOps, continuous integration, and faster time-to-market for digital services.

Data Center Virtualization Market Drivers:

One of the primary drivers of the data center virtualization market is the increasing need for cost-effective and scalable infrastructure.

One of the key trends that motivates the market for data center virtualization is the need to reduce costs and to have facilities that can grow as needed. An underutilization of hardware in traditional data centers leads to increased operational costs and inefficient use of resources. Hardware requirements and energy consumption would thus be reduced considerably as virtualization allows more than a single physical server to host multiple virtual machines (VMs). This allows organizations to reduce capital expenditures (CapEx) on servers and operational expenditures (OpEx) on power, cooling, and maintenance activities. Scaling of workload would thus be possible with the incoming resource provision, tailoring to the business growth, in addition to adequate virtualized environments. This way, scaling is effortless and does not require major hardware updates. Elasticity is, thus, a vital asset for organizations interested in hybrid cloud adoption or transformation into digital readiness. Moreover, virtualization enhances ease in managing IT through consolidated control, centralized monitoring, and automation. The effect of such technology is improved resource utilization, speedy application deployment, and reduction of total cost of ownership (TCO), which pushes organizations in different sectors to scale up the virtualization in place.

The global shift toward cloud computing and hybrid IT architectures is another key driver fueling data center virtualization.

Another significant factor leading virtualization of data centers is the global push for cloud-based and hybrid forms of IT architecture. Digital transformation by organizations requires infrastructure that can easily respond to periodic demands, facilitate remote operations, and integrate with international public clouds or private clouds. Virtualization presents the opportunity for the seamless transfer of workloads between on-premise data centers and cloud environments, ensuring agility and business continuity. The primary use of hybrid clouds, which combine private infrastructure with external public cloud resources, is in virtual environments to achieve easy management of resources. Organizations also exploit virtualization technology to build up software-defined data centers (SDDCs) capable of automation, workload orchestration, and policy-based governance across both IT assets. Also, as remote work and distributed applications become mainstream, virtual machines and containers would facilitate flexible deployment along with centralized control. Thus, virtualization creates the required agile, cloud-ready architecture that modern enterprises need.

Data Center Virtualization Market Restraints and Challenges:

Despite its many advantages, data center virtualization introduces significant management complexity and potential security vulnerabilities, especially in large-scale environments.

Data center virtualization has many advantages, but it also brings a high level of complexity in management and potential security holes, especially in large environments. With multiple VMs, containers, and applications housed on a single physical server, it can be even more difficult to monitor and manage performance, configurations, and security policies. Furthermore, an improper isolation between VMs and/or poorly configured hypervisors becomes an entry point to cyberattacks. This endangers both the risks of data breaches and unauthorized access. To this problem, organizations tend to have insufficient visibility into their virtualized workloads, especially in hybrid or multi-cloud environments, which affects resource tracking, compliance enforcement, and troubleshooting. Some legacy systems are not compatible with existing virtualization platforms, and integrating and migrating them can be quite laborious. Adding to this are insufficient training for personnel and expert knowledge, hindering further efficient implementation. Virtualized environments lack strong governance, automation, and real-time monitoring tools and, therefore, manifest into a complex, inefficient, and vulnerable environment, which limits the maximum realization of the benefits of virtualization.

Data Center Virtualization Market Opportunities:

Enterprises increasingly pursuing digital transformation, hybrid clouds, and agile IT strategies are giving rise to vast opportunities for the Data Center Virtualization Market. One such area of most promise is the advent of software-defined data centers (SDDCs). These centers virtualize compute, storage, and networking resources to create an infrastructure that is fully automated and scalable. With the supporting provision of infrastructure-as-code (IaC), real-time provisioning, and advanced policy-driven management, the environments are excellent for DevOps workflows that modernize.

Another important opportunity is the coupling of AI and machine learning capabilities with virtualization platforms to optimize workload distribution, energy efficiency, and predictive maintenance. More so, edge computing has created demands for lightweight, virtualized infrastructure closer to the end users-above all to support latency-sensitive applications for retail, healthcare, and manufacturing. From reluctance due to the high upfront costs, small and mid-sized enterprises are now realizing the possibilities of virtualization thanks to cloud-based managed services. Regulatory compliance, disaster recovery, and operational continuity form priority areas for any organization; virtualization carries built-in solutions using automated backups, fault tolerance, and workload migration. Innovations such as containerization, microservices, and zero-trust security models have become increasingly popular, and the future of data centers is going to be more virtual, intelligent, and cloud-connected, creating tremendous growth opportunities across all industries.

Data Center Virtualization Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

• Services

By type, the market is segmented into Server, Storage, Network, Desktop, and Application Virtualization, each serving different IT optimization goals. Server virtualization is the most widely adopted type, whereby multiple virtual servers run on one physical machine, increasing efficiency significantly and saving expenses on hardware. Storage virtualization allows multiple storage resources to be managed as one pool, thereby improving redundancy and utilization as well as simplifying backup and disaster recovery. Network virtualization abstracts networking functions from hardware, thereby enabling dynamic configuration and secure traffic segmentation across virtual machines and environments. Desktop virtualization caters for remote work and centralized desktop management, whereby users access their desktops from any device with enhanced security. Application virtualization isolates software applications from their underlying systems, thereby facilitating deployment and compatibility while guarding against system conflicts. These types of virtualization synergistically lead to the creation of agile, cost-effective, and scalable IT environments tailored to the requirements of enterprises.

Market Segmentation: By Type

• Server Virtualization

• Storage Virtualization

• Network Virtualization

• Desktop Virtualization

• Application Virtualization

The market has been segmented into different types by server, storage, network, desktop, and application virtualization for different types of IT optimization goals. Only server virtualization has been extensively adopted: running multiple virtual servers on a single physical machine, it has increased efficiency to the maximum and reduced hardware operating costs. The storage virtualization has enabled pooling multiple storage resources to manage as a whole and, hence, improved backup and disaster recovery management. Administering the network function among the equipment will lead to network virtualization, which allows dynamic configuration and secure traffic segmentation across machines and environments. Users can access their desktops using any device as it has better security via desktop virtualization, which also supports remote working and centralized desktop administration. Software applications are isolated from entire systems using application virtualization, making deployment and compatibility easier while preventing conflict with software on the operating systems. Collectively, such types of virtualization develop highly agile, cost-effective, and scalable IT environments for the enterprise's needs.

Market Segmentation: By End User

• IT & Telecom

• BFSI

• Healthcare

• Retail

In essence, the end-user segmentation covers IT & Telecom, BFSI, Healthcare, Retail, and Other applications-adopting virtualization to gain productivity advantages in their operational processes. For example, IT & Telecom companies are numerous because their infrastructure demands high performance and needs environments with multiple tenants and services with scale. BFSI banks use virtualization as a substitute for securing sensitive financial data, ensuring high availability, and instituting compliance with international regulations such as PCI-DSS and the GDPR. The Healthcare scene has patients assured of safe handling of electronic health records (EHRs), efficient management of diagnosis systems, and enhanced continuity in ongoing treatment. Virtualization helps retail businesses support point-of-sale systems, inventory control, and customer relationship management on centralized, secure servers, while the Others segment comprises education, manufacturing, and public sector entities that have improved online services with IT modernization and cost control from virtualization. Each industry has adopted data center virtualization to improve agility, increase reliability, and offer a better platform for digital service delivery.

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

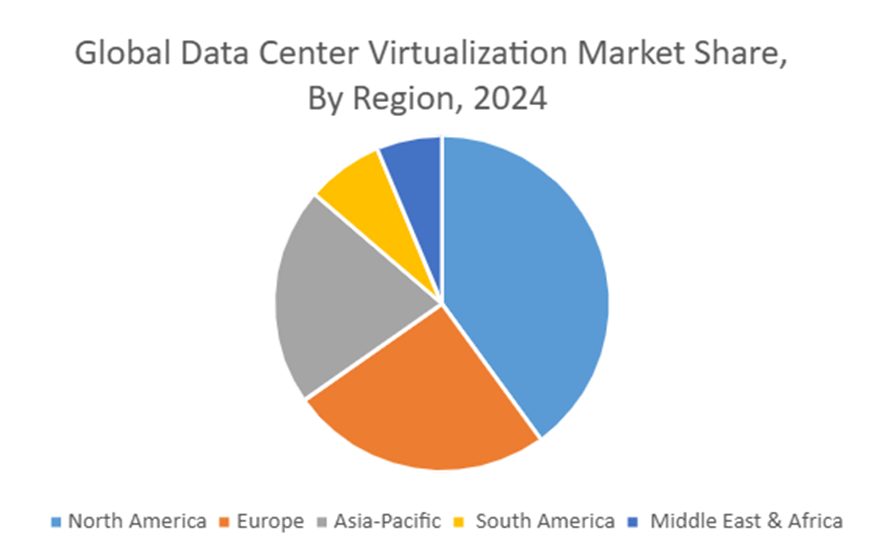

The Data Center Virtualization Market is led by the North American region, which boasts early adoption of advanced technologies, a highly established IT infrastructure, and the presence of international hardware players such as VMware, Cisco, and Microsoft. Organizations within the United States and Canada have become frontrunners in the adoption of virtualized environments to enable hybrid cloud strategies, automation needs, and remote activity. Europe comes right after because of the stringent data protection regulations, such as GDPR, in addition to the large-scale digital transformation initiatives across industries such as finance, manufacturing, and healthcare. Furthermore, environmentally sustainable infrastructure is an emerging trend within the region, where green data centers and energy-efficient virtualization solutions are gaining traction. Major drivers for investments in cloud computing, 5G, and virtualization in the Asia-Pacific region, mainly India, China, and Southeast Asia, are rapid urbanization and digitalization. Governments and enterprises are upgrading their data centers to support scalable and virtualized infrastructure to satisfy the growing demands of digital services. In South America, steady growth is being led by Brazil and Mexico, where the rising adoption of cloud platforms within fintech, e-commerce, and retail is generating demand for flexible and virtualized IT environments. On the other hand, the Middle East and Africa are turning into lucrative markets, supported by smart city developments and public sector digitization efforts in countries such as the UAE, Saudi Arabia, and South Africa. These regions acknowledge virtualization as a key enabler for agile, efficient, and secure digital ecosystems.

COVID-19 Impact Analysis on the Data Center Virtualization Market:

The Data Center Virtualization Market was spared neither the pangs of disruption nor the positive injection for growth by the COVID-19 pandemic. Demand for IT infrastructure that is flexible, scalable, and remotely operable skyrocketed, as organizations scrambled to get their workforce working remotely. Virtualization became one of the critical tools by which businesses seek to ensure continuity, provide secure remote access, and manage workloads effectively from a centralized location. Most companies with virtualized data centers adapted quite easily, while several other companies that had initially not used virtualization for their data center started fast-tracking their introduction in response to increasing digital demand and diminished dependence on physical hardware. Nevertheless, supply chain disruptions and temporary IT budget constraints led to project delays for some infrastructure initiatives during the early days of the pandemic. These notwithstanding, the long-term impact of the pandemic remains largely positive, with a steep upsurge in cloud adoption, hybrid IT models, and software-defined data centers. The pandemic has catalyzed the emerging trend of virtualization, ensuring business resilience, agility, and operational efficiency. Therefore, virtualization of the data center has redefined its construct from a cost-saving initiative to a strategic imperative for digital transformation in the present post-pandemic world.

Latest Trends/ Developments:

Data-center virtualization is changing with a few trends of transformation that are emerging. One such development is the establishment of software-defined data centers (SDDCs), which are fully virtualized with centralized management over compute, storage, and networking. This aspect fits the trend of infrastructure as code and allows dynamic provisioning with policy-driven automation, a perfect fit with a DevOps workflow. Another emerging trend is hyper-converged infrastructure (HCI), which bundles the virtualized compute and storage resources into a single appliance to ease management and scaling. Edge virtualization is gaining traction, as businesses deploy virtualized servers closer to end users for latency-sensitive applications, such as IoT and AI. Further containerization and microservice architectures—impelled by platforms such as Kubernetes—are inducing organizations to support virtual machines and containers side by side. Security is evolving too, with zero-trust virtualization assuring continuous validation and monitoring of access and interactions among VMs. AI-powered optimization is helping automate resource allocation, energy management, and predictive maintenance within virtualized environments. These changes together are reconstituting virtualized data centers into intelligent, flexible, and resilient infrastructure hubs.

Key Players:

1. ATTO Technology, Inc.

2. AT & T

3. Cisco Systems, Inc.

4. Dell Inc.

5. Fujitsu

6. HCL Technologies Limited

7. IBM

8. Oracle

9. Rahi

10. Hewlett Packard Enterprise Development LP

Chapter 1. Global Data Center Virtualization Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Data Center Virtualization Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Data Center Virtualization Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Data Center Virtualization Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Data Center Virtualization Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Data Center Virtualization Market – By Component

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Type

6.6. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 7. Global Data Center Virtualization Market – By Type

7.1. Introduction/Key Findings

7.2. Server Virtualization

7.3. Storage Virtualization

7.4. Network Virtualization

7.5. Desktop Virtualization

7.6. Application Virtualization

7.7. Y-O-Y Growth trend Analysis By Type

7.8. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 8. Global Data Center Virtualization Market – By End User

8.1. Introduction/Key Findings

8.2. IT & Telecom

8.3. BFSI

8.4. Healthcare

8.5. Retail

8.6. Y-O-Y Growth trend Analysis By End User

8.7. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 9. Global Data Center Virtualization Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Service Type

9.1.3. By Technology

9.1.4. By End User

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Component

9.2.3. By Type

9.2.4. By End User

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Component

9.3.3. By Type

9.3.4. By End User

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Component

9.4.3. By Type

9.4.4. By End User

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Component

9.5.3. By Type

9.5.4. By End User

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Data Center Virtualization Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. ATTO Technology, Inc.

10.2. AT & T

10.3. Cisco Systems, Inc.

10.4. Dell Inc.

10.5. Fujitsu

10.6. HCL Technologies Limited

10.7. IBM

10.8. Oracle

10.9. Rahi

10.10. Hewlett Packard Enterprise Development LP

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Data Center Virtualization Market was valued at USD 7.69 billion in 2024 and is projected to reach a market size of USD 21.09 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.36%.

The Data Center Virtualization Market is driven by the growing need for cost-efficient, scalable IT infrastructure and the rising adoption of hybrid cloud and digital transformation strategies. These solutions enhance agility, reduce hardware dependency, and support rapid application deployment.

The market is segmented by component into Hardware, Software, and Services, with each playing a vital role in enabling Data center virtualization solutions.

North America is the most dominant region for the Data Center Virtualization Market.

ATTO Technology, Inc., AT&T, Cisco Systems, Inc., Dell Inc., Fujitsu, HCL Technologies Limited, Hewlett Packard Enterprise Development LP, Huawei Technologies Co. are the key players in the Data Center Virtualization Market.