Consumer Cybersecurity Software Market Research Report – Segmentation by Type (Antivirus and Anti-malware Software, Identity Theft Protection, VPN Services, Password Managers, Parental Control Software, Privacy Protection Tools, Secure Web Gateways, Firewall Software, System Optimization Tools, Secure Backup Solutions); By Distribution Channel (Direct Sales through Vendor Websites, App Stores, Retail Electronics Stores, Internet Service Providers, Device Manufacturers, Value-Added Resellers, Telecommunications Companies); By User Type (Individual Consumers, Family Users, Remote Workers, Small Office/Home Office Users, Students and Educational Users, Seniors, Tech Enthusiasts/Power Users, Gaming-focused Users); By Subscription Model (Annual Subscription Plans, Monthly Subscription Plans, Freemium Models, One-time Purchase Licenses, Bundle Packages with Other Services, Free Ad-supported Models, Premium Tiered Subscriptions); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16528

Format:

Region: Global

Market Size and Overview:

The Consumer Cybersecurity Software Market was valued at USD 7.05 Billion in 2024 and is projected to reach a market size of USD 10.78 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 8.87%.

The consumer cybersecurity software market has evolved dramatically in 2024, transforming from a niche technological sector into an essential component of everyday digital life. With the proliferation of smart devices, expansion of remote work arrangements, and increasing sophistication of cyber threats, personal cybersecurity solutions have become as fundamental as home insurance for the average consumer. The market encompasses a wide spectrum of products designed to protect individuals' digital identities, personal data, financial information, and device integrity across multiple platforms and environments. These solutions range from traditional antivirus software to comprehensive security suites offering malware detection, privacy protection, secure browsing, password management, parental controls, and identity theft protection. The modern consumer cybersecurity landscape has witnessed significant consolidation, with major providers expanding their offerings to create all-in-one security platforms rather than standalone products.

Key Market Insights:

Mobile security applications have seen particularly strong growth, with 76% of smartphone users now utilizing some form of security software, compared to just 58% in the previous year.

Password management solutions have experienced dramatic adoption increases, with market penetration reaching 41% among internet users, driven by growing recognition of password vulnerability and increasing requirements for complex credentials across digital services.

Identity theft protection services have expanded their subscriber base by 34% year-over-year, now serving approximately 94 million users worldwide as data breach incidents continue to make headlines.

Secure VPN services have reached 215 million global users, representing a 28% increase from 2023 figures, as privacy concerns and remote work arrangements drive demand for secure connections.

Market Drivers:

Rising Sophistication of Cyber Threats Targeting Consumers

The consumer cybersecurity software market has experienced substantial growth primarily driven by the unprecedented evolution in cyber threats specifically engineered to target individuals rather than organizations. Modern malware, ransomware, and phishing campaigns have become remarkably sophisticated, employing advanced social engineering techniques, exploiting zero-day vulnerabilities, and utilizing artificial intelligence to create convincing deep fakes and personalized attacks. The technical complexity of these threats has surpassed the average consumer's ability to identify and avoid them through cautious behavior alone. The financial motivation behind consumer-targeted attacks has intensified, with cybercriminals recognizing the lucrative opportunities in targeting personal financial information, cryptocurrency wallets, and identity credentials that can be monetized through direct theft or dark web sales. The emergence of "cybercrime-as-a-service" models has democratized access to advanced attack tools, allowing less technically skilled criminals to deploy sophisticated campaigns against individual consumers. These converging factors have created an environment where consumers increasingly recognize that specialized security software has become essential rather than optional, driving market expansion as users seek protection that evolves alongside the threats they face.

Digital Lifestyle Integration and Remote Work Permanence

The permanent shift toward hybrid and remote work arrangements has fundamentally altered consumers' cybersecurity needs, blurring the boundaries between personal and professional digital activities and creating new vulnerabilities that traditional endpoint protection provided by employers cannot address. The average consumer now manages an ecosystem of interconnected devices—smartphones, tablets, laptops, smart home systems, wearables—each representing a potential entry point for cyberattacks and creating a substantially expanded attack surface that requires comprehensive protection. Digital services have become deeply integrated into everyday activities, with consumers conducting financial transactions, storing sensitive personal information, and sharing private communications across multiple platforms and services, all requiring consistent security coverage. The increased dependence on digital tools for essential activities has elevated the potential consequences of security breaches, with consumers recognizing that compromised accounts or stolen credentials can disrupt their ability to work, access critical services, or maintain privacy. This growing awareness of digital dependency has transformed cybersecurity from a technical consideration into a lifestyle necessity, driving demand for intuitive, comprehensive solutions that protect users across their entire digital footprint without requiring technical expertise or causing significant friction in daily activities.

Market Restraints and Challenges:

Despite growing awareness of cyber threats, consumer price sensitivity remains a significant barrier to premium security solution adoption, with many users opting for free alternatives despite their limitations. Technical complexity continues to challenge market expansion, as many comprehensive security solutions require configuration knowledge beyond average users' capabilities. The proliferation of connected devices has created protection gaps that current solutions struggle to address comprehensively. Additionally, persistent misconceptions about built-in operating system protections being sufficient undermines consumers' perceived need for dedicated security software, restraining market potential despite increasing threat sophistication.

Market Opportunities:

Emerging opportunities exist in developing security solutions specifically designed for smart home ecosystems and IoT devices, addressing a rapidly expanding and largely unprotected market segment. The integration of advanced behavioral biometrics offers potential for frictionless yet highly secure authentication systems that could revolutionize consumer cybersecurity. Growing consumer privacy concerns present significant opportunities for solutions that provide transparent control over personal data across platforms. Additionally, the underserved demographic of digitally engaged seniors represents an untapped market segment with specific security needs and increasing purchasing power, while educational components that enhance digital literacy alongside technical protection could create differentiation in an increasingly competitive market.

Market Segmentation:

Segmentation by Type:

• Antivirus and Anti-malware Software

• Identity Theft Protection

• VPN Services

• Password Managers

• Parental Control Software

• Privacy Protection Tools

• Secure Web Gateways

• Firewall Software

• System Optimization Tools

• Secure Backup Solutions

Antivirus and anti-malware software maintains market dominance, commanding approximately 38% of the total consumer cybersecurity market share in 2024. This segment's continued leadership reflects its status as the foundation of consumer cybersecurity strategies and the first security solution typically adopted. Major vendors have evolved their offerings beyond signature-based detection to incorporate behavior-based analysis, machine learning algorithms, and cloud-based threat intelligence, maintaining relevance despite changing threat landscapes. The segment's strength is reinforced by high brand recognition among mainstream consumers and established distribution channels through device manufacturers and operating system integrations.

Identity theft protection solutions represent the fastest-growing segment, experiencing 43% year-over-year growth as consumers increasingly recognize the devastating potential of identity compromise. This category has expanded beyond credit monitoring to offer comprehensive digital identity protection, including dark web monitoring, social media account protection, and automated remediation services for compromised credentials. The segment's growth reflects shifting consumer concerns from device security toward personal data protection, particularly as high-profile data breaches continue to expose personal information at unprecedented scale. Innovative subscription models combining insurance coverage with proactive monitoring have particularly resonated with privacy-conscious consumers.

Segmentation by Distribution Channel:

• Direct Sales through Vendor Websites

• App Stores (Mobile, Desktop)

• Retail Electronics Stores

• Internet Service Providers

• Device Manufacturers (Pre-installed)

• Value-Added Resellers

• Telecommunications Companies

App stores dominate distribution with 42% market share, leveraging the convenience of integrated discovery, purchasing, and installation processes across both mobile and desktop platforms. This channel's strength stems from simplified subscription management, automatic updates, and trusted payment processing that reduces consumer friction in security software acquisition. Major platforms' verification processes provide consumers with confidence in software legitimacy, addressing concerns about potentially malicious security applications. The dominance of app stores reflects broader consumer preferences for streamlined digital experiences and the central role of mobile devices in personal computing, with mobile-first security solutions particularly benefiting from this distribution approach.

Pre-installation by device manufacturers represents the fastest-growing distribution channel, expanding at 37% annually as hardware providers increasingly recognize security as a value-added differentiator. This channel's growth reflects strategic partnerships between cybersecurity vendors and device manufacturers seeking to enhance product value propositions with built-in protection. Consumer preference for seamless out-of-box experiences has driven this trend, as users demonstrate willingness to maintain pre-installed security subscriptions rather than researching alternatives. The channel particularly excels in reaching less tech-savvy demographics who might otherwise neglect security considerations, effectively expanding the total addressable market beyond security-conscious consumers.

Segmentation by User Type:

• Individual Consumers

• Family Users

• Remote Workers

• Small Office/Home Office Users

• Students and Educational Users

• Seniors

• Tech Enthusiasts/Power Users

• Gaming-focused Users

Family users dominate the consumer cybersecurity market with 36% share, driven by heightened protection motivation when children's digital safety is concerned. This segment demonstrates higher willingness to pay premium prices for comprehensive protection packages that include parental controls, screen time management, content filtering, and multi-device coverage. The complexity of managing diverse devices across family members with varying technical capabilities has created demand for intuitive, centrally managed solutions with customizable protection levels. Security vendors have successfully targeted this segment through feature bundling strategies that address both parents' security concerns and children's digital experience management needs.

Remote workers represent the fastest-growing user segment with 45% annual growth, as permanent hybrid work arrangements create personal responsibility for cybersecurity beyond employer-provided solutions. This segment seeks enhanced protection for home networks that now serve as extensions of corporate infrastructure, creating demand for enterprise-grade features in consumer-friendly packages. The segment demonstrates sophisticated threat awareness and willingness to invest in premium solutions that protect both personal and professional digital activities. Security vendors have successfully targeted this growing demographic through dedicated feature sets addressing specific remote work vulnerabilities, including enhanced VPN capabilities, secure document sharing, and separation between personal and professional digital environments.

Segmentation by Subscription Model:

• Annual Subscription Plans

• Monthly Subscription Plans

• Freemium Models

• One-time Purchase Licenses

• Bundle Packages with Other Services

• Free Ad-supported Models

• Premium Tiered Subscriptions

Annual subscription plans maintain market dominance with 49% share, offering vendors predictable revenue streams while providing consumers with optimal price-to-value ratios. This model's success reflects consumer acceptance of security as an ongoing necessity rather than a one-time purchase, supported by automatic renewal mechanisms that reduce churn. Annual plans typically incorporate incentivized discount structures compared to monthly options, effectively locking in customer relationships for longer periods. The model's dominance has been reinforced by vendors' strategic emphasis on annual billing cycles in marketing materials and user interfaces, establishing this approach as the default consumer choice.

Bundle packages with complementary services represent the fastest-growing subscription model, expanding at 41% annually as consumers seek integrated digital protection solutions. This model's growth reflects successful partnerships between cybersecurity vendors and complementary service providers, including cloud storage companies, productivity software developers, and telecommunications providers. Consumers demonstrate strong preference for consolidated billing and simplified management of digital services, creating natural synergies for security bundling approaches. The model particularly excels at reaching consumers who might not independently purchase dedicated security solutions but recognize value when included within broader service packages.

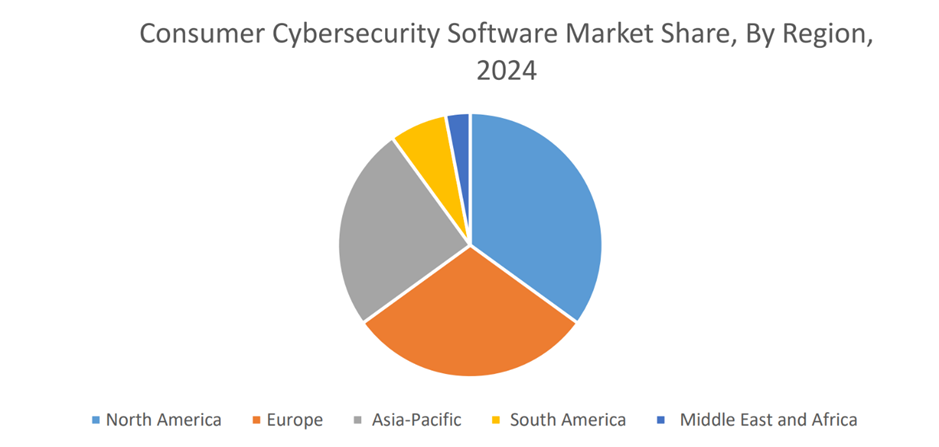

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

North America's dominance in the consumer cybersecurity market stems from its mature digital ecosystem, with consumers managing complex digital footprints across numerous services and devices requiring comprehensive protection. The region's significant data breach history has created heightened threat awareness, with consumers demonstrating sophisticated understanding of cybersecurity risks and corresponding willingness to invest in protection. Regulatory developments regarding data protection and privacy have further accelerated adoption, particularly for identity protection services and privacy-enhancing tools. The region benefits from strong existing cybersecurity infrastructure and vendor presence, with established brands commanding consumer trust and enabling premium pricing strategies that support continued innovation.

The Asia-Pacific region's explosive growth in consumer cybersecurity adoption is driven by several converging factors, including dramatic smartphone penetration increases, expanding middle-class consumer bases with discretionary spending capacity, and rapidly maturing e-commerce and digital payment ecosystems requiring protection. Local cybersecurity vendors have successfully captured market share through regionally tailored solutions addressing specific threat landscapes and consumer preferences, often at price points optimized for emerging market demographics. Government initiatives promoting cybersecurity awareness have significantly expanded the addressable market beyond traditionally security-conscious consumers. Mobile-first security approaches have particularly resonated in markets where smartphones represent the primary computing device for many consumers.

COVID-19 Impact Analysis:

The pandemic permanently accelerated consumer cybersecurity market growth by forcing rapid digital transformation across everyday activities, from remote work to telehealth, online education, and e-commerce. This expanded digital engagement created new attack vectors that cybercriminals quickly exploited, with phishing attempts targeting pandemic anxieties and remote work vulnerabilities. Consumer awareness of digital security risks dramatically increased as high-profile attacks targeting individuals made headlines throughout the pandemic period. The market underwent structural changes with heightened emphasis on integrated protection across home networks supporting multiple simultaneous remote users and devices. These pandemic-driven shifts have persisted beyond the immediate crisis, establishing higher baseline security adoption rates across consumer segments.

Latest Trends and Developments:

Artificial intelligence has transcended marketing hype to deliver meaningful consumer security improvements through predictive threat detection and automated response capabilities that address attacks before traditional signatures could identify them. Zero-trust architecture principles have migrated from enterprise environments to consumer solutions, implementing continuous verification processes rather than assuming device or network trustworthiness. Extended detection and response (XDR) capabilities now provide coordinated protection across devices, applications, and networks rather than siloed security approaches. Passwordless authentication technologies are gaining traction through biometric integration and secure passkeys, addressing fundamental vulnerability points while enhancing user experience. Additionally, gaming-specific security solutions have emerged as a distinct market subcategory, protecting against unique threats targeting valuable in-game assets and accounts.

Key Players in the Market:

• AVG Technologies.

• Fortinet

• Juniper Netwokrs

• CyberArk Software Ltd

• Microsoft Corporation

• Check Point Software

• IBM Corporation

• Sophos Group

• McAfee

• Cisco Systems Inc.

Market Segmentation:

By Type

• Antivirus and Antimalware Software

• Firewall and Network Security

• Identity Theft Protection

• Password Management Software

• Parental Control Software

• Virtual Private Network (VPN) Software

• Anti-phishing and Email Security

• Mobile Security Software

• Secure Browsing Tools

• Data Encryption Software

• Cloud-Based Consumer Security Solutions

• Others

By End User

• Individual Consumers

• Home Offices

• Students and Educational Users

• Freelancers and Independent Professionals

• Elderly and Senior Users

• Gamers and High-Usage Internet Users

• Other

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The growth of the Consumer Cybersecurity Software Market is primarily driven by the rising sophistication of cyber threats specifically targeting individual users rather than just organizations.

The primary concerns about the Consumer Cybersecurity Software Market include persistent price sensitivity among consumers, with many users opting for free alternatives despite their limitations in providing comprehensive protection.

Key players include Norton LifeLock, McAfee, Trend Micro, Kaspersky Lab, Bitdefender, Avast (now part of Gen Digital), ESET, F-Secure, Malwarebytes

North America currently holds the largest market share, estimated around 35%.

Asia-Pacific has shown significant room for growth in specific segments.