Artificial Intelligence (AI) in Medical Imaging Market Research Report – Segmentation by Type (AI-powered Software and Platforms, AI-integrated Medical Imaging Hardware); By Application (Radiology and Diagnostic Imaging, Cardiology, Oncology, Neurology, Ophthalmology); By Deployment Model (Cloud-based Solutions, On-premises Deployments, Hybrid Models); By End-User (Hospitals and Healthcare Systems, Diagnostic Imaging Centers, Academic and Research Institutions, Medical Technology Companies); Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16505

Format:

Region: Global

Market Size and Overview:

The Artificial Intelligence (AI) in Medical Imaging Market was valued at USD 1.03 Billion in 2024 and is projected to reach a market size of USD 1.56 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 8.60%.

The Artificial Intelligence (AI) in Medical Imaging Market has materialized as a profoundly disruptive and strategically vital force within the global healthcare technology sector, fundamentally reimagining the paradigms of medical diagnostics, treatment planning, and clinical workflow efficiency. This pioneering market encompasses a sophisticated ecosystem of AI-driven software, platforms, and integrated hardware designed to analyze and interpret medical images with unprecedented speed, accuracy, and depth. The market is witnessing a meteoric rise, propelled by an exponential surge in the volume of medical imaging data generated from modalities like MRI, CT, X-ray, and ultrasound, coupled with the escalating demand for enhanced diagnostic precision and the pressing need to alleviate the burden on overwhelmed healthcare professionals. The core of this market lies in the application of advanced machine learning (ML) and deep learning algorithms that can identify subtle patterns, anomalies, and pathologies in images that may be imperceptible to the human eye. These technologies are not merely augmenting human capabilities but are evolving to perform autonomous and semi-autonomous tasks, from initial triage and anomaly detection to quantitative analysis and predictive risk scoring. Furthermore, the regulatory landscape is adapting to this technological wave, with bodies like the FDA establishing clearer pathways for the approval of AI and ML-based medical devices, which in turn is bolstering investor confidence and fostering a vibrant ecosystem of startups and established industry players dedicated to pioneering the next generation of medical imaging intelligence.

Key Market Insights:

In 2024, investments in AI imaging startups exceeded $1.2 billion, signaling robust investor confidence in the sector's potential.

Over 500 AI-based medical imaging solutions have received FDA clearance as of early 2024, a 40% increase from the previous year.

Approximately 35% of all hospitals and imaging centers in the United States reported using at least one AI-powered imaging tool in their clinical workflow.

AI integration in radiology departments has been shown to reduce image interpretation times by an average of 25%.

In oncology, AI algorithms achieved over 95% accuracy in detecting malignant tumors in certain studies conducted in 2024.

The market for cloud-deployed AI imaging solutions saw a 60% increase in adoption in 2024.

It is estimated that AI tools helped avoid over 10 million diagnostic errors globally in 2024.

The cardiology segment saw AI adoption increase by 30%, particularly for analyzing echocardiograms.

Neurological applications, specifically for MRI analysis, accounted for 15% of the market's software revenue.

AI-powered operational tools for workflow optimization and patient scheduling in imaging departments grew by 50%.

Market Drivers:

The Imperative for Diagnostic Efficiency and Accuracy

A primary driver propelling the AI in medical imaging market is the overwhelming volume of diagnostic imaging studies, which has far outpaced the growth in the number of qualified radiologists and specialists. This imbalance creates significant workflow pressures, leading to potential delays in diagnosis and an increased risk of burnout and error. AI serves as a powerful force multiplier, automating repetitive tasks, prioritizing urgent cases by flagging potential abnormalities, and providing quantitative insights that enhance diagnostic confidence. By streamlining workflows and reducing interpretation times, AI directly addresses the efficiency imperative, allowing clinicians to focus their expertise on the most complex cases.

Rising Prevalence of Chronic Diseases and Aging Populations

The global increase in chronic diseases such as cancer, cardiovascular disorders, and neurological conditions, coupled with a rapidly aging population, is another critical market driver. These demographic and epidemiological trends translate into a greater demand for medical imaging as a key tool for early detection, diagnosis, and ongoing management of disease. AI-powered solutions are uniquely suited to handle this increased demand by enabling earlier and more accurate detection of pathologies. For instance, AI can identify subtle signs of disease that may be missed in routine screenings, facilitating timely intervention and improving long-term patient outcomes.

Market Restraints and Challenges:

The AI in Medical Imaging market, despite its promise, faces considerable hurdles. The high cost of implementing sophisticated AI systems, including integration with existing PACS and EMR infrastructure, can be prohibitive for many healthcare providers. A significant "black box" problem persists, where the decision-making processes of complex algorithms lack transparency, creating a challenge for clinical validation and trust. Furthermore, navigating the complex and evolving global regulatory landscape for AI medical devices is a major challenge, alongside persistent concerns over patient data privacy and security.

Market Opportunities:

Substantial opportunities exist for growth and innovation within the market. The expansion of AI into predictive analytics, moving beyond diagnosis to forecast disease progression and treatment response, represents a major frontier. There is immense potential in developing AI for underserved and highly specialized areas like pediatric radiology and fetal medicine. Furthermore, the integration of AI with other data sources, such as genomics and clinical notes, to create holistic patient profiles for precision medicine offers a vast and largely untapped opportunity for market expansion and clinical impact.

Market Segmentation:

Segmentation by Type:

• AI-powered Software and Platforms

• AI-integrated Medical Imaging Hardware

The AI-powered software and platforms segment is the fastest-growing area, driven by its inherent scalability, flexibility, and lower upfront cost compared to hardware. Cloud-based SaaS models allow for rapid deployment and continuous updates, enabling healthcare facilities of all sizes to access state-of-the-art algorithms without major capital expenditure on new imaging machines.

AI-powered software also stands as the most dominant type, commanding the largest share of the market. Its dominance is rooted in the vast and diverse range of applications available, from workflow optimization to specific diagnostic modules for numerous diseases. These software solutions can be integrated into existing hospital IT infrastructure, making them a more accessible entry point for AI adoption.

Segmentation by Application:

• Radiology and Diagnostic Imaging

• Cardiology

• Oncology

• Neurology

• Ophthalmology

Oncology is the fastest-growing application, fueled by the critical need for precision in cancer detection, staging, and treatment planning. AI tools are proving indispensable for automating tumour segmentation for radiotherapy, identifying subtle cancerous lesions missed by the human eye, and predicting tumour response to therapies, directly impacting patient survival rates and driving rapid adoption.

Radiology and diagnostic imaging remain the most dominant application, as it is the foundational discipline for a vast majority of medical imaging. The sheer volume of CT, MRI, and X-ray scans performed daily creates an immense and immediate need for AI-driven tools that can enhance efficiency, triage critical findings, and improve diagnostic accuracy across the board.

Segmentation by Deployment Model:

• Cloud-based Solutions

• On-premises Deployments

• Hybrid Models

Cloud-based solutions are the fastest-growing deployment model, offering unparalleled scalability, accessibility, and computational power without the need for significant on-site hardware investment. This model democratizes access to powerful AI tools for smaller clinics and facilitates seamless, large-scale data analysis and algorithm training, fostering rapid innovation and collaboration across institutions.

On-premises deployments continue to dominate the market, particularly in large, established hospitals and healthcare systems. The dominance is driven by long-standing concerns over data security, patient privacy, and the desire to maintain complete control over sensitive health information within the institution's own IT infrastructure, despite the growing appeal of cloud alternatives.

Segmentation by End-User:

• Hospitals and Healthcare Systems

• Diagnostic Imaging Centers

• Academic and Research Institutions

• Medical Technology Companies

Diagnostic imaging centers represent the fastest-growing end-user segment. These specialized centers are highly focused on efficiency and throughput, making them aggressive adopters of AI tools that can accelerate workflows, automate reporting, and enhance diagnostic quality. Their agile operational structure allows for quicker implementation and realization of ROI from AI investments compared to larger hospital systems.

Hospitals and healthcare systems are the most dominant end-user, commanding the largest market share due to the sheer scale of their operations and the breadth of their imaging needs across multiple clinical departments. They are the primary purchasers of comprehensive, enterprise-level AI platforms and integrated solutions, making them the central pillar of the market.

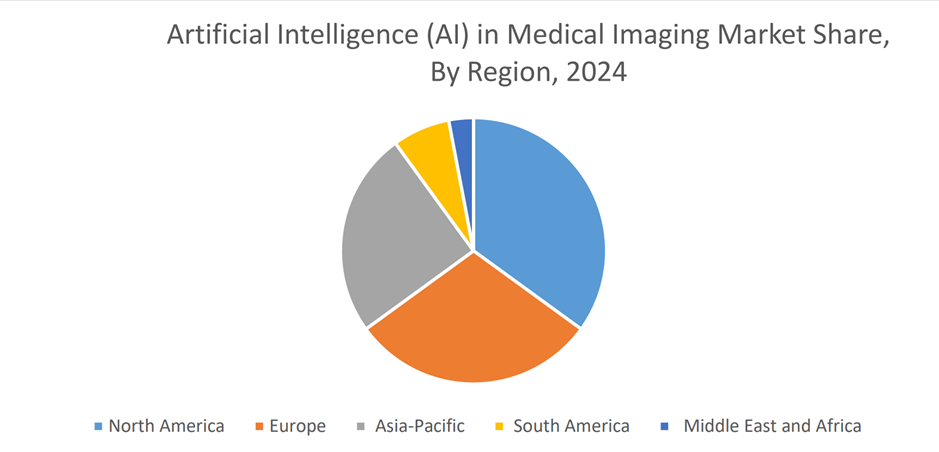

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

North America, holding approximately 45% of the market, is the dominant region due to advanced healthcare infrastructure, high levels of investment in AI technology, a supportive regulatory framework from the FDA, and the presence of numerous key market players and pioneering research institutions that drive continuous innovation and early adoption.

The Asia-Pacific region is the fastest-growing, fueled by increasing government and private investment in healthcare modernization, a large and aging population, and a burgeoning tech sector. Countries like China and India are rapidly adopting digital health technologies, creating immense opportunities for AI imaging vendors to expand their footprint.

COVID-19 Impact Analysis:

The COVID-19 pandemic acted as a significant catalyst for the AI in medical imaging market. The crisis created an urgent need for tools to rapidly analyze chest CT and X-ray scans to detect and quantify COVID-19 pneumonia, proving AI's value in a public health emergency. Furthermore, the pandemic exacerbated existing workflow backlogs and staff shortages, compelling healthcare organizations to accelerate their adoption of AI-powered automation and remote reading solutions to manage the crisis and maintain diagnostic continuity.

Latest Trends and Developments:

The market is rapidly advancing with several key trends. Federated learning is gaining significant traction, allowing AI models to be trained across multiple hospitals without sharing sensitive patient data, thus overcoming major privacy barriers. There is a strong push towards Explainable AI (XAI), developing algorithms that can provide clear rationale for their diagnostic conclusions to build clinician trust. Another major trend is the integration of AI across the entire patient pathway, from initial scan acquisition and image quality control to diagnosis, treatment planning, and follow-up.

Key Players in the Market:

• Siemens Healthineers

• GE HealthCare

• Philips Healthcare

• Canon Medical Systems

• IBM Watson Health

• Arterys

• Aidoc

• Zebra Medical Vision (Nanox)

• Viz.ai

• HeartFlow

Chapter 1. Global Artificial Intelligence (AI) in Medical Imaging Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Artificial Intelligence (AI) in Medical Imaging Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Artificial Intelligence (AI) in Medical Imaging Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Artificial Intelligence (AI) in Medical Imaging Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Artificial Intelligence (AI) in Medical Imaging Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Artificial Intelligence (AI) in Medical Imaging Market – By Type

6.1. Introduction/Key Findings

6.2. AI-powered Software and Platforms

6.3. AI-integrated Medical Imaging Hardware

6.4. Y-O-Y Growth trend Analysis By Type

6.5. Absolute $ Opportunity Analysis By Type, 2025-2030

Chapter 7. Global Artificial Intelligence (AI) in Medical Imaging Market – By Application

7.1. Introduction/Key Findings

7.2. Radiology and Diagnostic Imaging

7.3. Cardiology

7.4. Oncology

7.5. Neurology

7.6. Ophthalmology

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 8. Global Artificial Intelligence (AI) in Medical Imaging Market – By Deployment Model

8.1. Introduction/Key Findings

8.2. Cloud-based Solutions

8.3. On-premises Deployments

8.4. Hybrid Models

8.5. Y-O-Y Growth trend Analysis By Deployment Model

8.6. Absolute $ Opportunity Analysis By Deployment Model, 2025-2030

Chapter 9. Global Artificial Intelligence (AI) in Medical Imaging Market – By End-User

9.1. Introduction/Key Findings

9.2. Hospitals and Healthcare Systems

9.3. Diagnostic Imaging Centers

9.4. Academic and Research Institutions

9.5. Medical Technology Companies

9.6. Y-O-Y Growth trend Analysis By End-User

9.7. Absolute $ Opportunity Analysis By End-User, 2025-2030

Chapter 10. Global Artificial Intelligence (AI) in Medical Imaging Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Application

10.1.4. By Deployment Model

10.1.5. By End-User

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Type

10.2.3. By Application

10.2.4. By Deployment Model

10.2.5. By End-User

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.2. By Type

10.3.3. By Application

10.3.4. By Deployment Model

10.3.5. By End-User

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Type

10.4.3. By Application

10.4.4. By Deployment Model

10.4.5. By End-User

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Type

10.5.3. By Application

10.5.4. By Deployment Model

10.5.5. By End-User

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Artificial Intelligence (AI) in Medical Imaging Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Siemens Healthineers (Germany)

11.2. GE HealthCare (USA)

11.3. Philips Healthcare (Netherlands)

11.4. Canon Medical Systems (Japan)

11.5. IBM Watson Health (USA)

11.6. Arterys (USA)

11.7. Aidoc (Israel)

11.8. Zebra Medical Vision (Nanox) (Israel)

11.9. Viz.ai (USA)

11.10. HeartFlow (USA)

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary drivers are the overwhelming volume of medical imaging data that requires analysis and a shortage of specialists, the increasing prevalence of chronic diseases that necessitate early and accurate diagnosis, and the proven ability of AI to significantly enhance diagnostic efficiency, accuracy, and workflow automation in clinical settings.

Key concerns include the high implementation costs of AI systems, the lack of transparency or "black box" nature of some algorithms which affects clinical trust, navigating complex global regulatory approval processes, and ensuring robust patient data privacy and cybersecurity, which are paramount in healthcare.

The market includes established giants like Siemens Healthineers, GE HealthCare, and Philips Healthcare, as well as specialized AI pioneers such as Aidoc, Viz.ai, Qure.ai, Arterys, and Zebra Medical Vision (Nanox), creating a competitive and innovative landscape.

North America currently holds the largest market share, estimated at around 45%, due to its advanced healthcare infrastructure, high R&D investment, favorable regulatory environment, and the presence of major industry players.

The Asia-Pacific region is expanding at the highest rate. This growth is driven by significant investments in healthcare digitalization, a large patient population, rising healthcare expenditure, and a rapidly growing technology sector focused on health-tech innovations.