Global Cloud Infrastructure Services Market Research Report – Segmentation by Service Type (IaaS, PaaS, CDN, Managed Hosting, Colocation); By Deployment (Public, Private, Hybrid); By Industry Vertical (BFSI, Retail, Healthcare, Manufacturing, IT & Telecom, Others); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-9411

Format:

Region: Global

Market Size and Overview:

The Cloud Infrastructure Services Market was valued at USD 320 billion in 2024. Over the forecast period of 2025-2030, it is projected to reach USD 689.67 billion by 2030, growing at a CAGR of 16.60%.

Key Market Insights:

The global market for Cloud Infrastructure Services is witnessing robust expansion, primarily fueled by the growing requirement for adaptable and scalable IT solutions. Enterprises are progressively implementing cloud-based technologies to streamline their operations and achieve cost efficiency.

One of the prominent drivers of this growth is the widespread adoption of remote work, which necessitates dependable and seamless access to data across various locations. This shift is encouraging organizations to utilize cloud platforms to foster enhanced collaboration and improved workflow productivity.

Furthermore, as businesses globalize, there is an increasing emphasis on standardizing IT systems to support international expansion and deliver consistent service across multiple regions.

Cloud Infrastructure Services Market Drivers:

Rising demand for scalable and flexible IT infrastructure continues to be a primary catalyst for market expansion.

The Global Cloud Infrastructure Services Market is experiencing notable growth, driven by a rising need for IT solutions that offer both scalability and flexibility. As reported by the International Data Corporation, nearly 90% of organizations worldwide intend to expand their use of cloud-based infrastructure to better accommodate fluctuating workload requirements. This surge is largely attributed to the growing shift toward remote work models and the demand for more agile and responsive business operations. Such advancements are enabling enterprises to optimize operational management and significantly accelerate time-to-market for new offerings. Furthermore, the increasing adoption of Infrastructure as a Service (IaaS) reflects the efforts of businesses to gain a strategic edge, thereby contributing to the continued expansion of the Global Cloud Infrastructure Services Market.

The evolution of operational models to harness the capabilities of generative AI is emerging as a key driver of market growth.

According to a survey conducted by PwC, approximately 70% of business leaders consider artificial intelligence to be essential for driving future business opportunities. In this context, generative AI has emerged as a transformative force within cloud infrastructure. It plays a pivotal role in enhancing security across cloud environments by enabling the detection of potential threats through the analysis of large and complex datasets. By anticipating cyber risks before they manifest, generative AI supports the implementation of proactive defense strategies, thereby fortifying cloud systems against a range of cyber threats, including malware, intrusions, and advanced persistent attacks. Beyond security, generative AI also contributes to improving operational efficiency, making it a critical enabler for modernizing cloud infrastructure.

Cloud Infrastructure Services Market Restraints and Challenges:

Constraints in customization capabilities may pose challenges to the expansion of the Cloud Infrastructure Services Market.

The lack of customization for specific workloads has emerged as a significant constraint in the Cloud Infrastructure Services Market. Standardized, one-size-fits-all cloud solutions often fall short in addressing the unique and highly specialized computing requirements of certain industries. Organizations operating in niche domains—such as advanced simulations or scientific research—frequently demand tailored configurations that are not easily accommodated within conventional cloud frameworks. This limitation hampers the broader adoption of cloud services in sectors where bespoke solutions are critical to achieving optimal efficiency and performance.

Cloud Infrastructure Services Market Opportunities:

The growing adoption of hybrid and multi-cloud strategies is serving as a key driver for the expansion of the Cloud Infrastructure Services Market.

Amid rising cloud resource costs, market participants are increasingly adopting strategies aimed at minimizing inefficiencies and reducing unnecessary expenditures. Research indicates that approximately 90% of large enterprises have already implemented multicloud architectures, distributing their data across multiple cloud service providers. The adoption of hybrid and multi-cloud environments represents a continuing trend in cloud computing, expected to gain further momentum through 2024 and beyond. These models enable optimized workload distribution by ensuring that applications and services are deployed within the most appropriate cloud environments. This strategic framework enhances operational flexibility, mitigates risks, and strengthens the overall management of IT infrastructure.

Multi-cloud architecture is becoming the standard for modern enterprises, offering enhanced control over data privacy and improved alignment with regulatory requirements related to data sovereignty. By leveraging independent cloud platforms, organizations can better address compliance mandates while maintaining a resilient and adaptable infrastructure strategy.

Cloud Infrastructure Services Market Segmentation:

By Service type:

● Compute as a Service (CaaS)

● Storage as a Service (STaaS)

● Disaster Recovery & Backup as a Service (DRaaS)

● Networking as a Service (NaaS)

● Desktop as a Service (DaaS)

● Managed Hosting Services (MHS)

● Content Delivery Services (CDS)

The Compute as a Service segment held the largest share of the market. This service model enables enterprises to swiftly deploy and manage containers, allowing for on-demand scalability of applications. It also facilitates efficient allocation of computing resources such as CPU, memory, and storage, tailored to specific application requirements. Additionally, Compute as a Service offers APIs that support automation and management of container-related operations, streamlining overall IT processes.

The Network as a Service (NaaS) segment is projected to register the highest compound annual growth rate (CAGR) during the forecast period. NaaS provides real-time network monitoring and proactive maintenance capabilities, helping identify and address performance issues, such as elevated latency levels at specific locations. This model offers a modern, more flexible alternative to traditional networking solutions like virtual private networks (VPNs) and multiprotocol label switching (MPLS), thereby improving network agility and operational efficiency.

Meanwhile, Software as a Service (SaaS) continues to maintain a strong market presence. Its popularity stems from its user-friendly and accessible nature, enabling organizations to utilize software applications via subscription without the burden of managing updates or infrastructure. The growing demand for scalable and easily integrable software solutions has fueled SaaS adoption across a broad range of industries, attracting a wide customer base seeking streamlined and cost-effective digital transformation.

By Deployment model:

● Public Cloud

● Private Cloud

● Hybrid Cloud

The Public Cloud continues to experience growing adoption, driven by its scalability, cost-efficiency, and wide accessibility—qualities that make it a preferred deployment model for organizations across the globe. Conversely, the Private Cloud offers greater control, enhanced security, and dedicated infrastructure, making it an attractive option for industries with stringent regulatory requirements and a need for robust data governance.

The Hybrid Cloud distinguishes itself through its ability to combine the strengths of both public and private models. This approach provides businesses with the flexibility to distribute workloads across environments, optimize resource utilization, and implement effective disaster recovery mechanisms.

Ongoing technological advancements and innovations in cloud services are creating new opportunities to enhance service delivery and operational performance. However, the market continues to face challenges such as data security risks and complexities in integrating diverse cloud environments. The increasing shift towards remote work and the proliferation of cloud-native applications underscore the critical role of these deployment models in establishing a resilient and scalable digital infrastructure on a global scale.

By Organization Size:

● Small and Medium-sized Enterprises (SMEs)

● Large Enterprises

Small and Medium Enterprises (SMEs) are increasingly utilizing cloud services to boost adaptability and improve operational efficiency, contributing significantly to the segment's expansion. In contrast, Large Enterprises continue to dominate the market, driven by their complex service requirements, larger data volumes, and greater capacity to invest in advanced infrastructure solutions.

The Government sector is also emerging as a key contributor, leveraging cloud technologies to optimize internal processes, enhance the delivery of public services, and strengthen data security protocols. Market insights reveal a growing inclination toward hybrid cloud models, allowing organizations to strike a balance between operational flexibility and stringent security requirements.

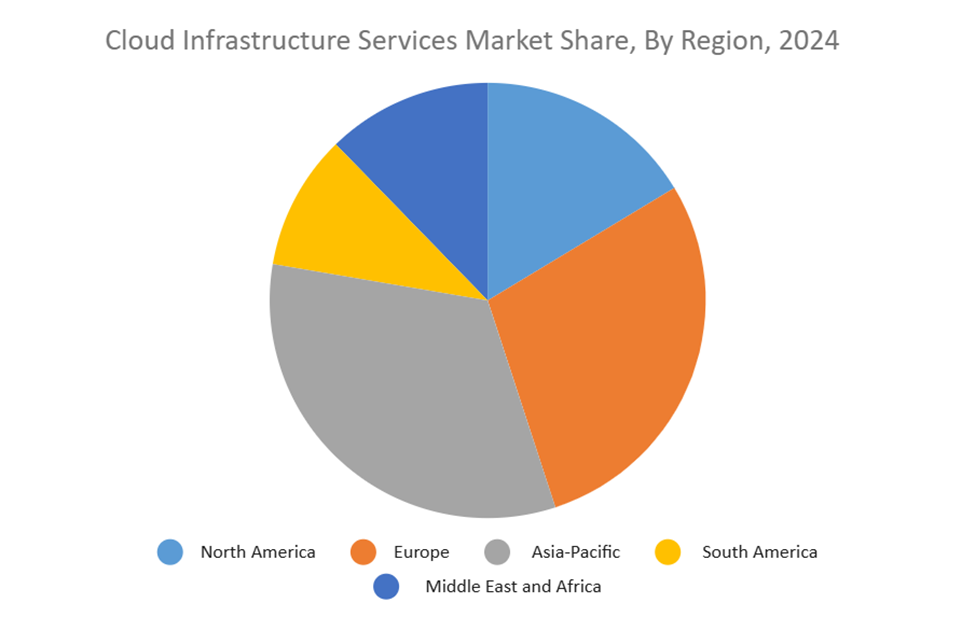

Cloud Infrastructure Services Market Segmentation- by region

● North America

● Europe

● Asia Pacific

● South America

● Middle East & Africa

North America led the market in terms of revenue, driven by the widespread digitization of enterprises across the region. The U.S. Federal Cloud Computing Strategy, through the implementation of the Cloud First policy, has significantly accelerated the adoption of cloud technologies. Approximately 94% of enterprises in the U.S. and 88% in Canada have adopted at least one form of cloud deployment, with multi-cloud and hybrid models being the most prevalent.

The Asia Pacific region is expected to register the highest compound annual growth rate (CAGR) over the forecast period. According to RedHat, 87% of executives in Japan reported full adoption of cloud computing, while 68% of respondents in Singapore confirmed complete cloud integration within their organizations. In India, cloud-related investments surged during the pandemic, with the market anticipated to reach approximately USD 13 billion by 2025. These increasing investments across countries in the region are playing a critical role in driving overall market growth.

Europe is also witnessing notable expansion, supported by proactive investments from both governmental bodies and private enterprises aimed at accelerating cloud adoption. As reported by Eurostat, nearly 73% of European enterprises are utilizing advanced cloud services for application security and cloud-based development platforms, contributing to the region’s strong market performance.

COVID-19 Pandemic: Impact Analysis

The COVID-19 pandemic acted as a catalyst for digital transformation, prompting small, medium, and large enterprises to migrate their workloads to the cloud and adopt productivity and collaboration tools. The shift to remote work further underscored the critical role of cloud technologies in ensuring business continuity. According to a Flexera survey, 27% of industry leaders observed a substantial increase in cloud-related expenditures directly resulting from the pandemic. These developments significantly accelerated the demand for cloud infrastructure services, positioning the cloud as a foundational element in modern enterprise operations.

Latest Trends/ Developments:

March 2024 – Fujitsu Limited expanded its collaboration with Amazon Web Services (AWS) to accelerate the modernization of legacy applications, leveraging the AWS cloud platform to enhance scalability and performance.

September 2023 – Oracle and Microsoft deepened their strategic alliance to offer Oracle Database Services, aimed at simplifying cloud migration processes and enabling seamless multicloud deployment and management for enterprise clients.

May 2023 – IBM Corporation unveiled IBM Hybrid Cloud Mesh, a solution designed to assist organizations in managing hybrid multi cloud environments.

May 2023 – VMware launched VMware Cross-Cloud Managed Services, an offering intended to improve partner profitability and drive growth in recurring revenue streams by supporting cross-cloud service delivery and management.

Key Players:

These are top 10 players in the Cloud Infrastructure Services Market :-

CloudHesive

Amazon Web Services, Inc.

DigitalOcean

Coastal Cloud

Alibaba Cloud

GroundCloud

Google

Microsoft Azure

IBM

Oracle Cloud

Chapter 1. Cloud Infrastructure Services Market – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Cloud Infrastructure Services Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Cloud Infrastructure Services Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Cloud Infrastructure Services Market - Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Cloud Infrastructure Services Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Cloud Infrastructure Services Market – By Service type

6.1. Compute as a Service (CaaS)

6.2. Storage as a Service (STaaS)

6.3. Disaster Recovery & Backup as a Service (DRaaS)

6.4. Networking as a Service (NaaS)

6.5. Desktop as a Service (DaaS)

6.6. Managed Hosting Services (MHS)

6.7. Content Delivery Services (CDS)

6.8. Y-O-Y Growth trend Analysis By Service Type

6.9. Absolute $ Opportunity Analysis By Service Type, 2024-2030

Chapter 7. Cloud Infrastructure Services Market – By Deployment model

7.1. Public Cloud

7.2. Private Cloud

7.3. Hybrid Cloud

7.4. Y-O-Y Growth trend Analysis By Deployment model

7.5. Absolute $ Opportunity Analysis By Deployment model, 2024-2030

Chapter 8. Cloud Infrastructure Services Market – By Organization Size

8.1. Small and Medium-sized Enterprises (SMEs)

8.2. Large Enterprises

8.3. Y-O-Y Growth trend Analysis By Organization Size

8.4. Absolute $ Opportunity Analysis By Organization Size, 2024-2030

Chapter 9. Cloud Infrastructure Services Market, By Geography – Market Size, Forecast, Trends & Insights

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Service type

9.1.3. By Deployment Model

9.1.4. By Organization Size

9.1.5. Countries & Segments – Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Service type

9.2.3. By Deployment Model

9.2.4. By Organization Size

9.2.5. Countries & Segments – Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Service type

9.3.3. By Deployment Model

9.3.4. By Organization Size

9.3.5. Countries & Segments – Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By Service type

9.4.3. By Deployment Model

9.4.4. By Organization Size

9.4.5. Countries & Segments – Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By Service type

9.5.3. By Deployment Model

9.5.4. By Organization Size

9.5.5. Countries & Segments – Market Attractiveness Analysis

Chapter 10. Cloud Infrastructure Services Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

10.1. Microsoft Corporation

10.2. Palo Alto Networks

10.3. Zscaler, Inc

10.4. CrowdStrike

10.5. BeyondTrust Corporation

10.6. Check Point Software Technologies Ltd

10.7. NextLabs

10.8. SailPoint Technologies

10.9. Orca Security

10.10. CyberArk

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Enterprises are progressively implementing cloud-based technologies to streamline their operations and achieve cost efficiency.

The top players operating in the Cloud Infrastructure Services Market are - CloudHesive, Amazon Web Services, Inc. and DigitalOcean.

The COVID-19 pandemic acted as a catalyst for digital transformation, prompting small, medium, and large enterprises to migrate their workloads to the cloud and adopt productivity and collaboration tools.

These models enable optimized workload distribution by ensuring that applications and services are deployed within the most appropriate cloud environments. This strategic framework enhances operational flexibility, mitigates risks, and strengthens the overall management of IT infrastructure

Asia Pacific is the fastest-growing region in the Cloud Infrastructure Services Market.