Cyber Insurance Market Research Report – Segmentation by Type (Data Breach Coverage, Network Security Liability, Media Liability, Network Business Interruption, Cyber Extortion Coverage, Regulatory Defense Coverage, Technology Errors & Omissions); By Distribution Channel (Direct Writers, Retail Brokers, Wholesale Brokers, Managing General Agents (MGAs), Digital Platforms, Embedded Insurance Programs); By Organization Size (Enterprise (>5,000 employees), Large Business (1,000-5,000 employees), Mid-Market (250-999 employees), Small Business (50-249 employees), Micro Business (<50 employees)); By Industry Vertical (Financial Services, Healthcare, Retail, Manufacturing, Professional Services, Technology, Education, Public Sector, Critical Infrastructure, Media & Entertainment); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16536

Format:

Region: Global

Market Size and Overview:

The Cyber Insurance Market was valued at USD 22.66 Billion in 2024 and is projected to reach a market size of USD 69.43 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 25.1%.

The cyber insurance landscape has transformed dramatically in 2024, evolving from a niche offering into an essential risk management tool for organizations across all sectors. As digital transformation accelerates and cyber threats proliferate with unprecedented sophistication, businesses increasingly recognize cyber insurance as a critical component of their security framework rather than merely a discretionary safeguard. The market has matured significantly, with insurers developing more nuanced underwriting methodologies and tailoring coverage options to address the complex and ever-evolving nature of cyber risks. Particularly noteworthy is the shift from reactive coverage models primarily focused on breach response to more comprehensive frameworks encompassing preventative services, including threat intelligence, vulnerability assessments, and security awareness training.

Key Market Insights:

Small and medium enterprises now account for 47% of all cyber insurance policies issued, indicating growing awareness among businesses that previously considered themselves too small to be targeted.

Premium increases have moderated to an average of 15% in 2024, down from the dramatic 28% increases observed in 2023, suggesting a stabilizing market after years of volatility.

Ransomware incidents trigger approximately 31% of all cyber insurance claims, maintaining their position as the predominant threat vector despite enhanced security measures and awareness.

The average cost of a data breach has escalated to $4.85 million globally, with regulated industries such as healthcare experiencing significantly higher costs at $10.2 million per incident.

Policy limits have increased substantially, with 35% of large enterprises now carrying coverage exceeding $25 million, while deductibles have risen by an average of 22% as insurers attempt to balance risk exposure.

Standalone cyber policies represent 68% of the market, continuing to outpace packaged or bundled offerings as organizations seek specialized and comprehensive coverage options.

The insurance-to-value ratio remains problematic, with studies indicating that 73% of businesses are underinsured relative to their actual cyber risk exposure.

Market Drivers:

Escalating Cyber Threat Landscape

The unprecedented sophistication and frequency of cyber attacks serve as the primary catalyst driving cyber insurance adoption across all business sectors in 2024. Organizations face an increasingly professionalized adversary ecosystem, with threat actors operating structured enterprises complete with specialized roles, technical support teams, and service-level agreements for their criminal clientele. Ransomware-as-a-Service platforms have democratized advanced attack capabilities, enabling less sophisticated actors to execute complex operations against vulnerable targets. The average dwell time—the period attackers remain undetected within compromised networks—has shortened to just 11 days, reflecting the accelerated monetization strategies employed by modern threat actors. This compressed attack timeline limits defenders' opportunities to detect and mitigate breaches before significant damage occurs. Particularly concerning is the evolution toward destructive attacks targeting operational technology environments, with potential consequences extending beyond data compromise to physical infrastructure disruption. These developments have fundamentally altered organizational risk calculations, transforming cyber insurance from a discretionary purchase into an essential component of comprehensive risk management strategies, especially as traditional security measures prove increasingly inadequate against determined and well-resourced adversaries.

Regulatory and Compliance Requirements

The global regulatory landscape has become an increasingly powerful driver of cyber insurance adoption, with new and strengthened data protection frameworks imposing substantial compliance obligations and financial penalties. Organizations face a complex patchwork of regulations across jurisdictions, including the implementation of comprehensive state-level privacy laws in California, Virginia, Colorado, Connecticut, and Utah, supplementing existing federal regulations. The extraterritorial reach of regulations like the EU's General Data Protection Regulation continues to influence global operations, with potential fines reaching 4% of annual global revenue. Mandatory breach notification requirements have expanded to cover more organizations and data types, increasing both compliance complexity and potential liability. Securities and Exchange Commission rules now mandate disclosure of material cybersecurity incidents for publicly traded companies, elevating cyber risk management to board-level concern. Regulatory investigations following incidents typically extend 12-18 months beyond the breach itself, creating prolonged financial uncertainty that organizations seek to mitigate through insurance coverage. These converging regulatory pressures have transformed cyber insurance from a voluntary risk transfer mechanism into an essential component of regulatory compliance strategies, with policies increasingly structured to address specific notification requirements, regulatory defense costs, and potential penalties.

Market Restraints and Challenges:

The cyber insurance market faces significant challenges despite its growth trajectory. Accurately quantifying cyber risk remains problematic, with limited historical data and rapidly evolving threat landscapes complicating actuarial models. Systemic risk concerns persist, particularly regarding widespread attacks exploiting common vulnerabilities across multiple policyholders simultaneously. Insurers struggle to develop sustainable pricing models that balance affordability with profitability while accounting for catastrophic loss scenarios. The dynamic nature of cyber threats requires continuous adaptation of underwriting criteria and coverage terms, creating market inconsistency and customer confusion about protection scope.

Market Opportunities:

Emerging opportunities in the cyber insurance market include developing specialized coverage for operational technology environments and critical infrastructure, particularly as cyber-physical attacks increase in frequency. The integration of cybersecurity services with insurance products offers promising growth avenues, with insurers uniquely positioned to leverage claims data for developing effective risk mitigation services. Parametric insurance structures represent an innovative approach to coverage, providing predefined payouts based on objective triggers rather than traditional indemnification models. Microinsurance products targeting small businesses with streamlined underwriting and affordable premiums could significantly expand market penetration among historically underserved segments.

Market Segmentation:

Segmentation by Type:

• Data Breach Coverage

• Network Security Liability

• Media Liability

• Network Business Interruption

• Cyber Extortion Coverage

• Regulatory Defense Coverage

• Technology Errors & Omissions

Data breach coverage maintains its position as the dominant cyber insurance type, accounting for approximately 42% of premium volume in 2024. This coverage addresses the substantial costs associated with data compromise incidents, including forensic investigation, notification expenses, credit monitoring services, and regulatory penalties. Its dominance reflects the continued prevalence of data-focused breaches and the maturity of this coverage type, which has benefited from extensive claims data enabling more precise underwriting. Organizations primarily seek this coverage due to regulatory requirements mandating specific response protocols following personal data compromises.

Network business interruption coverage has emerged as the fastest-growing segment, expanding at nearly triple the market average as organizations increasingly recognize operational disruption as their primary cyber risk concern. This coverage specifically addresses revenue losses and extra expenses stemming from system outages, whether caused by malicious attacks or technical failures. The segment's growth reflects the evolution of cyber-attacks beyond data theft toward operational disruption, particularly through ransomware and wiperware targeting critical business systems. Organizations increasingly value this coverage for its direct impact on financial performance protection rather than just compliance requirements.

Segmentation by Distribution Channel:

• Direct Writers

• Retail Brokers

• Wholesale Brokers

• Managing General Agents (MGAs)

• Digital Platforms

• Embedded Insurance Programs

Retail brokers maintain their dominance in cyber insurance distribution, accounting for 58% of premium placement in 2024. Their market leadership stems from the complexity of cyber insurance products requiring substantial expertise to match client needs with appropriate coverage options. Businesses particularly value the advisory role these brokers provide in navigating evolving underwriting requirements and implementing risk control measures necessary to secure favourable terms. The increasing integration of risk management services with insurance products further strengthens the broker's position as they help clients access and implement these value-added offerings.

Digital platforms represent the fastest-growing distribution channel for cyber insurance, experiencing 87% year-over-year growth as streamlined application processes and algorithmic underwriting reduce traditional friction points. These platforms excel in serving small and microbusinesses seeking standardized coverage with minimal complexity and immediate binding capabilities. Their growth reflects the market's response to previously underserved segments where traditional distribution channels proved economically unviable due to relatively low premiums. The integration of automated risk scanning tools further enhances these platforms' value proposition by providing instant security assessments during the quotation process.

Segmentation by Organization Size:

• Enterprise (>5,000 employees)

• Large Business (1,000-5,000 employees)

• Mid-Market (250-999 employees)

• Small Business (50-249 employees)

• Micro Business (<50 employees)

Enterprise organizations dominate cyber insurance premium volume, contributing 38% of total market value despite representing just 7% of policyholders. Their premium dominance stems from substantially higher coverage limits, typically exceeding $50 million for comprehensive programs addressing their complex risk profiles. These organizations typically implement multi-layered insurance strategies combining primary policies with excess layers and specialized coverages addressing industry-specific exposures. The long-term relationships between enterprise clients and insurers have created more stable pricing dynamics in this segment compared to other market sectors experiencing greater volatility.

Small Business segment exhibits the most rapid growth in cyber insurance adoption, expanding 62% year-over-year as awareness of cyber vulnerability increases and more accessible insurance options emerge. This growth reflects the democratization of cyber insurance through simplified underwriting processes, standardized policy forms, and more affordable premium structures specifically designed for smaller organizations. Insurers have successfully leveraged technology to reduce acquisition costs for this segment, enabling profitable operations despite lower individual premium values. Industry association programs and chamber of commerce partnerships have proven particularly effective in expanding small business coverage through trusted distribution channels.

Segmentation by Industry Vertical:

• Financial Services

• Healthcare, Retail

• Manufacturing

• Professional Services

• Technology

• Education

• Public Sector

• Critical Infrastructure

• Media & Entertainment

Financial services retain their position as the dominant industry vertical in cyber insurance consumption, accounting for 27% of global premium volume. This sector's prominence stems from its extensive digital transformation initiatives creating expansive attack surfaces, combined with its position as a high-value target for financially motivated threat actors. Regulatory oversight intensifies the importance of cyber insurance for financial institutions, with specific requirements governing data protection, incident response capabilities, and third-party vendor management. The sector typically maintains the highest average coverage limits, reflecting both substantial risk exposure and greater financial resources allocated to comprehensive risk management programs.

Manufacturing has emerged as the fastest-growing industry vertical for cyber insurance adoption, expanding 74% year-over-year as operational technology environments increasingly connect to business networks and the internet. This convergence creates novel risk exposures as previously isolated industrial control systems become vulnerable to cyber-attacks capable of disrupting physical production processes. The growth reflects a fundamental shift in manufacturing risk profiles, with cyber threats now potentially impacting worker safety, product quality, and supply chain reliability beyond traditional information security concerns. The sector's increasing adoption of IoT technologies further accelerates coverage demand as connected devices multiply across production environments.

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

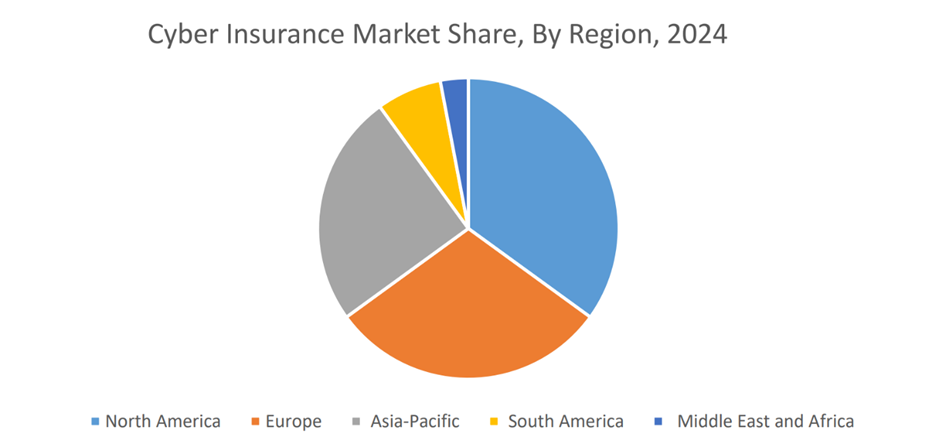

North America maintains its commanding position in the global cyber insurance market with 63% market share in 2024, built upon its early adoption advantage and sophisticated regulatory environment. The region benefits from the most extensive historical claims data, enabling more refined underwriting practices and product innovation compared to emerging markets. Particularly significant is the contribution of the U.S. healthcare sector, where HIPAA compliance requirements and high breach costs drive robust coverage demand. The region also demonstrates the highest penetration among small and medium enterprises, reflecting successful market education efforts and more accessible products designed specifically for this segment.

The Asia-Pacific region exhibits remarkable growth in cyber insurance adoption, expanding 46% year-over-year as digital transformation initiatives accelerate and regulatory frameworks mature across developing economies. This growth stems primarily from dramatic uptake in previously underpenetrated markets including India, Indonesia, and Vietnam, where increasing connectivity creates new vulnerabilities for businesses historically less focused on cybersecurity. Financial services and retail organizations lead adoption trends, particularly as e-commerce platforms expand rapidly throughout the region. Notably, regional insurers are increasingly developing localized products addressing specific regulatory environments rather than simply adopting Western policy structures, creating more relevant coverage options for local business conditions.

COVID-19 Impact Analysis:

The pandemic catalyzed permanent structural changes in the cyber insurance market, with remote work environments dramatically expanding attack surfaces and accelerating digital transformation initiatives. Claim frequency increased significantly across all business segments as organizations hastily implemented remote access solutions without adequate security controls. Underwriting practices evolved in response, with insurers now placing greater emphasis on remote work security protocols, cloud configuration assessments, and distributed workforce training programs. The pandemic permanently altered risk evaluation frameworks, with physical location security becoming less relevant compared to logical access controls and endpoint protection capabilities.

Latest Trends and Developments:

The integration of artificial intelligence into underwriting processes represents a transformative trend, enabling more dynamic risk assessment through continuous monitoring rather than point-in-time evaluations. Parametric cyber insurance structures are gaining traction for specific scenarios like distributed denial of service attacks, offering predefined payouts based on objective triggers rather than complex claims adjustments. Coverage options increasingly address reputational damage through dedicated sublimits for crisis communications and brand rehabilitation following publicized incidents. The industry demonstrates growing sophistication in quantifying business interruption exposures through detailed business impact analyses prior to binding coverage, enabling more tailored protection for operational disruption scenarios.

Key Players in the Market:

• AON Plc

• American International Group, Inc.

• Allianz Group

• Berkshire Hathaway

• Lockton Companies, Inc.

• The Chubb Corporation

• Munich Re Group

• XL Group Ltd.

• Zurich Insurance Co. Ltd.

Chapter 1. Global Cyber Insurance Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Cyber Insurance Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Cyber Insurance Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Cyber Insurance Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Cyber Insurance Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Cyber Insurance Market – By Type

6.1. Introduction/Key Findings

6.2. Data Breach Coverage

6.3. Network Security Liability

6.4. Media Liability

6.5. Network Business Interruption

6.6. Cyber Extortion Coverage

6.7. Regulatory Defense Coverage

6.8. Technology Errors & Omissions

6.9. Y-O-Y Growth trend Analysis By Type

6.10. Absolute $ Opportunity Analysis By Type, 2024-2030

Chapter 7. Global Cyber Insurance Market – By Distribution Channel

7.1. Introduction/Key Findings

7.2. Direct Writers

7.3. Retail Brokers

7.4. Wholesale Brokers

7.5. Managing General Agents (MGAs)

7.6. Digital Platforms

7.7. Embedded Insurance Programs

7.8. Y-O-Y Growth trend Analysis By Distribution Channel

7.9. Absolute $ Opportunity Analysis By Distribution Channel, 2024-2030

Chapter 8. Global Cyber Insurance Market – By Organization Size

8.1. Introduction/Key Findings

8.2. Enterprise (>5,000 employees)

8.3. Large Business (1,000-5,000 employees)

8.4. Mid-Market (250-999 employees)

8.5. Small Business (50-249 employees)

8.6. Micro Business (<50 employees)

8.7. Y-O-Y Growth trend Analysis By Organization Size

8.8. Absolute $ Opportunity Analysis By Organization Size, 2024-2030

Chapter 9. Global Cyber Insurance Market – By Industry Vertical

9.1. Introduction/Key Findings

9.2. Financial Services

9.3. Healthcare

9.4. Retail

9.5. Manufacturing

9.6. Professional Services

9.7. Technology

9.8. Education

9.9. Public Sector

9.10. Critical Infrastructure

9.11. Media & Entertainment

9.12. Y-O-Y Growth trend Analysis By Industry Vertical

9.13. Absolute $ Opportunity Analysis By Industry Vertical, 2024-2030

Chapter 10. Global Cyber Insurance Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Distribution Channel

10.1.4. By Organization Size

10.1.5. By Industry Vertical

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Distribution Channel

10.2.4. By Organization Size

10.2.5. By Industry Vertical

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Type

10.3.3. By Distribution Channel

10.3.4. By Organization Size

10.3.5. By Industry Vertical

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Distribution Channel

10.4.4. By Organization Size

10.4.5. By Industry Vertical

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Distribution Channel

10.5.4. By Organization Size

10.5.5. By Industry Vertical

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Cyber Insurance Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. AON Plc

11.2. American International Group, Inc.

11.3. Allianz Group

11.4. Berkshire Hathaway

11.5. Lockton Companies, Inc.

11.6. The Chubb Corporation

11.7. Munich Re Group

11.8. XL Group Ltd.

11.9. Zurich Insurance Co. Ltd

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary factors driving the growth of the Cyber Insurance Market include the escalating cyber threat landscape characterized by increasingly sophisticated and frequent attacks from professionalized adversary ecosystems.

The main concerns about the Cyber Insurance Market center around the challenges in accurately quantifying cyber risk due to limited historical data and rapidly evolving threat landscapes that complicate actuarial models.

Key players include AIG, Chubb, Beazley, AXA XL, Munich Re, Allianz, CNA Financial, The Hartford, Hiscox, Liberty Mutual, Travelers, Zurich Insurance Group, Coalition, At-Bay, and Cowbell Cyber.

North America currently holds the largest market share, estimated around 35%.

Asia-Pacific has shown significant room for growth in specific segments.