Global Data-Center Transformation Market Research Report – Segmentation By Deployment Model (On-premise, Cloud-Based, Colocation); By Tier Type (Tier 1 Data Centers, Tier 2 Data Centers, Tier 3 Data Centers, Tier 4 Data Centers); By End User (IT & Telecom, BFSI, Healthcare, Government & Public Sector); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9902

Format:

Region: Global

Market Size and Overview:

The Data-Center Transformation Market was valued at USD 8.8 billion in 2024 and is projected to reach a market size of USD 24.98 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.02%.

The ever-evolving Data-Center Transformation Market is fueled by the fact that organizations are modernizing legacy setups to respond to the demands of the digital-first world. The influences of cloud computing, edge technologies, automation, and sustainability concerns all push this market towards a strategic transformation as organizations plan to use their data environments to become more agile, scalable, and energy-efficient. Businesses in all sectors are looking toward transformation enhancements such as performance, cost savings, protection improvements, and new technologies such as AI and IoT of which have made data centers the mainstay of digital transformation strategies.

Key Market Insights:

Data center automation reduces operational costs by up to 30%. AI-driven monitoring, predictive maintenance, and infrastructure-as-code tools are increasing efficiency and reducing human error. Automation is now considered a critical pillar in modern IT strategy.

Edge data center deployments increased by 34% in the last year. As real-time data processing becomes crucial for applications like IoT and autonomous systems, edge computing is gaining traction. It enables faster response times and reduces latency significantly.

Data-Center Transformation Market Drivers:

The shift towards digital business models has placed enormous pressure on traditional IT systems, prompting a massive move toward agile and scalable data center infrastructures.

Financial transactions swell both in volume and complexity, bringing along threats of cyber fraud, identity theft, and financial crimes. Most advanced forms of fraud escape detection by traditional rule-based systems. AI and machine learning take that dynamic self-learning approach to real-time anomaly detection, keeping pace with emergent threats and flagging suspicious activity instantly. These models look into thousands of parameters simultaneously location and transaction pace, to devise fingerprints for a proactive security framework. For example, leading banks now employ AI for transaction surveillance with high accuracy, looking at billions of transactions a day. Besides, AI advances risk modeling in terms of deeper knowledge regarding credit, operational, and market risks. There is thus better compliance with regulatory standards like Basel III and the KYC/AML requirements. Global fraud losses are projected to cross billions of dollars in a year, thus exponentially increasing the demand for AI-enabled risk solutions across the BFSI sector.

Sustainability has become a critical driver of data-center transformation, as enterprises face growing pressure from regulators, stakeholders, and customers to reduce their environmental impact.

With digitization, the business model moves. Under pressure, traditional IT systems make massive migrations into agile and scalable data center infrastructures. Companies today must ready themselves for competition through real-time data access, faster application deployments, and seamless scalability, all of which are standard today in continuously changing environments. Legacy systems generally incur too much rigidity and cost on maintenance, along with their inability to support modern workloads such as AI, big data, and IoT. Cloud integration-hybrid and multi-cloud models-forms opportune outlets for organizations to manage workloads across platforms while optimizing cost and performance. Recent industry reports indicate that more than 70 percent of enterprises are making investments in hybrid cloud infrastructure to assist with operational flexibility. Agile data centers allow companies to respond faster to market changes, customer demand, and internal innovation cycles. In addition, containerization and virtualization technologies complement DevOps practices by supporting dynamic provisioning and resource optimization. The driving force further accelerated has been the growing need for agile infrastructure to cater to the new norm of remote working, mobile accessibility, and distributed teams. As such, edge computing has been closely associated with this transformation in bringing data processing closer to sources of latency and faster decision-making. This foundation of the new infrastructure goes on to solidify real-time analytics, the betterment of end-user experience, and improved business outcomes as well. Therefore, agility and scalability in data centers will no longer remain a luxury within IT; they are going to be taken as a first need by future organizations.

Data-Center Transformation Market Restraints and Challenges:

One of the major restraints in the Data-Center Transformation Market is the high upfront capital investment and integration complexity involved in upgrading legacy systems.

One of the major restraints in the Data-Center Transformation Market is the high upfront capital investment and integration complexity in upgrading a legacy system. Transforming traditional data centers into agile and cloud-ready environments entails considerable investments in new hardware, software, skilled personnel, and infrastructure redesign. This financial burden can be a primary reason for discouraging SMEs if ROI does not appear on the horizon immediately. The associated integration issues posed by introducing modern technologies like AI, virtualization, and hybrid cloud with legacy systems could likewise cause compatibility problems, operational disruption, data migration, and many other challenges. Most organizations are grappling with the shortage of skilled IT personnel who can handle and orchestrate such a complicated transformation. Security risks during migration and compliance issues add to the hesitation. The absence of standard frameworks for such transitions and vendor lock-in makes transitions a gamble and quite an expensive affair. While the long-term benefits may be hugely apparent, it is seen that many companies either delay or downscale their transformation initiatives. Hence, these hurdles call for the development of modular, cost-effective, and well-supported solutions to facilitate the phased transition without overburdening existing operations.

Data-Center Transformation Market Opportunities:

With AI-driven automation and edge computing taking center stage, the Data-Center Transformation Market also opens various doors of opportunity. As enterprises increasingly rely on data to make operational decisions, sustainable and intelligent self-optimizing infrastructure is becoming more necessary. AI and machine learning are beginning to automate critical workloads in an operational environment, such as workload management, predictive maintenance, and energy optimization, which would consequently help minimize downtime and cost. The demand for edge data centers is also heightened with the advent of IoT, smart cities, autonomous vehicles, and 5G, pushing for a greater processing of data nearer to the source of data generation. This essentially creates a huge opportunity for vendors to offer micro-data centers and modular, scalable solutions targeted at different sectors and geographical regions. Further, the rising trend toward data sovereignty and regulatory compliance brings regional opportunity as localized infrastructure is usually preferred. Emerging markets in Asia-Pacific, Latin America, and the Middle East are among the steepest in growth, prompted by digitalization and cloud adoption. Also, data center solutions aligned with the "green" goals confer a market advantage by appealing to eco-conscious parties. Each of these trends gives room for vendors and service providers to explore a vibrant and expanding environment in which to innovate, differentiate, and scale.

Data-Center Transformation Market Segmentation:

Market Segmentation: By Deployment Model

• On-Premise

• Cloud-Based

• Colocation

The transformation market for data centers around the world can be segmented based on deployment mode into on-premise solutions, cloud-based solutions, and colocation solutions-with each of these solutions having its own set of advantages and driving factors. Preferred for organizations with high security, compliance, and control requirements, on-premise solutions are especially favored in sectors such as government and banking. For the most part, they require a large amount of capital, are complex to manage, and encounter difficulties in terms of scaling. Thus began the rise of cloud-based deployment; generally flexible, with low upfront costs and rapid scalability, it grew in importance. Most public, private, and hybrid cloud models allow seamless integration with AI, automation, and remote access, making those solutions desirable for export-oriented companies. With cloud-native provisioning of resources in real-time and the possibility for enhanced disaster recovery, these solutions are on the rise. Meanwhile, colocation seems to have significant demand as a secure and cost-effective hosting solution for enterprises that do not want to bear the physical infrastructure. It gives a guarantee of uptime, specialized management in running the facility, and energy saving-the true strategy for companies that want to focus on their core business. Colocation is becoming an increasingly appealing choice for small and medium enterprises and multinational corporations with operations spread across different geographies. Against this backdrop, with increasing demand for edge computing and hybrid work cultures, a blend of cloud and colocation emerges as a preferred strategy. Across these models, vendors are increasingly offering integrated platforms to streamline the deployment and provide IT leaders, finding their way through transformation, with end-to-end visibility and control.

Market Segmentation: By Tier Type

• Tier 1 Data Centers

• Tier 2 Data Centers

• Tier 3 Data Centers

• Tier 4 Data Centers

Data centers are classified into four standard tiers, Tier 1 through Tier 4, based on uptime, redundancy, and operational capabilities, and these classifications strongly influence transformation strategies. Tier 1 data centers, with basic infrastructure and single power and cooling paths, are the most economical but least reliable, often used by startups or local businesses with limited uptime requirements. Tier 2 data centers introduce partial redundancy, improving fault tolerance slightly while keeping costs relatively low. These are typically found in mid-sized enterprises that need moderate levels of availability. However, as business operations become more data-dependent, the market is rapidly shifting toward Tier 3 and Tier 4 facilities. Tier 3 data centers offer concurrently maintainable infrastructure with 99.982% uptime, enabling continuous operation even during maintenance.

They are popular in sectors like finance, healthcare, and IT services. Tier 4 data centers, the most advanced, deliver fault-tolerant systems with 99.995% uptime, ensuring the highest level of redundancy, automation, and disaster resilience. These are adopted by mission-critical operations requiring 24/7 availability and no tolerance for downtime. Enterprises are increasingly upgrading to higher-tier facilities or transforming their Tier 1/2 setups to Tier 3/4 standards through modular redesigns and automation tools. This shift is expected to gain momentum through 2030, especially as digital services demand more robust infrastructure.

Market Segmentation: By End User

• IT & Telecom

• BFSI

• Healthcare

• Government & Public Sector

Saying that the segments of end users in this market on data-center transformation would bring different drivers and needs for the key verticals-such as IT & Telecom, BFSI, Healthcare, and Government & Public Sector-is somewhat evident in terms of the transformation directions those in the IT & Telecom domains take as they're structural elements of the digital economy demanding the lowest latency and highest availability data centers for cloud platforms, 5G networks, and AI-based applications. Nowadays, modern infrastructure should be more scalable, agile, and edge-enabled, so the focus on transformations has broadened among telcos and tech companies. Bank, Financial Services & Insurance institutional data centers are transformed on a compliance basis with the regulator, as well as cyber security concerns, along with 24/7 service deliverables with high expectations on multi-tier data centers and state-of-the-art encryption with cloud-assisted disaster recovery offerings. The healthcare facilities have now embraced a more digital health system approach with telemedicine and real-time patient data connecting platforms, thus requiring secure infrastructural compliance. Data centers in this area have to meet HIPAA standards and other similar data security standards, forcing hybrid and automated standards to meet such demands. Digitization projects at the national level, smart city projects, and citizen service portals are also prompting this transformation in order to modernize their legacy infrastructures. Governments are also adding value to this market through green data centers by incentives and public-private partnerships. Each has its transformation challenges and opportunities, thus making a vertical-specific customization key to success for a provider.

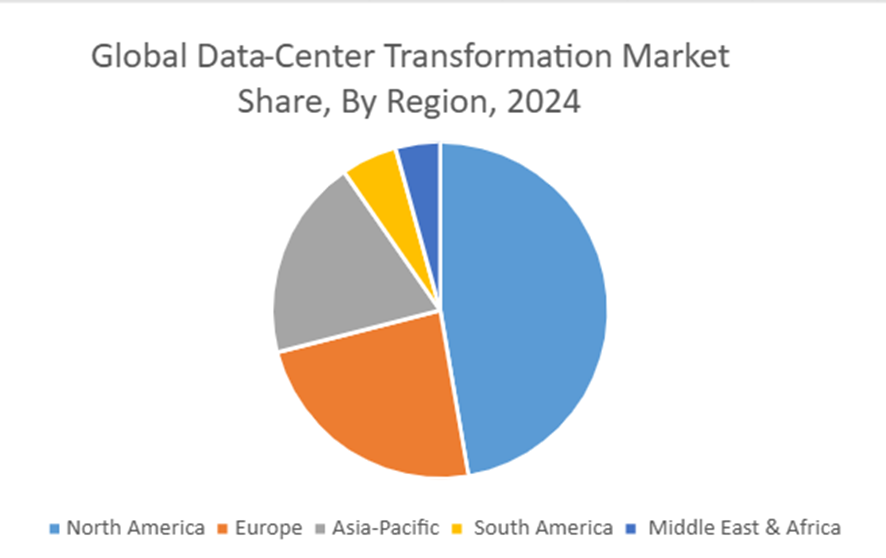

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

The transformation of the Data Center Market presents various growth drivers across different regions. Among the territories, North America is taking the lead, with the U.S. demonstrating a larger share and being the cradle of hyperscale data centers, rapid cloud adoption, and heavy investments in AI-driven infrastructure. Europe is becoming a sustainability-oriented region, which sees its transformation strategies being shaped by strict data privacy regulations such as GDPR, all put together with a growing focus on green and hybrid data centers. On the other hand, the Asia Pacific market is in massive expansion powered by the wake of 5G deployment, increasing IoT use cases, and major smart cities initiatives across key states such as China, India, and Singapore. South America is witnessing steady growth due to an uptick in cloud migration and IT outsourcing, especially in Brazil and Mexico. The comparatively new digital infrastructure upgrades are being carried out in the Middle East and Africa, where implementing national digital transformations and smart governance projects has been majorly instrumental in pushing forward data center modernization. Each continent has a list of opportunities that are unique when placed in context with technological maturity, regulatory environment, and economic development.

COVID-19 Impact Analysis on the Data-Center Transformation Market:

The impact of COVID-19 was deep in the Data-Center Transformation Market-the prime driver within it for accelerated digital adoption across all sectors. With global lockdowns in order, organizations moved into a remote, virtual, collaborative, cloud-dependent operation mode, and the demand for scalable, secure, and resilient data center infrastructure has outgrown any previous levels. Enterprises that had put off modernization now had to hasten their transformation initiatives for business continuity and operational agility. Cloud migration activity increased significantly, and a hybrid infrastructure that allowed organizations maximum flexibility and cost efficiency was standard. Furthermore, the pandemic uncovered the weak points of legacy systems: uptime, remote access, and cybersecurity, all of which spurred new investment in automation and software-defined data centers. However, the calamity also disrupted global supply chains and delayed hardware upgrades and new data center builds in certain regions. Some smaller enterprises faced tighter budgetary situations, slowing their transformation. Still, the net effect of COVID-19 on the overall market was considered to be mostly beneficial from a long-term perspective; new strategic priorities were reshaped, and digital infrastructure was embedded as a core element of organizational resilience. More agile after the pandemic, the market will put a larger emphasis on cloud-native solutions, remote monitoring, and a range of edge computing as vital enablers of the next growth phase into the future.

Latest Trends/ Developments:

Up until October 2023, vast amounts of data halls have been undergoing innovation in their transformation market, catalyzed by AI, sustainability, and edge computing. The trends mark big data center "factories" powered by AI, with vendors such as Dell providing delivery within hours of installation of modular GPU racks built to support the massive demand for AI workloads. At the same time, the business of delivering low latency to IoT and 5G applications is witnessing a rush toward implementing edge computing close to the users in the form of micro-data centers for real-time data production. The demand for energy efficiency is another prime target since rack power demand is anticipated to double by 2030, thus accelerating the adoption of liquid and immersion cooling technologies. The EU Climate Neutral Pact and Singapore's Green Mark for sustainability regulations are integrating renewable energy with waste heat reuse. In addition, DCaaS is emerging as the favorite option, which is architected to facilitate scalability and cushion operational upfront capital for the enterprises. On the cybersecurity front, zero trust architecture is fast becoming commonplace, with AI-based detection and response to threats gaining traction. Apart from these, the industry is grappling with a severe shortage of talent; hence, the shift towards standardization in operations and modular as well as prefabricated data centers to lower the needs for a specialized workforce. All these trends point to a direction of greater intelligence, environmental friendliness, and decentralized transition of data infrastructure.

Key Players:

• Dell (US)

• Microsoft (US)

• IBM (US)

• Schneider Electric (France)

• Cisco (US)

• NTT (Japan)

• HCLTech (India)

• Accenture (Ireland)

• Cognizant (India)

• Google (US)

Chapter 1. Global Data-Center Transformation Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Data-Center Transformation Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Data-Center Transformation Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Data-Center Transformation Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Data-Center Transformation Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Data-Center Transformation Market – By Deployment Model

6.1. Introduction/Key Findings

6.2. On-premise

6.3. Cloud-Based

6.4. Colocation

6.5. Y-O-Y Growth trend Analysis By Model

6.6. Absolute $ Opportunity Analysis By Model, 2025-2030

Chapter 7. Global Data-Center Transformation Market – By Tier Type

7.1. Introduction/Key Findings

7.2. Tier 1 Data Centers

7.3. Tier 2 Data Centers

7.4. Tier 3 Data Centers

7.5. Tier 4 Data Centers

7.6. Y-O-Y Growth trend Analysis By Type

7.7. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 8. Global Data-Center Transformation Market – By End User

8.1. Introduction/Key Findings

8.2. IT & Telecom

8.3. BFSI

8.4. Healthcare

8.5. Government & Public Sector

8.6. Y-O-Y Growth trend Analysis By End User

8.7. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 9. Global Data-Center Transformation Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Deployment Model

9.1.3. By Tier Type

9.1.4. By End User

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Deployment Model

9.2.3. By Tier Type

9.2.4. By End User

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Deployment Model

9.3.3. By Tier Type

9.3.4. By End User

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Deployment Model

9.4.3. By Tier Type

9.4.4. By End User

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Deployment Model

9.5.3. By Tier Type

9.5.4. By End User

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Data-Center Transformation Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Dell

10.2. Microsoft

10.3. IBM

10.4. Schneider Electric

10.5. Cisco

10.6. NTT

10.7. HCLTech

10.8. Accenture

10.9. Cognizant

10.10. Google

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Data-Center Transformation Market was valued at USD 8.8 billion in 2024 and is projected to reach a market size of USD 24.98 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.02%.

The key drivers of the Data-Center Transformation Market are the rising demand for agile, scalable, and cloud-integrated infrastructure and the need for energy-efficient, sustainable data center operations. These are fueled by digital transformation, AI workloads, edge computing, and stricter regulatory and ESG requirements.

The Data-Center Transformation Market by tier type is segmented into Tier 1, Tier 2, Tier 3, and Tier 4. Each type caters to different user needs.

North America is the most dominant region for the Data-Center Transformation Market.

Dell (US), Microsoft (US), IBM (US), Schneider Electric (France), Cisco (US), NTT (Japan), HCLTech (India), Accenture (Ireland), Cognizant (India), Google (US), Wipro (India), Atos (France), TCS (India), Hitachi (Japan) are the key players in the Data-Center Transformation Market.