Global Cybersecurity for Autonomous Vehicles Market Research Report – Segmentation By Security Type (Network Security, Endpoint & ECU Security, Identity & Authentication, Data Security, Security Analytics), By Deployment Mode (On-board, Off-board Cloud, Hybrid), By Vehicle Level (Lvl 3, Lvl 4-5), By End-Use (OEM, Tier-1 Suppliers, Fleet Operators), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16540

Format:

Region: Global

Market Size and Overview:

The Global Cybersecurity for Autonomous Vehicles Market was valued at USD 3.3 billion and is projected to reach a market size of USD 12.24 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 29.97%.

The quick adoption of automated and connected vehicles, increasing cyberattacks, particularly on V2X communications, and tough legislative requirements on vehicle and data security all contribute to this growth. Intrusion-prevention ECUs, cryptographic modules, over-the-air (OTA) update security services, and cloud-based threat analytics platforms, designed to protect autonomous-driving systems, infotainment, and telematics from hacking, data breaches, and malware exploits.

Key Market Insights:

With manufacturers including secure-boot and HSMs in ECUs to stop illegal code execution, identity-management and authentication solutions (hardware roots of trust, biometric in-cabins) develop at a 25% CAGR.

Driven by government-backed C-V2X pilot projects in China and South Korea's investments in 5 G-enabled autonomous fleets, APAC commanded around 75%.

Offering OEMs real-time threat-intelligence feeds and OTA-patch-validation features, cloud-off-board security analytics solutions grow at a 24% CAGR.

Cybersecurity for Autonomous Vehicles Market Drivers:

The huge surge in connected and automated fleets is driving the growth of this market.

Each requiring secure communication links between vehicles and cloud backends, OEMs introducing Level 3 conditional‑automation systems in passenger cars and pilot Level 4 shuttles in urban settings, drives this development. Each unit produces terabytes of sensor and V2X data daily as robo‑taxis and autonomous delivery vehicles grow, therefore, strong encryption and intrusion‑detection capabilities are needed to safeguard telemetry and control channels. Early adopters incorporating HSMs into ADAS controllers for cryptographic key storage, tier-1 suppliers are merging secure-boot and hardware-root-of-trust modules into ECUs to stop unlawful firmware changes. Driven by demand for end-to-end security, covering on-board gateways to off-board analytics, fleet operators are fueling expansion in hybrid cybersecurity designs that combine real-time intrusion alerts with cloud-based forensics. Demonstrating scalable V2X protection plans, pilot projects in China have already acquired over 5,000 linked buses using data‑diode architectures to isolate safety‑critical networks from passenger Wi‑Fi. Encrypted DSRC (Dedicated Short‑Range Communications) channels and multi‑factor authentication for distant diagnostic access are among the North American robo‑taxi initiatives in Arizona and California. Cyber‑attack simulations on linked dump trucks in Europe showed that unprotected telematics systems could be seized in less than 90 seconds, emphasizing the need for thorough network‑security modules.

The mandatory compliance with the rules and standards is seen as a great market growth driver.

For all new vehicle kinds from July 2024, UNECE WP.29 (R155/R156) and ISO/SAE 21434 introduced required cybersecurity management system (CSMS) and software‑update‑management‑system (SUMS) requirements, establishing formal procedures for risk assessment and secure development lifecycles. Non-compliance with WP.29 can bar vehicles from type approval in UNECE member nations, therefore forcing OEMs and Tier‑1 suppliers to include early in product design threat‑analysis, vulnerability‑management, and incident‑response processes. ISO/SAE 21434 codifies engineering requirements for cybersecurity risk management over concept, development, manufacturing, operation, and decommissioning phases, therefore lowering residual‑risk levels via organised hazard analysis and countermeasure mapping. NHTSA's updated Cybersecurity Best Practices for Modern Vehicles advises alignment with WP.29 and ISO/SAE⠄21434, hence speeding the adoption of certified security‑engineering methods among U.S. OEMs. European authorities also demand monthly security‑patch reporting for all linked vehicles, which will cause a 45% increase in managed‑OTA‑update‑security subscriptions amongst automakers.

The recent escalation in cyber threats has increased the need for this market, which is a major growth driver.

Adversaries have used wireless interface flaws for spoofing, jamming, and injection attacks, as shown in research hacks of DSRC stacks, when V2X communications allow cars to exchange safety messages and telemetry with infrastructure. Remote disabling of test vehicles by injecting false GPS and sensor data over C‑V2X channels emphasizes the potential for traffic‑manipulation attacks and underlines the need for cryptographic authentication of each message. Denial‑of‑service (DoS) jamming attacks on V2I roadside units have been shown to block critical safety‑priority messages, prompting the development of frequency‑hopping and spread‑spectrum techniques in secure‑gateway designs. Recent black‑hat tests showed how poorly secured mid‑range infotainment Wi‑Fi access points might be used as pivot points to reach V2X and CAN bus segments, therefore highlighting the need for network segmentation and micro‑segmentation strategies. The Automotive ISAC notes a 230% rise in V2X‑related vulnerability disclosures, driving demand for OTA‑delivered security patches and in‑vehicle intrusion‑detection systems (IDS) that monitor CAN bus anomalies. Threat actors have started utilizing certificate‑misissuance via compromised PKI authorities to generate rogue V2X credentials, thus encouraging the deployment of certificate‑revocation‑list (CRL) distribution and online certificate status protocol (OCSP) responders in automotive networks.

The recent shift towards OTA and Software-defined Vehicles is considered a great market growth driver.

The growth of software-defined-vehicle (SDV) architectures, where most vehicle capabilities are implemented in software running on zonal controllers or domain ECUs, depends much on OTA updates for security patches and feature enhancements. Driven by increasing connected‑car numbers and the need to remotely remedy vulnerabilities, the worldwide automotive OTA‑updates market hit USD 3.8 billion in 2023 and is projected to rise at an estimated 17% CAGR through 2032. OTA channels carry great risks, though: unencrypted or unauthenticated update procedures have resulted in proof-of-concept attacks wherein hackers installed dangerous firmware on test cars. Modern SDV platforms include runtime‑integrity monitors that verify key code sections via hash comparisons at boot and periodically in operation, detecting in‑memory tampering attempts, to help reduce these dangers. OTA-security-as-a-service systems that combine vulnerability scanning, cryptographic signing capabilities, and monitoring dashboards for update-delivery health are now available from vendors.

Cybersecurity for Autonomous Vehicles Market Restraints and Challenges:

The market faces a challenge from the complexity of integration with the existing systems.

Modern cars have dozens to hundreds of Electronic Control Units (ECUs) connected via heterogeneous bus architectures, CAN, FlexRay, MOST, Ethernet, and emerging field‑bus protocols, thus making uniform security integration very challenging. Each bus protocol has different timing constraints and payload structures; for instance, CAN lacks built-in encryption or authentication, therefore needing custom lightweight MACs to stop spoofing without breaking real-time deadlines. Automotive Ethernet (IEEE 802.3) introduces packet-based communication and TSN (Time-Sensitive Networking), but incorporating TSN-based E/E architectures with legacy CAN or LIN networks adds protocol-conversion overhead and security flaws. Switching and routing components needed for Ethernet-backbone deployments increase system complexity, therefore necessitating more security functions at each node to check and filter traffic. Resource-constrained MCUs' often-lacking support for developing protocols like TLS-PSK or DTLS calls for hardware updates to execute secure-stack implementations without lag consequences. Network segmentation techniques, such as gateway‑enforced ECUs zones, help restrict lateral movement, but they call for in‑depth mapping of signal flows across buses, which is time-consuming and error-prone. High‑volume, high‑speed bus traffic must be managed by automotive intrusion-detection systems (IDS); studies say that real-time CAN frames processing calls for specialized co‑processors to prevent missing vital anomalies. Resource-constrained MCUs' often-lacking support for developing protocols like TLS-PSK or DTLS calls for hardware updates to execute secure-stack implementations without lag consequences. Network segmentation techniques, such as gateway‑enforced ECUs zones, help restrict lateral movement, but they call for in‑depth mapping of signal flows across buses, which is time-consuming and error-prone. High‑volume, high‑speed bus traffic must be managed by automotive intrusion-detection systems (IDS); vector.com says that real-time CAN frames processing calls for specialized co‑processors to prevent missing vital anomalies.

The certification cost for this market is considered to be very high, affecting the adoption rate of this market.

Formal Cybersecurity Management Systems (CSMS) and Product Security Incident Response Teams (PSIRT) are required under UNECE WP.29 (R155/R156) and ISO/SAE 21434, thus demanding thorough documentation and independent audits. Combined with ISO 26262 functional‑safety alignment, the certification process entails threat‑analysis reports, software‑architecture reviews, and penetration‑testing evidence, costing USD 0.5–1 million per vehicle platform. Smaller OEMs and Tier‑1 suppliers struggle to amortize these fixed costs across lower production volumes, leading many to delay or underfund critical security processes. Worldwide, there are few penetration‑testing facilities approved for automotive scopes, which causes local bottlenecks and inflated costs, sometimes 20–30% more than comparable IT‑sector equivalents. Additionally, every major software update, such as an OTA security patch, calls for re‑validation of cybersecurity certifications, therefore increasing repeated certification costs. Although compliance automation tools can simplify evidence collection, they sometimes lack support for domain‑specific needs such as ECU‑level safety‑integrity measures, hence restricting their usefulness. Consulting fees for automotive-cybersecurity specialists exceed USD 300 per hour since businesses need a specific understanding of AUTOSAR, SAFE‑Lib, and automotive PKI architectures.

The ever-evolving threat landscape poses a big challenge for this market as it would hinder its growth.

Using AI-enhanced tools, threat actors create context-aware phishing attacks against vehicle-owner portals as well as adaptive malware able to change signatures to avoid static-analysis engines. Over-the-air (OTA) update channels integrated into V2X and telematics units are targets for man-in-the-middle (MITM) attacks should cryptographic validation not be strictly enforced. Zero-day vulnerabilities in infotainment-system Linux kernels allow attackers root access, which they next pivot to safety-critical networks via loosely segmented internal gateways. Attackers are now reversing CAN message payloads to mimic vehicle‑control instructions, necessitating the use of app‑layer encryption and message‑authentication codes (MACs) on top of raw CAN frames. Integrating emerging threat‑intelligence feeds for automotive contexts curated by industry ISACs into SIEM systems is required, but correlating domain‑specific indicators presents difficulties. Banks and fleet operators assessing risk include automotive‑cyber threats in their wider corporate risk profiles, therefore spurring cross-industry MDR and threat-hunting service expansion.

The amount of skilled workforce needed for this market is very low, hampering the market’s operational efficiency.

Automotive cybersecurity jobs demand dual skills: deep knowledge of E/E architectures (AUTOSAR, CAN, Ethernet) and IT‑security fields (cryptography, network‑security protocols). Industry surveys reveal that only roughly 10% of cybersecurity experts have direct experience in the automobile domain, which causes rapid learning curves for new hires being onboarded. Universities and vocational programs are just starting to implement curricula covering automotive-cybersecurity standards (ISO/SAE 21434, UNECE WP.29), therefore, graduates have a two- to three-year wait to become fully productive. According to consulting firms, a single platform certification team would require 15–20 specialized engineers, each commanding USD 150–300 per hour, so raising project expenses. Regional talent shortages, especially in APAC beyond major tech hubs, compel corporations to depend on remote-working models, therefore complicating coordination and IP-protection agreements. 5–8% yearly higher pay in the automotive industry for cybersecurity positions than average tech-sector increases causes retention issues, as highly paying fintech and cloud-security companies steal talent.

Cybersecurity for Autonomous Vehicles Market Opportunities:

The growth of V2X Cybersecurity Platforms is seen as a great market growth opportunity.

With a 51.3% CAGR from USD 43 million to USD 778 million by 2030, the worldwide V2X-cybersecurity market is projected to rise, highlighting the need to protect vehicle-to-everything connections against interception and spoofing. OEMs are mandating end-to-end AES-128 and AES-256 encryption on V2V and V2I messages as 5 G-based C-V2X deployments accelerate, hence generating the need for dedicated crypto-gateways inside on-board systems. Major Tier-1 companies like Continental, Qualcomm, and Autotalks are integrating PKI-based authentication systems, enabling real-time issuance and withdrawal of V2X certificates, therefore averting rogue-node participation. The V2X market in Europe alone is projected to reach USD 168 million by 2030, at 41.7% CAGR, driven by urban-mobility pilots requiring high-assurance message integrity. Encouraged by government-backed C-V2X trials, cryptographic attestation of roadside units (RSUs) has boosted local security-platform sales by 60% in 2024 in China. Over 5 million connected vehicles in North America will employ secure‑V2X solutions by 2028, therefore driving the growth of managed certificate‑lifecycle services and OTA key rotations, a feature insurers find useful in underwriting autonomous‑fleet policies. Traffic‑pattern baselining is used by anomaly‑detection modules in security platforms now to flag unusual V2X packets.

The recent emergence of Hardware-Root-Of-Trust and HSMs is considered a major market opportunity.

Highlighting growing demand for hardware-anchored security, the worldwide automobile HSM market increased from USD 1.5 billion to an estimated USD 4.2 billion at a 15.2% CAGR by 2030. Automakers employ secure, immutable boot‑chains anchored in tamper‑resistant HSM IP to guarantee secure‑boot across zonal controllers and essential ECUs. Multiple Tier‑1s have licensed Rambus's ISO 26262 ASIL‑B–certified RT‑640 HSM IP, which includes TRNG, DPA‑resistant ciphers, and glitch‑detection, for next‑gen SoCs. ETAS and Rambus's integrated iHSM‑64x solution combines ESCRYPT CycurSoC firmware with the RT‑64x root‑of‑trust IP, offering open interfaces (SHE+, AUTOSAR) on RISC‑V architectures. Academic assessments confirm that hardware‑protected security anchors reduce tampering risk by >90% relative to software‑only approaches, therefore supporting premium chip‑pricing. HSM‑backed key‑management modules enable safe V2X certificate storage and OTA‑update signature verification, therefore streamlining compliance with UNECE WP.29 R155 criteria. Immutable and certifiable roots of trust allow for strong chain-of-trust systems across boot ROM to application layers. Leading MCU providers (Renesas, NXP) now incorporate silicon HSM blocks with vendor-supported firmware stacks (veSHM, CycurHSM), speeding OEM acceptance. Reflecting the value of ASIL-B approvals, the integrated HSM modules command ASPs 20–25% greater than those of non‑certified security components.

The use of AI-based intrusion detection has helped the market to develop further, being a great market growth opportunity.

Using SVM, Decision Tree, and KNN models, ML-driven intrusion-detection systems (IDS) customized for automotive bus traffic attain >98% detection rates in field tests against CAN-bus spoofing and DoS attacks. Showing viability in real‑world scenarios, recent research by Sharmin et al. reveals that deep‑learning IDS using LSTM autoencoders can detect zero‑day CAN‑bus intrusions with 99.99% accuracy and 0.016% false‑alarm rates. Graph‑ML techniques model CAN‑bus frames as message‑sequence graphs, increasing masquerade‑attack detection by 25% over pure statistical methods on the ROAD dataset. Scalable IDS systems based on graph convolutional networks detect mixed attacks in real time, outperforming baseline IDS with 5–10% greater precision and recall. Open‑access datasets (ROAD, car‑hacking challenge) underpin cross‑vendor benchmarking, enabling vendors to validate ML‑IDS performance on varied attack patterns. ML‑IDS modules are now offered as microservices on zonal‑controller OS stacks, isolating security analytics workloads from critical real‑time control loops. Embedded in ECUs, edge‑AI accelerators process bus traffic at line rates (up to 10⠁Mbps for CAN‑FD), therefore ensuring sub-millisecond anomaly detection without affecting safety‑critical tasks.

The use of managed security services for fleets is seen as an opportunity for the market to enhance its operations.

Lacking internal cybersecurity knowledge, fleet operators, particularly robo‑taxi and autonomous‑delivery services, are driving an 18.3% CAGR rise in MDR and SIEM‑as‑a‑service offerings designed for vehicle telemetry monitoring. By 2025, Gartner expects 50% of businesses (including huge fleets) will use MDR services, thereby outsourcing 24×7 threat hunting, incident response, and forensics to specialized SOC teams. Tier‑1 cybersecurity vendors (Airbus Protect, CrowdStrike) now provide "Cyber‑Fleet MDR" bundles combining V2X‑traffic analysis, ECU‑log intake, and incident‑playbook orchestration. These services eat CAN, Ethernet, and sensor-bus logs via edge agents, forwarding normalized events to cloud SIEMs for correlation with global threat feeds, a capability MSSPs historically lacked. Targeted to SMEs, MDR tiers range from USD 50–150 per vehicle per month, which is a fraction of per-unit in-house SOC staffing expenses; therefore, accessible for mid-sized fleet operators. Providers integrate virtual CISO (vCISO) consultations, compliance-report automation (WP.29 evidence packs), and phishing-simulation campaigns to strengthen remote-operator portals. Managed-SIEM offerings add user-behavior analytics (UBA) for portal-access monitoring, therefore lowering unauthorized-access events by 30% in pilot fleets. Global MDR vendors are creating automotive-focused SOC centers, staffed with CEH, CISSP, and ISO/SAE 21434 specialists, to give domain-aware threat analysis. This shift to outside security allows fleet operators to concentrate on core operations, route optimization, and vehicle maintenance, while ensuring continuous cybersecurity posture management.

Cybersecurity for Autonomous Vehicles Market Segmentation:

Market Segmentation: By Security Type

• Network Security

• Endpoint & ECU Security

• Identity & Authentication

• Data Security

• Security Analytics

The Network Security segment dominates the market, accounting for around 42% of income. V2X and intra-vehicle communications are protected via safe gateways, cryptography, and intrusion prevention. The Identity & Authentication segment is the fastest-growing segment, it includes hardware roots of trust, HSM integration, and biometric cabin‑access controls; projected CAGR around 25% as manufacturers meet ISO/SAE 21434 and UNECE WP.29.

When it comes to the Endpoint & ECU Security segment, securely boot, anomaly-detection software, and firewall-enabled microcontrollers provide for individual ECUs and in-vehicle endpoints, therefore accounting for somewhat 20% of the market. The Data Security segment contributes around 18% of the market as data-privacy rules tighten. Cloud-based threat intelligence and behavioral analytics systems that process vehicle telemetry for anomaly detection hold about a 10% share but are expanding as fleets need real-time insights.

Market Segmentation: By Deployment Mode

• On-board

• Off-board Cloud

• Hybrid

The On-board segment is said to dominate the market with the highest market share of around 50%, which is due to zero-latency protection. The Off-board Cloud segment is the fastest-growing segment of the market, as OEMs use scalable off-board processing for fleetwide monitoring, cloud-hosted analytics, OTA-security services, and threat-intelligence feeds grow at roughly 24% CAGR. The Hybrid segment is favored for balanced latency and processing efficiency, hybrids, that is, on-board controls with cloud intelligence, such as edge‑AI intrusion detection, supplying central SIEM, account for around 30% share.

Market Segmentation: By Vehicle Level

• Lvl 3

• Lvl 4-5

The Lvl 3 segment dominates this market, prioritized for first security investments in sophisticated driver-assist systems (ADAS), SAE Level 3 (conditional automation) cars make up about 60% of all deployments. The Lvl 4-5 segment is said to be the fastest-growing segment of the market, growing at around 30% CAGR as commercial testing and robo‑taxi services scale, full autonomy (Levels 4–5) solutions call for strong end-to-end security.

Market Segmentation: By End-Use

• OEM

• Tier-1 Suppliers

• Fleet Operators

The OEM segment is said to be the dominant segment of the market. Original Equipment Manufacturers (OEMs) account for nearly 45% of market spend, embedding cybersecurity during vehicle design under regulatory mandates. The Fleet Operators segment is the fastest-growing segment, driven by about 28% CAGR in fleet-focused cybersecurity services, and autonomous fleet operators (e.g., robo-taxis, delivery robots) are outsourcing security to managed-service companies. Tier‑1 suppliers provide OEMs with secure ECUs, gateways, and software stacks with around a 30% share in the market.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

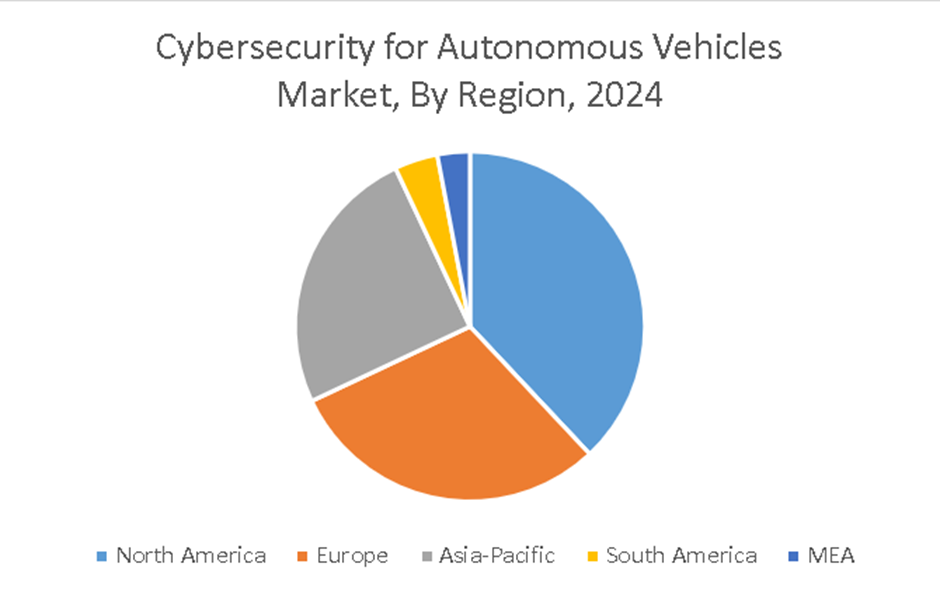

North America is said to lead this market with the highest market share. Driven by substantial investments in autonomous car technology, a strong presence of automakers, and an emphasis on assuring safety and security in linked cars. The Asia-Pacific region is the fastest-growing region. Accelerated expansion of the automotive industry, increasing investments in intelligent transportation solutions, and government policies to support autonomous vehicle development, particularly in nations like China and Japan, drive quick growth.

Strong growth in Europe arises from tight legal standards for vehicle safety, rising uptake of autonomous driving technology, and partnerships between automotive and cybersecurity companies. South America is an emerging market with development potential as governments and automobile manufacturers start to see the need for cybersecurity in the advancement of autonomous vehicles. The MEA region is considered to be a smaller market size, yet increased interest in cybersecurity products for autonomous vehicles as the area updates its transportation infrastructure and raises vehicle safety.

COVID-19 Impact Analysis on the Global Cybersecurity for Autonomous Vehicles Market:

The pandemic accelerated interest in autonomous delivery and contactless mobility solutions, prompting pilot deployments of Level 4 shuttles and eVTOL air taxis in 2020–2021. Supply-chain disruptions, however, delayed semiconductor deliveries, critical for secure ECUs by 4 to 6 months, are postponing some cybersecurity Integrations. Lockdowns also limited vehicle penetration testing and OTA update trials, slowing WP.29 certification schedules by up to 12 months. On the other hand, remote-operated fleet-monitoring services saw a 35% increase, which increased demand for cloud-based security analytics solutions.

Latest Trends/ Developments:

Release of 3GPP Rel-16 specifications for LTE-V2X and 5 G-NR V2X includes built-in encryption and authentication primitives, prompting chipset vendors to integrate secure PHY/MAC layers.

Automotive HSM Standardization: The recently released ISO 23837 standard sets out automotive HSM criteria, therefore hastening acceptance of certified crypto-modules in ECUs.

Cross-industry cyber ranges simulating large-scale vehicle-network assaults improve readiness for mass-deployment situations through collaborative initiatives including OEMs, Tier-1s, and governmental organizations.

Specialized OTA-security-as-a-service platforms that include signed-firmware provisioning, automatic vulnerability assessments, and rollback protection have emerged.

Key Players:

• Trillium Secure, Inc.

• Cisco Systems, Inc.

• Argus Cuber Security

• Symantec Corporation

• GuardKnox

• Upstream Security

• HARMAN International

• Trend Micro

• SafeRide Technologies

• Karamba Security

Chapter 1. Global Cybersecurity for Autonomous Vehicles Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Cybersecurity for Autonomous Vehicles Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Cybersecurity for Autonomous Vehicles Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Cybersecurity for Autonomous Vehicles Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Cybersecurity for Autonomous Vehicles Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Cybersecurity for Autonomous Vehicles Market– By Security Type

6.1. Introduction/Key Findings

6.2. Network Security

6.3. Endpoint & ECU Security

6.4. Identity & Authentication

6.5. Data Security

6.6. Security Analytics

6.7. Y-O-Y Growth trend Analysis By Security Type

6.8. Absolute $ Opportunity Analysis By Security Type, 2025-2030

Chapter 7. Global Cybersecurity for Autonomous Vehicles Market– By Deployment Mode

7.1 Introduction/Key Findings

7.2. On-board

7.3. Off-board Cloud

7.4. Hybrid

7.5. Y-O-Y Growth trend Analysis By Deployment Mode

7.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global Cybersecurity for Autonomous Vehicles Market– By Vehicle Level

8.1. Introduction/Key Findings

8.2. Lvl 3

8.3. Lvl 4-5

8.4. Y-O-Y Growth trend Analysis By Vehicle Level

8.5. Absolute $ Opportunity Analysis By Vehicle Level, 2025-2030

Chapter 9. Global Cybersecurity for Autonomous Vehicles Market– By End-Use

9.1. Introduction/Key Findings

9.2. OEM

9.3. Tier-1 Suppliers

9.4. Fleet Operators

9.5. Y-O-Y Growth trend Analysis By End-Use

9.6. Absolute $ Opportunity Analysis By End-Use, 2025-2030

Chapter 10. Global Cybersecurity for Autonomous Vehicles Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Security Type

10.1.3. By Deployment Mode

10.1.4. By Vehicle Level

10.1.5. By End-Use

10.1.6 By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Security Type

10.2.3. By Deployment Mode

10.2.4. By Vehicle Level

10.2.5. By End-Use

10.2.6. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Security Type

10.3.3. By Deployment Mode

10.3.4. By Vehicle Level

10.3.5. By End-Use

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Security Type

10.4.3. By Deployment Mode

10.4.4. By Vehicle Level

10.4.5. By End-Use

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Security Type

10.5.3. By Deployment Mode

10.5.4. By Vehicle Level

10.5.5. By End-Use

10.5.6. By Region

Chapter 11. Global Cybersecurity for Autonomous Vehicles Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Trillium Secure, Inc.

11.2. Cisco Systems, Inc.

11.3. Argus Cuber Security

11.4. Symantec Corporation

11.5. GuardKnox

11.6. Upstream Security

11.7. HARMAN International

11.8. Trend Micro

11.9. SafeRide Technologies

11.10. Karamba Security

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Cybersecurity for Autonomous Vehicles Market was valued at USD 3.3 billion and is projected to reach a market size of USD 12.24 billion by the end of 2030 with a CAGR of 29.97%.

The Network Security segment is said to dominate the market with around 35% market share, and the Identity & Authentication segment is the fastest-growing segment of the market.

OEMs must include cybersecurity-management systems and product-security procedures under UNECE WP.29 and ISO/SAE 21434, hence spurring early-stage integrations and standards compliance.

Asia Pacific is said to be the fastest-growing region for this market, driven by South Korean and Chinese C-V2X pilot projects and fast autonomous-fleet deployments.

High WP.29 certification costs (USD 0.5–1 million per platform), integration with legacy ECUs, and a dearth of specialized automotive-cybersecurity talent can extend time-to-market and raise development budgets.