Global Data Center Automation Market Research Report – Segmentation by Offerings (Solutions, Services), Application (BFSI, IT & Telecom, Healthcare, Government), Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-4084

Format:

Region: Global

Market Size and Overview:

The Global Data Center Automation Market was valued at USD 6.8 billion in 2024 and will grow at a CAGR of 14.2% from 2025 to 2030. The market is expected to reach USD 13.21 billion by 2030.

The Data Center Automation Market focuses on automating routine and complex data center operations through software tools and intelligent management platforms. This market includes solutions such as automated provisioning, configuration, patching, monitoring, and workload management. As organizations increasingly rely on cloud services, virtualization, and software-defined infrastructure, the need for automation is growing rapidly. Businesses are aiming to improve efficiency, reduce operational costs, minimize human error, and ensure consistent performance across data center environments. The market is driven by the proliferation of big data, increasing demand for scalable infrastructure, and rising adoption of hybrid cloud strategies. Automation also enables faster time-to-market, improved security, and better resource utilization, making it essential in modern IT strategies. The trend toward digital transformation, coupled with the integration of AI and ML in operations, further accelerates the growth of this market.

Key market insights:

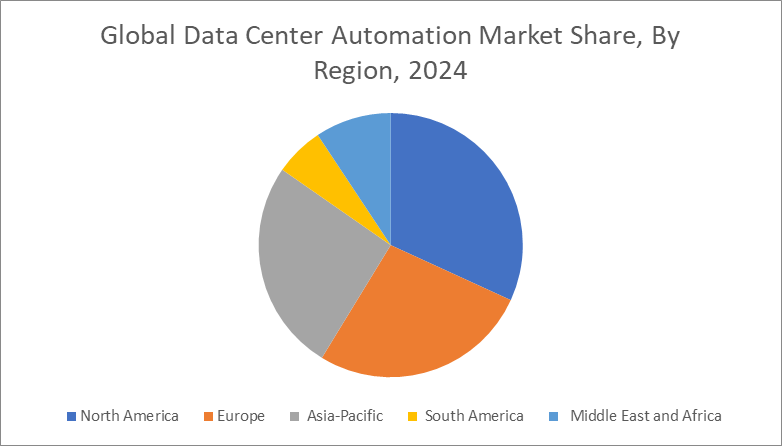

North America held the largest market share of over 35% in 2024, due to the strong presence of key technology players and early adoption of automation technologies.

The IT & telecom sector contributed over 30% of the total market share in 2024, driven by cloud infrastructure expansion and digital service demands.

Solution-based offerings dominated the market with a 60% share in 2024, including tools for configuration management, orchestration, and monitoring.

Hybrid cloud deployment models are expected to grow at a CAGR of 16.5%, driven by flexibility and cost-effectiveness.

AI and ML integration in data center operations saw adoption rise by 27% year-on-year in 2024, streamlining predictive maintenance and fault detection.

Increasing demand for energy-efficient data centers has led to a 22% rise in automation-based cooling and power management solutions.

Global Data Center Automation Market Drivers

Rising demand for scalable IT infrastructure is driving the market growth

With the increasing complexity of IT environments and the explosion of data volumes, enterprises are moving toward highly scalable infrastructure. Traditional manual management methods can no longer meet the speed, scale, or efficiency required by modern digital businesses. Data center automation allows organizations to streamline their processes through centralized control and orchestration. This, in turn, enables faster deployment of resources, improved uptime, and enhanced performance metrics. By automating provisioning, configuration, patching, and monitoring, enterprises can respond quickly to dynamic workload demands. The demand for scalable solutions is particularly high in industries like e-commerce, BFSI, and telecom where traffic and data loads fluctuate significantly. As cloud computing and virtualization further evolve, the need for a more agile and responsive infrastructure grows stronger. Automation becomes the linchpin for delivering services with precision and speed while reducing operational overheads. The scalability offered by automation tools ensures long-term adaptability and sustainability in an increasingly data-driven landscape.

Shift towards hybrid and multi-cloud environments is driving the market growth

Organizations across the globe are adopting hybrid and multi-cloud strategies to improve operational flexibility, reduce dependency on a single vendor, and balance workload placement. However, managing and orchestrating operations across on-premise, public, and private cloud platforms presents challenges related to integration, performance consistency, and cost control. Data center automation solutions address these challenges by providing unified control and visibility across heterogeneous environments. These tools help in automating routine tasks such as deployment, scaling, backup, and disaster recovery while ensuring security compliance. Hybrid architectures also benefit from workload optimization, dynamic resource allocation, and predictive analytics, all powered by automation. As enterprises strive for business continuity and faster innovation cycles, automation provides the necessary agility and resilience. The shift toward hybrid and multi-cloud frameworks is therefore fueling robust growth in the automation market, with increasing investments being made to modernize infrastructure and reduce operational complexity.

Focus on operational efficiency and cost reduction is driving the market growth

Enterprises are under continuous pressure to optimize their IT expenditures while maintaining service quality and operational efficiency. Manual interventions in data centers not only slow down operations but also introduce a higher risk of human error, leading to system downtime or configuration issues. Data center automation helps streamline workflows and eliminate repetitive tasks, thereby increasing overall Offeringsivity. Automation reduces dependency on manual labor and enables standardized procedures that enhance predictability and accuracy. This leads to substantial cost savings in terms of labor, time, and error remediation. Moreover, with the incorporation of AI and analytics, data center operations can become proactive rather than reactive, identifying potential problems before they escalate. Energy management is another area where automation contributes to cost efficiency by optimizing cooling systems, power distribution, and space utilization. As businesses seek to do more with less, the ROI of data center automation becomes increasingly clear, establishing it as a strategic investment for cost-conscious enterprises.

Global Data Center Automation Market Challenges and Restraints

High initial investment and integration complexity is restricting the market growth

While data center automation promises long-term operational and cost benefits, the initial implementation can be expensive and complex. Setting up an automated infrastructure involves investments in software, hardware, training, and ongoing maintenance. For many small and medium-sized enterprises, the upfront cost is a significant deterrent. Additionally, integrating automation tools into existing legacy systems requires careful planning and customization. The lack of standardization across platforms and the wide variety of vendor-specific solutions complicate integration efforts. Compatibility issues and the need to restructure processes and policies add to the complexity. Organizations may also face internal resistance from IT teams due to concerns over job displacement or disruptions in existing workflows. Inadequate expertise and lack of trained personnel further hinder the effective deployment of automation technologies. Thus, while the benefits are evident, the adoption curve can be steep, particularly for organizations with limited resources and legacy-heavy infrastructure.

Security and compliance concerns is restricting the market growth

As automation tools gain control over critical data center functions, security and compliance become paramount concerns. Automated systems handle vast amounts of sensitive data and manage privileged access to infrastructure components. A misconfigured automation script or a software vulnerability can expose systems to significant risks, including data breaches and service outages. Moreover, compliance with regulations such as GDPR, HIPAA, and PCI-DSS adds another layer of complexity. Automation must be designed to align with specific policy requirements and ensure auditable actions across all activities. Organizations must invest in secure coding practices, access controls, encryption, and monitoring tools to safeguard automated environments. Furthermore, real-time oversight and anomaly detection mechanisms are essential to prevent unauthorized actions. As cyber threats evolve in sophistication, automation systems must continuously adapt. While automation offers improved consistency and responsiveness, failure to address security implications can undermine trust and hinder widespread adoption in sensitive industries.

Market Opportunities

The global data center automation market is poised to unlock significant opportunities as digital transformation continues to reshape industries. With organizations increasingly embracing cloud-native infrastructure, DevOps practices, and edge computing, automation has become an enabler of agile IT operations. One major opportunity lies in the adoption of AI-powered automation, which allows data centers to shift from reactive to predictive and autonomous management. This includes real-time optimization of resources, automated root cause analysis, and self-healing systems. The increasing number of hyperscale data centers globally also opens up avenues for automation vendors to provide tailored solutions for orchestration, security, and energy efficiency. Moreover, emerging markets in Asia-Pacific, Latin America, and the Middle East are investing heavily in digital infrastructure, thereby offering fresh growth prospects. Another opportunity exists in sustainability, where automation tools can help reduce energy consumption and carbon footprints through intelligent power management. The proliferation of 5G and IoT further expands the need for highly responsive and decentralized data centers that can only be effectively managed through automation. Vendors who focus on providing customizable, scalable, and secure automation frameworks will find ample growth space across sectors such as finance, healthcare, telecom, and manufacturing. Partnerships between hardware providers and automation software companies will also enhance end-to-end offerings. With the rising importance of business continuity and disaster recovery, automation will become indispensable in minimizing downtime and improving resiliency. Overall, the convergence of advanced technologies, growing enterprise demands, and evolving IT landscapes presents a vibrant and expanding horizon for the data center automation market.

Market segmentation

By Offerings

• Solutions

• Services

In 2024, the solutions segment dominated the data center automation market due to its wide applicability in managing provisioning, orchestration, configuration, and monitoring functions. These tools form the backbone of automated infrastructure and are widely adopted across industries. Solutions help enterprises reduce human dependency, improve uptime, and scale efficiently. As organizations increasingly shift to hybrid and cloud-native setups, automation solutions that support cross-platform orchestration are becoming essential. The demand for integrated platforms with AI and analytics capabilities has further strengthened the growth of this segment.

By Application

• BFSI

• IT & Telecom

• Healthcare

• Government

• Manufacturing

• Retail

• Energy & Utilities

The IT & telecom segment accounted for the largest market share in 2024, driven by the massive demand for digital services, data hosting, and cloud platforms. This sector requires highly available and responsive infrastructure to manage dynamic workloads and high traffic volumes. Automation enables telecom providers to enhance operational agility, reduce latency, and optimize resources. With the ongoing 5G rollout and exponential data growth, this segment is expected to continue driving demand for scalable and intelligent automation frameworks across both core and edge data centers.

Regional segmentation

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America emerged as the leading region in the data center automation market in 2024, capturing over 35% of the total market share. This dominance is attributed to the early adoption of automation technologies, high investment in data infrastructure, and a robust presence of global cloud service providers and tech giants. The region’s digital-first economy, especially in the U.S. and Canada, has accelerated the need for efficient and scalable data centers. Companies in North America are increasingly integrating AI, ML, and analytics into their IT operations, creating favorable conditions for automation vendors. Additionally, stringent data compliance regulations and increasing cyber threats are pushing organizations to adopt automation for enhanced security and resilience. The expansion of hyperscale data centers and edge computing projects in North America further boosts demand for advanced automation solutions. Strong R&D capabilities, availability of skilled professionals, and government support for digital initiatives contribute to sustained regional leadership.

COVID-19 Impact Analysis on the Data Center Automation Market

The COVID-19 pandemic significantly influenced the data center automation market by accelerating the global shift toward digital services, remote operations, and cloud adoption. As businesses adapted to lockdowns and remote work models, the demand for reliable and scalable data infrastructure surged. Data centers experienced increased pressure to maintain uptime and efficiency under changing workloads and constrained human resources. Automation played a crucial role in enabling remote management, reducing the need for on-site personnel, and maintaining business continuity. Organizations invested in automation tools to automate provisioning, monitoring, and patch management, ensuring operational resilience. Additionally, industries such as healthcare, education, e-commerce, and financial services saw an unprecedented rise in online transactions, further pushing the demand for automated infrastructure. Although supply chain disruptions initially delayed some projects, the long-term impact has been positive, with many enterprises fast-tracking their automation strategies. The pandemic served as a catalyst for modernizing IT operations, and even post-COVID, organizations are likely to continue prioritizing automation for its scalability, cost efficiency, and adaptability in uncertain environments.

Latest trends/Developments

The data center automation market is witnessing transformative trends driven by the convergence of AI, cloud-native architectures, and edge computing. One of the most notable developments is the growing adoption of AI-driven automation tools capable of predictive maintenance, workload optimization, and intelligent alerting. These tools enable data centers to move toward self-healing and self-optimizing operations. The rise of infrastructure as code (IaC) is another trend, allowing developers to programmatically manage and automate IT infrastructure. Additionally, software-defined data centers (SDDCs) are becoming mainstream, enhancing flexibility and reducing vendor lock-in. The emergence of edge data centers in support of 5G, IoT, and real-time applications is pushing automation closer to the data source. Sustainability is also taking center stage, with green automation solutions optimizing energy usage and supporting ESG initiatives. Another key development is the increasing collaboration between cloud providers and automation software vendors to offer unified orchestration tools. These innovations, combined with growing demand for cybersecurity automation and compliance management, are shaping a dynamic and rapidly evolving data center automation landscape.

Key Players:

IBM

Cisco

VMware

Microsoft

BMC Software

Hewlett Packard Enterprise

Puppet

Chapter 1. Global Data Center Automation Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Data Center Automation Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Data Center Automation Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Data Center Automation Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porter’s Five Forces Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Power of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Data Center Automation Market – Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Data Center Automation Market – By Offerings

6.1. Introduction/Key Findings

6.2. Solutions

6.3. Services

6.4. Y-O-Y Growth Trend Analysis By Offerings Type

6.5. Absolute $ Opportunity Analysis By Offerings Type, 2025–2030

Chapter 7. Global Data Center Automation Market – By Application

7.1. Introduction/Key Findings

7.2. BFSI

7.3. IT & Telecom

7.4. Healthcare

7.5. Government

7.6. Y-O-Y Growth Trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025–2030

Chapter 8. Global Data Center Automation Market, By Geography – Market Size, Forecast, Trends & Insights

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Offerings

8.1.3. By Application

8.1.4. Countries & Segments – Market Attractiveness Analysis

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Offerings

8.2.3. By Application

8.2.4. Countries & Segments – Market Attractiveness Analysis

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia-Pacific

8.3.2. By Offerings

8.3.3. By Application

8.3.4. Countries & Segments – Market Attractiveness Analysis

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Offerings

8.4.3. By Application

8.4.4. Countries & Segments – Market Attractiveness Analysis

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. United Arab Emirates (UAE)

8.5.1.2. Saudi Arabia

8.5.1.3. Qatar

8.5.1.4. Israel

8.5.1.5. South Africa

8.5.1.6. Nigeria

8.5.1.7. Kenya

8.5.1.8. Egypt

8.5.1.9. Rest of MEA

8.5.2. By Offerings

8.5.3. By Application

8.5.4. Countries & Segments – Market Attractiveness Analysis

Chapter 9. Global Data Center Automation Market – Company Profiles – (Overview, Offerings Portfolio, Financials, Strategies & Developments, SWOT Analysis)

9.1. Cisco Systems, Inc.

9.2. Hewlett Packard Enterprise

9.3. IBM Corporation

9.4. Microsoft Corporation

9.5. VMware Inc.

9.6. BMC Software Inc.

9.7. Fujitsu Ltd.

9.8. Citrix Systems, Inc.

9.9. Dell Technologies Inc.

9.10. Puppet, Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Data Center Automation Market was valued at USD 6.8 billion in 2024 and will grow at a CAGR of 14.2% from 2025 to 2030. The market is expected to reach USD 13.21 billion by 2030.

Key drivers include the demand for scalable infrastructure, hybrid cloud adoption, and operational cost reduction.

Segments include Solutions and Services by Offerings; BFSI, IT & Telecom, Healthcare, Government by application.

North America dominates with the largest market share due to early tech adoption and strong cloud infrastructure.

Key players include IBM, Cisco, VMware, Microsoft, BMC Software, and Hewlett Packard Enterprise