Commercial Green Construction Market Research Report - Segmentation by Product Type (Insulation, Roofing, Framing, Interior Finishing, Exterior Siding, HVAC Systems, Others); By Application (Commercial Buildings, Institutional Buildings, Industrial Buildings); By End-User (Corporates, Government, Healthcare, Education, Retail, Others); Region - Forecast (2025 - 2030)

Published: 2025 - June

Report Code: IM-16524

Format:

Region: Global

Market Size and Overview:

The Commercial Green Construction Market was valued at USD 707.4 billion in 2024 and is projected to reach a market size of USD 1,175.99 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 10.7%.

Commercial Green Construction represents a transformative approach to building design, construction, and operation that prioritizes environmental sustainability, energy efficiency, and occupant health. This rapidly evolving sector has gained tremendous momentum in the 21st century as organizations increasingly recognize the financial and environmental benefits of sustainable building practices. With the continuous advancement of green building technologies and growing regulatory pressures for environmental compliance, the demand for sustainable construction solutions is experiencing unprecedented growth across commercial, institutional, and industrial sectors worldwide.

Key Market Insights:

According to the U.S. Green Building Council's 2022 annual report, LEED-certified buildings demonstrated an average 25% reduction in energy consumption and 19% decrease in maintenance costs compared to conventional buildings. Additionally, organizations occupying green buildings reported a 6% increase in productivity and 15% improvement in employee well-being metrics, translating to approximately $1,200 per employee annually in improved performance outcomes.

A comprehensive survey conducted by the World Green Building Council involving 1,000 corporate real estate executives revealed that 73% of companies reported increased property values averaging 7.5% for green-certified commercial buildings. Furthermore, 68% of respondents indicated that sustainable buildings achieved 3.7% higher rental rates and experienced 16% faster tenant lease-up times compared to conventional commercial properties.

Research from the International Energy Agency shows that green commercial buildings consume 30-50% less energy than traditional buildings, with advanced systems achieving up to 70% energy savings in optimal configurations. The study also found that buildings incorporating renewable energy systems, particularly solar installations, recovered their additional investment costs within 8-12 years through reduced operational expenses and available tax incentives.

Commercial Green Construction Market Drivers:

The implementation of stringent environmental regulations and building codes, coupled with increasing corporate sustainability commitments, is fundamentally transforming the commercial construction landscape and driving unprecedented adoption of green building practices.

Governments worldwide are implementing increasingly stringent environmental regulations that mandate energy efficiency standards, carbon emission reductions, and sustainable construction practices for commercial buildings. The European Union's Energy Performance of Buildings Directive requires all new buildings to be nearly zero-energy by 2025, while similar regulations in California, New York, and other jurisdictions are creating mandatory compliance requirements that drive green construction adoption. These regulatory frameworks are supported by substantial financial incentives, including tax credits, rebates, and expedited permitting processes that can reduce project costs by 10-15% for qualified green buildings. Corporate sustainability initiatives have become equally influential, with over 70% of Fortune 500 companies establishing carbon neutrality goals by 2030, creating substantial demand for sustainable building solutions across their real estate portfolios. According to CDP's 2022 Global Supply Chain Report, companies with aggressive sustainability targets are 43% more likely to require green building certifications for their facilities and are willing to pay premium rents for certified sustainable spaces. The growing emphasis on Environmental, Social, and Governance (ESG) criteria in corporate decision-making has further accelerated this trend, with institutional investors increasingly favoring companies with strong environmental performance records

The growing recognition of occupant health and productivity benefits associated with green buildings, combined with technological advances in sustainable building systems, is accelerating market adoption across diverse commercial sectors.

Research consistently demonstrates that green buildings provide significant health and productivity benefits for occupants, creating compelling business cases for sustainable construction investments. Studies indicate that employees in green buildings experience 15% improvement in cognitive function, 6% increase in cognitive scores, and 2% improvement in sleep quality compared to conventional buildings. These improvements translate to measurable economic benefits, with productivity gains averaging $1,200-$3,000 per employee annually, far exceeding the typical premium for green construction. The enhanced indoor air quality achieved through advanced ventilation systems, low-emission materials, and improved filtration reduces sick building syndrome symptoms by up to 40%, resulting in decreased absenteeism and healthcare costs.

Commercial Green Construction Market Restraints and Challenges:

Despite significant growth momentum, the commercial green construction market faces several constraints that could impact its expansion trajectory. Higher upfront capital costs remain a primary barrier, with green buildings typically requiring 2-7% additional initial investment compared to conventional construction, creating challenges for cost-sensitive projects and organizations with limited capital budgets. The complexity of green building certification processes, including LEED, BREEAM, and other standards, can extend project timelines and increase administrative costs, particularly for smaller developers lacking specialized expertise. Skills shortages in sustainable construction practices and green building technologies create workforce constraints that can limit project execution capabilities and increase labor costs. Additionally, the fragmented nature of the construction industry makes it challenging to standardize green building practices across different regions and project types. Market perception issues persist, with some stakeholders remaining skeptical about the long-term financial benefits of green construction investments despite mounting evidence of positive returns. The lack of consistent regulatory frameworks across different jurisdictions creates complexity for multi-regional developers and can limit the scalability of green construction solution.

Commercial Green Construction Market Opportunities:

The commercial green construction market presents substantial opportunities across multiple dimensions as sustainability becomes increasingly central to business strategy and operations. The growing emphasis on corporate carbon neutrality commitments creates demand for net-zero energy buildings and carbon-negative construction materials, representing a premium market segment with higher profit margins. Retrofit and renovation of existing commercial buildings offers a massive addressable market, with an estimated $1.4 trillion in potential investment opportunities globally for energy efficiency improvements and sustainable system upgrades. The integration of smart building technologies with green construction creates opportunities for comprehensive building performance optimization, predictive maintenance, and advanced energy management systems that can deliver superior operational efficiency. Government infrastructure investments, particularly in healthcare, education, and public facilities, increasingly mandate green building standards, creating stable long-term demand for sustainable construction solutions.

Commercial Green Construction Market Segmentation:

Market Segmentation: By Product Type

• Insulation

• Roofing

• Framing

• Interior Finishing

• Exterior Siding

In 2024, HVAC systems dominated the commercial green construction market with approximately 24.8% revenue share, reflecting the critical importance of energy-efficient heating, ventilation, and air conditioning systems in achieving green building performance targets. Advanced HVAC technologies, including geothermal systems, variable refrigerant flow systems, and smart building controls, represent the largest investment category in most green construction projects due to their substantial impact on energy consumption and indoor environmental quality.

The solar panels segment is projected to grow at the fastest CAGR of 14.6% during the forecast period, driven by declining solar technology costs, improving efficiency ratings, and increasing corporate renewable energy procurement commitments. The integration of building-integrated photovoltaics (BIPV) and advanced energy storage systems is creating new opportunities for solar installations in commercial buildings, particularly as net-zero energy building requirements become more prevalent across various jurisdictions and building types.

Market Segmentation: By Application

• Commercial Buildings

• Institutional Buildings

• Industrial Buildings

Commercial buildings accounted for the largest market share of 52.3% in 2024, encompassing office buildings, retail facilities, hospitality properties, and mixed-use developments. This segment's dominance reflects the substantial commercial real estate market and the growing tenant demand for sustainable workspace environments that support employee health and productivity while reducing operational costs.

Institutional buildings represent the fastest-growing application segment with a projected CAGR of 12.4% during the forecast period. This growth is driven by government mandates for public building sustainability, healthcare facility requirements for improved indoor environmental quality, and educational institution commitments to environmental stewardship. The institutional segment also benefits from consistent funding sources and long-term operational perspectives that support higher initial investments in sustainable building systems.

Market Segmentation: By End-User

• Corporates

• Government

• Healthcare

• Education

• Retail

• Others

The corporate segment dominated the market with 38.7% share, driven by large corporations' sustainability commitments, ESG reporting requirements, and employee attraction and retention strategies. Corporate real estate strategies increasingly prioritize green building certifications as part of broader sustainability initiatives, with many companies establishing internal requirements for LEED Gold or Platinum certification for new facilities and major renovations.

The government segment is expected to witness the highest growth rate during the forecast period, with a CAGR of 13.8%. This growth is attributed to federal, state, and local government mandates for sustainable public buildings, substantial infrastructure investment programs, and the demonstration effect of government leadership in environmental stewardship. Government projects also benefit from specialized financing mechanisms and long-term operational perspectives that support comprehensive sustainable building investments.

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

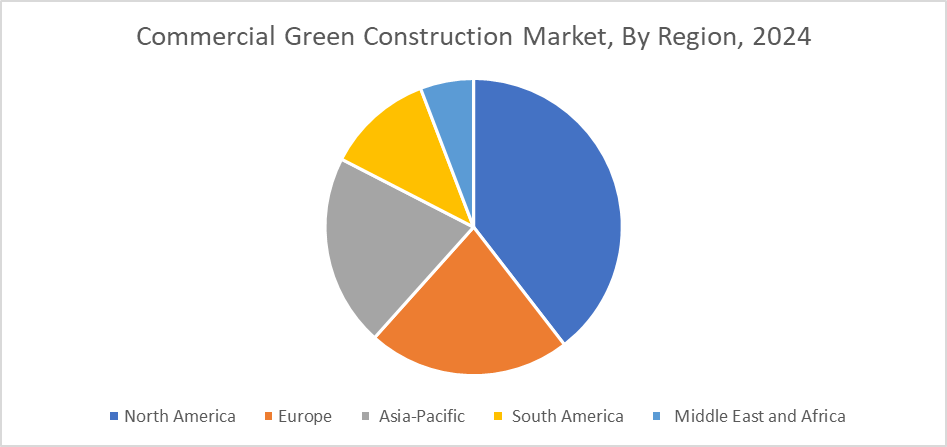

North America maintained its leadership position in the global commercial green construction market in 2024, accounting for 42.1% of the total market share. This dominance is attributed to mature green building certification programs, extensive government incentives, and strong corporate sustainability commitments. The United States leads with comprehensive LEED certification programs and substantial federal tax incentives for energy-efficient buildings, while Canada has implemented aggressive carbon reduction targets that drive sustainable construction adoption.

The Asia-Pacific region is anticipated to witness the highest growth rate during the forecast period, with a CAGR of 13.2%. This accelerated growth is driven by rapid urbanization, government sustainability initiatives, and increasing environmental awareness among businesses and consumers. China's commitment to carbon neutrality by 2060 and substantial investments in green building standards are creating significant market opportunities, while countries like Singapore, Australia, and Japan are implementing innovative green building policies that drive market adoption.

COVID-19 Impact Analysis on the Global Commercial Green Construction Market:

The COVID-19 pandemic initially disrupted construction activities worldwide, causing project delays and supply chain interruptions that temporarily slowed green construction market growth. However, the crisis ultimately accelerated interest in sustainable building practices as organizations recognized the connection between indoor environmental quality and occupant health. The pandemic highlighted the importance of advanced ventilation systems, air filtration technologies, and touchless building systems that are commonly featured in green building designs.

The shift toward remote and hybrid work models created new considerations for commercial building design, with emphasis on flexible spaces, enhanced indoor air quality, and energy-efficient systems that can adapt to variable occupancy patterns. Healthcare facilities emerged as a priority segment for green construction investments, with hospitals and medical facilities seeking to improve indoor environmental quality while reducing operational costs.

Latest Trends/ Developments:

The integration of artificial intelligence and machine learning into building management systems is revolutionizing green construction by enabling predictive maintenance, optimal energy usage patterns, and real-time performance optimization. Smart building technologies are becoming standard in green construction projects, with AI-powered systems capable of reducing energy consumption by an additional 15-20% beyond traditional green building performance levels through automated system adjustments and predictive analytics.

Net-zero energy building design is gaining significant traction as the next frontier in green construction, with major developers and corporations setting ambitious goals for carbon-neutral facilities. This trend is driving innovation in building-integrated renewable energy systems, advanced energy storage solutions, and ultra-efficient building envelope technologies that can achieve net-positive energy performance in various climate conditions and building types.

Key Players:

• AECOM

• Jacobs Engineering Group

• Fluor Corp

• Galfar Engineering

• Kimly Construction

• Soil build Construction

• Lum Chang

• The Turner Corp

• Clark Group

• DPR Construction

Chapter 1. Commercial Green Construction Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Commercial Green Construction Market – Executive Summary

2.1. Market End User & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Commercial Green Construction Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Commercial Green Construction Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Commercial Green Construction Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Commercial Green Construction Market – By Product

6.1. Introduction/Key Findings

6.2. Insulation

6.3. Roofing

6.4. Framing

6.5. Interior Finishing

6.6. Y-O-Y Growth trend Analysis By Product

6.7. Absolute $ Opportunity Analysis By Product, 2025-2030

Chapter 7. Commercial Green Construction Market – By Application

7.1. Introduction/Key Findings

7.2. Commercial Buildings

7.3. Institutional Buildings

7.4. Industrial Buildings

7.5. Y-O-Y Growth trend Analysis By Application

7.6. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Commercial Green Construction Market – By End User

8.1. Introduction/Key Findings

8.2. Corporate

8.3. Government

8.4. Healthcare

8.5. Y-O-Y Growth trend Analysis By End User

8.6. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 10. Commercial Green Construction Market, By Geography – Market End User, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Product

10.1.3. By Application

10.1.4. By End User

10.1.5. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product

10.2.3. By Application

10.2.4. By End User

10.2.5. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Product

10.3.3. By Application

10.3.4. By End User

10.3.5. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Product

10.4.3. By Application

10.4.4. By End User

10.4.5. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Product

10.5.3. By Application

10.5.4. By End User

10.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Commercial Green Construction Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. AECOM

11.2. Jacobs Engineering Group

11.3. Fluor Corp

11.4. Galfar Engineering

11.5. Kimly Construction

11.6. Soil build Construction

11.7. Lum Chang

11.8. The Turner Corp

11.9. Clark Group

11.10. DPR Construction

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Commercial Green Construction Market was valued at USD 707.4 billion in 2024 and is projected to reach a market size of USD 1,175.99 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 10.7%.

The implementation of stringent environmental regulations and building codes, coupled with increasing corporate sustainability commitments, are the primary drivers propelling the global commercial green construction market.

Based on Product Type, the Global Commercial Green Construction Market is segmented into Insulation, Roofing, Framing, Interior Finishing, Exterior Siding, HVAC Systems, Solar Panels, Water Management Systems, and Others.

North America is the most dominant region for the Global Commercial Green Construction Market.

Johnson Controls International, Siemens AG, Schneider Electric SE, and Honeywell International Inc. are the key players operating in the Global Commercial Green Construction Market.