Global Artificial Intelligence (AI) Supercomputer Market Research Report – Segmentation By Component (Hardware, Software, Services), By Application (Model Training, Inference, High Performance Computing & Research, Others), By End-Use Industry (Healthcare, Automotive, Financial services, Retail, Government & Defense, Academia & Research, Others), By Deployment Mode (On-premises, Cloud-based, Hybrid), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16482

Format:

Region: Global

Market Size and Overview:

The Global Artificial Intelligence (AI) Supercomputer Market was valued at USD 2.56 billion and is projected to reach a market size of USD 6.13 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 19.07%.

Powered by cutting-edge GPUs, customized ASICs, high-bandwidth memory, and extremely low-latency interconnects, these systems are essential for training large language models, real-time inference, scientific simulations, and sophisticated data analysis. Growing demand from hyperscale cloud providers, national labs, and AI-driven companies is encouraging ongoing investments in next-generation supercomputing infrastructure, therefore boosting both on-premises installations and cloud-based HPC services.

Key Market Insights:

About 70% of total market revenue is accounted for by GPUs, NPUs, and interconnects, hardware for AI supercomputers, as companies give raw processing power and specialized accelerators above software and services.

Exponential increase in model sizes, from millions of parameters to hundreds of billions, drives training deep-learning models, which takes the largest part (approximately 45%) of artificial intelligence supercomputing jobs.

About 18% of the market is healthcare applications, including drug discovery, genomics, and medical‑image analysis, as life-science companies use supercomputers to speed precision medicine research.

Driven by significant artificial intelligence R&D, hyper-scale cloud supercomputer debuts, and government-supported exascale projects, North America generates 38% of market revenues.

Artificial Intelligence (AI) Supercomputer Market Drivers:

The recent proliferation of generative AI and Large Language Models (LLMs) is driving the growth of this market.

Driven by transformer-based systems like GPT-4 (1 8 trillion parameters) and multi-modal models (e.g., Stable Diffusion, Gemini), the explosive growth of generative AI has completely changed supercomputing needs. According to Jensen Huang, GPT-4's basic pre‑training used three months on 8,000 NVIDIA H100 GPUs, equal to 20,000 A100s, yielding continuous petaflops of computing to handle 10 trillion tokens. Training times on commodity clusters become untenable as companies chase ever bigger models, pushing into the trillions-to-quadrillions of parameters epoch. This has driven procurement of dedicated AI supercomputers with dense GPU pods, tailored ASIC accelerators, and super-low-latency fabrics capable of compressing weeks to months of training into days or hours. Further increasing demand for scalable, high-performance artificial intelligence supercomputing infrastructure, open-source communities and businesses alike started refining multi-modal "foundation" models over voice, vision, and code in 2024.

The initiatives taken by national and enterprise exascale are seen as major market growth drivers.

With flagship systems like the U. S. DOE's Aurora (1,012 exaFLOPS Rmax; deployed Nov 2023) and El Capitan (1,742 exaFLOPS Rmax; operational Nov 2024)—proving the viability of continuous exaflops performance—exascale computing has become a worldwide strategic need. Europe's EuroHPC JU machines (e.g., LUMI, Leonardo) and China's forthcoming Tianhe successors likewise target the exascale barrier. In addition to furthering scientific investigation, these national-scale deployments establish performance standards that fuel commercial supercomputer upgrades. Particularly in life sciences and financial sectors, businesses seek to emulate exascale-class capability inside their private data centers or through enterprise-grade cloud offerings made possible by public-private partnerships such as the DOE Exascale Computing Project, which co-funds hardware, building, and software ecosystem development.

The cloud-based HPC Services have seen a massive expansion globally, which is developing this market.

On‑demand HPC instances and managed artificial intelligence supercomputer clusters from hyperscale cloud providers have changed supercomputing access. Driven by AI/ML, big‑data analytics, and the need for scalable compute without CAPEX burdens, Mordor Intelligence estimates the Cloud HPC market will expand from USD 11. 56 billion in 2025 to USD 18 billion. 86 billion by 2030 at a 10.29 percent CAGR. Global Industry Analysts projects an even faster trajectory, USD 12.5 billion in 2024 to USD 31 billion. 1 billion by 2030 at 16.5 percent CAGR. Startups, colleges, and companies can now swiftly create thousands of GPU/ASIC accelerators, elastically grow training and inference demands, and pay just for use. By means of this democratization of AI supercomputing, time-to-insight is quickened and innovation obstacles are decreased.

The increasing adoption of cross-industry HPC beyond the tech industry is bringing innovation to the market.

AI supercomputing is not limited to hyperscalers and national labs. Automotive manufacturers use HPC clusters for digital‑twin simulations, aerodynamic CFD, and autonomous‑driving scenario creation; financial services companies utilize supercomputers for high‑frequency trading back‑testing, credit‑risk Monte Carlo simulations, and fraud‑detection model training; retailers depend on HPC for supply‑chain optimization, dynamic pricing simulations, and extensive customer‑behavior analytics. Life‑sciences companies, energy firms, and government research organizations also tap supercomputer power for genomics, materials discovery, and climate modeling. This expansion of use cases highlights the competitive edge provided by in-house or on-demand artificial intelligence supercomputing power over practically all industry verticals.

Artificial Intelligence (AI) Supercomputer Market Restraints and Challenges:

The capital and operational expenditure is very high, which is a major challenge for this market.

The cost of AI supercomputers is astronomical: Epoch AI data reveals that the most expensive cluster in mid-2025 (xAI’s Colossus) consumed over USD 7 billion just for hardware, following an annual cost doubling rate of 1.9× since 2019. Beyond purchase, constant operating costs—power, cooling, facilities, and maintenance- might push total cost of ownership (TCO) to more than USD 500,000 per rack annually, driven by tens of megawatts of continuous power draw and special liquid‑cooling infrastructure. Global data‑center expenditures to match AI demand would surpass USD 6.7 trillion by 2030, emphasizing the capital intensity of sustaining exascale-class systems. These significant upfront and continuing expenditures restrict AI supercomputer ownership to national labs, hyperscale cloud companies, and deep-pocketed businesses, therefore restricting more general market penetration, even if there are obvious performance advantages.

The market faces constraints regarding power and cooling, which hamper market operation.

TechCrunch estimates that by 2030, next-generation AI supercomputers could need up to 9 GW of electricity, about nine nuclear reactors. Maintaining even smaller‑scale exascale systems (10–30MW) calls for sophisticated liquid‑cooling or immersion‑cooling solutions, therefore raising capital costs for facility renovations and custom plumbing by 20–30%. Lacking the grid capacity to handle such loads, urban campuses compel new deployments to find isolated locations with access to dedicated substations or renewable energy sources. By 2030, data center energy demand is projected to rise 20%, hence increasing the stress on the electricity infrastructure and raising questions regarding sustainability and carbon footprints. Consequently, even businesses with enough funding have to strike a delicate balance between performance goals and energy‑and‑facility limitations, frequently delaying acquisition or selecting for smaller, modular systems.

The problem of talent shortage in the fields of AI and HPC is a great challenge for this market.

Running and perfecting artificial intelligence supercomputers call for rare skills in parallel programming (MPI, CUDA), HPC system administration, and large-model scaling. According to Rescale, 95% of tech managers have difficulties locating talent with the most recent HPC/AI skills, and 65% see increasingly poor skill gaps year over year. Many companies depend on expensive outside advisors or managed-service partnerships without in-house experts, which can raise project costs 30 to 40% and lengthen time-to-value by months. In specialized fields like HPC networking and liquid‑cooling activities, where hands‑on experience is crucial, the dearth is especially serious. Although academic courses and corporate training programs are accelerating, developing a sustainable talent pipeline is a multi-year effort that slows down the rate at which businesses may use and fully utilize their AI supercomputing assets.

The supply chain bottlenecks for specialized chips result in increased lead time, harming the market.

Demand for GPUs and AI‑ASICs has overtaken fabrication capacity, therefore increasing lead times for high-end accelerators such as NVIDIA H100 and unique ASICs to 6–12 months. Packaging technologies—particularly high-bandwidth memory (HBM)—are recurrent chokepoints as substrate shortages and assembly complexity slow down module distribution. Geopolitical export restrictions limit access even further: U. S. sanctions limit advanced GPU shipments to certain regions, pushing non-U.S. customers to seek alternative suppliers or risk extended backlogs. Procurement cycles are disturbed by these supply constraints, which may force companies to run with suboptimal hardware setups, therefore compromising performance goals. The market's expansion of production of specialized semiconductors and memory components will be a major factor determining market growth and system availability as demand for artificial intelligence supercomputing grows.

Artificial Intelligence (AI) Supercomputer Market Opportunities:

The increasing use of AI Supercomputing as a Service is seen as a major market opportunity.

With companies such as HPE GreenLake for LLMs providing completely managed artificial intelligence supercomputing clusters on a subscription basis, the Supercomputing-as-a-Service (SCaaS) paradigm is quickly developing. Valued at USD 9 5 billion in 2024, the world SCaaS market is expected to reach USD 23.5 billion by 2033, growing at a 10%. 5% CAGR. SCaaS eliminates the need for large capital expenditures, often USD 100 million+ for on‑prem exascale systems, by integrating hardware, software, maintenance, and system management into an OPEX‑friendly model. Companies across sectors can burst into massive GPU/ASIC clusters for short‑term AI training or inference tasks without ownership of the underlying infrastructure. Mid‑market companies and research institutions can gain access thanks to the turnkey onboarding and pay‑as‑you‑go pricing, therefore helping to democratize supercomputing and speeding AI innovation cycles worldwide.

The HPC architecture is said to be extremely energy efficient, which is a great opportunity for this market.

The need to limit data-center energy use has motivated the use of liquid-cooling, immersion-cooling, and processor-in-memory designs that offer 30–50% reductions in cooling capacity and total PUE relative to conventional air-cooled facilities. For instance, TSMC's immersion‑cooled Fab 12B lowered total energy consumption by 30% and garbage by 50% while increasing computer performance by 10%. With waste heat recovered for on-site heating, NREL's direct liquid‑cooling deployments showed 30–50% energy‑saving PUE improvements over conventional data centers. Vendors including HPE, Dell, and Supermicro now have turnkey liquid‑cooling solutions integrated with AI supercomputer racks that help customers to fulfill sustainability requirements, lower facility TCO, and sustain ever‑growing rack densities without grid upgrades.

The use of specialized domain-specific accelerators is giving the market an opportunity to develop.

With 4 trillion transistors and 900,000 AI-optimised cores, Cerebras' WSE-3 delivers up to 256 exaFLOPS across 2,048 nodes, outpacing traditional GPU clusters in both speed and energy per operation, and has been deployed in six new inference datacentres to serve 40 million Llama 70B tokens/sec. Domain-specific ASICs like Cerebras' Wafer-Scale Engine (WSE-3) and Graphcore's Intelligence Processing Units (IPUs) are carving out niche supercomputing segments optimized for transformer workloads and graph-based ML. Graphcore's IPU‑M2000 contains 1 petaFLOP of artificial intelligence compute in a 1U blade featuring integrated 3 6 GB in‑processor memory and 256 GB streaming memory, therefore allowing turnkey IPU‑Pod clusters that extend to 16 exaFLOPS for graph‑centric and sparse‑computation applications. Pre‑validated supercomputer products customized for particular artificial intelligence applications are being created via partnerships between these chip pioneers and system integrators, therefore lowering integration risk and boosting performance efficiency.

The emergence of edge supercomputing is transforming the market and helping it to grow.

To satisfy sub‑millisecond latency criteria for programs including autonomous cars, AR/VR, and industrial control, edge supercomputing uses compact, high‑performance clusters—usually consisting of dozens of GPUs or ASICs—at Multi‑Access Edge Computing (MEC) sites. Developments in edge-optimized racks and ruggedized form factors allow on‑prem inference for sensor‑fused workloads, processing data streams of up to 2 GB/s straight at the network edge. Telecom operators and companies are testing micro‑supercomputers to carry out real‑time anomaly detection, predictive maintenance, and V2X collision‑avoidance—all without round‑trip delays to central data centers—as 5G MEC infrastructures grow. Early implementations reveal 50–70% reductions in end‑to‑end latency for vital edge workloads, so unlocking new classes of safety‑critical and interactive AI services demanding both high throughput and ultralow latency.

Artificial Intelligence (AI) Supercomputer Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

• Services

The Hardware segment is the dominant segment of the market. This is due to the high sales of NPUs, GPUs, memory modules, and interconnects, which contribute about 70% of the market’s revenue. The organizations are now prioritizing raw compute capacity for large-scale model training. The Software segment is said to be the fastest-growing segment. At roughly 22% CAGR is AI‑orchestration frameworks, performance‑profiling tools, and optimized libraries, driven by demand for simplified workload management and scale efficiency. When it comes to the Services segment, it is the smallest slice yet expanding quickly. Managed-HPC services, system tuning, and integration services reflect firms' need for specialist help for challenging deployments.

Market Segmentation: By Application

• Model Training

• Inference

• High Performance Computing & Research

• Others

The Model Training segment is said to dominate this market. As model sizes soar into the hundreds of billions of parameters, training deep‑learning systems (e.g., LLMs) occupies roughly 45% of supercomputer activity. The Inference segment is the fastest-growing segment of the market. As businesses integrate artificial intelligence capabilities into customer-facing applications, real-time AI services and edge inference needs are propelling inference workloads to rise at roughly 24% CAGR.

When it comes to the High-Performance Computing and Research segment, using supercomputers' parallelism for non-AI workloads, traditional uses of HPC, scientific simulations, and weather modeling are still important. The Others segment includes a small but constantly growing segment that is occupied by niche uses, including data analytics and cryptography.

Market Segmentation: By End-Use Industry

• Healthcare

• Automotive

• Financial services

• Retail

• Government & Defense

• Academia & Research

• Others

The Healthcare segment dominates this market, due to genomics, drug discovery, and medical-image analysis, which drives the demand for this market. The life sciences institutions are rapidly adopting supercomputers for precision medicine. The Automotive segment is the fastest-growing segment. Simulations of autonomous vehicles and digital-twin development drive automotive sector expansion at about 26% CAGR, mirroring significant investment in AI-driven mobility R&D.

The Financial Services segment includes High-speed analysis and scenario simulations using supercomputers that rely on risk modeling and algorithmic trading. For the Retail segment, Supercomputing helps retailers customize experiences by means of supply-chain optimization and customer behavior simulations. National security organizations and defense contractors use exascale-class computers for cryptographic analysis and mission-critical simulations. When it comes to the Academia and Research segment, from particle physics to climate modeling, universities and laboratories use common supercomputing assets for cross-disciplinary research. The Others segment includes supercomputers that are used for network-planning analytics and grid optimization in sectors including telecommunications and energy.

Market Segmentation: By Deployment Mode

• On-premises

• Cloud-based

• Hybrid

On‑premises systems prevail (~58%) due to data-sovereignty concerns and the need for predictable, sustained performance in private data centers. The Cloud-based segment is the fastest-growing segment with roughly 25% CAGR, cloud HPC instances and managed supercomputing clusters provide OPEX flexibility and quick access to top-tier hardware. Appealing to companies, striking a balance between control and elasticity, hybrid models merge public‑cloud scalability with private‑cloud security.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

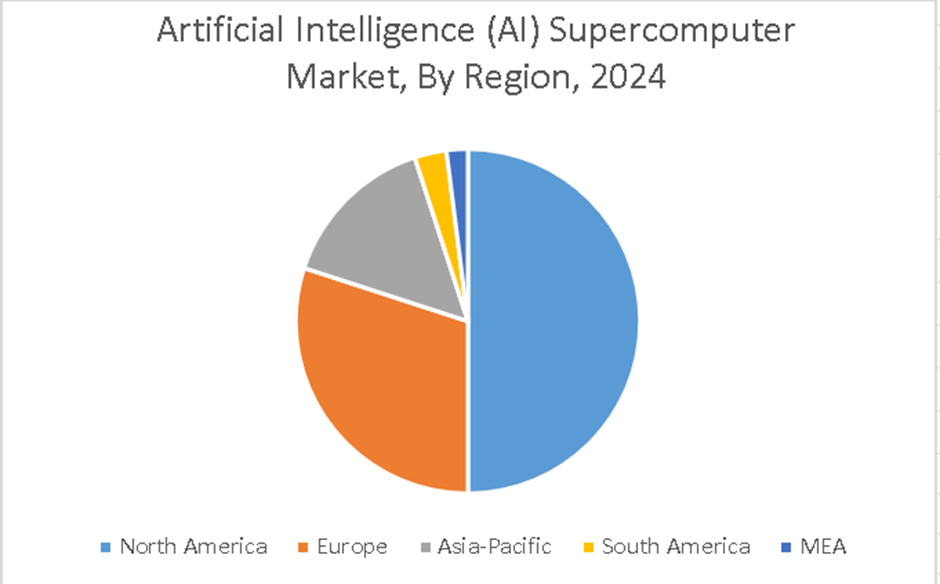

North America dominates this market, driven by significant exascale initiatives and hyperscaler cloud-HPC services. North America leads with about 38% of AI supercomputer expenditure. The Asia-Pacific region is the fastest-growing region. Driven by fast government and commercial investments in China, Japan, and India, a 21% CAGR is generated as Asia-Pacific strives for equality in artificial intelligence and high-performance computing skills.

Europe about 25% Europe's portion is supported by the EuroHPC‑JU infrastructure and business artificial intelligence use in France and Germany. In South America, about 6% of regional development is supported by expanding academic cooperation and cloud-HPC partnerships in Brazil and Argentina. MEA (about 3%). Alongside South African research facilities, Gulf-region smart-city and defense HPC initiatives help to create a smaller but growing market presence.

COVID-19 Impact Analysis on the Global Artificial Intelligence (AI) Supercomputer Market:

The epidemic fast-tracked remote R&D and AI-model development, therefore causing research centers and businesses to boost HPC expenditure. Closed on‑premises laboratories caused 53% of businesses to transfer workloads to cloud‑based supercomputing, which resulted in a 15% rise in AI supercomputer purchasing in 2021–2022. Even as hybrid-work models became established and companies gave AI-driven innovation top priority, particularly in vaccine research and supply-chain optimization, this momentum kept the market expanding despite general economic obstacles.

Latest Trends/ Developments:

Artificial intelligence workloads push performance beyond 1 exa‑FLOP with new systems from HPE (Frontier), Lenovo (El Capitan), and AWS (Ultracluster).

Integrating GPUs, TPUs, NPUs, and FPGAs inside a single chassis will help to maximize many AI and HPC activities.

To handle >30 MW power densities sustainably, quick deployment of direct-liquid-cooled racks and immersion systems is necessary.

Emergence of consistent orchestration solutions (e.g., NVIDIA AI Enterprise, AMD Instinct software) that simplify multi-node training and real-time inferencing.

Key Players:

• NIVIDIA Corporation (US)

• Intel Corporation (US)

• Advanced Micro Devices Inc. (US)

• Samsung Electronics (South Korea)

• Micron Technology Inc. (US)

• IBM Corporation (US)

• Meta (US)

• Google (US)

• Dell Inc. (US)

• Microsoft (US)

Chapter 1. Global Artificial Intelligence (AI) Supercomputer Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Artificial Intelligence (AI) Supercomputer Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Artificial Intelligence (AI) Supercomputer Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Artificial Intelligence (AI) Supercomputer Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Artificial Intelligence (AI) Supercomputer Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Artificial Intelligence (AI) Supercomputer Market- By Component

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global Artificial Intelligence (AI) Supercomputer Market– By Application

7.1 Introduction/Key Findings

7.2. Model Training

7.3. Inference

7.4. High Performance Computing & Research

7.5. Others

7.6. Y-O-Y Growth trend Analysis By Application

7.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Artificial Intelligence (AI) Supercomputer Market– By End-Use Industry

8.1. Introduction/Key Findings

8.2. Healthcare

8.3. Automotive

8.4. Financial services

8.5. Retail

8.6. Government & Defense

8.7. Academia & Research

8.8. Others

8.9. Y-O-Y Growth trend Analysis By End-Use Industry

8.10. Absolute $ Opportunity Analysis By End-Use Industry, 2025-2030

Chapter 9. Global Artificial Intelligence (AI) Supercomputer Market– By Deployment Mode

9.1. Introduction/Key Findings

9.2. On-premises

9.3. Cloud-based

9.4. Hybrid

9.5. Y-O-Y Growth trend Analysis By Deployment Mode

9.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 10. Global Artificial Intelligence (AI) Supercomputer Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Application

10.1.4. By End-Use Industry

10.1.5. By Deployment Mode

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Application

10.2.4. By End-Use Industry

10.2.5. By Deployment Mode

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Application

10.3.4. By End-Use Industry

10.3.5. By Deployment Mode

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Application

10.4.4. By End-Use Industry

10.4.5. By Deployment Mode

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Application

10.5.4. By End-Use Industry

10.5.5. By Deployment Mode

10.5.6. By Region

Chapter 11. Global Artificial Intelligence (AI) Supercomputer Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. NIVIDIA Corporation (US)

11.2. Intel Corporation (US)

11.3. Advanced Micro Devices Inc. (US)

11.4. Samsung Electronics (South Korea)

11.5. Micron Technology Inc. (US)

11.6. IBM Corporation (US)

11.7. Meta (US)

11.8. Google (US)

11.9. Dell Inc. (US)

11.10. Microsoft (US)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

Key influences are rapid expansion in generative artificial intelligence, national exascale projects, and hyperscale-cloud HPC services.

The Hardware segment is said to dominate this market. Led by strong GPU sales and interconnects, hardware accounts for around 70% of the market share.

The Model Training segment is said to be the largest segment of this market. The majority of computing cycles are spent training huge neural networks, roughly 45% of supercomputer consumption in 2024.

Asia Pacific (~21% CAGR) region is the fastest-growing region for this market, driven mostly by China, Japan, and India's government and private HPC investments.

The 15% rise in both on-premises and cloud-based supercomputer installations in 2021–2022 was driven by pandemic-induced remote study needs and vaccination research.