Global Custom Software Development Market Research Report – Segmentation By Type (Web-based Solutions, Mobile Applications, Enterprise Software), By Deployment Mode (Cloud-based, On-premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Industry (BFSI, Healthcare, IT & Telecom, Manufacturing, Retail, Government, Education, Others), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16535

Format:

Region: Global

Market Size and Overview:

The Global Custom Software Development Market was valued at USD 52.84 billion in 2024 and is projected to reach a market size of USD 146.36 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.6%.

Businesses seeking digital transformation, improved customer experiences, and operational agility have come to depend on custom software, specially created applications and platforms designed to satisfy particular corporate demands. Demand for web-based portals, enterprise resource planning (ERP) tools, and mobile applications incorporating new technologies like artificial intelligence/machine learning (AI/ML), IoT, and blockchain underlies market growth. Key sectors using bespoke solutions include manufacturing for Industry 4.0 coordination, healthcare for telemedicine apps, and BFSI for safe transaction platforms.

Key Market Insights:

Driven by fast adoption of cloud-native architectures and API-first development techniques that simplify worldwide access, the web-based solutions, including custom web portals, e-commerce systems, and BI dashboards, accounted for roughly 38% of all revenue.

Organizations want SaaS and PaaS models for quicker time-to-market, elastic scalability, and lower up-front infrastructure costs, so cloud-based custom development services are expected to grow at a 23% compound annual growth rate between 2025 and 2030.

Approximately 65% of the market spend in 2024, big corporations with massive digital portfolios and transformation budgets, hired sophisticated custom platforms for worldwide operations and compliance.

With a share of around 31% backed by robust IT ecosystems, high per capita software spending, and a concentration of major tech vendors and service providers, North America led regional support.

Custom Software Development Market Drivers:

The recent initiatives taken regarding digital transformation are driving the growth of this market at a rapid pace.

European businesses and public-sector entities will spend USD 1.1 trillion on IT in 2024, a 9% increase, therefore emphasizing ongoing software and digital services investment, according to the Financial Times. Further research shows that 46% of businesses intend to increase application-modernization budgets, therefore making it a top-four area of spending. Driving custom development that incorporates AI/ML, cloud microservices, and IoT data streams into major processes, boards are demanding digital-business acceleration, 70% will demand quantifiable digital goods and service results by 2025. API-first, event-driven designs are helping businesses to eliminate monolithic legacy systems and improve agility by up to 40%, therefore lowering time-to-market.

There is a rise in the demand for applications that are customer-centric in nature, which drives the demand for this market.

In a world of hyperconnected customers, businesses distinguish themselves via extremely customized, context-aware apps. McKinsey research reveals that businesses providing superior digital experiences have 15–20% greater customer retention and satisfaction levels. Businesses can provide offers triggered by user behaviors and preferences across touchpoints by incorporating real-time recommendation engines, dynamic loyalty platforms, and custom-built mobile self-service portals using first-party data. Banking applications, for instance, adjust interfaces according on location and past transactions, hence raising 25% active‐user participation. Deploying in-app AR try-on experiences, merchants claim session durations that are 30% longer. Demand for UX/UI-driven custom software projects keeps skyrocketing as customer experience becomes the main brand differentiator.

The regulatory compliance is shaping the future of this market by helping it grow faster.

A rapidly changing regulatory environment compels businesses to construct compliance "into the code." Over 170 data-protection and cybersecurity laws now govern digital activities, including GDPR in Europe, CCPA in California, PSD2 for payments, and HIPAA in healthcare; noncompliance fines can be as high as 4% of global turnover or USD 20 million under GDPR. Industry-specific rules (e.g., IEC 62443 for industrial control systems) demand secure-by-design development lifecycles, extensive audit tracks, and automated breach-notification procedures. By proactively incorporating regulatory controls and automated compliance-reporting modules, companies lower audit preparation time by 50% and minimize the danger of expensive penalties.

The recent proliferation of emerging technologies is driving innovation in this market.

A golden age of custom software invention is being spurred by the intersection of AI/ML, blockchain, and IoT. According to IDC, spending on artificial intelligence technologies will reach over USD 337 billion in 2025, with 67% of this coming from businesses directly integrating AI into essential applications. Blockchain-based origin and smart-contract modules are customized for supply-chain traceability, hence lowering product-counterfeiting incidents by 30%. Utilizing real-time sensor data and tailored analytics pipelines, IoT-driven digital twins in manufacturing maximize manufacturing yields and predictive maintenance, hence lowering unplanned downtime by 25%. Custom development continues to be the preferred path to create solutions that fit exactly with particular operational contexts and strategic objectives as companies attempt to use these innovative technologies at scale.

Custom Software Development Market Restraints and Challenges:

The cost related to the development and maintenance of the market is quite high, hampering market growth.

Six-figure budgets are commonly needed for custom software development initiatives to encompass requirements gathering, UI/UX design, programming, testing, and deployment, with mid-sized applications running between USD 50,000 and USD 150,000 and enterprise-scale projects exceeding USD 500,000. Beyond initial construction, continuous maintenance, including security patching, library upgrades, performance tuning, and minor improvements, can add 15–25% of the original development cost annually and, in total, account for 60–80% of all lifetime costs over five years. Particularly, SMEs note these high total cost of ownership numbers as a major hurdle, therefore choosing patchwork, off-the-shelf alternatives lacking the smooth integration and customized features of custom builds.

There is a global shortage of skilled workforce, which slows down the operations of this market.

A serious worldwide lack of developers experienced in leading frameworks (React, Angular, Kubernetes) and advanced domains (AI/ML, blockchain, IoT) has intensified competition for qualified personnel, pushing senior engineer billing rates over USD 150 per hour in main markets. 73% of companies report difficulty filling specialized software roles, which leads to protracted hiring cycles that delay project kick-offs by an average of 3–6 months and raise budgets by 20–30%. This-skill-gap-not-only-hampers-time-to-market-but-also-exacerbates-risks-of-code-defects-and-security-vulnerabilities-when-under-skilled-teams-attempt-complex-custom-implementations.

The integration process with the legacy system is quite complex which would hinder market growth.

Many businesses use monolithic on-premise ERPs, CRM systems, and bespoke databases dating back to modern microservices and cloud architectures. Combining new custom applications with these old systems usually calls for extensive middleware, data-mapping, and API orchestration, therefore increasing costs by 15–25% and stretching project schedules by 20–30%. Organizations battle to get real-time data consistency without standardized data models and company-wide integration frameworks, which results in sporadic user experiences and manual reconciliation procedures that offset the efficiency gains of custom software.

The market faces challenge from the challenge of scope creep and project overruns.

Custom development projects are especially vulnerable to scope creep. Studies estimate that unanticipated feature requests and changing business needs cause 80% of software projects to go over their initial schedules or budgets. Each extra requirement adds complexity without strong change-management governance, clear baselines, impact analysis, and formal sign-off procedures, usually increasing total project expenses by 15–20%. This dynamic undermines stakeholder trust, raises project cancellation risk, and causes companies to approve more upcoming customer projects.

Custom Software Development Market Opportunities:

The emergence of low-code and no-code code platforms is presenting the market with an opportunity to grow.

Low-code/no-code (LCNC) development tools let "citizen developers" create company apps with little coding, hence changing the custom software environment. With businesses trying to close the developer skills gap and speed delivery, the LCNC market reached USD 20.5 billion in 2024 and is expected to grow at a 25.4 percent CAGR through 2030. Providing drag-and-drop interfaces, prebuilt connectors, and AI-assisted logic generation, LCNC tools lower traditional development costs by up to 50% and compress project timelines from months to weeks. Particularly small and medium-sized businesses use LCNC to automate internal procedures, invoice approvals, and customer onboarding, for example, without having to wait for limited IT resources, therefore democratizing innovation and facilitating fast prototyping. This enables corporate users to repeatedly focus on process optimization in real time, fostering general organizational agility, while professional developers can concentrate on difficult, high-value solutions.

The growing use of vertical-specific solutions gives the market an opportunity to develop further.

Vertical-specific demands are increasingly driving custom software development since off-the-shelf solutions fall short. For example, by 2027, the worldwide telemedicine software market alone is estimated to reach over USD 33.4 billion, therefore driving tailored portal and mobile-app deployments integrating patient data, video consultations, and remote monitoring. In manufacturing, digital-twin systems, allowing real-time simulation of production lines, are expected to top USD 73.5 billion by 2028, necessitating customized integrations with IIoT devices and analytics engines. Financial services, a market area with a 20% CAGR, are commissioning authorized regtech modules, automating KYC/KYB and transaction monitoring, to meet changing AML guidelines. As developers provide ready-made solutions that include industry best practices and compliance controls, these high-value, domain-targeted projects command premium prices and promote close client relationships.

The growing use of 5G networks and edge computing is transforming this market at a rapid rate.

5G and edge computing are generating a new generation of customized applications requiring extremely low latency and great throughput. By 2026, 5G subscriptions will surpass one billion, and edge computing income will reach USD 17.7 billion, up from USD 3.6 billion. Custom software optimized for edge nodes, such as real-time video analytics for autonomous vehicles, AR/VR collaboration suites for remote maintenance, and AI-driven anomaly detection in smart grids, delivers response times under 10 milliseconds, impossible with centralized cloud models. Enterprises in healthcare are commissioning edge-enabled tele-surgery platforms, while broadcasters develop low-latency live-stream workflows. These specialized, network-aware applications demand close cooperation with telcos and hardware manufacturers, producing a profitable niche where custom developers may set themselves apart via performance tuning and 5G–edge orchestration proficiency.

The recent popularity of subscription-based delivery models is helping this market develop better.

Custom software companies have found a major opportunity in switching to subscription-based delivery since it provides clients with predictable OpEx models and ongoing innovation. According to Forrester, 68% of software buyers now prefer subscription over perpetual licensing, valuing built-in maintenance, security updates, and feature rollouts. Custom developers are packaging their solutions as managed services, delivering hosted applications with tiered SLAs, usage-based billing, and ongoing support, thereby smoothing clients’ budgeting cycles and fostering long-term relationships. This change also gives developers consistent revenue streams and greater lifetime customer value; clients gain from always changing functionality without disruptive upgrade projects. Particularly among SMEs looking for enterprise-grade solutions with little beginning investment, subscription-based custom-software offerings will keep gaining traction.

Custom Software Development Market Segmentation:

Market Segmentation: By Type

• Web-based Solutions

• Mobile Applications

• Enterprise Software

The Web-based Solutions segment is the dominant segment of this market. Web-Based Solutions (about 38%) are preferred for cross-platform accessibility and cloud integration. The Mobile Application segment is the fastest-growing for this market. Driven by the rise of smartphones and the need for on-the-go services, mobile applications (CAGR ~24%) are the fastest-growing. When it comes to the Enterprise Software segment of this market, with ERP, CRM modifications for sophisticated back-office processes, Enterprise Software comprises around 29% of the market share in 2024.

Market Segmentation: By Deployment Mode

• Cloud-based

• On-premises

• Hybrid

The Cloud-based segment of the market is said to dominate. Cloud-based, with around 60% market share in 2024, dominates due to rapid provisioning and lower infrastructure expenses. The Hybrid mode is the fastest-growing one. Hybrid (CAGR ~23 %) combines on-premise control with cloud scalability, thereby drawing regulated sectors. For consumers with tight data-residency requirements, on-premises (~25%) is still stable.

Market Segmentation: By Enterprise Size

• Large Enterprises

• SMEs

Large Enterprises are said to dominate this market with the largest market share. It holds around 65% of the market share in 2024, which is due to rapid global digital transformation for leveraging custom platforms. The SMEs segment is the fastest-growing segment. SMEs (CAGR ~18 %) are adopting customized solutions through reasonably priced, SaaS-driven models.

Market Segmentation: By Industry

• BFSI

• Healthcare

• IT & Telecom

• Manufacturing

• Retail

• Government

• Education

• Others

The IT & Telecom segment dominates this market. Information Technology and Telecom Leading the custom software development sector, the IT and telecom industry accounts for around 24% of all revenue as operators and cloud providers order specialized network-automation, CRM, and cybersecurity solutions to enable digital-service portfolios. The Government segment is said to be the fastest-growing segment. This is due to the initiatives taken by the governments in the field of digital transformation, digital identity framework, and smart city management system.

BFSI accounts for a substantial portion (around 18%) of investment by banks and insurers in compliance solutions, AI-driven risk analytics, and secure mobile banking. With pandemic-driven telemedicine driving expansion, healthcare (around 14%) sees custom EHR systems, telemedicine applications, and medical-device interfaces developed by hospitals and clinics. Manufacturing (around 15%): Industry 4.0 projects, digital twins, MES, IIoT analytics, need specific software to maximize output and predictive maintenance. Retail (approximately 12%): Omnichannel commerce, tailored recommendation engines, and loyalty-program integrations stimulate specialized retail-tech growth. Education (around 8%): K–12 districts and colleges create LMS integrations, online-classroom platforms, and secure exam-proctoring tools. Others (about 9%) apply custom asset-tracking, supply-chain, and smart-grid solutions across sectors like real estate, logistics, and energy.

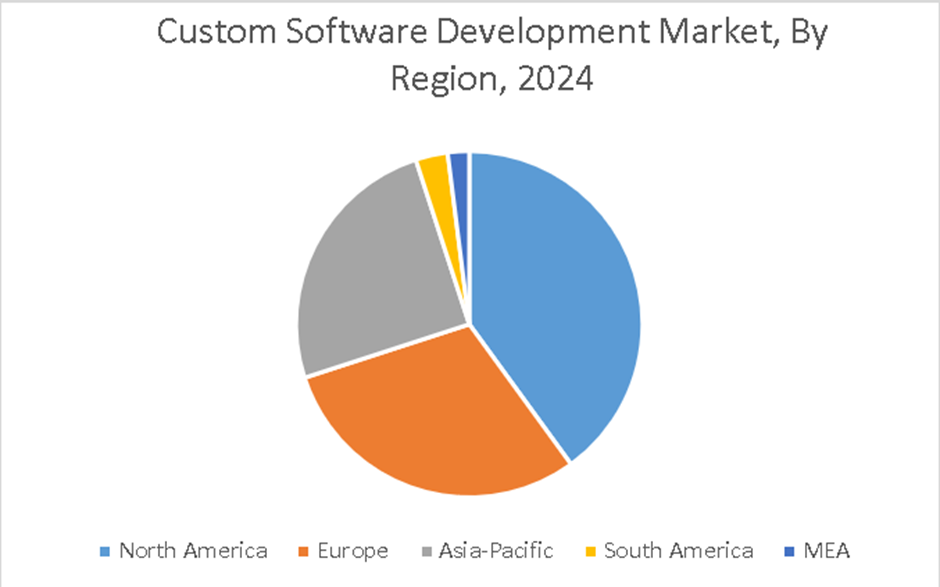

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

North America dominates the market. North America dominates the market at around 31%, driven by strong per-capita IT budgets, established software ecosystems, and providers. The Asia-Pacific region is said to be the fastest-growing region of this market. Driven by quick digitization in China, India's tech-hub expansion, and booming e-commerce and smart-city projects in Southeast Asia, Asia Pacific is expected to grow at a ~22% compound annual growth rate.

Europe (about 28%), with GDPR compliance, German Industry 4.0, and UK-based fintech innovation driving a strong need for personalized solutions. South America, with around 15% market share, is defined by Custom Financial, ERP, and IoT applications flourishing as a result of Brazil's fintech expansion and Mexico's manufacturing digitization. Middle East and Africa (around 6%) emerging custom-software expenditures include UAE smart-city projects, Saudi Vision 2030 digital initiatives, and South Africa's telecom modernization initiative.

COVID-19 Impact Analysis on the Global Custom Software Development Market:

The epidemic quickened digital transformation, therefore driving businesses to use custom applications, telehealth, e-learning, and remote-work platforms instead of manual procedures and raising custom development spending by 25% in 2020–2021. Although the first budgets were reallocated to immediate digital solutions, 72% of companies maintained elevated custom-software pipelines post-pandemic to enable hybrid models and resilient supply networks.

Latest Trends/ Developments:

The process of integrating Generative AI with IDEs for the purpose of code generation is helping in reducing the development time by 30%.

Microservices are used in bespoke solutions to allow modular scalability and continuous distribution.

Security moves left with built-in vulnerability scanning and compliance inspections in CI/CD processes.

Mendix and OutSystems are two platforms that speed up prototyping, letting company users with little technical expertise create apps.

Key Players:

• Accenture plc

• Brainvire Infotech Inc.

• Capgemini

• Cognizant

• HCL Technologies Limited

• Iflexion

• Infopulse

• Infosys Ltd.

• Magora

• Microsoft

Chapter 1. Global Custom Software Development Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Custom Software Development Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Custom Software Development Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Custom Software Development MarketEntry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Custom Software Development Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Custom Software Development Market- By Type

6.1. Introduction/Key Findings

6.2. Web-based Solutions

6.3. Mobile Applications

6.4. Enterprise Software

6.5. Y-O-Y Growth trend Analysis By Type

6.6. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 7. Global Custom Software Development Market– By Deployment Mode

7.1 Introduction/Key Findings

7.2. On-premises

7.3. Cloud-based

7.4. Hybrid

7.5. Y-O-Y Growth trend Analysis By Deployment Mode

7.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global Custom Software Development Market– By Enterprise Size

8.1. Introduction/Key Findings

8.2. SMEs

8.3. Large Enterprises

8.4. Y-O-Y Growth trend Analysis By Enterprise Size

8.5. Absolute $ Opportunity Analysis By Enterprise Size, 2025-2030

Chapter 9. Global Custom Software Development Market– By Industry

9.1. Introduction/Key Findings

9.2. BFSI

9.3. Healthcare

9.4. IT & Telecom

9.5. Manufacturing

9.6. Retail

9.7. Government

9.8. Education

9.9. Others

9.10. Y-O-Y Growth trend Analysis By Industry

9.11. Absolute $ Opportunity Analysis By Industry, 2025-2030

Chapter 10. Global Custom Software Development Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Deployment Mode

10.1.4. By Enterprise Size

10.1.5. By Industry

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Deployment Mode

10.2.4. By Enterprise Size

10.2.5. By Industry

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Type

10.3.3. By Deployment Mode

10.3.4. By Enterprise Size

10.3.5. By Industry

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Deployment Mode

10.4.4. By Enterprise Size

10.4.5. By Industry

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Deployment Mode

10.5.4. By Enterprise Size

10.5.5. By Industry

10.5.6. By Region

Chapter 11. Global Custom Software Development Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Accenture plc

11.2. Brainvire Infotech Inc.

11.3. Capgemini

11.4. Cognizant

11.5. HCL Technologies Limited

11.6. Iflexion

11.7. Infopulse

11.8. Infosys Ltd.

11.9. Magora

11.10. Microsoft

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Key drivers are demand for individualized customer experiences, integration of AI/ML and IoT, digital transformation mandates, and the need for compliance-centric platforms.

Leading with 31% market share in 2024, North America is followed by Asia-Pacific as the fastest-growing (CAGR ~22%), as China, India, and Southeast Asia quickly digitalize.

High TCO, talent deficits, interface complexity with older systems, and scope creep continue to be major obstacles, postponing time-to-value and increasing prices.

With 72% of businesses keeping high-development channels after 2021, the epidemic drove a 25% increase in custom development for telehealth, remote-work tools, and e-commerce platforms.

While BFSI continues to be a strong sector for safe fintech and compliance solutions, telemedicine and patient-engagement apps are forecast to grow at a roughly 20% CAGR (2025–2030).