Global Data Center Power Market Research Report – Segmentation By Component (Solutions, Services), By Data Center Type (Hyperscale, Colocation, Enterprise), By End-Use Industry (IT & Telecom, BFSI, Government, Healthcare, Manufacturing, Others), By Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9893

Format:

Region: Global

Market Size and Overview:

The Global Data Center Power Market was valued at USD 24.56 billion in 2024 and is projected to reach a market size of USD 34.85 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 7.25%.

This expansion is indicative of the fast-rising demand for capacity fueled by edge‑computing deployments, AI/ML workloads, and cloud services, all of which call for resilient power‑distribution systems (PDUs, busways, UPS) and specialized design, integration, and maintenance.

Key Market Insights:

Driven by hyperscalers' need for high‑density, fault‑tolerant power paths, power‐distribution and backup systems (PDUs, UPS, busways) made for approximately 70% of revenue in 2024.

At around 15% CAGR, design consulting and integration services are increasing as expert integrators outsource complex modular and multi‑vendor power installations.

With significant investment in multi‑MW UPS and automated transfer‑switch systems to assist AI clusters and cloud infrastructure, hyperscale installations comprise around 50% of market consumption.

Driven by China and India's cloud-and-5G infrastructure build-outs, APAC is expanding at around 13. 2% CAGR; regional power-capacity reservations surpassing those of North America for the first time in 2024.

Data Center Power Market Drivers:

The recent surge in the deployment of data center capacity is driving the immense growth of this market.

With JLL projecting a 15% CAGR in new build-outs through 2027 and McKinsey anticipating total capacity demand to reach 82 GW by 2025, up sharply from 64 GW, global data-center IT capacity additions have quickened dramatically. Hypercale cloud providers and major corporations enlarging their colocation and edge footprint have fueled operators to order over 30 GW of new IT rack load. Millions of kVA of UPS, PDUs, and overhead busway are needed to ensure racks running 20–30 kW each get dependable, high‑density electricity. Data center designers are embracing modular power-skid solutions, pre-integrated assemblies of UPS, switchgear, and busway, which may be installed in 12–16 weeks to speed expansions and control costs, hence lowering both engineering lead times and site‑work complexity.

The growing need for high levels of redundancy and reliability is driving the demand for this market.

Meeting "five-9s" (99.999%) to "six-9s" (99.9999%) availability targets translates into tolerating less than 10 minutes of downtime per year, a prerequisite for mission-critical cloud, financial-services workloads based on AI, and financial-services workloads. Achieving this level of resilience drives data centers to specify N+1 or 2N UPS architectures, dual-fed PDUs, and automatic transfer switches with sub-10 ms failover times. These redundancy solutions call for substantial CapEx, but the demanding SLA commitments, especially from hyperscalers and BFSI tenants, justify continuing spending in preventative-maintenance contracts, remote-monitoring services, and rapid-response field-service agreements, which together maintain strong revenue growth in both equipment and consulting areas.

The recent rise of edge and micro data centers is also considered a major market driver.

Beyond huge facilities, the edge‑computing wave is driving power‑market demand from micro data centers, compact modules hosting AI inference, CDN caches, and IoT gateways, which are being installed in metro PoPs, campus networks, and industrial sites at around 18% CAGR. Pre-tested offsite for quick field deployment, these edge locations call integrated, skid-mounted power solutions combining UPS, PDUs, and switchgear into single enclosures. To reduce footprint, edge power modules are sometimes used with ambient-cooled batteries or fuel cell backups supporting densities of 2–5 kW per cabinet. For power-system vendors capable of providing turnkey, OPEX-based "power-as-a-service" solutions that fit the speed and scale of modern micro-data-center roll-outs, the edge trend opens fresh income channels.

The mandates regarding energy efficiency and sustainability are also said to drive the growth of this market.

Under corporate net‑zero targets and laws such as the EU's Carbon Border Adjustment Mechanism, data‑center operators are under growing pressure to cut carbon footprints and boost energy efficiency. High‑efficiency online Eco‑mode UPS systems (with up to 99% efficiency), low‑loss copper busway, and dynamic power‑management software throttling power consumption based on real‑time IT loads are being used by facilities aiming for PUE targets under 1.2. Power‑control systems are increasingly combined with behind‑the‑meter renewables, solar canopies, wind turbines, and battery‑energy storage facilities, to facilitate on‑site generation and peak‑shaving. In addition to reducing lifetime operating costs by 15–25%, these sustainable power systems open rewards like renewable energy tax credits and green bond financing, propelling new capex and opex streams in the data-center power market.

Data Center Power Market Restraints and Challenges:

The infrastructure is said to be capital-intensive, which makes this market less affordable.

Deploying modern data‑center power systems calls for tremendous upfront capital. Not including housing, switchgear, or busway installations, high‑efficiency, modular UPS skids rated for 1–2 MW cost USD 1–2 million per MW. Pod‑style power modules, which combine UPS, PDU, and automatic transfer switches, further increase prices when tailored for high‑density AI racks. Most small colocation companies and enterprise IT departments lack the balance‑sheet capacity to absorb such CapEx, hence many postpone required power upgrades or retrofit old infrastructure at the expense of reliability and efficiency. Extended payback terms, sometimes surpassing five years, discourage quick modernization even when finance choices exist; pockets of power risk emerge across the global data-center estate.

The market faces constraints due to volatility and limited grid capacity, which hampers market growth.

Already consuming > 1% of worldwide electricity, data centers' share is rising with the growth of artificial intelligence and cloud workloads. Local networks reach capacity limits in many urban regions; therefore, operators are compelled to negotiate firm‑capacity contracts months in advance or to agree to interruptible‑power agreements at cheaper prices. These approaches call for advanced load-forecasting and risk-management solutions to avoid unexpected curtailments, particularly during high-demand seasons and to hedge erratic spot-market pricing. Data centers have major budget uncertainty where electricity rates soar 100 to 200%, hence increasing investments in on-site production (gensets, fuel cells) and energy-storage systems as insurance against grid stability.

The process of integration with the existing systems is said to be quite complex, which hampers its reach.

Highly modular and multi‑vendor, contemporary power architectures in data centers integrate switchgear, PDUs, busway, UPS systems, and control software from several OEMs. Interoperability issues result from a lack of uniform communication methods; nevertheless, although BMS often speaks BACnet, many power systems utilize SNMP, Modbus, or proprietary APIs. To combine power measures, allow automatic transfer-switch logic, and interface with DCIM systems, custom middleware and extensive control-system changes are needed. Three to six months can be added to commissioning timelines by these unique integration projects; they also increase project management costs and expose single points of failure if not thoroughly evaluated across all interfaces.

The market faces a challenge regarding the shortage of skilled labor that is required for the smooth functioning of the market.

Using and managing sophisticated power systems calls for particular expertise in electrical engineering, power electronics, and control software integration. Still, the data‑center sector has a clear talent shortage: Uptime Institute surveys show that 70% of operators have difficulties finding competent power‑infrastructure staff, with recruitment processes lasting 3–6 months and wage rates up 15–20% owing to competitive poaching. The lack of qualified technicians compels some operators to depend on rare outside contractors, hence scheduling bottlenecks for maintenance and enhancements. The gap between industry need and available expertise threatens to retard critical-power projects and raise operational risk as power-system complexity increases with AI-driven management and hybrid energy integrations.

Data Center Power Market Opportunities:

The emergence of Power as a Service (PaaS) Model is said to transform this market.

By packaging UPS capacity, PDUs, and maintenance into predictable, OPEX-based contracts, subscription-based Power-as-a-Service (PaaS) offers help to relieve the significant up-front CapEx burdens of conventional power procurement. Early adopters report 20% faster capacity on-ramps, as PaaS providers pre-configure modular power skids off-site and provide "plug-and-play" solutions, circumventing drawn-out procurement cycles. With transparent monthly fees encompassing equipment, installation, and service-level guarantees, operators experience predictable five-year Total Cost of Ownership (TCO) and less financing complexity. Smaller colocation companies and edge‑data‑center operators who can match power capacity to real load growth without financial limitations find this model particularly enticing. PaaS is changing to encompass renewable integration and performance-based SLAs as the market develops, therefore establishing it as a basis for flexible, scalable data-center power systems.

The opportunity to integrate with renewable energy and storage gives a boost to the growth of this market.

Resilience and sustainability are being provided to data-center operations by hybrid power architectures including on‑site solar PV, Battery‑Energy Storage Systems (BESS), and utility grid supply. Co-locating solar arrays on rooftops or nearby land enables operators to offset 20–30% of yearly onsite energy consumption; BESS units store extra production for evening or peak-demand use, therefore lowering grid draw and demand charges by up to 30% over 10 years. These combined systems allow participation in grid services markets, such as frequency regulation, generating fresh revenue streams. Advances in controller software now synchronize renewable output, BESS dispatch, and UPS readiness, ensuring smooth transition during outages and supporting corporate net-zero commitments. The installation of renewable and storage systems next to conventional power modules offers a major growth opportunity in the data center power business since their costs keep dropping.

The emergence of power management software that is AI-driven is said to present a good opportunity to the market.

Rising AI/ML‑based power-management solutions maximize load sharing, phase balancing, and equipment dispatch by examining real-time electrical and cooling data over busway, PDUs, and UPS. These systems absorb telemetry, power consumption, voltage, temperature, and use predictive-maintenance models that identify early warning indicators of part deterioration, hence extending equipment lifespans by 15% and avoiding unexpected outages. Additionally, recommending dynamic PDU and busway provisioning to uniformly distribute loads, AI algorithms improve overall power-use efficiency (PUE) and minimize thermal hotspots. AI-driven automation provides a path to leaner O&M teams, cheaper energy bills, and greater reliability, tailoring power delivery to real-time needs while minimizing waste as data centers grow in sophistication, with heterogeneous power infrastructure and varying IT loads.

The microgrid and Islanding capabilities are considered to be major market opportunities.

Advanced microgrid controllers enable data centers relying on behind‑the‑meter generation and BESS to island from the grid seamlessly during outages and maintain 100% uptime. Pilot deployments combining generator sets, solar PV, and battery storage have shown uninterrupted operation during Category 3 storms and grid disturbances, therefore eliminating downtime risks for crucial services. Optimized dispatch algorithms schedule generator run times and battery cycling to reduce fuel expenses by 25% while guaranteeing UPS batteries remain at peak charge levels. Besides increasing resilience, this integrated microgrid architecture lets data centers sell surplus capacity back to utilities under resiliency tariffs. Microgrid-enabled data centers provide a strong chance to stand apart on reliability and sustainability in the cutthroat power market since regulators and customers want greater uptime assurances.

Data Center Power Market Segmentation:

Market Segmentation: By Component

• Solutions

• Services

The Solutions segment is said to dominate this market with approximately 70% of market revenue in 2024 coming from power solutions (PDUs, UPS, busway), as data centers give resilient, fault-tolerant power distribution and backup architectures top priority to help ever-higher rack densities and SLA needs. The Services segment is considered to be the fastest-growing segment. Driven by the complexity of modular power skids, hybrid on-site/edge architectures, and outsourced commissioning requirements, professional services, covering design consulting, system integration, and managed deployments, are expanding at around 15% CAGR.

Market Segmentation: By Data Center Type

• Hyperscale

• Colocation

• Enterprise

The Hyperscale segment dominates this market. Investing heavily in multi‑megawatt UPS systems, automated transfer switches, and high‑density busway to enable AI/ML clusters and worldwide cloud infrastructure, hyperscale data centers use around half of the whole power market capacity. The Enterprise segment is said to be the fastest-growing one. Driven by digital transformation projects and the need to satisfy internal uptime SLAs without complete cloud migration, on-premise enterprise data centers are updating legacy UPS and PDU infrastructure at a 12% CAGR. Favoring flexible power-as-a-service models and OPEX-based contracts to rapidly scale tenant deployments with guaranteed power-density and uptime SLAs, colocation facilities account for the remaining roughly 30%.

Market Segmentation: By End-Use Industry

• IT & Telecom

• BFSI

• Government

• Healthcare

• Manufacturing

• Others

The IT & Telecom segment is said to dominate the market, and the Manufacturing segment is the fastest-growing segment in this market. Leading with around 20% of market income in 2024, the IT and telecoms sector reflects considerable investment in 5G edge compute nodes, network operator PoPs, and cloud service provider campuses that need strong power solutions. Manufacturing, specifically Industry 4.0 smart‐factory implementations, is the fastest-growing sector at roughly 14% CAGR as real-time automation and robotics need highly reliable, low-latency power architectures.

With a share of about 18%, BFSI employs redundant power systems to aid trading platforms, data analytics frameworks, and regulatory compliance infrastructure. Healthcare's share is around 12%, driven by electronic-medical-records storage and critical-care systems needing uninterruptible power for life-safety applications. When it comes to the Government and Public Sector, with constant growth as agencies update ancient facilities and deploy hybrid‑cloud for public services, government data centers account for around a 10% share. With demand linked to e‑commerce back ends and streaming content platforms, other sectors, including retail and media, contribute to the equilibrium.

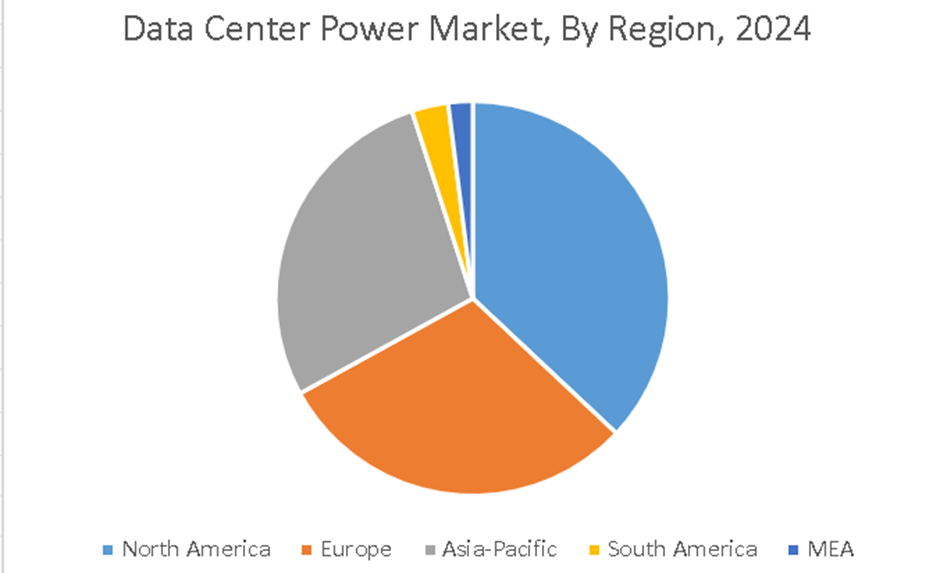

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America is said to lead this market, and the Asia-Pacific region is said to be the fastest-growing region. Driven by the growth of data centers and the need for dependable, efficient power systems, North America leads the data center power solutions market. The development of the Internet of Things (IoT), big data analysis, and cloud computing drives investments in power management solutions in this area. The Asia-Pacific area is seeing fast expansion in the data center power industry, particularly in nations including China, India, and Japan. Driven by digital transformation and growing internet use, the need for effective power infrastructure is spurred by the proliferation of data centers.

Demand for data center power solutions in Europe is high, especially in nations like Germany, the UK, and France. Encouraging the use of sophisticated power solutions in data centers is the focus on energy efficiency, sustainability, and regulatory compliance, like the EU's Green Deal. With rising demand for data center power solutions from companies looking to improve their IT capabilities, the South American market is developing. Though the data center market presents obstacles connected to infrastructure building and economic circumstances, nations such as Brazil and Argentina are starting to invest in it. Organizations striving to boost their operational efficiency are making more data center power solutions investments in the MEA region, which has a lower market share. Future market expansion should be fueled by the development of digital services and government programs designed to advance technology infrastructure.

COVID-19 Impact Analysis on the Global Data Center Power Market:

Lockdowns in 2020–2021 postponed deliveries of essential power equipment and on-site installations by three to four months but also sped demand for digital services, therefore driving a 25% rise in new-build power contracts by late 2021. A 30% rise in managed-service agreements for power-system support resulted from the emphasis on remote monitoring and maintenance during travel bans.

Latest Trends/ Developments:

Power modules intended for direct-to-chip immersion and cold-plate cooling in racks with high-density AI.

Designs influenced by SDN dynamically route power across meshed busway topologies.

Pre‑configured, containerized power modules for quick deployment in edge‑data‑centers and telecom PoPs.

Arrays for backup and UPS are able to toggle between hydrogen fuel cells and diesel for zero-emission resilience.

Key Players:

• Schneider Electric SE

• Eaton Corporation Plc

• Cummins Inc.

• ABB Ltd.

• Vertiv Holdings Co.

• Legrand SA

• Siemens AG

• Raritan Inc.

• Mitsubishi Electric Corp

• Caterpillar Inc.

Chapter 1. Global Data Center Power Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Data Center Power Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Data Center Power Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Data Center Power Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Data Center Power Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Data Center Power Market - By Component

6.1. Introduction/Key Findings

6.2. Solution

6.3. Services

6.4. Y-O-Y Growth trend Analysis By Component

6.5. Absolute $ Opportunity Analysis By Component , 2025-2030

Chapter 7. Global Data Center Power Market– By Data Center Type

7.1 Introduction/Key Findings

7.2. Hyperscale

7.3. Colocation

7.4. Enterprise

7.5. Y-O-Y Growth trend Analysis By Data Center Type

7.6. Absolute $ Opportunity Analysis By Data Center Type, 2025-2030

Chapter 8. Global Data Center Power Market– By End-Use Industry

8.1. Introduction/Key Findings

8.2. IT & Telecom

8.3. BFSI

8.4. Government

8.5. Healthcare

8.6. Manufacturing

8.7. Others

8.8. Y-O-Y Growth trend Analysis By End-Use Industry

8.9. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 9. Global Data Center Power Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Component

9.1.3. By Data Center Type

9.1.4. By End-Use Industry

9.1.5. By Region

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Component

9.2.3. By Data Center Type

9.2.4. By End-Use Industry

9.2.5. By Region

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Component

9.3.3. By Data Center Type

9.3.4. By End-Use Industry

9.3.5. By Region

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Component

9.4.3. By Data Center Type

9.4.4. By End-Use Industry

9.4.5. By Region

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Component

9.5.3. By Data Center Type

9.5.4. By End-Use Industry

9.5.5. By Region

Chapter 10. Global Data Center Power Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Schneider Electric SE

10.2. Eaton Corporation Plc

10.3. Cummins Inc.

10.4. ABB Ltd.

10.5. Vertiv Holdings Co.

10.6. Legrand SA

10.7. Siemens AG

10.8. Raritan Inc.

10.9. Mitsubishi Electric Corp

10.10. Caterpillar Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Data Center Power Market was valued at USD 24.56 billion in 2024 and is projected to reach a market size of USD 34.85 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 7.25%.

Massive IT-load expansions are triggered by the explosive growth in cloud and artificial intelligence workloads, which calls for fresh UPS, PDU, and busway equipment to guarantee uptime and scalability.

Reflecting the fundamental need for resilient power distribution, power solutions, UPS, PDU, and busway held around 70% of the market income in 2024.

Driven by China's and India's investments in cloud and 5 G infrastructure, Asia Pacific is expected to grow at around 13.2% CAGR.

Lockdowns for the pandemic slowed down installations but sped adoption of remote monitoring and managed services, which resulted in a 25% comeback in power contracts by late 2021.