Global Banking As A Service Market Research Report – Segmentation by Type (API-based and Cloud-based); By Application (Digital Banking, Payment Processing, Lending, Banking Compliance, Account & Transaction Management, Card Issuance); By Enterprise (Large Enterprise and SMEs); By End Use (Banks, NBFC, Others); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16496

Format:

Region: Global

Market Size and Overview:

The Global Banking As A Service Market was valued at USD 18.6 billion in 2024 and is projected to reach a market size of USD 55.41 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 24.3%.

The Banking-as-a-Service (BaaS) market represents a transformative shift in the financial services industry, enabling non-bank businesses to offer banking products and services through APIs and licensed financial institutions. By leveraging BaaS platforms, fintechs, e-commerce companies, and other digital enterprises can seamlessly integrate capabilities like payments, lending, digital wallets, and account management into their applications without owning a banking license. This model not only reduces entry barriers but also accelerates innovation and enhances customer experience. As need for embedded finance grows, BaaS is reshaping how banking is delivered, fostering greater collaboration between traditional banks and technology-driven companies.

Key Market Insights:

The adoption of Banking-as-a-Service is accelerating rapidly, with over 70% of fintechs globally integrating BaaS platforms to deliver seamless financial services. This reflects a rising preference for API-driven, modular banking solutions that reduce time-to-market and allow greater product customization. The shift is especially prominent in digital-first businesses aiming to enhance user experience through embedded finance features.

A recent global survey showed that 6 out of 10 consumers prefer financial services offered directly by non-banking platforms they already use, such as retail or ride-hailing apps. This trend is fueling the demand for BaaS infrastructure, enabling non-financial companies to meet evolving customer expectations with flexible and accessible financial tools.

Additionally, more than 80% of traditional banks are either partnering with or planning to collaborate with BaaS providers to expand their digital offerings. These partnerships help banks stay competitive, extend their reach, and generate new revenue streams without the need for building new technology stacks from scratch.

Banking As A Service Market Drivers:

The Rising Demand for Embedded Finance Is Fueling the Rapid Growth of BaaS

One of the most significant drivers of the Banking-as-a-Service (BaaS) market is the surging demand for embedded finance, where banking services are seamlessly integrated into non-banking platforms like e-commerce apps, ride-hailing services, and digital marketplaces. Consumers now expect frictionless financial experiences that fit naturally within their daily digital interactions—whether it's making payments, applying for credit, or managing digital wallets. This trend is pushing businesses across industries to incorporate banking capabilities without becoming licensed banks themselves. As a result, BaaS providers enable faster go-to-market timelines and lower compliance burdens, allowing companies to offer tailored financial services that enhance customer loyalty and engagement.

The Growing Fintech Ecosystem and Startup Culture Are Creating a Strong Foundation for BaaS

The explosive growth of the fintech sector is another strong catalyst fueling the expansion of the BaaS market. Thousands of startups and digital-first businesses are entering the financial services space, and BaaS offers them a cost-effective, scalable, and regulation-compliant infrastructure. These companies can focus on user experience, product design, and branding, while the underlying banking functions—such as KYC, card issuance, and transaction management—are handled by BaaS platforms. This decoupling of front-end innovation from back-end complexity enables faster innovation cycles and reduces technical overhead, making it easier for small players to compete with established banks.

Regulatory Support and Open Banking Initiatives Are Accelerating BaaS Adoption Worldwide

Supportive regulations and open banking initiatives in regions like Europe, Asia-Pacific, and parts of North America have created a fertile environment for BaaS to thrive. By requiring banks to share data securely with third-party providers, open banking frameworks have paved the way for BaaS models to emerge and evolve. Regulators are increasingly recognizing the potential of BaaS to promote financial inclusion, improve competition, and drive innovation in financial services. As trust in API-driven services increases and licensing structures become clearer, both new entrants and traditional financial institutions are embracing BaaS as a strategic growth channel.

Strategic Partnerships Between Banks and Tech Firms Are Driving Ecosystem Expansion

Another key driver of the BaaS market is the rise in strategic partnerships between legacy banks and technology firms. Rather than competing head-on with fintech startups, many traditional banks are leveraging BaaS to extend their reach, tap into new customer segments, and modernize their digital offerings. These collaborations allow banks to monetize their core infrastructure by offering it as a service, while tech firms gain credibility and access to regulated banking rails. As these partnerships grow, they foster a robust BaaS ecosystem where innovation, speed, and compliance can coexist—ultimately benefiting businesses and end-users alike.

Banking As A Service Market Restraints and Challenges:

Regulatory Complexities and Security Concerns Pose Major Challenges to BaaS Expansion

Despite its rapid growth, the Banking-as-a-Service (BaaS) market faces significant restraints, primarily because of the complex regulatory landscape and heightened concerns around data privacy and cybersecurity. Navigating compliance across different jurisdictions is challenging, especially for global BaaS providers and their partners who must adhere to varying banking, anti-money laundering (AML), and consumer protection laws. Additionally, the increasing reliance on APIs and third-party integrations introduces potential vulnerabilities, making security breaches and data misuse a critical concern. Without robust governance frameworks and trust-building measures, these issues may slow adoption and limit partnerships between traditional banks and non-financial platforms.

Banking As A Service Market Opportunities:

The Banking-as-a-Service (BaaS) market holds immense opportunities as demand grows for digital-first, personalized, and easily accessible financial services across industries. With increasing smartphone penetration, the expansion of internet infrastructure, and increasing consumer comfort with digital payments, BaaS providers have the chance to tap into vast underserved and unbanked populations, especially in emerging markets. Additionally, sectors like retail, travel, healthcare, and logistics are increasingly looking to integrate financial services into their ecosystems, opening up new revenue channels. As technology evolves and regulations become more BaaS-friendly, providers that offer secure, scalable, and API-rich platforms are well-positioned to lead the next phase of embedded banking innovation.

Banking As A Service Market Segmentation:

Market Segmentation: By Type:

• API-based

• Cloud-based

API-based Banking-as-a-Service has emerged as the dominant segment in the market, enabling seamless integration of financial services into third-party platforms with high flexibility and scalability. Through standardized APIs, businesses can quickly embed services such as payments, KYC verification, digital lending, and account management without having to build banking infrastructure from scratch. This model has gained strong momentum among fintechs, e-commerce companies, and startups that prioritize speed-to-market and user experience. The API-based approach also ensures faster innovation, allowing businesses to adapt and launch new features efficiently, making it the preferred choice for companies aiming to stay competitive in a rapidly evolving financial ecosystem.

Cloud-based BaaS platforms represent the fastest-growing segment, offering end-to-end financial solutions that are hosted, managed, and updated in real-time. With minimal on-premise infrastructure requirements and the ability to scale resources as needed, cloud-based solutions have become increasingly attractive to enterprises seeking agility, cost-effectiveness, and global reach. These platforms allow for centralized data management, high availability, and improved security protocols, making them ideal for businesses looking to handle large volumes of financial transactions. As data compliance and uptime become mission-critical in financial services, the cloud model ensures BaaS providers can meet performance and regulatory demands with greater efficiency.

Market Segmentation: By Application:

• Digital Banking

• Payment Processing

• Lending

• Banking Compliance

• Account & Transaction Management

• Card Issuance

Digital banking is the dominant application segment in the Banking-as-a-Service market, driven by the rising demand for seamless, user-centric, and 24/7 accessible financial services. BaaS enables non-banking platforms like neobanks, fintech apps, and digital marketplaces to offer core banking features such as opening accounts, fund transfers, and managing balances without needing a banking license. As consumers move away from traditional brick-and-mortar branches, the appeal of instant, mobile-based banking services has skyrocketed. This surge has led to increased reliance on BaaS infrastructure by challenger banks and tech-driven financial institutions to deliver banking experiences that are both innovative and regulation-compliant.

Payment processing and lending are among the fastest-growing applications of BaaS, as businesses increasingly look to offer integrated, low-friction financial transactions within their ecosystems. From in-app purchases to point-of-sale systems and digital lending solutions, BaaS provides the infrastructure to facilitate fast, secure, and scalable payment options and credit offerings. For example, retail companies and ride-sharing apps can now offer instant loans, “buy now, pay later” features, or branded payment methods by leveraging BaaS platforms. Additionally, the ability to manage card issuance, real-time account data, and transaction histories through embedded services has accelerated the adoption of BaaS across multiple sectors.

Market Segmentation: By Enterprise:

• Large Enterprise

• Small and Medium Enterprise (SMEs)

Large enterprises are the dominant users of Banking-as-a-Service (BaaS) platforms, leveraging their extensive customer bases and technological infrastructure to integrate advanced financial features directly into their ecosystems. These corporations—ranging from multinational e-commerce giants to global tech firms—are increasingly adopting BaaS to offer services like digital wallets, in-app banking, and card issuance without building complex financial back-ends. Their strategic investments in digital transformation, compliance systems, and cross-border scalability give them an edge in deploying BaaS at scale.

Small and Medium Enterprises (SMEs) represent the fastest-growing segment in the BaaS market, driven by their desire to innovate, compete, and diversify revenue streams. Unlike large corporations, SMEs typically lack the resources to build traditional banking capabilities from the ground up. BaaS solves this challenge by offering modular, API-first financial services that are affordable, scalable, and easy to implement. From offering credit facilities to automating payments and onboarding digital wallets, SMEs are using BaaS to modernize their operations and reach broader customer segments. The rise of SME-focused fintech startups and digital platforms has further fueled BaaS adoption, enabling smaller firms to act like fintechs without the burden of banking licenses or regulatory complexity.

Market Segmentation: By End Use:

• Banks

• NBFC

• Others

Banks are the dominant end users of Banking-as-a-Service (BaaS), leveraging it as a strategic tool to modernize their legacy systems, expand digital capabilities, and reach new customer bases through embedded finance. Rather than competing with fintech startups, many traditional banks are partnering with BaaS providers to offer their infrastructure as a service, enabling third-party platforms to access regulated financial products. This not only creates new revenue streams but also helps banks maintain relevance in an increasingly digital-first world. With BaaS, banks can operate more like technology companies—agile, scalable, and data-driven—while preserving regulatory compliance and customer trust.

Non-Banking Financial Companies (NBFCs) and others are the fastest-growing users in the BaaS ecosystem, taking advantage of its flexibility to deliver specialized financial products without needing a full banking license. NBFCs are increasingly using BaaS to embed payment solutions, credit offerings, and digital wallets into their platforms, helping them improve operational efficiency and user experience. Additionally, sectors such as retail, travel, and healthcare are rapidly integrating BaaS capabilities to offer embedded financial services that enhance customer engagement and retention. These diverse use cases beyond traditional financial institutions highlight the expanding scope of BaaS, as it becomes a foundational layer for digital transformation across industries.

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

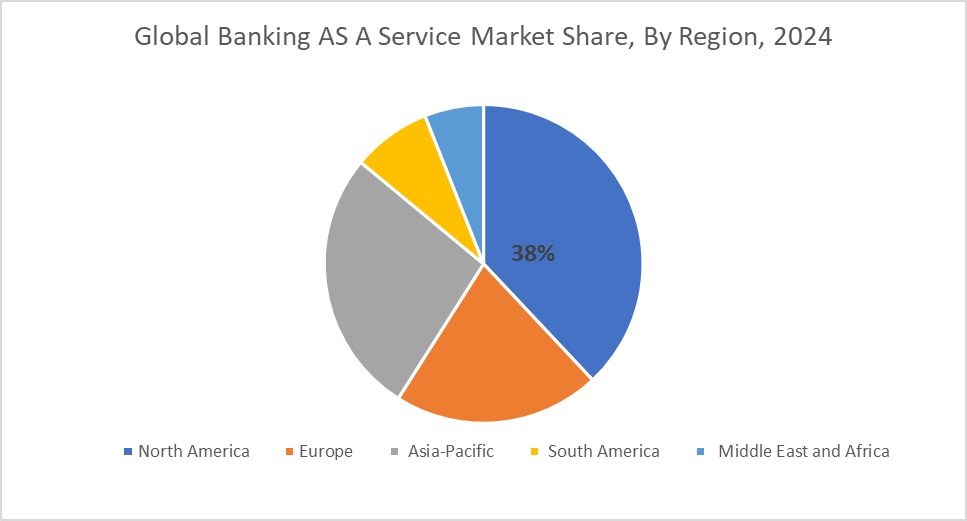

North America is the dominant region in the Banking-as-a-Service (BaaS) market, contributing 38% to the global share. The region benefits from a mature financial ecosystem, high digital adoption, and a strong presence of fintech startups and technology-driven banks. U.S.-based companies have been at the forefront of integrating BaaS into e-commerce, digital payments, and mobile banking apps, fostering widespread acceptance. With well-defined regulatory frameworks and a highly competitive fintech landscape, North America continues to lead in innovation, partnerships, and platform-based banking models, making it the most established and influential market for BaaS globally.

Asia-Pacific is the fastest-growing region, accounting for 27% of the market. Rapid digital transformation across emerging economies, coupled with rising smartphone penetration and increased financial inclusion efforts, has made the region a fertile ground for BaaS adoption. Countries like India, China, and Southeast Asian nations are witnessing a rise in digital-first banking models, with both startups and traditional financial institutions embracing BaaS to tap into large unbanked populations. Government-backed open banking regulations, fintech-friendly policies, and a young, tech-savvy population are further accelerating the expansion of BaaS platforms across the Asia-Pacific region.

COVID-19 Impact Analysis on the Global Banking As A Service Market:

The COVID-19 pandemic significantly accelerated the growth of the Banking-as-a-Service (BaaS) market by pushing both consumers and businesses toward digital-first financial solutions. As physical banking became restricted, demand surged for online banking, contactless payments, and embedded finance, prompting traditional banks and fintechs to rapidly adopt BaaS models. The crisis highlighted the importance of agility and scalability in financial services, encouraging companies across industries to integrate BaaS platforms to stay connected with customers, enhance service delivery, and ensure business continuity in a contactless economy.

Latest Trends/ Developments:

One of the key trends reshaping the Banking-as-a-Service (BaaS) market is the rapid integration of embedded finance into non-financial platforms such as e-commerce, ride-sharing, and healthcare apps. Businesses across industries are embedding financial services like lending, insurance, payments, and digital wallets directly into their customer journeys using BaaS infrastructure. This trend is empowering brands to deliver seamless, value-added services while increasing customer retention and unlocking new revenue streams. Additionally, white-label banking solutions are becoming more popular, enabling companies to launch customized financial products without building or owning the underlying banking infrastructure.

Another major development is the rising adoption of real-time APIs and open banking protocols that enable faster onboarding, instant payments, and smoother KYC/AML compliance processes. These advancements are driving innovation in neobanking and challenger bank ecosystems, where speed and user experience are crucial differentiators. Moreover, strategic partnerships between traditional banks and fintech startups are increasing, allowing legacy institutions to stay competitive by offering modern digital experiences through BaaS platforms. With growing investor interest and evolving regulatory frameworks, the BaaS space is becoming a key enabler of financial democratization and digital transformation globally.

Key Players:

• Green Dot Bank

• Solarisbank AG

• PayPal Holdings, Inc.

• Fidor Solutions AG

• Moven Enterprise

• The Currency Cloud Ltd.

• Treezor

• Bnkbl Ltd.

• MatchMove Pay Pte Ltd.

• Block, Inc.

Chapter 1. Global Banking As A Service Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Banking As A Service Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Banking As A Service Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Banking As A Service Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Banking As A Service Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Banking As A Service Market – By Type

6.1. API-based

6.2. Cloud-based

6.3. Y-O-Y Growth trend Analysis By Type

6.4. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 7. Global Banking As A Service Market – By Application

7.1. Digital banking

7.2. Payment Processing

7.3. Lending

7.4. Banking Compliance

7.5. Account & Transaction Management

7.6. Card Issuance

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Banking As A Service Market – By Enterprise

8.1. Large Enterprise

8.2. Small and Medium Enterprise (SMEs)

8.3. Y-O-Y Growth trend Analysis By Enterprise

8.4. Absolute $ Opportunity Analysis By Enterprise, 2025-2030

Chapter 9. Global Banking As A Service Market – By End Use

9.1. Banks

9.2. NBFC

9.3. Others

9.4. Y-O-Y Growth trend Analysis By End Use

9.5. Absolute $ Opportunity Analysis By End Use, 2025-2030

Chapter 10. Global Banking AS A Service Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Application

10.1.4. By Enterprise

10.1.5. By End Use

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Application

10.2.4. By Enterprise

10.2.5. By End Use

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Type

10.3.3. By Application

10.3.4. By Enterprise

10.3.5. By End Use

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Application

10.4.4. By Enterprise

10.4.5. By End Use

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Application

10.5.4. By Enterprise

10.5.5. By End Use

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Banking As A Service Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1 Green Dot Bank

11.2 Solarisbank AG

11.3 PayPal Holdings, Inc.

11.4 Fidor Solutions AG

11.5 Moven Enterprise

11.6 The Currency Cloud Ltd.

11.7 Treezor

11.8 Bnkbl Ltd.

11.9 MatchMove Pay Pte Ltd.

11.10 Block, Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Banking As A Service Market was valued at USD 18.6 billion in 2024 and is projected to reach a market size of USD 55.41 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 24.3%.

Growing demand for embedded finance and digital banking solutions.

Based on Type, the Global Banking As A Service Market is segmented into API-based and Cloud-based.

North America is the most dominant region for the Global Banking As A Service Market.

Green Dot Bank, Solarisbank AG, PayPal Holdings are the leading players in the Global Banking As A Service Market.