Global AI Edge Computing Market Research Report – Segmentation By Component (Hardware, Software, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, SMEs), By Application (Video Surveillance & Analytics, Predictive Maintenance, Autonomous Vehicles & Drones, Others), By Region – Forecast (2025 – 2030)

Published: 2025 - June

Report Code: IM-16476

Format:

Region: Global

Market Size and Overview:

The Global AI Edge Computing Market was valued at USD 20.78 billion in 2024 and is projected to reach a market size of USD 55.48 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 21.7%.

The convergence of edge computing and artificial intelligence drives this rapid growth by enabling real-time data processing near data sources, reducing latency, and conserving bandwidth across various applications, including video analytics, predictive maintenance, and autonomous systems.

Key Market Insights:

Reflecting significant spending in in-device inference capabilities, edge artificial intelligence hardware, including vision processors, smart gateways, and AI accelerators, controlled the most revenue share in 2024.

The main input for edge AI tasks is sensor data, environmental, motion, and biometric data, therefore highlighting the need for IoT in spreading AI-enabled edge applications.

Driven by security, traffic monitoring, and retail analytics applications requiring sub-second inference at the edge, video analytics applications make up the greatest application share.

AI Edge Computing Market Drivers:

The sudden surge in the number of IoT endpoints at a global level is driving the need for this market.

Together producing petabytes of raw data daily, this expansion encompasses smart sensors in manufacturing, video cameras in smart cities, and wearables in healthcare. Bringing this information to central clouds would overburden network infrastructure and entail exorbitant bandwidth costs without local processing. Edge AI systems solve this issue by gathering and evaluating data flows near or at the device, filtering noise, and generating insights before any transfer. On-site anomaly detection in vibration or temperature data stops real-time equipment failures in industrial environments. To track customer movement and automatically improve designs, merchants employ edge analytics on in-store cameras. Edge nodes in smart agriculture analyze soil moisture and weather sensor data to automate irrigation. Edge AI is necessary to preserve network health, provide real-time response, and enable scalable IoT deployments as IoT device numbers near 40 billion.

The rising demand for Ultra-low latency is said to drive the growth of this market at a rapid scale.

Emerging applications, autonomous vehicles, AR/VR systems, and smart-factory robots demand end-to-end latencies well below 10 milliseconds to function safely and effectively. While 5G-enabled tactile-Internet scenarios seek 1–5 ms round-trip times, research shows that perceptual stability depends on sub-17 ms latencies for VR head-tracking systems. Any lag beyond these limits will disrupt immersion in augmented reality (AR) / VR or jeopardize collision-avoidance systems in self-driving vehicles. Edge computing lowers round-trip delays by running artificial intelligence (AI) inference on-device or in local micro-data centers, therefore obviating the need for large-area network traversal. Ensuring assembly-line safety and throughput, robotic arms carry out accurate movements based on local artificial intelligence inference within 2–3 ms in manufacturing. Live video feeds in autonomous drones, likewise, go into object detection at the edge, which makes for immediate navigational corrections. Edge-based ultra-reliable low-latency communications (URLLC) will be the enabling next-generation, mission-critical applications demanding deterministic performance as networks grow toward 5G and beyond.

The existence of bandwidth constraints and costs is said to increase the demand for this market.

Rapidly saturate network links and raise operating costs when high-frequency sensor streams or raw high-definition video feeds are sent to the cloud. Edge AI reduces bandwidth consumption by as much as 90% in video analytics cases by conducting data filtering, aggregation, and compression locally, such that just metadata or actionable alerts travel across the WAN. A security camera with edge AI, for example, could send "person detected at 3 PM" alerts instead of constant HD streams, therefore saving valuable communication resources. In industrial IoT, vibration sensors process hundreds of readings per second into summarized health indicators, therefore reducing data transfers while retaining important insights. Smart-city implementations use edge nodes to instantly analyze traffic-camera feeds and send only congestion alerts to core systems. Besides alleviating network congestion, this local pre-processing cuts down on cloud ingress and egress fees. As companies grow their edge-AI deployments, maximizing bandwidth use becomes a major facilitator of affordable, widespread IoT rollouts.

The latest advancements seen in the field of edge AI chips are considered a major market growth driver.

Rapid breakthroughs in AI-optimized silicon are improving on-device inference performance and significantly lowering power consumption, hence enabling complex deep-learning algorithms at the edge. Driven by demand for high-efficiency NPUs and vision processors, the edge AI chip industry grew from USD 20.9 billion in 2024 at a blistering 33. 9% CAGR to a predicted USD 120.0 billion by 2030. Platforms like NVIDIA's Jetson series, Google's Edge TPU, and Intel's Movidius VPUs now deliver multi-TOPS (trillions of operations per second) inference performance at sub-10 W power envelopes. This jump allows for real-time computer vision in battery-powered drones, sub-millisecond speech recognition in smart assistants, and quick fault detection in industrial controllers. ASIC-based NPUs and FPGA accelerators further diversify the silicon landscape, offering tailored performance/power trade-offs for vertical markets. As chip designs increasingly incorporate more on-chip memory and sophisticated quantizing methods, edge-AI equipment will enable ever more complex models, opening new application possibilities in healthcare diagnostics, retail analytics, and autonomous robotics.

AI Edge Computing Market Restraints and Challenges:

The market is said to face a huge challenge from the problem of the integration process, which is complicated.

Operationalizing artificial intelligence at the edge requires combining various AI frameworks, TensorFlow, PyTorch, and ONNX, with heterogeneous hardware architectures—CPUs, GPUs, NPUs, FPGAs, and already existing legacy systems, each with unique interfaces and data schemes. As teams create CI/CD pipelines, handle model versioning, and build strong MLOps backends to meet data governance and compliance, Gartner claims end-to-end AI/ML operationalization can take 7–12 months. Between vendor-specific SDKs and target hardware, custom adapters and middleware are frequently needed to translate, therefore raising professional-services fees, usually USD 150–250 per hour, and lengthening time-to-value. Furthermore, organizational overhead is added by cross-functional teams of data scientists, software engineers, and IT operations since every group employs different tools and procedures. Furthermore, adding to complexity is the ongoing integration of AI model updates, which calls for thorough automated testing on limited edge nodes to prevent performance regressions. Many companies, therefore, employ managed-services partners to negotiate integration issues, but this adds to OPEX and might lead to vendor-lock-in hazards.

The risk related to the security and privacy of data and rising cases of data breaches are also major challenges for the market.

Decentralized edge nodes increase the attack surface as every device could be a vector for malware, firmware manipulation, or data exfiltration. Ensuring only authorized firmware loads, secure boot mechanisms based on hardware root-of-trust modules must be used throughout thousands of distributed endpoints to be effective. Using Hardware Security Modules (HSMs) to implement and manage cryptographic keys adds design complexity and cost, while data at rest and in transit needs AES-256 encryption and TLS/DTLS channels. Additionally, compliance with GDPR, CCPA, and emerging PIPL rules calls for on-device data anonymization and audit-trail capabilities, thereby increasing firmware complexity and R&D budgets. According to a current MDPI study, edge-level security requirements are still in their early stages, therefore generating gaps in real-time threat detection and centralized identity management across layers.

The existence of fragmented standards for the market globally hinders the operational efficiency of the market.

Edge-AI ecosystems struggle with a quilt of proprietary APIs, communication protocols, and data formats that impede flawless interoperability. 68% of edge-AI projects invest an additional 4 to 6 months fixing compatibility problems between chipsets and frameworks like TensorFlow Lite versus PyTorch Mobile. Open initiatives, ONNX for model exchange, and Kubernetes for edge container orchestration are attracting attention, but adoption is uneven across vendors and regions. Hardware modularity and virtualization can increase device lifespans, the ECS SRIA observes, but true standardization must begin at design time to prevent restrictive or too general requirements. At large in IoT, platform fragmentation persists: no one protocol unifies wireless (Wi-Fi, Bluetooth, LoRa, NB-IoT) and compute interfaces, therefore necessitating custom middleware and raising development and maintenance expenses.

The constraints faced by the market in the fields of power and thermal are said to negatively impact the growth potential of the market.

Operating in hostile settings, extreme temperatures, dust, vibration, with limited access to active cooling and inconsistent electricity, edge-AI devices often need thermal solutions like liquid cooling, heat pipes, and IP-rated sealed enclosures to maintain optimum operating conditions from –40°C to 70°C. Typical AI accelerators (e.g., NVIDIA Jetson, Intel Xeon D-2100) have TDPs ranging from 60–110 W, challenging passive‐cooling designs ℅ for QATS. Device operating conditions ranging from –40°C to 70°C require thermal solutions like liquid cooling, heat pipes, and IP-rated sealed enclosures; in remote or solar-powered sites, devices must balance continuous real-time inference with sub-10 W power budgets; dynamic frequency scaling and low-power NPUs can reduce consumption by up to 30%. Material innovations, thermally conductive enclosures, and advanced thermal interface materials are essential but add BOM cost and weight. Edge-AI equipment has to include sophisticated thermal management and energy-aware scheduling in order to maintain performance and reliability as compute densities rise to enable bigger models.

AI Edge Computing Market Opportunities:

The emergence of 5 G-enabled edge AI is transforming this market at a rapid pace, creating a good market opportunity.

As enterprises plan over 10,000 private 5G installations by 2026, DCI and edge-AI alliances between telecom and hardware providers will be critical to unlocking next-generation use cases. For autonomous vehicles on factory floors, 5G backhaul to edge servers reduces inference latencies to sub-5 ms, ensuring safe navigation and collision avoidance. In smart-grid deployments,5G-enabled edge nodes process sensor data locally for real-time voltage regulation before forwarding summaries to central management systems. By 2027, over 30% of industrial IoT traffic will traverse private 5G networks, up from under 5%, reflecting enterprises’ appetite for deterministic performance in control-loop scenarios. Edge-AI vendors are integrating 5G network-slice orchestration directly into their platforms, enabling on-demand bandwidth adjustments and end-to-end QoS guarantees. Verizon’s contract at the UK’s Thames Freeport illustrates how dedicated 5G connectivity is now underpinning predictive maintenance analytics and real-time logistics coordination on manufacturing floors and port facilities.

The growing use of Healthcare IoT and remote monitoring due to the pandemic is said to be a major market growth opportunity.

By directly integrating smart analytics into medical equipment and gateways, edge artificial intelligence is transforming patient care. As hospitals and home-care providers start to utilize edge-powered vitals analysis to triage patients in real time, the worldwide AI-enabled remote patient-monitoring market at USD 1.99 billion in 2024 with a projected 27.98% CAGR through 2030. Driven by the increasing number of IoMT sensors, edge computing in healthcare rose from USD 4.5 billion to a projected USD 43.8 billion by 2033, highlighting a 26.3% CAGR. Through on-device processing of ECG, blood-oxygen, and imaging data, edge AI lowers cloud-ingress loads by more than 70%, lowers data-transmission latency, and guarantees HIPAA/GDPR compliance via local anonymization. While rural clinics use portable edge-AI scanners to examine ultrasound photos on-site, critical-care units use bedside edge nodes for arrhythmia detection within milliseconds. Payers are increasingly rewarding telemedicine initiatives; thus, edge-AI integration is a vital enabler for affordable, scalable healthcare delivery.

The deployment of this market in smart cities is helping the market to gain popularity and hence a faster growth rate too.

To improve resilience, sustainability, and citizen services, cities all around are including edge artificial intelligence into their infrastructure. With edge AI as a fundamental component for traffic, public safety, and environmental monitoring, the smart-cities market is surging from USD 623.9 billion to USD 4,647.6 billion at a 25.2% CAGR by 2032. AI-driven traffic-management systems, like India’s first ATMS on Delhi’s Dwarka Expressway, use high-resolution cameras and edge inference to optimize signal timings and reduce congestion by up to 25% in real time. Environmental sensors set at edge gateways locally analyze air quality, noise, and weather data to provide instant alarms for contamination peaks or flood dangers. Public-safety networks stream ANPR and video analytics at the edge, guaranteeing compliance with privacy rules by discarding identifiable on-device data. Smart-lighting and energy systems cut municipal energy costs by 30% by using edge AI to adjust streetlight brightness to pedestrian flows. Scaled urban-intelligence projects rely on vendor alliances with system integrators and telecom companies as over 1,000 cities worldwide pilot edge-AI programs.

The emergence of AI-driven robotics and automation is also considered to be an important market growth opportunity.

New degrees of independence in mobile robots, drones, and industrial automation are made possible by the convergence of edge artificial intelligence and robotics. A Wall Street Journal feature underlines significant investments, from Elon Musk's robotaxi trials to Daniel Ek's $691 million infusion into Helsing's AI drone endeavors, thus showing investor faith in "hard tech" applications of edge AI. For warehouse logistics, edge-embedded computer vision enables automated guided vehicles to perform real-time pallet recognition and obstacle avoidance, reducing collision incidents by over 50%. Agriculture drones, powered by onboard AI accelerators, process multispectral imagery at 30 FPS to detect crop stress zones instantaneously, optimizing inputs and boosting yields. In healthcare logistics, autonomous robots navigate hospital corridors with sub-10 ms latency, delivering medications and supplies without human intervention. Robotics vendors are integrating low-power NPUs (e.g., Arm Ethos, Google Coral) to sustain continuous edge inference on battery-powered platforms. As global robotics spending surpasses USD 200 billion by 2025, edge-AI architectures will be pivotal in scaling fully autonomous systems across industries.

AI Edge Computing Market Segmentation:

Market Segmentation: By Component

• Hardware

• Software

• Services

The Hardware segment is said to dominate this market. Driven by significant investment in on-device inference skills for low-latency applications, hardware, including accelerators (e.g., NVIDIA Jetson, Google Edge TPU), vision processors, and smart gateways, comprised the largest share in 2024. The Software segment is said to be the fastest-growing segment. This is because the Edge AI platforms are said to record the highest CAGR as the enterprises are standardizing deployment, automating life cycle management, and are also integrating distributed AI workloads. When it comes to the Services segment, as businesses look for ready-made edge-AI solutions and outsource difficult multi-vendor environments, professional and managed services, including consulting, integration, and continuing support, are expanding steadily.

Market Segmentation: By Deployment Mode

• Cloud-based

• On-premises

The On-premises segment is said to dominate this market due to highly regulated industries, tight latency guarantees, offline resilience, and data sovereignty. The Cloud-based segment is said to be the fastest-growing segment here, driven by demands for centralized model training, over-the-air updates, and scalable orchestration throughout geographically dispersed edge nodes. Cloud-enabled edge platforms are expanding fastest.

Market Segmentation: By Organization Size

• Large Enterprises

• SMEs

The Large Enterprises segment is said to lead this market, leveraging significant budgets, major corporations drive adoption by deploying fleet-wide edge-AI systems for enterprise security, smart-city efforts, and manufacturing automation. The SMEs segment is the fastest-growing segment of the market. Modular, pay-as-you-go edge-AI solutions and managed services that reduce entry barriers and minimize initial expenditures enable SMEs to be the fastest-growing sector.

Market Segmentation: By Application

• Video Surveillance & Analytics

• Predictive Maintenance

• Autonomous Vehicles & Drones

• Others

The Video Surveillance & Analytics segment is said to dominate this market, and the Predictive Maintenance segment is the fastest-growing segment. The greatest application share in 2024 was security and smart-city video analytics, as edge inference allows sub-second threat detection without consuming network bandwidth. Applications for industrial IoT, employing edge-AI to examine sensor streams for early fault detection, are expanding most rapidly and lowering maintenance expenditures and downtime throughout the energy and manufacturing industries.

For the Autonomous Vehicles and Drones segment, real-time object detection and navigation tasks make use of on-device artificial intelligence for safety-critical operations in supply chain and transportation. The Others segment includes environmental monitoring, retail analytics (such as cashier-less checkout), and AR/VR processing, all of which show strong niche expansion.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

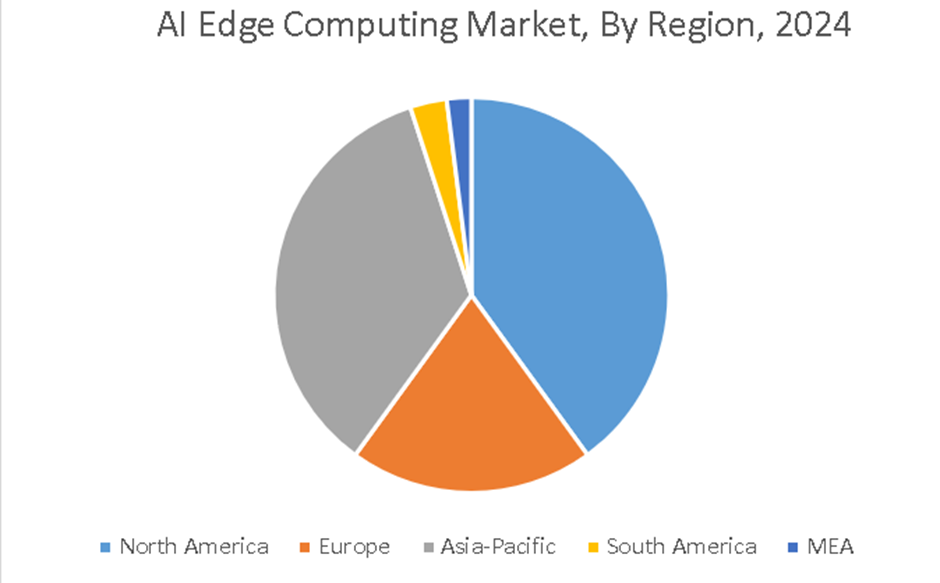

North America is said to lead this market. Driven by early edge-AI adoption, dense IoT deployments, and significant R&D investments by hyperscalers and semiconductor companies, North America dominated the market in 2024. The Asia-Pacific region is the fastest-growing segment, backed by fast industrial automation in China and India, government smart-city initiatives, and expanding artificial intelligence research ecosystems. APAC is expected to record the highest CAGR by 2030.

Europe, on the other hand, is said to have shown steady growth when it comes to this market. This region is supported by strict rules regarding the privacy of data. It is also defined by the robust IoT adoption in places like Germany and the U.K. Both South America and the MEA regions are considered to be emerging markets. Growing interest in edge-AI for fields like agriculture, retail, and public safety, coupled with quickening investments in digital infrastructure, characterizes emerging markets.

COVID-19 Impact Analysis on the Global AI Edge Computing Market:

As companies aimed to reduce on-site staff and guarantee business continuity, the COVID-19 epidemic hastened the adoption of edge AI. High demand resulted in automated surveillance, retail analytics in unmanned stores, and remote-monitoring applications in healthcare. On the other hand, early supply chain disruptions postponed product releases. The crisis highlighted the need for decentralized intelligence; therefore, many companies fast-tracked edge-AI pilot initiatives into production deployments.

Latest Trends/ Developments:

Ultra-lightweight artificial intelligence models operating on microcontrollers allow for voice, gesture, and abnormality detection in highly ingrained uses.

Sharing model updates instead of unprocessed data helps distributed artificial intelligence training over edge nodes to maintain confidentiality.

Vendors are integrating 5G connectivity, real-time operating systems, and artificial intelligence accelerators into integrated edge-computing devices.

With subscription-based pricing, cloud providers and integrators are increasingly presenting completely managed edge-AI solutions.

Key Players:

• Vapor IO

• CISCO Systems, Inc.

• Saguna Networks Ltd.

• Huawei Technologies Co., Ltd

• International Business Machine Corporation

• RIGADO LLC

• Foghorn Systems

• Clearblade, Inc.

• NOKIA

• Hewlett-Packard Enterprise Development LP

Chapter 1. Global AI Edge Computing Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global AI Edge Computing Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global AI Edge Computing Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global AI Edge Computing Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global AI Edge Computing Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global AI Edge Computing Market- By Component

6.1. Introduction/Key Findings

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. Global AI Edge Computing Market– By Deployment Mode

7.1 Introduction/Key Findings

7.2. Cloud-based

7.3. On-premises

7.4. Y-O-Y Growth trend Analysis By Deployment Mode

7.5. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global AI Edge Computing Market– By Organization Size

8.1. Introduction/Key Findings

8.2. Large Enterprises

8.3. SMEs

8.4. Y-O-Y Growth trend Analysis By Organization Size

8.5. Absolute $ Opportunity Analysis By Organization Size, 2025-2030

Chapter 9. Global AI Edge Computing Market– By Application

9.1. Introduction/Key Findings

9.2. Video Surveillance & Analytics

9.3. Predictive Maintenance

9.4. Autonomous Vehicles & Drones

9.5. Others

9.6. Y-O-Y Growth trend Analysis By Application

9.7. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 10. Global AI Edge Computing Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Component

10.1.3. By Deployment Mode

10.1.4. By Organization Size

10.1.5. By Application

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Component

10.2.3. By Deployment Mode

10.2.4. By Organization Size

10.2.5. By Application

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Component

10.3.3. By Deployment Mode

10.3.4. By Organization Size

10.3.5. By Application

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Component

10.4.3. By Deployment Mode

10.4.4. By Organization Size

10.4.5. By Application

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Component

10.5.3. By Deployment Mode

10.5.4. By Organization Size

10.5.5. By Application

10.5.6. By Region

Chapter 11. Global AI Edge Computing Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Vapor IO

11.2. CISCO Systems, Inc.

11.3. Saguna Networks Ltd.

11.4. Huawei Technologies Co., Ltd

11.5. International Business Machine Corporation

11.6. RIGADO LLC

11.7. Foghorn Systems

11.8. Clearblade, Inc.

11.9. NOKIA

11.10. Hewlett-Packard Enterprise Development LP

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global AI Edge Computing Market was valued at USD 20.78 billion in 2024 and is projected to reach a market size of USD 55.48 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 21.7%.

Driving factors are the explosion of IoT endpoints, demand for sub-10 ms inference latencies, bandwidth restrictions on cloud transfers, and the rise of strong edge-AI chipsets.

Led by artificial intelligence accelerators, edge servers, and smart cameras that do on-device inference for latency-sensitive apps, the hardware segment rules this market.

Investments in remote-monitoring edge systems for healthcare, automated retail, and unmanned surveillance increased as the epidemic drove supply-chain delays, outweighing early impacts.

The major obstacles are integration complexity, broken standards, security/privacy risks, and balancing compute density with power/thermal constraints.