Global Content Recommendation Engine Market Research Report – Segmentation By Component (Solutions, Services), By Algorithm Type (Collaborative Filtering, Content-based, Hybrid), By End-Use Industry (E-commerce, Media & Entertainment, Retail & Consumer Goods, BFSI, Healthcare, Others), By Deployment Mode (Cloud-based, On-premises), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16530

Format:

Region: Global

Market Size and Overview:

The Global Content Recommendation Engine Market was valued at USD 10.67 billion in 2024 and is projected to reach a market size of USD 29.51 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.56%.

Rising e-commerce personalization, streaming-media expansion, and AI-driven analytics drive this rise. Driven by China's explosive online retail and India's digital‑media growth, Asia-Pacific leads with over 40% share (2030), while North America and Europe follow, propelled by SaaS adoption and data‑privacy laws. Engines power personalization across streaming platforms, e‑commerce sites, news portals, and corporate knowledge bases—filtering enormous content to improve engagement, retention, and revenue.

Key Market Insights:

By the year 2030, APAC is said to have a 40% share of the global revenue, which will be approximately 12 billion. This will be due to the rising e-commerce sector of China and the expansion of the OTT platforms in India.

Due to increasing need for ready-to-deploy projects, Recommendation Solutions (on-prem and embedded libraries) accounted for 60% of 2024 income; Services (custom-integration, tuning, managed-recommendation-as-a-service) grew at 37.9% CAGR.

With 30% of market share, retail and consumer products will bring in USD 2 billion in 2024 as customized product recommendations drive 22% more client lifetime value.

Comprising 55% of deployments, Cloud‑Based engines are growing at roughly 39% CAGR as SaaS models cut time-to-value and lower up-front expenses for SMEs.

Content Recommendation Engine Market Drivers:

There has been an explosive growth in the field of digital content worldwide, which is driving the growth of this market.

Reflecting the fast growth of video, social media, and e-commerce catalogues, the volume of worldwide digital data is projected to rise from about 120 zettabytes to 181 zettabytes by 2025. The worldwide Datasphere will hit 175 zettabytes by 2025, highlighting the never-before-experienced volume of material that sites must curate. This onslaught of material causes significant information-overload issues, which pushes companies to use recommendation systems that find pertinent items from maybe billions of assets. Keeping consumers interested longer and discovering more material, personalized recommendations have been found to raise average session durations by 20–30%. Directly translating personalization into quantifiable income benefits, recommendation-driven platforms also show conversion rate increases of up to 15%. Engines capable of real-time, scalable inference are further needed by rapid content expansion over UGC (user-generated content) sites and OTT services to manage surges in content submissions. Monthly, streaming-media companies now index petabytes of fresh video, rendering human curation impossible and stimulating the use of automated recommendation systems. E-commerce catalogs with millions of SKUs depend on AI-powered filtering to direct customers, hence lowering search friction and boosting mean order values 10–12%. Recommendations must change to handle fresh metadata kinds and user-interaction signals as content formats grow, 3D, VR, and live streams. Hybrid architectures combining on-prem indexing for latency-sensitive assets with cloud-based analytics for worldwide catalog processing are being invested in by companies. A primary growth driver for solutions for recommendation engines is the need for ongoing, automated content classification and suggestion optimization that follows.

The growing emphasis on customer preferences and experience is driving the growth of this market.

Seventy-one percent of modern consumers expect businesses to forecast their needs and provide pertinent information in real time. Research by Salesforce also shows that 71% of consumers become annoyed when customization is lacking, therefore jeopardizing brand trust and loyalty. By providing customized product suggestions, personalization efforts, including recommendation engines, have propelled 22% greater repeat-purchase rates for merchants. When consumers on e-commerce sites get context-aware recommendations, their average order values rise by 15%, therefore immediately affecting bottom-line sales. Personalized "Next Up" features in streaming media improve viewer retention, lowering churn in subscription services by 10–12%. According to post‑interaction surveys, real‑time customization also raises client happiness scores by 18%. Modeling interaction graphs, Graph Neural Networks (GNNs) further capture sophisticated user–item relationships, therefore improving hit‑rate metrics by 35–40% over conventional collaborative‑filtering techniques.

The recent advancements in the fields of AI and Deep Learning is helping to bring in innovations in this market.

Originally developed for NLP, transformers such as BERT and GPT have been adapted to recommendation chores so that models may capture long‑range dependencies in user–item interaction sequences and raise top‑K hit rates by 35 to 40% over traditional approaches. Graph Neural Networks (GNNs) further enhance suggestion accuracy by modeling user–item interactions as graph structures; surveys show 20 to 30% improvement in precision and recall scores on public datasets like MovieLens and Amazon Reviews. Using TransGNN, a new architecture that alternates Transformer and GNN layers, the global attention of transformers expands GNN receptive fields and message‑passing of GNNs infuses structural graph information, therefore producing up to 15% performance gain on benchmark tasks. Deep autoencoders compress high‑dimensional user–item matrices into low‑rank latent representations, therefore allowing scalable inference on catalogues with millions of items while keeping >90% of recommendation quality. Session-based recommenders using self-attention mechanisms capture real-time behavioural patterns, thereby increasing click-through rates by 12 to 18% over RNN-based sequence models.

The integration of cloud-based systems and MLOps is helping this market to develop further.

By 2024, 65% of businesses had embraced Kubernetes as their main orchestration platform for machine learning workloads, therefore allowing dynamic scaling and resilient deployments. Cloud-native infrastructures and MLOps automation have transformed how companies develop, deploy, and maintain recommendation engines at scale. Declarative MLOps pipelines, implemented via GitOps workflows with Argo CD and GitHub Actions, offer reproducible, versioned deployments for both data-processing and model-serving components, therefore reducing manual configuration mistakes by 40%. Automated A/B testing frameworks—incorporated into CI/CD pipelines—route subsets of live traffic to new model variations, thereby speeding up feature rollout cycles by 50%. Continuous integration of feature stores (e.g., Feast, Tecton) synchronizes offline training and online inference, hence preventing feature drift and raising recommendation accuracy by 15% over disjointed pipelines. Automatic flagging of input changes by feature-drift detectors using statistical tests (Kolmogorov–Smirnov) and data-drift alerts guarantees retraining pipelines run only when needed, therefore lowering 35% of computer expenditure.

Content Recommendation Engine Market Restraints and Challenges:

The market faces a huge challenge from the risk of data leaks, which hampers the growth of this market.

Strict data‑privacy regulations GDPR in Europe and CCPA in California, restrict the gathering and use of personal information, obliging recommendation engineers to reduce dependence on raw user identifiers and behavioral logs. GDPR makes it necessary to get express consent for personal data processing; users can demand deletion of their data at any time, therefore challenging the retention of long‑term contact histories needed for exact recommendations. Many SaaS companies implement consent-management modules that mask or obfuscate user IDs during model training because the CCPA gives California residents the right to opt out of data sales and to access or delete personal information. To comply, engineers increasingly use federated learning, which stores raw data on-device and only distributes model changes, therefore circumventing PII centralization; however, federated methods add overhead in arranging training rounds across edge customers and might slow convergence by 20–30%.

The issues related to cold-start and sparsity greatly affect the growth of the market.

Data sparsity and cold-start are ongoing difficulties restricting the performance of recommendation systems. Lack of interaction history for fresh users and new items in a cold-start situation precludes collaborative filtering algorithms from producing precise recommendations. Likewise, sparse user–item matrices, especially in long-tail product categories, lower the dependability of preference estimates. This causes up to 20% of suggestions to be less than ideal, therefore lowering user interaction. Using metadata like item descriptions or user profiles, content-based techniques can offer some respite. When content information is scarce or unstructured, however, these techniques could fail. Hybrid models, which incorporate cooperative and content-based filtering, help reduce the problem but add architectural intricacy and computational strain. Advanced methods, including meta-learning, transfer learning, and knowledge graphs, are being used to enhance generalization in sparse data settings. They still need close adjusting and integration, nevertheless. Though still experimental, newer approaches like reinforcement learning and LLM-augmented simulations are surfacing. Personalization at the cold-start stage sometimes depends on implicit behavior like click-throughs or dwell time, which might not always represent actual intent. Cold-start problems are likely to persist as the quantity and variety of digital content keep increasing. Future engines could draw more on efficient onboarding approaches, user segmentation, and zero-shot learning. Dealing with this issue is still vital for reaching uniform user happiness across devices.

The costs related to computation are quite high, which makes it less affordable.

Modern content recommendation systems are resource-intensive, particularly those based on graph neural networks and deep learning. Particularly for systems handling millions of users and products, training large-scale models typically calls for 100 to 200 GPU hours per retraining cycle. This results in substantial operating expenses, particularly for cloud-based installations where high-performance GPUs and memory command a premium. Low-latency inference has to be supported by models for real-time personalization, therefore fueling the demand for high-throughput infrastructure. Moreover, especially in quickly changing fields like e-commerce or streaming media, regular retraining is required to keep recommendations relevant. Because several models are tested in parallel, AutoML solutions even increase compute time. Model compression methods like pruning or quantization help shorten inference time but can compromise accuracy if not appropriately calibrated. Particularly costly for hybrid models are inference pipelines, as they call for a simultaneous serving of several components. On-demand scaling and serverless GPU instances can help, but come with their cost unpredictability.

The process of integration is considered to be very complex, which slows down market operations.

Integrating recommendation engines into business systems is frequently a protracted, resource-intensive endeavor. Many companies use legacy CMS, ERP, and CRM systems devoid of the APIs or data pipelines needed for smooth suggestion distribution. Comprehensive custom engineering is needed to map data across several forms, sources, and schemas. Building dependable real-time feature pipelines and ETL processes increases technical debt. Implementation is made more difficult by poor data quality, such as erratic timestamps, missing values, or duplicate logs, which also impacts model performance. Six to nine months are frequently needed for organizations to thoroughly integrate and implement a suggested remedy, hence delaying return on investment and time-to-value. Real-time engines further complicate architectural design by requiring regular synchronization between batch and stream data. Integration is slowed in controlled industries like finance or healthcare by the requirement for audit trails, data provenance, and governance systems. Recommendations also need to match front-end UX and commercial regulations, therefore, teamwork among departments is required. Localization and compliance throughout several countries introduce additional levels of complexity for global companies. Companies could have to recruit consultants or platform integrators to expedite the process, therefore raising the total cost. Keeping and changing these integrations over time also calls for continuous technological knowledge.

Content Recommendation Engine Market Opportunities:

The integration of voice and visual recommendation interface presents a great market growth opportunity.

Early adopters of e-commerce and media sites are seeing significant rises in user interaction rates as these intuitive technologies minimize the barrier to finding pertinent information. For users with disabilities who may find traditional text-based search challenging and in situations where visual cues are very important, such as fashion e-commerce or home décor discovery, this trend is especially effective. Their part in improving the user experience and fueling content discovery via recommendation engines will only get more obvious as voice and visual search tools grow and become more ubiquitous on consumer devices, resulting in greater conversion rates and consumer pleasure.

The advent of real-time personalization improves user experience, which helps the market expand its reach.

The development of edge-deployed inference systems represents a big advance in real-time content personalization capabilities for recommendation. Directly running complex machine learning algorithms on user devices like smartphones and IoT devices, these engines can provide suggestions with incredibly low latency, often less than 50 milliseconds. This speed opens the door for very context-aware recommendations based on immediate elements, including the user's present location, browsing history within the current session, and even real-time interactions. For example, a news app might propose stories pertinent to the user's present location, or a streaming service could recommend the next episode depending on their viewing behavior over the previous few seconds. With research showing significant increases in click-through rates and content consumption, this level of responsiveness results in a much more interesting and pertinent user experience. Real-time, context-aware recommendations will become a normal expectation on several digital platforms as edge computing gets more common and devices get more processing power.

The demand for B2B content creation is rising rapidly, offering this market a chance to penetrate new markets.

The demand for customized internal recommendation systems targeted for B2B settings—specifically, knowledge management and e-learning systems inside businesses—is a growing market sector with great growth potential. Companies understand the need to effectively compile and present pertinent internal information to their staff as remote work grows more common and digital training programs gather pace. Leading to better productivity, quicker onboarding, and increased skill development, these recommendation engines enable staff members to find important knowledge assets, interact with pertinent experts, and customize their learning routes. The projection of a great CAGR for this sector highlights the growing awareness of internal content as a valuable asset and the need for smart systems to properly handle and spread it across businesses. The need to promote ongoing learning, increase information access, and improve cooperation in a digitally driven work environment is what propels this trend.

The emergence of RaaS (Recommendation as a Service) has opened up new opportunities for this market.

The emergence of RaaS (Recommendation as a Service) has opened up new opportunities for this market. The appearance of Recommendation as a Service (RaaS) platforms is democratizing advanced personalization tools and making them available to Small and Medium-sized Businesses (SMBs) that might lack the internal machine learning skills and infrastructure to construct and maintain their recommendation engines. By providing simple-to-integrate APIs and user-friendly interfaces, RaaS lets niche e-tailers, media startups, and other SMBs use the power of individualized recommendations to boost user engagement, boost conversions, and increase customer retention. These subscription-based models let companies avoid the challenges and costs involved with establishing and maintaining their ML pipelines.

Content Recommendation Engine Market Segmentation:

Market Segmentation: By Component

• Solutions

• Services

The Solutions segment dominates the market. As businesses integrate AI-powered personalization right into their apps, platforms, libraries, and APIs that offer out‑of‑the‑box recommendation capabilities make up around 60% of market revenue. The Services segment is the fastest-growing segment, with a roughly 37.9% CAGR. Services include managed "Recommendation‑as‑a‑Service" offerings as well as consulting, implementation, and customization. These professional services are growing quickly as companies look for ready-to-use deployments and constant tuning.

Market Segmentation: By Algorithm Type

• Collaborative Filtering

• Content-based

• Hybrid

The Collaborative Filtering segment dominates this market, with its maturity and success in e‑commerce and media channels, this method generated roughly 45 to 50 percent of algorithm-type revenues based on user-item interaction matrices. The Hybrid segment is the fastest-growing segment. Combining collaborative and content‑based methods, hybrid engines are growing at about 35% CAGR as they overcome cold‑start and scarcity problems, providing more precise recommendations across uses. With other techniques for new-item recommendations, Content-Based (Niche) segment accounts for around a 20% share, dependent only on item characteristics.

Market Segmentation: By End-Use Industry

• E-commerce

• Media & Entertainment

• Retail & Consumer Goods

• BFSI

• Healthcare

• Others

The E-commerce segment is said to dominate the market. Online retail drives adoption via suggestion engines, which results in a 15–22% increase in AOV (average order value) and a 20–30% rise in conversion rates. The BFSI and Healthcare segments together are said to be the fastest-growing segments, as financial services and healthcare are using customized content for cross-selling and patient-education platforms, as data-driven involvement becomes essential.

When it comes to the Media & Entertainment segment, One-quarter of expenditure is from media and entertainment (~25%), as personalization helps streaming services and news outlets to increase engagement and memory. The Retail & Consumer Goods segment has a 15% market share. This segment includes recommendations for web and in-store kiosks, generating USD 2 billion in engine-driven sales growth in 2024. The Others segment includes B2B information‑management systems, travel, and instruction.

Market Segmentation: By Deployment Mode

• Cloud-based

• On-premises

The Cloud-based segment dominates this market with around 55% market share, as it offers lower upfront costs, rapid time-to-value, and elastic scalability, which are attractive to the SMEs. This segment is also considered to be the fastest-growing because of increased outsourcing, A/B Testing, and continuous optimization. The on-premises segment is preferred by major corporations with demanding data sovereignty and latency needs; on-premises (~45%) keeps a large market in controlled sectors.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

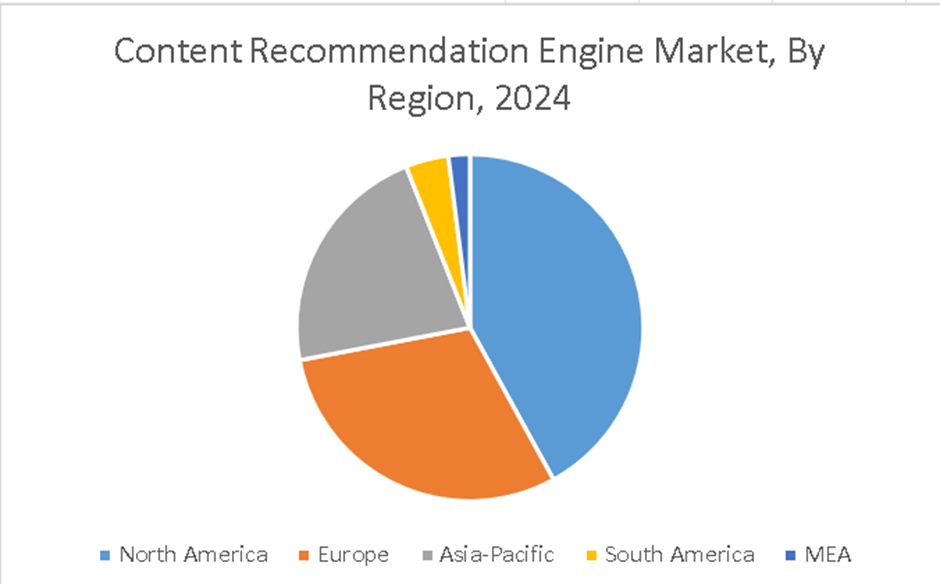

North America has emerged as the leader of the market. Driven by widespread adoption of digital content platforms, substantial investments in artificial intelligence and machine learning technologies, and a great focus on tailored user experiences across several sectors, the largest market is emerging. The Asia-Pacific region is said to be the fastest-growing region of the market. The adoption of sophisticated analytics and AI-driven solutions in nations such as China and India, as well as the increasing internet penetration and growing consumption of digital content, propelled fast expansion.

The European region is defined by strong expansion is driven by growing demand for content personalization, legislative compliance on data privacy, and media and entertainment firms' investments in sophisticated recommendation technologies. South America and the MEA regions are the emerging markets, rising markets with growth potential, as companies start to invest in content recommendation systems to boost consumer experiences and improve user engagement. The MEA is a smaller market size, but growing interest in content suggestion engines as companies try to use custom content strategies to boost user interaction.

COVID-19 Impact Analysis on the Global Content Recommendation Engine Market:

With a 45% increase in digital-media consumption and a 32% rise in e-commerce adoption, the epidemic accelerated the adoption of 50% higher recommendation‑engine deployments to tailor user experiences and boost up-sell/cross-sell. Early 2020 supply-chain disruptions delayed enterprise-software projects by three to six months, but cloud-based engines saw 25% more adoption as companies gave priority to fast-to-implement SaaS solutions. Furthermore, remote-work models created demand for B2B curation and knowledge-base recommendations, therefore preparing the ground for post-2021 expansion.

Latest Trends/ Developments:

Leading suppliers, including Amazon Personalize and Algolia, now use transformer architectures to boost long‑tail product recommendations by 20% over LSTM models.

Emerging federal learning systems let models be trained on edge data without raw data transmission, thus complying with GDPR and developing privacy requirements.

Compared to static profiles, session-based algorithms employing real-time clickstreams provide 15 to 18% more click-through rates.

XAI modules are being integrated on platforms to reveal “Why this recommendation?” stories, therefore improving user trust and lowering opt-out rates by 12%.

Key Players:

• IBM

• Amazon Web Services

• Taboola

• Cxense

• Outbrain

• Revcontent

• Kibo Commerce

• Dynamic Yield

• Curate

• Boomtrain

Chapter 1. Global Content Recommendation Engine Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Content Recommendation Engine Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Content Recommendation Engine Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Content Recommendation Engine Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Content Recommendation Engine Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Content Recommendation Engine Market– By Component

6.1. Introduction/Key Findings

6.2. Solution

6.3. Services

6.4. Y-O-Y Growth trend Analysis By Component

6.5. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global Content Recommendation Engine Market– By Algorithm Type

7.1 Introduction/Key Findings

7.2. Collaborative Filtering

7.3. Content-based

7.4. Hybrid

7.5. Y-O-Y Growth trend Analysis By Algorithm Type

7.6. Absolute $ Opportunity Analysis By Algorithm Type, 2025-2030

Chapter 8. Global Content Recommendation Engine Market– By End-Use Industry

8.1. Introduction/Key Findings

8.2. E-commerce

8.3. Media & Entertainment

8.4. Retail & Consumer Goods

8.5. BFSI

8.6. Healthcare

8.7. Others

8.8. Y-O-Y Growth trend Analysis By End-Use Industry

8.9. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 9. Global Content Recommendation Engine Market– By Deployment Mode

9.1. Introduction/Key Findings

9.2. Cloud-based

9.3. On-premises

9.4. Y-O-Y Growth trend Analysis By Deployment Mode

9.5. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 10. Global Content Recommendation Engine Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Algorithm Type

10.1.4. By End-Use Industry

10.1.5. By Deployment Mode

10.1.6 By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Algorithm Type

10.2.4. By End-Use Industry

10.2.5. By Deployment Mode

10.2.6. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Algorithm Type

10.3.4. By End-Use Industry

10.3.5. By Deployment Mode

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Algorithm Type

10.4.4. By End-Use Industry

10.4.5. By Deployment Mode

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Algorithm Type

10.5.4. By End-Use Industry

10.5.5. By Deployment Mode

10.5.6. By Region

Chapter 11. Global Content Recommendation Engine Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. IBM

11.2. Amazon Web Services

11.3. Taboola

11.4. Cxense

11.5. Outbrain

11.6. Revcontent

11.7. Kibo Commerce

11.8. Dynamic Yield

11.9. Curate

11.10. Boomtrain

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Increased expectations for personalization (74% of consumers), fast growth in volumes of digital content, and advancements in artificial intelligence/machine learning speeding up implementation cycles are among the most frequently asked questions.

Though APAC is fastest overall, Europe is growing fastest (~32% CAGR) thanks to increased OTT platform investments and e-privacy laws (GDPR).

As businesses looked for fast SaaS deployments to customize remote-user experiences, pandemic-induced digital acceleration propelled 55% cloud-based engine adoption.

Data privacy compliance, cold start for new users/items, and high compute costs for big artificial intelligence models continue to be major challenges requiring hybrid algorithm techniques.

Driving the next wave of personalization innovation are privacy-preserving ML (federated learning), explainable AI, session-aware transformers, and edge-deployed inference.