Global Data Center Solutions Market Research Report – Segmentation by Solution Type (IT Infrastructure, Power Solutions, Cooling Solutions, Security Solutions, DCIM); by Data Center Type (Enterprise Data Centers, Colocation Data Centers, Hyperscale Data Centers, Edge Data Centers); by End-User Industry (IT & Telecom, Banking, Financial Services & Insurance (BFSI), Healthcare, Government & Defense, Retail & E-commerce, Energy & Utilities); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9900

Format:

Region: Global

Market Size and Overview:

The Data Center Solutions Market was valued at USD 376 billion in 2024 and is projected to reach a market size of USD 721.42 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 13.92%.

The data center solutions market encompasses a wide range of technologies and services designed to support the efficient operation of data centers. It includes components such as IT infrastructure, power and cooling systems, physical and cybersecurity, and software for infrastructure management. These solutions are essential for maintaining uptime, ensuring scalability, and optimizing energy efficiency. The market serves various data center types, including enterprise, colocation, hyperscale, and edge facilities. It caters to a broad range of industries such as IT and telecom, finance, healthcare, retail, and government.

Modern data centers require high-performance computing, storage, and network resources to handle increasing workloads and data volumes. Providers in this space offer both hardware and software products, often integrated with cloud and virtualization technologies. Sustainability and energy efficiency have become major focus areas, prompting demand for innovations in cooling and power distribution. The adoption of AI, IoT, and 5G technologies is reshaping the design and operation of next-generation data centers. Vendors compete on reliability, scalability, security, and the ability to deliver hybrid and multi-cloud environments.

Key Market Insights:

Hyperscale data centers are rapidly expanding to support the growth of cloud services and AI-driven workloads. As of mid-2022s estimates, there are over 800 hyperscale data centers globally, with hundreds more planned by 2030. These facilities can support tens of thousands of servers and often exceed 100,000 square feet, driving demand for scalable power, cooling, and IT infrastructure.

Data centers account for approximately 1–1.5% of global electricity use, making energy efficiency a top priority. Solutions like liquid cooling and renewable-powered backup systems are gaining traction to reduce operating costs and carbon footprints. Power Usage Effectiveness (PUE), a key efficiency metric, is now targeted at 1.1–1.3 in modern, green-certified data centers.

Security remains a critical concern as cyberattacks and physical threats to data centers increase. Over 80% of enterprises cite security as a top consideration when selecting data center providers. Solutions now integrate AI-driven monitoring, biometric access control, and encrypted network infrastructure to mitigate both internal and external risks.

Data Center Infrastructure Management (DCIM) tools are evolving into software-defined platforms with AI and machine learning capabilities. These tools enable predictive maintenance, automated energy optimization, and dynamic resource allocation. By 2025, it's estimated that over 60% of new data centers will incorporate some level of AI-based management system to improve operational efficiency.

Data Center Solutions Market Drivers:

Surge in Cloud Computing and Digital Transformation

The widespread adoption of cloud-based services by enterprises and consumers is a major driver of demand for advanced data center infrastructure. Businesses are migrating workloads to hybrid and multi-cloud environments, requiring scalable, secure, and high-performance data center solutions. This trend is reinforced by ongoing digital transformation initiatives across sectors such as finance, healthcare, and retail. As cloud traffic grows, so does the need for robust backend infrastructure.

Proliferation of AI, IoT, and Big Data Applications

AI, IoT, and big data analytics are generating vast volumes of data that must be processed, stored, and transmitted efficiently. These technologies demand high-performance computing, low latency, and reliable storage capabilities—necessitating powerful and specialized data center solutions. Edge computing is also being adopted to bring processing closer to the data source, minimizing latency. This technological evolution is reshaping the architecture and capacity requirements of modern data centers.

Rising Demand for Energy-Efficient and Sustainable Operations

Energy consumption is a growing concern for data center operators due to environmental regulations and rising operational costs. There is a strong push toward energy-efficient hardware, renewable energy integration, and advanced cooling systems to reduce carbon footprints. Government incentives and corporate sustainability goals are further accelerating the shift toward green data center solutions. As a result, sustainability is becoming a competitive differentiator in the market.

Data Center Solutions Market Restraints and Challenges:

High Capital and Operational Expenditures

Building and maintaining data centers requires significant upfront investment in land, infrastructure, equipment, and energy systems. Operational costs remain high due to the need for continuous power, cooling, security, and staffing. These financial barriers can limit entry for smaller players and delay expansion plans for existing operators. The high cost of compliance with regulatory standards further adds to the burden.

Infrastructure Scalability and Legacy System Integration

Many enterprises struggle to scale their data center infrastructure efficiently while maintaining compatibility with older systems. Legacy hardware and software can hinder the adoption of modern, software-defined, or cloud-integrated solutions. Upgrading existing infrastructure without disrupting critical operations is both complex and costly. This challenge slows down digital transformation and reduces agility in responding to new demands.

Skilled Workforce Shortage

The data center industry faces a global shortage of skilled professionals in areas such as network engineering, cooling technologies, and data center management. As infrastructure becomes more complex with AI, edge computing, and automation, the demand for specialized talent is rising sharply. However, the pipeline of trained personnel is not keeping pace, leading to operational risks and project delays. Retaining experienced staff is also becoming increasingly difficult in competitive markets.

Data Center Solutions Market Opportunities:

The data center solutions market presents several compelling opportunities driven by evolving digital infrastructure needs. The rapid expansion of edge computing opens new markets for compact, modular data centers that serve remote and latency-sensitive applications. Emerging economies in Asia-Pacific, Latin America, and Africa are investing heavily in digital infrastructure, creating demand for new facilities and local data hosting solutions. The push toward sustainability is spurring innovation in green technologies, including liquid cooling, renewable energy integration, and energy-efficient power systems.

There's also strong opportunity in AI-optimized data center management, where predictive analytics and automation can reduce costs and downtime. As regulatory pressures increase around data sovereignty and privacy, there’s a growing need for localized and compliant infrastructure solutions. Additionally, hybrid and multi-cloud environments are becoming the norm, opening opportunities for vendors offering flexible and interoperable systems. These trends collectively signal long-term growth potential for companies delivering scalable, secure, and energy-conscious data center solutions.

Data Center Solutions Market Segmentation:

Market Segmentation: by Solution Type

• IT Infrastructure

• Power Solutions

• Cooling Solutions

• Security Solutions

• DCIM

IT infrastructure is the backbone of any data center and includes servers, storage systems, and networking equipment. These components enable data processing, transmission, and storage at high speeds and with high reliability. With the rise of cloud computing, virtualization, and AI, demand for high-performance and scalable infrastructure continues to grow. IT infrastructure accounts for approximately 40% of the total data center solutions market, making it the largest segment by value.

Power solutions ensure uninterrupted energy supply and include systems like UPS (Uninterruptible Power Supply), backup generators, and power distribution units (PDUs). These solutions are vital for maintaining uptime and protecting data centers from outages or power fluctuations. With rising energy demands and the need for efficiency, there is increasing interest in smart grid integration and renewable energy sources. Power solutions contribute to around 20% of the market, driven by both operational needs and sustainability goals.

Cooling systems manage the temperature and airflow within data centers to prevent overheating of IT equipment. Solutions include CRAC units, chillers, liquid cooling systems, and economizers, with newer technologies focusing on energy efficiency. Efficient cooling has become critical as server densities increase, particularly in hyperscale and AI-intensive environments. Cooling solutions hold approximately 18% of the market, and this share is expected to rise with demand for greener, more effective systems.

Market Segmentation: by Data Center Type

• Enterprise Data Centers

• Colocation Data Centers

• Hyperscale Data Centers

• Edge Data Centers

Enterprise data centers are privately owned facilities operated by a single organization, primarily used to manage internal IT operations and proprietary data. These data centers offer high control, customization, and security, which is why they’re still preferred in regulated industries like banking and healthcare. However, many enterprises are gradually shifting to hybrid or cloud models to reduce costs and improve scalability. Enterprise data centers currently account for approximately 35% of the global market, though this share is slowly declining as outsourcing increases.

Colocation centers provide shared space, power, and cooling for businesses to house their servers and networking equipment. They are attractive due to lower capital expenditures, scalability, and access to premium infrastructure and connectivity without full ownership. Enterprises and small-to-medium businesses often prefer colocation to avoid the operational burden of managing in-house facilities. Colocation data centers hold about 30% of the global market, supported by rising demand for flexibility and proximity to end users.

Market Segmentation: by End-User Industry

• IT & Telecom

• Banking

• Financial Services & Insurance (BFSI)

• Healthcare

• Government & Defense

• Retail & E-commerce

• Energy & Utilities

Enterprise data centers are privately owned and operated facilities dedicated to supporting the IT operations of a single organization. These are commonly used by large corporations for hosting proprietary applications and sensitive data within their own infrastructure. While enterprises still maintain on-premises data centers, many are transitioning to hybrid or cloud-first models to increase flexibility. Enterprise data centers currently hold around 35% of the market share, though this share is gradually declining due to rising demand for colocation and cloud-based alternatives.

Colocation facilities provide shared physical space, power, and cooling for multiple organizations, allowing them to deploy their own IT equipment within a secure third-party environment. This model is especially attractive to businesses seeking to avoid the high capital expenditures of building their own data centers. With scalability, geographic diversity, and high-speed interconnection services, colocation continues to be a popular option for mid-sized and large enterprises. Colocation data centers account for approximately 25% of the market, with steady growth driven by demand for flexibility and proximity to cloud providers.

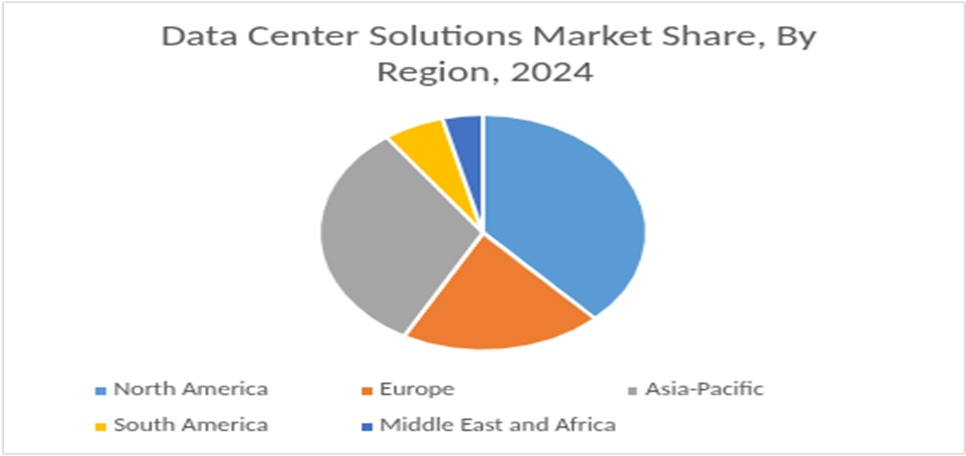

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is the largest and most mature market for data center solutions, driven by high digital adoption and the presence of tech giants like Amazon, Google, and Microsoft. The U.S. alone accounts for a major share, hosting hundreds of hyperscale and colocation data centers. The region has strong regulatory frameworks, widespread use of cloud computing, and early adoption of AI and edge technologies. North America holds approximately 38% of the global market share, maintaining its leadership in both innovation and capacity.

Asia-Pacific is the fastest-growing region due to rapid digitization, rising internet penetration, and increasing cloud adoption in countries like China, India, Japan, and Southeast Asia. Government initiatives to support digital economies and smart city development are fueling demand for data center infrastructure. The expansion of 5G and AI-driven services further boosts the need for hyperscale and edge facilities. Asia-Pacific accounts for about 32% of the global market, with strong upward momentum.

COVID-19 Impact Analysis on the Global Data Center Solutions Market:

The COVID-19 pandemic had a significant impact on the data center solutions market, accelerating demand while exposing operational vulnerabilities. As businesses rapidly shifted to remote work, online collaboration, and cloud-based services, the need for reliable data center infrastructure surged. Video conferencing, e-commerce, and digital entertainment platforms experienced sharp spikes in traffic, prompting expansions in server capacity and bandwidth. This unexpected growth created supply chain disruptions, particularly in hardware components like servers, cooling units, and power systems, leading to delays in new deployments and upgrades.

Labor shortages and lockdown restrictions also slowed down on-site construction and maintenance activities in several regions. However, the crisis reinforced the importance of resilient, scalable, and secure data infrastructure, driving long-term investment in automation, AI-driven management, and hybrid cloud solutions. Data center operators also began to prioritize remote monitoring tools and software-defined infrastructure to reduce reliance on physical presence. Overall, while the pandemic caused short-term logistical challenges, it ultimately accelerated digital transformation and pushed the market toward faster innovation and cloud adoption.

Latest Trends/Developments:

The data center solutions market is experiencing rapid transformation, shaped by technological innovation, sustainability goals, and evolving user demands. One of the most prominent trends is the rise of AI-driven infrastructure management, where machine learning and automation are being used to optimize energy consumption, predict equipment failure, and enhance operational efficiency. Liquid cooling technologies are gaining traction, especially in hyperscale and high-performance computing environments, offering better thermal management than traditional air cooling. Sustainability is now a key priority, with data center operators increasingly turning to renewable energy sources, green building certifications, and carbon-neutral goals.

Edge computing continues to grow, with smaller, decentralized data centers being deployed closer to end users to support latency-sensitive applications such as IoT, autonomous vehicles, and 5G. In parallel, modular and prefabricated data centers are emerging as a cost-effective and scalable solution for fast deployment in urban and remote areas. The demand for hybrid and multi-cloud environments is reshaping IT infrastructure strategies, requiring flexible and interoperable solutions. Enhanced cybersecurity solutions are also a focus, as data centers face growing threats from ransomware, DDoS attacks, and internal breaches. Additionally, there's growing investment in data center automation and software-defined infrastructure, enabling remote management and reducing dependence on physical staff. Together, these trends reflect a shift toward more intelligent, efficient, and resilient data center ecosystems.

Key Players:

• Huawei (China)

• Equinix (US)

• KDDI (Japan)

• Dell (US)

• Microsoft (US)

• Digital Realty (US)

• AWS (US)

• NTT (Japan)

• HPE (US)

• Google (US)

Chapter 1. Global Data Center Solutions Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Data Center Solutions Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn/$Tn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Data Center Solutions Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Data Center Solutions Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Data Center Solutions Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Data Center Solutions Market – By Solution Type

6.1. Introduction/Key Findings

6.2. IT Infrastructure

6.3. Power Solutions

6.4. Cooling Solutions

6.5. Security Solutions

6.6. DCIM

6.7. Y-O-Y Growth trend Analysis By Solution Type

6.8. Absolute $ Opportunity Analysis By Solution Type, 2025-2030

Chapter 7. Global Data Center Solutions Market – By Data Center Type

7.1. Introduction/Key Findings

7.2. Enterprise Data Centers

7.3. Colocation Data Centers

7.4. Hyperscale Data Centers

7.5. Edge Data Centers

7.6. Y-O-Y Growth trend Analysis By Data Center Type

7.7. Absolute $ Opportunity Analysis By Data Center Type, 2025-2030

Chapter 8. Global Data Center Solutions Market – By End-User Industry

8.1. Introduction/Key Findings

8.2. IT & Telecom

8.3. Banking

8.4. Financial Services & Insurance (BFSI)

8.5. Healthcare

8.6. Government & Defense

8.7. Retail & E-commerce

8.8. Energy & Utilities

8.9. Y-O-Y Growth trend Analysis By End User

8.10. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 9. Global Data Center Solutions Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Solution Type

9.1.3. By Data Center Type

9.1.4. By End-User Industry

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Solution Type

9.2.3. By Data Center Type

9.2.4. By End-User Industry

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Solution Type

9.3.3. By Data Center Type

9.3.4. By End-User Industry

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Solution Type

9.4.3. By Data Center Type

9.4.4. By End-User Industry

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Solution Type

9.5.3. By Data Center Type

9.5.4. By End-User Industry

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Global Data Center Solutions Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Huawei (China)

10.2. Equinix (US)

10.3. KDDI (Japan)

10.4. Dell (US)

10.5. Microsoft (US)

10.6. Digital Realty (US)

10.7. AWS (US)

10.8. NTT (Japan)

10.9. HPE (US)

10.10. Google (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Data Center Solutions Market was valued at USD 376 billion in 2024 and is projected to reach a market size of USD 721.42 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 13.92%.

Surge in Cloud Computing and Digital Transformation, Proliferation of AI, IoT, and Big Data Applications, Rising Demand for Energy-Efficient and Sustainable Operations are some of the key market drivers in the Data Center Solutions Market.

IT Infrastructure, Power Solutions, Cooling Solutions, Security Solutions, DCIM are the segments by Solution Type in the Data Center Solutions Market.

North America is the most dominant region for the Global Data Center Solutions Market.

Huawei (China), Equinix (US), KDDI (Japan), Dell (US), Microsoft (US), Digital Realty (US), AWS (US), NTT (Japan), HPE (US), Google (US) etc.