AI in Asset Management Market

Published: 2025 - June

Report Code: IM-16477

Format:

Region: Global

Market Size and Overview:

The AI In Asset Management Market was valued at USD 4.62 Billion in 2024 and is projected to reach a market size of USD 13.36 Billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 23.67%.

The AI in Asset Management Market has materialized as a profoundly disruptive and pivotal force within the global financial services industry, heralding a new epoch of data-centric investment strategies and operational paradigms. Valued at approximately USD 4.16 Billion in 2024, the market is on a steep upward trajectory, fundamentally reshaping the core functions of asset and wealth management firms. This market encompasses an advanced ecosystem of intelligent software, platforms, and services engineered to automate, augment, and revolutionize decision-making processes, from portfolio construction to risk mitigation and client interaction. The surge in market valuation is propelled by an confluence of factors, including the astronomical growth in financial and alternative data, the pressing need for greater operational efficiency in a margin-compressed environment, and the relentless pursuit of "alpha" through superior analytical capabilities. At its core, the market's dynamism is rooted in the transition from traditional, human-centric analysis to a hybrid model where human expertise is magnified by machine intelligence.

Key Market Insights:

An estimated 75% of asset management firms globally have initiated at least one AI-related project, moving beyond pilot stages into active deployment.

In 2024, AI-driven platforms were responsible for analyzing over 50 zettabytes of financial and alternative data, a 40% increase from the previous year.

The application of machine learning for predictive analytics reduced portfolio risk by an average of 22% for firms that fully integrated these solutions.

Furthermore, operational cost savings attributed to AI-powered automation reached approximately 18% for middle-office functions within adopting firms.

The use of Natural Language Processing for sentiment analysis of news and social media feeds influenced trading decisions in over 65% of quantitative funds.

It is estimated that AI algorithms were involved in executing nearly 35% of all institutional trades in 2024.

Market Drivers:

The Imperative for Enhanced Efficiency and Cost Reduction

In an era of increasing fee compression and intense competition, asset managers are under immense pressure to optimize their operations and reduce costs. AI emerges as a powerful catalyst for achieving these objectives. By automating routine and labor-intensive tasks such as data reconciliation, compliance checks, and report generation, AI-powered systems free up human analysts to focus on high-value strategic activities. This operational leverage not only drives down expenses and minimizes the risk of human error but also enhances overall productivity, allowing firms to manage larger asset pools more effectively without a proportional increase in headcount.

The Proliferation of Big Data and the Quest for Alpha

The modern financial world is inundated with an ever-expanding universe of data, ranging from traditional market feeds to alternative sources like satellite imagery, social media sentiment, and supply chain information. Human capabilities are insufficient to process and analyze this data deluge effectively. AI, particularly machine learning, provides the necessary tools to sift through this noise, identify non-obvious patterns, and extract actionable insights. This ability to leverage alternative data and uncover hidden correlations is a primary driver for generating alpha—returns above the market benchmark—giving early adopters a distinct competitive advantage in a crowded marketplace.

Market Restraints and Challenges:

The primary restraints impeding market growth include the significant upfront investment costs and the complexity of integrating AI systems with legacy IT infrastructure. Furthermore, a persistent shortage of skilled data scientists and AI specialists who also possess deep financial domain expertise creates a critical talent bottleneck. Data privacy, security, and governance remain paramount concerns, with firms navigating a complex web of regulations. A significant challenge lies in the "black box" nature of some advanced models, making it difficult to achieve the explainability and transparency demanded by regulators and clients. Additionally, the substantial initial capital investments required for AI system implementation, including infrastructure development, talent acquisition, and ongoing technology maintenance costs, create barriers to entry for smaller asset management firms seeking to compete with larger institutional players.

Market Opportunities:

Substantial opportunities lie in the hyper-personalization of wealth management services for the mass-affluent and retail segments, using AI to deliver tailored advice at scale. The growing emphasis on ESG (Environmental, Social, and Governance) investing presents a key opportunity, as AI is uniquely capable of processing vast amounts of unstructured ESG data to provide deeper insights and ratings. There is also immense potential in developing sophisticated AI-driven solutions for alternative asset classes like private equity and real estate, which have traditionally been data-poor. The integration of environmental, social, and governance factors into investment decision-making processes offers opportunities for AI systems specializing in ESG data analysis and sustainable investment strategies, while the growing popularity of alternative investments and digital assets creates demand for specialized AI algorithms capable of analyzing non-traditional asset classes.

Market Segmentation:

Segmentation by Technology:

• Predictive Analytics and Forecasting

• Machine Learning and Deep Learning

• Natural Language Processing (NLP)

• Robotic Process Automation (RPA)

Machine learning and its advanced subset, deep learning, represent the fastest-growing technology segment. This growth is fueled by their unparalleled ability to analyze vast and complex datasets to identify predictive patterns for alpha generation, dynamic risk assessment, and algorithmic trading strategies. As firms move beyond simple automation, the demand for sophisticated, self-improving models that can adapt to changing market conditions is skyrocketing.

Predictive analytics and forecasting remain the most dominant technology, serving as the foundational AI application for most asset managers. These tools are essential for core functions like market trend analysis, asset allocation modeling, and performance attribution. Their dominance is secured by their proven ability to provide actionable forward-looking insights that are critical for strategic decision-making across all levels of an investment firm.

Segmentation by Application:

• Portfolio Management and Optimization

• Risk and Compliance Management

• Algorithmic Trading

• Customer Service and Acquisition

• Fraud Detection and Prevention

• Fastest-Growing Application: Risk and Compliance Management

The application of AI in risk and compliance management is expanding at the fastest rate. In a climate of increasing regulatory scrutiny and market volatility, firms are aggressively adopting AI to automate compliance monitoring, conduct real-time risk simulations, and proactively identify potential breaches. The ability of AI to analyze regulations and internal policies to ensure adherence provides invaluable protection against financial and reputational damage.

Portfolio management and optimization is the most dominant application, as it lies at the very heart of the asset management business. AI tools are fundamentally ingrained in processes for asset allocation, rebalancing, tax-loss harvesting, and identifying new investment opportunities. The direct impact of these applications on investment performance ensures their continued dominance and widespread adoption across the industry.

Segmentation by Deployment Model:

• Cloud-based

• On-premises

• Hybrid

Cloud-based deployments are the fastest-growing segment, driven by the need for scalability, flexibility, and lower upfront capital expenditure. Cloud platforms provide access to immense computing power and pre-built AI services, democratizing access for smaller firms and enabling larger institutions to innovate more rapidly. The ease of integration with diverse data sources makes the cloud the preferred choice for modern data-centric strategies.

On-premises deployments, while growing more slowly, remain the dominant model, particularly among large, established financial institutions. This dominance is due to long-standing security protocols, the need for maximum control over sensitive proprietary data and algorithms, and existing investments in legacy data centers. Many firms prefer to keep their most critical intellectual property and client data within their own firewalls.

Segmentation by Component:

• Solutions

• Services

Services, including AI-as-a-Service (AIaaS), consulting, and managed services, are the fastest-growing component. Many asset management firms lack the in-house expertise to build and maintain complex AI systems from scratch. They are increasingly turning to specialized service providers to accelerate their AI adoption, access top-tier talent, and ensure their models are effectively integrated and managed, driving rapid growth in this segment.

Software solutions, including off-the-shelf platforms and customizable tools, remain the dominant market component. These solutions provide the core engines for portfolio analytics, risk management, and trading automation. As the market matures, the availability of robust, feature-rich software that can be integrated into existing workflows makes it the primary entry point for firms looking to leverage AI capabilities.

Market Segmentation: Regional Analysis:

• North America

• Europe

• Asia-Pacific

• South America

• Middle East & Africa

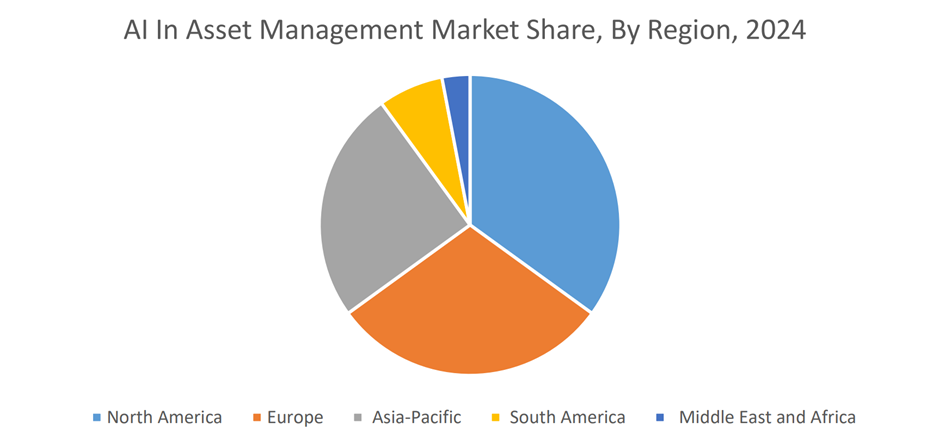

North America, led by the United States, dominates the market due to the presence of the world's largest financial centers, a high concentration of leading technology vendors and fintech innovators, and substantial R&D investment. Early adoption by major investment banks and hedge funds has created a mature ecosystem that continues to drive innovation and widespread implementation of AI technologies.

The Asia-Pacific region is the fastest-growing market, fueled by rapid digitalization, a burgeoning middle class seeking new investment avenues, and strong government support for technological advancement in financial hubs like Singapore, Hong Kong, and China. The region's vibrant fintech scene and increasing cross-border investments are accelerating the demand for intelligent asset management solutions.

COVID-19 Impact Analysis:

The COVID-19 pandemic acted as a powerful accelerant for AI adoption in the asset management sector. The unprecedented market volatility rendered many traditional risk models obsolete, highlighting the urgent need for more dynamic, adaptive AI-powered systems. The widespread shift to remote work further catalyzed investment in cloud-based AI solutions and automation to ensure business continuity and operational resilience. The crisis underscored the strategic necessity of data-driven decision-making, transforming AI from a long-term aspiration into an immediate operational imperative for navigating uncertainty and capturing emerging opportunities.

Latest Trends and Developments:

The most significant trend is the rise of Generative AI, which is being used to automate the creation of market commentary, client reports, and even initial investment hypotheses. Another key development is the focus on Explainable AI (XAI), driven by regulatory pressure to make algorithmic decisions transparent and interpretable. Hyper-personalization is also gaining traction, with AI engines crafting bespoke investment portfolios and financial advice for individual clients at scale. Finally, there's a growing trend of integrating AI with blockchain for enhanced security and transparent asset tokenization.

Key Players in the Market:

• BlackRock

• IBM

• Microsoft

• Amazon Web Services (AWS)

• S&P Global

• Genpact

• Infosys

• Charles Schwab

• Bridgewater Associates

• Renaissance Technologies

Chapter 1. Global AI In Asset Management Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global AI In Asset Management Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global AI In Asset Management Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global AI In Asset Management Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global AI In Asset Management Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global AI In Asset Management Market – By Technology

6.1. Introduction/Key Findings

6.2. Predictive Analytics and Forecasting

6.3. Machine Learning and Deep Learning

6.4. Natural Language Processing (NLP)

6.5. Robotic Process Automation (RPA)

6.6. Y-O-Y Growth trend Analysis By Technology

6.7. Absolute $ Opportunity Analysis By Technology, 2024-2030

Chapter 7. Global AI In Asset Management Market – By Application

7.1. Introduction/Key Findings

7.2. Portfolio Management and Optimization

7.3. Risk and Compliance Management

7.4. Algorithmic Trading

7.5. Customer Service and Acquisition

7.6. Fraud Detection and Prevention

7.7. Y-O-Y Growth trend Analysis By Application

7.8. Absolute $ Opportunity Analysis By Application, 2024-2030

Chapter 8. Global AI In Asset Management Market – By Deployment Model

8.1. Introduction/Key Findings

8.2. Cloud-based

8.3. On-premises

8.4. Hybrid

8.5. Y-O-Y Growth trend Analysis By Deployment Model

8.6. Absolute $ Opportunity Analysis By Deployment Model, 2024-2030

Chapter 9. Global AI In Asset Management Market – By Component

9.1. Introduction/Key Findings

9.2. Solutions

9.3. Services

9.4. Y-O-Y Growth trend Analysis By Component

9.5. Absolute $ Opportunity Analysis By Component, 2024-2030

Chapter 10. Global AI In Asset Management Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Technology

10.1.3. By Application

10.1.4. By Deployment Model

10.1.5. By Component

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Technology

10.2.3. By Application

10.2.4. By Deployment Model

10.2.5. By Component

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Technology

10.3.3. By Application

10.3.4. By Deployment Model

10.3.5. By Component

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Technology

10.4.3. By Application

10.4.4. By Deployment Model

10.4.5. By Component

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Technology

10.5.3. By Application

10.5.4. By Deployment Model

10.5.5. By Component

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global AI In Asset Management Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. BlackRock

11.2. IBM

11.3. Microsoft

11.4. Amazon Web Services (AWS)

11.5. S&P Global

11.6. Genpact

11.7. Infosys

11.8. Charles Schwab

11.9. Bridgewater Associates

11.10. Renaissance Technologies

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The primary growth drivers are the pressing need for greater operational efficiency and cost reduction in a competitive environment, and the ability to analyze massive volumes of traditional and alternative data to find new sources of investment returns (alpha).

The main challenges include high initial implementation costs, a significant shortage of talent with combined expertise in AI and finance, concerns over data security and privacy, and the regulatory demand for transparency and explainability in AI-driven decisions.

Key players include BlackRock, IBM, Microsoft, Amazon Web Services (AWS), S&P Global, Genpact, Infosys, Charles Schwab, Bridgewater Associates, Renaissance Technologies, Citadel, Two Sigma, Google, Oracle, and SAP.

North America currently holds the largest market share, estimated at around 42%, due to its mature financial industry, high technology adoption rates, and the presence of numerous leading AI vendors.

The Asia-Pacific region is expanding at the highest rate, driven by rapid digital transformation, a growing investor base, and significant investments in fintech and AI infrastructure across countries like China, Singapore, and India.