Global Data Center Security Market Research Report – Segmentation by Component (Solution & Services); By Type (Small Data Center, Medium Data Center, Large Data Center); By End Use (IT & Telecom, BFSI, Retail & E-commerce, Media & Entertainment, Healthcare, Energy & Utilities, Government, Manufacturing, Education, others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9898

Format:

Region: Global

Market Size and Overview:

The Global Data Center Security Market was valued at USD 18.42 billion in 2024 and is projected to reach a market size of USD 46.10 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 20.14%.

The Data Center Security Market focuses on protecting the critical infrastructure, data, and applications within data centers from evolving cyber threats, physical breaches, and operational vulnerabilities. As data centers become the backbone of digital enterprises, safeguarding sensitive information and ensuring continuous uptime have become paramount. The increasing adoption of cloud computing, virtualization, and hybrid environments has introduced new security challenges, requiring advanced solutions that combine physical security measures with robust cybersecurity technologies. With growing cyberattacks and stricter regulatory requirements, organizations are prioritizing comprehensive security frameworks to protect their data centers from both internal and external risks, driving innovation in security tools, monitoring, and response systems.

Key Market Insights:

The increasing number of cyberattacks targeting critical infrastructure has driven a sharp increase in the demand for robust data center security. Reports indicate that data breaches exposed over 22 billion records globally in a single year, underlining the urgency for stronger protection. As data centers continue to handle sensitive financial, healthcare, and enterprise information, organizations are adopting multi-layered security systems to address both digital and physical vulnerabilities.

The adoption of biometric access controls and advanced surveillance systems is rising rapidly in physical security across data centers. Nearly 60% of large data centers have already implemented biometric authentication methods to restrict unauthorized access, ensuring only verified personnel can enter sensitive areas. This move significantly reduces the risk of physical threats such as hardware tampering, insider breaches, or theft.

On the cybersecurity front, the rise in insider threats and malware has driven the use of AI-driven monitoring tools. Studies reveal that over 70% of enterprises now integrate AI and machine learning into their security systems to detect anomalies and respond to threats in real-time. These intelligent systems not only reduce incident response times but also improve overall data center resilience in an era of growing digital complexity.

Data Center Security Market Drivers:

Rising Frequency of Cyberattacks and Data Breaches Is Forcing Enterprises to Strengthen Data Center Security Infrastructure

As cyber threats become more sophisticated and frequent, organizations are under mounting pressure to fortify their data center security. From ransomware to advanced persistent threats (APTs), attackers are continuously targeting sensitive enterprise data, seeking vulnerabilities in both physical and digital infrastructures. With cyberattacks now capable of halting operations, stealing intellectual property, or compromising customer information, enterprises are increasingly adopting layered defense mechanisms that include firewalls, intrusion prevention systems, and behavioral analytics. This urgency is especially high in sectors like BFSI, healthcare, and government, where data sensitivity is critical and compliance with regulatory mandates is non-negotiable.

Increased Adoption of Cloud and Virtualized Environments Is Driving the Need for Integrated and Scalable Security Solutions

The global shift toward cloud computing, virtualization, and hybrid environments is dramatically reshaping the data center landscape—and with it, the security requirements. Traditional perimeter-based security models are no longer sufficient in a distributed computing ecosystem where data is constantly in motion across on-premises systems and multiple cloud platforms. This has led to the rise of zero-trust frameworks and micro-segmentation strategies, which ensure that even within a network, every access request is verified. Enterprises are increasingly demanding solutions that can provide real-time visibility, automation, and control across both physical and virtual environments. The dynamic nature of cloud environments, combined with constant application updates and third-party integrations, requires a security infrastructure that is agile, adaptive, and centrally managed.

Tightening Regulatory Landscape and Compliance Requirements Are Compelling Organizations to Prioritize Security Measures

Data privacy regulations such as GDPR, HIPAA, and others across different regions have put immense pressure on enterprises to demonstrate compliance through stringent data security practices. Non-compliance not only results in financial penalties but also damages brand reputation and customer trust. This regulatory pressure has encouraged organizations to invest proactively in advanced data center security solutions that ensure end-to-end protection and auditability. Compliance requirements often necessitate encryption, access controls, data loss prevention, and detailed logging—all of which are increasingly becoming standard components of data center security frameworks.

Rapid Growth of IoT and Connected Devices Is Expanding the Attack Surface of Data Centers

With billions of connected devices transmitting data to and from data centers, the threat surface has expanded exponentially. IoT devices, often lacking built-in security, can become easy entry points for cybercriminals, posing significant risks to data center integrity. As smart technologies are integrated into industries ranging from manufacturing to healthcare, data centers must now handle more traffic, more endpoints, and more vulnerability points than ever before. This has pushed data center security providers to innovate with network access controls, device authentication protocols, and anomaly detection tools tailored for IoT-rich environments.

Data Center Security Market Restraints and Challenges:

High Cost of Implementation and Complex Integration Pose Major Restraints in Widespread Adoption of Data Center Security Solutions

Despite the rising importance of securing data centers, the high initial cost of advanced security infrastructure and the complexity of integrating various solutions into existing systems remain significant barriers. Many organizations, particularly small and mid-sized enterprises, struggle with the capital expenditure required for technologies like biometric access controls, AI-based monitoring tools, and real-time threat analytics. Additionally, implementing these solutions often demands skilled personnel and a deep understanding of cybersecurity frameworks, which can lead to increased operational complexity. Compatibility issues with legacy systems and the ongoing need for updates, maintenance, and compliance adherence further add to the challenge, limiting faster adoption across the global landscape.

Data Center Security Market Opportunities:

The Data Center Security Market presents significant opportunities driven by the rising demand for edge computing, AI integration, and smart infrastructure across industries. As organizations expand their digital ecosystems and decentralize data processing closer to the user, the need for robust, scalable, and adaptive security frameworks becomes critical. This opens avenues for innovative security solutions that combine real-time monitoring, predictive analytics, and automated threat response tailored for edge and hybrid environments. Additionally, the growing popularity of Software-Defined Data Centers (SDDCs) and cloud-native applications is fueling demand for flexible, API-driven security tools.

Data Center Security Market Segmentation:

Market Segmentation: By Component:

• Solution

• Services

The solution segment plays a dominant role in the data center security market, driven by the increasing need for advanced protection mechanisms such as firewalls, intrusion detection systems, access controls, encryption, and data loss prevention tools. As cyber threats grow in frequency and sophistication, enterprises are prioritizing the deployment of comprehensive, layered security solutions that provide both physical and virtual safeguards. The push toward zero-trust architecture and automation has further elevated the importance of integrated security platforms, enabling organizations to detect, respond to, and neutralize threats in real-time.

Meanwhile, the services segment is expected to experience fastest growth during the forecast period, fueled by increasing demand for professional and managed security services across industries. As the complexity of data center environments rises—particularly with multi-cloud adoption, remote workforces, and IoT integration—businesses are turning to external service providers for expertise in risk assessments, security audits, incident response, and regulatory compliance. These services not only fill the skill gaps within organizations but also provide scalable, cost-effective solutions that can be tailored to evolving security requirements. Managed services, in particular, are gaining traction among small and mid-sized enterprises, offering round-the-clock threat monitoring and reduced internal workload.

Market Segmentation: By Type:

• Small Data Center

• Medium Data Center

• Large Data Center

The large data center segment holds a dominant position in the data center security market, primarily due to its expansive infrastructure and high-volume data processing responsibilities. These facilities support mission-critical applications for major enterprises, cloud service providers, and government institutions, making them prime targets for sophisticated cyber threats and physical intrusions. As a result, large data centers invest heavily in advanced, multi-layered security systems that include biometric access controls, AI-powered threat detection, video surveillance, and encryption solutions. The demand to comply with stringent global regulations and ensure uninterrupted service delivery further pushes these organizations to adopt the most robust and comprehensive security frameworks available in the market.

On the other hand, the medium data center segment is projected to grow at the fastest rate, supported by the rapid digitalization of mid-sized enterprises and the growing need for secure infrastructure in regional markets. These centers serve as a critical bridge between small IT setups and hyperscale facilities, offering scalable computing and storage solutions while maintaining cost-efficiency. With increasing pressure to ensure data privacy and business continuity, medium-sized facilities are now integrating cloud security, endpoint protection, and managed services into their operations. Their adoption of hybrid cloud strategies and virtualization technologies has also accelerated the need for customized, scalable security tools that align with their evolving infrastructure needs.

Market Segmentation: By End Use:

• IT & Telecom

• BFSI

• Retail & E-commerce

• Media & Entertainment

• Healthcare

• Energy & Utilities

• Government

• Manufacturing

• Education

• Others

The IT & Telecom segment is the dominant end-use sector in the data center security market, primarily due to the massive volumes of sensitive data generated, processed, and stored by telecom operators and tech companies. These organizations manage everything from customer data to communication infrastructures and cloud services, making them frequent targets of cyberattacks and data breaches. The rise of 5G networks, IoT devices, and edge computing has further expanded the attack surface, prompting this sector to invest heavily in robust data center security frameworks.

The healthcare segment is expected to be the fastest-growing end-use category, fueled by the digitization of medical records, the surge of telemedicine, and the integration of connected medical devices. Healthcare organizations handle extremely sensitive patient information and are bound by strict data privacy regulations such as HIPAA, pushing them to adopt high-level security solutions for their data centers. With the increased use of AI for diagnostics, cloud-based healthcare platforms, and remote patient monitoring, the need for real-time data protection, anomaly detection, and access restrictions has intensified.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

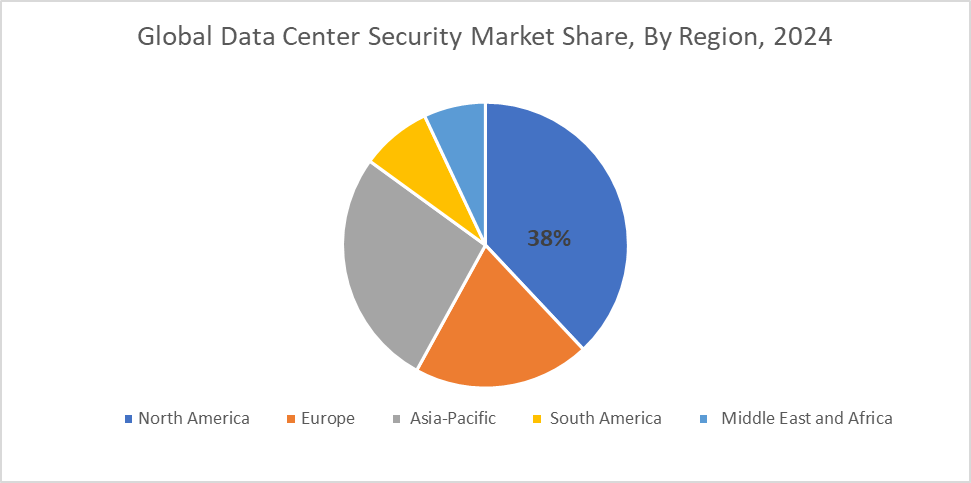

The dominant region in the data center security market is North America, accounting for 38% of the global share. This leadership position is fueled by the presence of major technology companies, extensive data center infrastructure, and early adoption of advanced security technologies such as AI-based threat detection and zero-trust architectures. The region also has strict regulatory requirements, like CCPA and HIPAA, which compel organizations to invest significantly in robust data center protection strategies. Additionally, frequent targeted cyberattacks have made security a top priority for enterprises and public agencies alike.

The fastest-growing region is Asia-Pacific, contributing around 27% of the market but showing the highest CAGR. This rapid growth is attributed to increasing digital transformation initiatives across emerging economies, particularly in India, China, and Southeast Asia. The expansion of cloud services, data localization mandates, and rising concerns over cybersecurity threats are pushing enterprises in the region to upgrade their data center security frameworks. Government initiatives promoting smart cities and digital banking, along with increasing investments in data center construction, are also fueling the need for both physical and cyber-security solutions at scale.

COVID-19 Impact Analysis on the Global Data Center Security Market:

The COVID-19 pandemic accelerated the adoption of remote work and cloud-based services, significantly increasing the demand for robust data center security solutions. As organizations rapidly shifted to digital operations, the volume and complexity of cyber threats also surged, pushing companies to strengthen their security infrastructure. However, supply chain disruptions and budget constraints during the pandemic slowed down new deployments for some businesses. Overall, the pandemic highlighted the critical demand for resilient, scalable, and adaptive security measures, driving long-term investment and innovation in the data center security market.

Latest Trends/ Developments:

The data center security market is witnessing rapid advancements in artificial intelligence (AI) and machine learning (ML) technologies that enhance threat detection and response capabilities. These intelligent systems analyze vast amounts of data in real-time to identify unusual patterns and potential breaches, enabling proactive defense against sophisticated cyberattacks. Additionally, the integration of zero-trust security models, which verify every user and device before granting access, is becoming a standard practice to minimize insider threats and unauthorized access within data centers. These trends are fueling a shift from traditional perimeter-based security to more dynamic, behavior-based protection frameworks.

Another significant development is the growing adoption of software-defined security solutions that provide flexibility and scalability in protecting hybrid and multi-cloud data center environments. These solutions allow organizations to centrally manage security policies and automate responses across distributed infrastructures, improving efficiency and reducing human error. Furthermore, there is an increased focus on securing edge data centers, as the proliferation of IoT devices and 5G networks expands the attack surface. Vendors are innovating with lightweight, yet robust security technologies tailored for edge environments, ensuring consistent protection from the core to the edge of the network.

Key Players:

• Cisco Systems, Inc.

• IBM Corporation

• Broadcom Inc.

• Dell Inc.

• Siemens AG

• Schneider Electric SE

• Juniper Networks, Inc.

• Fortinet, Inc.

• Honeywell International Inc.

• Palo Alto Networks, Inc.

Chapter 1. DATA CENTER SECURITY MARKET– Scope & Methodology

1.1. Market Segmentation

1.2. Assumptions

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. DATA CENTER SECURITY MARKET– Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.3. COVID-110 Impact Analysis

2.3.1. Impact during 2023 – 2030

2.3.2. Impact on Supply – Demand

Chapter 3. DATA CENTER SECURITY MARKET– Competition Scenario

3.1. Market Share Analysis

3.2. Product Benchmarking

3.3. Competitive Strategy & Development Scenario

3.4. Competitive Pricing Analysis

3.5. Supplier - Distributor Analysis

Chapter 4. DATA CENTER SECURITY MARKET- Entry Scenario

4.1. Case Studies – Start-up/Thriving Companies

4.2. Regulatory Scenario - By Region

4.3 Customer Analysis

4.4. Porter's Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. DATA CENTER SECURITY MARKET- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. DATA CENTER SECURITY MARKET– By Component

6.1. Solutions

6.2. Logical Security

6.3. Physical Security

6.4. Services

6.5. Professional Services

6.6. Managed Services

Chapter 7. DATA CENTER SECURITY MARKET– By Data Center Type

7.1. Mid-Sized Data Centers

7.2. Enterprise Data Centers

7.3. Large Data Centers

Chapter 8. DATA CENTER SECURITY MARKET– By Vertical

8.1. IT and Telecom

8.2. BFSI

8.3. Government and Defence

8.4. Healthcare

8.5. Energy

8.6. Others (Retail, Manufacturing, etc.)

Chapter 9. DATA CENTER SECURITY MARKET– By Region

9.1. North America

9.2. Europe

9.3. The Asia Pacific

9.4. Latin America

9.5. Middle-East and Africa

Chapter 10. DATA CENTER SECURITY MARKET – Company Profiles – (Overview, Product Portfolio, Financials, Developments)

10.1. Company 1

10.2. Company 2

10.3. Company 3

10.4. Company 4

10.5. Company 5

10.6. Company 6

10.7. Company 7

10.8. Company 8

10.9. Company 9

10.10. Company 10

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Data Center Security Market was valued at USD 18.42 billion in 2024 and is projected to reach a market size of USD 46.10 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 20.14%.

The global data center security market is driven by rising cyber threats and increasing adoption of cloud and hybrid infrastructures.

Based on Type, the Global Data Center Security Market is segmented into Small, Medium, and Large

North America is the most dominant region for the Global Data Center Security Market.

Cisco Systems, Inc., IBM Corporation, Broadcom Inc., Dell Inc. are the leading players in the Global Data Center Security Market.