AI Infrastructure Market Research Report -- Segmentation by Component (Hardware, Software, Services); By Deployment (On-Premises, Cloud, Hybrid); By Technology (Machine Learning, Deep Learning, Natural Language Processing, Computer Vision); By Organization Size (Small and Medium Enterprises, Large Enterprises); By Industry Vertical (Healthcare, BFSI, Retail, Manufacturing, Automotive, Government, Others); Region - Forecast (2025 - 2030)

Published: 2024 - January

Report Code: IM-1017

Format:

Region: Global

Market Size and Overview:

The Global AI Infrastructure Market was valued at USD 40.19 billion in 2024 and is projected to reach a market size of USD 112.69 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.9%.

AI Infrastructure encompasses the underlying hardware, software, and services required to develop, deploy, and scale artificial intelligence applications across various computing environments. This rapidly evolving sector has become a cornerstone of digital transformation in the 21st century, driven by exponential growth in data generation, advances in machine learning algorithms, and increasing demand for intelligent automation across industries. With the continuous evolution of AI technologies, the demand for specialized computing infrastructure capable of handling complex AI workloads is experiencing unprecedented growth, creating substantial opportunities across sectors including healthcare, finance, manufacturing, and autonomous systems.

Key Market Insights:

According to a comprehensive survey by McKinsey Global Institute in 2022, organizations implementing AI infrastructure solutions reported an average 26% increase in operational efficiency and a 19% reduction in operational costs within the first 18 months of deployment.

Research from IDC reveals that companies investing in specialized AI infrastructure achieved 3.2 times faster model training times compared to traditional computing infrastructure, enabling accelerated time-to-market for AI applications.

A 2024 enterprise AI adoption survey involving 2,100 global organizations found that 84% of respondents planned to increase their AI infrastructure budgets by an average of 35% over the next two years. Furthermore, organizations with mature AI infrastructure reported processing 8.7 times more data for AI workloads compared to those with basic setups, demonstrating the scalability advantages of sophisticated AI infrastructure implementations.

Market intelligence from NVIDIA indicates that AI training workloads have grown by 300,000 times since 2012, with inference workloads increasing by 11,000 times during the same period. This exponential growth has driven demand for specialized AI chips, with GPU-accelerated infrastructure accounting for approximately 85% of AI training workloads and 62% of AI inference applications across enterprise deployments worldwide.

AI Infrastructure Market Drivers:

The exponential growth in AI model complexity and the increasing demand for real-time AI applications are fundamentally driving the need for specialized, high-performance AI infrastructure across diverse industries and use cases.

Modern AI applications, particularly large language models and computer vision systems, require unprecedented computational resources that far exceed the capabilities of traditional IT infrastructure. The latest generation of AI models, such as GPT-style transformers, contain billions or even trillions of parameters, demanding specialized hardware architectures optimized for parallel processing and high-bandwidth memory access. According to research from Stanford University, the computational requirements for training state-of-the-art AI models have increased by a factor of 300,000 since 2012, with this trend showing no signs of deceleration. This exponential growth has created a critical need for purpose-built AI infrastructure that can efficiently handle massive datasets, complex mathematical operations, and distributed training processes. Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), and other AI-optimized chips have become essential components, with leading organizations investing heavily in specialized hardware configurations. The proliferation of real-time AI applications, including autonomous vehicles, fraud detection systems, and conversational AI platforms, has further intensified infrastructure requirements, as these applications demand ultra-low latency processing capabilities that traditional computing architectures cannot provide. Edge AI deployments have emerged as another significant driver, requiring distributed infrastructure that can process AI workloads locally while maintaining connection to centralized training and management systems.

The democratization of AI through cloud-based infrastructure services and the increasing adoption of MLOps practices are accelerating market growth by making advanced AI capabilities accessible to organizations of all sizes.

Cloud service providers have revolutionized AI infrastructure accessibility by offering scalable, on-demand computing resources specifically optimized for AI workloads, eliminating the need for substantial upfront capital investments. Amazon Web Services, Microsoft Azure, and Google Cloud Platform have invested over $50 billion collectively in AI infrastructure capabilities since 2018, creating comprehensive ecosystems that support the entire AI development lifecycle from data preparation to model deployment and monitoring. This cloud-based approach has enabled smaller organizations to access enterprise-grade AI infrastructure through consumption-based pricing models, with 73% of mid-market companies now utilizing cloud AI services compared to just 23% three years ago.

AI Infrastructure Market Restraints and Challenges:

Despite its robust growth prospects, the AI infrastructure market faces significant challenges that could impact its expansion trajectory. The shortage of specialized AI talent represents a critical bottleneck, with demand for AI engineers and data scientists outstripping supply by approximately 250% globally, leading to increased implementation costs and project delays. Technical complexity remains a substantial barrier, as AI infrastructure requires deep expertise in distributed computing, specialized hardware optimization, and complex software frameworks that many organizations lack internally. Power consumption and cooling requirements for AI infrastructure can be 3-5 times higher than traditional computing systems, creating operational challenges and environmental concerns that complicate deployment decisions. Additionally, the rapid pace of technological evolution in AI hardware creates risks of infrastructure obsolescence, with organizations concerned about making substantial investments in technologies that may become outdated within 2-3 years

AI Infrastructure Market Opportunities:

The AI infrastructure market presents extraordinary growth opportunities across multiple dimensions as organizations accelerate their digital transformation initiatives and AI adoption strategies. Edge AI represents a particularly promising frontier, with the proliferation of IoT devices and 5G networks creating demand for distributed AI processing capabilities that can operate with minimal latency and reduced bandwidth requirements. Industry analysts project that edge AI infrastructure will grow at a 45% CAGR through 2030, driven by applications in autonomous vehicles, smart cities, and industrial automation. Specialized AI infrastructure for emerging technologies such as quantum machine learning, federated learning, and neuromorphic computing presents additional growth vectors as these technologies transition from research to commercial applications. The healthcare sector offers substantial opportunities, with AI infrastructure investments for medical imaging, drug discovery, and personalized medicine projected to reach $18.2 billion by 2027.

AI Infrastructure Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

• Services

The hardware segment dominated the global AI infrastructure market in 2024, accounting for approximately 52.8% of the total market share. This dominance is primarily attributed to the critical role of specialized processing units such as GPUs, TPUs, and AI-optimized chips in enabling high-performance AI workloads. Leading hardware providers including NVIDIA, Intel, and AMD have invested heavily in developing purpose-built AI accelerators that deliver significantly superior performance compared to traditional CPUs for machine learning tasks.

The software segment is projected to experience the highest growth rate during the forecast period, with an estimated CAGR of 26.4%. This accelerated growth is driven by the increasing complexity of AI software frameworks, the proliferation of MLOps platforms, and the growing demand for AI infrastructure management tools. Organizations are recognizing that software optimization is crucial for maximizing the performance of their AI hardware investments, leading to increased adoption of specialized AI software platforms and development tools.

Market Segmentation: By Deployment

• On-Premises

• Cloud

• Hybrid

The cloud deployment segment accounted for the largest market share of approximately 48.7% in 2024, reflecting the growing preference for scalable, flexible AI infrastructure solutions that can be rapidly provisioned and scaled based on demand. Cloud-based AI infrastructure offers organizations the ability to access cutting-edge hardware and software without significant upfront investments, making advanced AI capabilities accessible to a broader range of organizations.

The hybrid deployment model is projected to witness the fastest growth rate during the forecast period, with a CAGR of 28.6%. This growth is driven by organizations' desire to balance the scalability and cost-effectiveness of cloud infrastructure with the security and control offered by on-premises deployments. Hybrid approaches enable organizations to process sensitive data on-premises while leveraging cloud resources for computationally intensive training workloads and development activities.

Market Segmentation: By Technology

• Machine Learning

• Deep Learning

• Natural Language Processing

• Computer Vision

Deep learning represented the largest technology segment in 2024, capturing approximately 38.9% of the market share due to its widespread application across industries for image recognition, natural language processing, and predictive analytics. The computational intensity of deep learning algorithms has driven substantial demand for GPU-accelerated infrastructure and specialized AI chips optimized for neural network operations.

Natural Language Processing (NLP) is anticipated to grow at the fastest rate during the forecast period, with a CAGR of 31.2%. This growth is fuelled by the increasing adoption of conversational AI, chatbots, and large language models across customer service, content generation, and business process automation applications.

Market Segmentation: By Organization Size

• Small and Medium Enterprises (SMEs)

• Large Enterprises

Large enterprises dominated the AI infrastructure market in 2024, accounting for approximately 72.4% of the total market share. These organizations typically have the financial resources, technical expertise, and complex use cases that justify substantial AI infrastructure investments. Large enterprises often implement comprehensive AI strategies that span multiple departments and business functions, requiring sophisticated infrastructure platforms capable of supporting diverse workloads and use cases.

The SME segment is projected to experience the highest growth rate during the forecast period, with a CAGR of 29.7%. This accelerated growth is primarily driven by the increasing availability of cloud-based AI infrastructure services that eliminate the need for substantial upfront investments. Additionally, the development of user-friendly AI platforms and pre-built solutions has made AI technology more accessible to smaller organizations with limited technical resources, enabling them to compete more effectively with larger enterprises.

Market Segmentation: By Industry Vertical

• Healthcare

• BFSI (Banking, Financial Services, and Insurance)

• Retail

• Manufacturing

• Automotive

• Government

• Others

The BFSI sector emerged as the largest industry vertical in 2024, accounting for 24.6% of the AI infrastructure market share. Financial institutions have been early adopters of AI technology for applications including fraud detection, algorithmic trading, risk assessment, and customer service automation. The sector's regulatory requirements and need for real-time processing capabilities have driven substantial investments in high-performance AI infrastructure.

Healthcare is projected to witness the fastest growth rate during the forecast period, with a CAGR of 33.8%. This growth is driven by increasing adoption of AI for medical imaging analysis, drug discovery, precision medicine, and clinical decision support systems. The COVID-19 pandemic has accelerated digital transformation in healthcare, leading to increased investments in AI infrastructure to support telemedicine, diagnostic imaging, and research applications that require substantial computational resources.

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

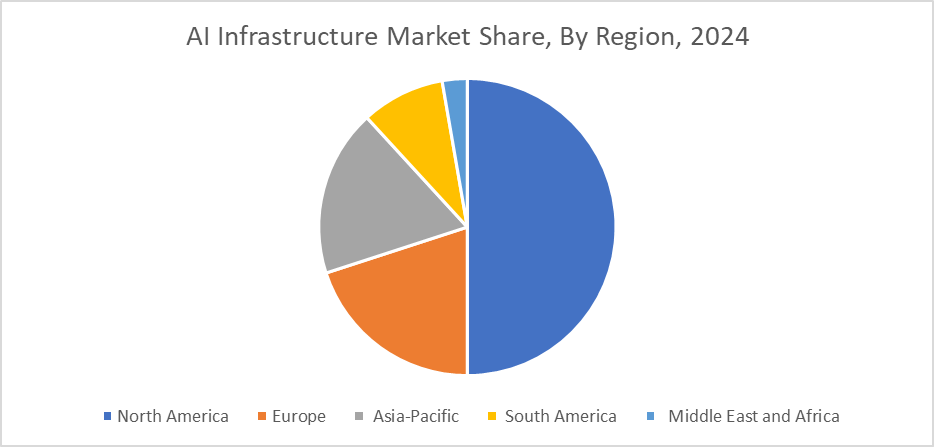

North America maintained its leadership position in the global AI infrastructure market in 2024, commanding approximately 39.2% of the total market share. This dominance is attributed to the region's advanced technology ecosystem, presence of major AI infrastructure providers, and substantial investments in AI research and development by both private enterprises and government agencies. The United States alone accounts for over 60% of global AI infrastructure investments, with major technology companies investing over $40 billion annually in AI infrastructure development.

The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, with a CAGR of 27.8%. This accelerated growth is driven by rapid digital transformation initiatives across emerging economies, substantial government investments in AI development, and the region's strong manufacturing base for AI hardware components. China and India represent the largest growth opportunities, with both countries implementing national AI strategies that include significant infrastructure investments to support domestic AI development and adoption.

COVID-19 Impact Analysis on the Global AI Infrastructure Market:

The COVID-19 pandemic initially created uncertainty in technology spending as organizations focused on immediate operational continuity challenges. However, the crisis ultimately accelerated AI infrastructure adoption as organizations recognized the critical importance of automated, intelligent systems for maintaining operations during disruptions. Healthcare organizations rapidly deployed AI infrastructure to support diagnostic imaging for COVID-19 detection, drug discovery research, and patient monitoring systems, leading to a 156% increase in healthcare AI infrastructure investments during 2020-2021.

Latest Trends/ Developments:

The emergence of large language models and generative AI applications is driving unprecedented demand for specialized AI infrastructure, with organizations requiring massive computational resources to train and deploy models with billions of parameters. Companies are investing heavily in distributed training infrastructures that can handle the enormous memory and processing requirements of next-generation AI models, leading to the development of new architectural approaches and specialized hardware solutions.

Sustainable AI infrastructure has become a critical focus area, with major cloud providers and enterprises implementing energy-efficient AI chips, improved cooling systems, and renewable energy sources to address the environmental impact of AI workloads.

Leading technology companies have committed to carbon-neutral AI operations by 2030, driving innovation in power-efficient hardware designs and intelligent workload management systems that optimize energy consumption without sacrificing performance

Key Players:

• NVIDIA Corporation

• Intel Corporation

• Advanced Micro Devices (AMD)

• International Business Machines (IBM)

• Google LLC (Alphabet Inc.)

• Microsoft Corporation

• Amazon Web Services (AWS)

• Xilinx Inc. (now part of AMD)

• Qualcomm Technologies

• Graphcore Ltd.

Chapter 1. AI Infrastructure Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. AI Infrastructure Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. AI Infrastructure Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. AI Infrastructure MarketEntry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. AI Infrastructure Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. AI Infrastructure Market– By Component

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. AI Infrastructure Market– By Deployment

7.1. Introduction/Key Findings

7.2. On Premises

7.3. Cloud

7.4. Hybrid

7.5. Y-O-Y Growth trend Analysis By Deployment

7.6. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 8. AI Infrastructure Market– By Size

8.1. Introduction/Key Findings

8.2. Machine Learning

8.3. Deep Learning

8.4. Natural Language Processing

8.5. Computer Vision

8.6. Y-O-Y Growth trend Analysis By Size

8.7. Absolute $ Opportunity Analysis By Size, 2025-2030

Chapter 9. AI Infrastructure Market– By Organization Size

9.1. Introduction/Key Findings

9.2. Small and Medium Sized Enterprises (SME)

9.3. Large Enterprises

9.4. Y-O-Y Growth trend Analysis By Organization Size

9.5. Absolute $ Opportunity Analysis By Organozation Size, 2025-2030

Chapter 10. AI Infrastructure Market– By Industry Vertical

10.1. Introduction/Key Findings

10.2. Healthcare

10.3. BFSI

10.4. Retail

10.5. Manufacturing

10.6. Automotive

10.7. Government

10.8. Others

10.9. Y-O-Y Growth trend Analysis By Organization Size

10.10. Absolute $ Opportunity Analysis By Organization Size, 2025-2030

Chapter 11. Global AI Infrastructure Market, By Geography – Market Size, Forecast, Trends & Insights

11.1. North America

11.1.1. By Country

11.1.1.1. U.S.A.

11.1.1.2. Canada

11.1.1.3. Mexico

11.1.2. By Component

11.1.3. By Deployment

11.1.4. By Technology

11.1.5. By Organization Size

11.1.6. By Industry Vertical

11.1.7. Countries & Segments – Market Attractiveness Analysis

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.1.2. Germany

11.2.1.3. France

11.2.1.4. Italy

11.2.1.5. Spain

11.2.1.6. Rest of Europe

11.2.2. By Component

11.2.3. By Deployment

11.2.4. By Technology

11.2.5. By Organization Size

11.2.6. By Industry Vertical

11.2.7. Countries & Segments – Market Attractiveness Analysis

11.3. Asia Pacific

11.3.1. By Country

11.3.1.1. China

11.3.1.2. Japan

11.3.1.3. South Korea

11.3.1.4. India

11.3.1.5. Australia & New Zealand

11.3.1.6. Rest of Asia-Pacific

11.3.2. By Component

11.3.3. By Deployment

11.3.4. By Technology

11.3.5. By Organization Size

11.3.6. By Industry Vertical

11.3.7. Countries & Segments – Market Attractiveness Analysis

11.4. South America

11.4.1. By Country

11.4.1.1. Brazil

11.4.1.2. Argentina

11.4.1.3. Colombia

11.4.1.4. Chile

11.4.1.5. Rest of South America

11.4.2. By Component

11.4.3. By Deployment

11.4.4. By Technology

11.4.5. By Organization Size

11.4.6. By Industry Vertical

11.4.7. Countries & Segments – Market Attractiveness Analysis

11.5. Middle East & Africa

11.5.1. By Country

11.5.1.1. United Arab Emirates (UAE)

11.5.1.2. Saudi Arabia

11.5.1.3. Qatar

11.5.1.4. Israel

11.5.1.5. South Africa

11.5.1.6. Nigeria

11.5.1.7. Kenya

11.5.1.8. Egypt

11.5.1.9. Rest of MEA

11.5.2. By Component

11.5.3. By Deployment

11.5.4. By Technology

11.5.5. By Organization Size

11.5.6. By Industry Vertical

11.5.7. Countries & Segments – Market Attractiveness Analysis

Chapter 14. AI Infrastructure Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

12.1. NVIDIA Corporation

12.2. Intel Corporation

12.3. Advanced Micro Devices (AMD)

12.4. International Business Machines (IBM)

12.5. Google LLC (Alphabet Inc.)

12.6. Microsoft Corporation

12.7. Amazon Web Services (AWS)

12.8. Xilinx Inc. (now part of AMD)

12.9. Qualcomm Technologies

12.10. Graphcore Ltd.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global AI Infrastructure Market was valued at USD 40.19 billion in 2024 and is projected to reach a market size of USD 112.69 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 22.9%.

The exponential growth in AI model complexity and the increasing demand for real-time AI applications are the primary drivers propelling the global AI infrastructure market.

Based on Component, the Global AI Infrastructure Market is segmented into Hardware, Software, and Services.

North America is the most dominant region for the Global AI Infrastructure Market.

NVIDIA Corporation, Intel Corporation, Advanced Micro Devices (AMD), and International Business Machines (IBM) are the key players operating in the Global AI Infrastructure Market.