Agriculture Drone Market Research Report – Segmentation by Drone Type (Fixed-Wing, Rotary Blade, Hybrid); By Component (Hardware, Software, Services); Region – Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-10352

Format:

Region: Global

Market Size and Overview:

The Agriculture Drone Market was valued at USD 3.65 billion and is projected to reach a market size of USD 9.30 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 20.56%.

Agriculture drones represent a rapidly evolving technology in the 21st-century farming landscape, revolutionizing traditional agricultural practices through advanced aerial monitoring and precision application capabilities. With continuous technological advancements in sensors, imaging, autonomous flight, and data analytics, agriculture drones have attracted significant interest from both academic researchers and commercial agriculture professionals. The growing integration of these unmanned aerial vehicles into farming operations is creating substantial opportunities for increased efficiency, sustainability, and productivity in global agriculture systems.

Key Market Insights:

According to the International Association of Precision Agriculture (IAPA) survey, approximately 65% of large-scale farms have implemented drone technology in at least one aspect of their operations, representing a 27% increase from 2020 and highlighting the accelerating adoption rate of this technology.

Drone-based crop monitoring has demonstrated yield improvements averaging 18.3% across diverse crop types while reducing chemical application volumes by 30-40%, according to the Agricultural Drone Technology Assessment published by Cornell University, establishing these systems as economically viable investments with typical ROI periods of 12-18 months.

In North America, agriculture drones equipped with multispectral imaging capabilities have achieved 93% accuracy in early disease detection when paired with appropriate AI analytics platforms, enabling treatment interventions approximately 11.5 days earlier than conventional scouting methods according to the American Farm Technology Institute's 2023 report.

The USDA Precision Agriculture Survey indicates that farms utilizing drone technology for variable rate applications have realized input cost savings averaging $32.50 per acre across fertilizer, pesticide and water usage, while simultaneously reducing environmental impacts and improving compliance with increasingly stringent agricultural regulations.

Agriculture Drone Market Drivers:

The increasing global food demand coupled with declining agricultural labour availability is driving unprecedented adoption of drone technology in farming operations worldwide.

With global population projected to reach 9.8 billion by 2050, agricultural production must increase by approximately 70% to meet anticipated food demand according to FAO estimates. This requirement coincides with declining agricultural workforces in most regions, with developed nations experiencing 2.1% annual reductions in available farm labour and developing countries showing similar trends as urbanization accelerates. Agriculture drones directly address this challenge by multiplying human efficiency - a single drone operator can survey approximately 700 acres daily compared to 25 acres through traditional field walking methods, representing a 28-fold productivity increase for monitoring operations. The impact is particularly significant in specialized operations like crop scouting, where drones equipped with multispectral imaging can identify pest infestations, nutrient deficiencies, and water stress with 96% accuracy compared to ground verification. Advanced spraying drones demonstrate application precision within 2.5cm and can treat approximately 40-60 acres per day with 30-40% less chemical usage than conventional methods, simultaneously addressing efficiency and sustainability concerns. Data from the International Drone Agricultural Network indicates farms implementing comprehensive drone programs have documented average operational cost reductions of 25-30% across monitoring, application, and management activities while increasing yields by 14.3% through more timely interventions and precise resource application.

Regulatory evolution and technological convergence are accelerating agriculture drone adoption across diverse farming operations.

Regulatory frameworks governing unmanned aerial vehicles have evolved significantly since 2018, with 72% of major agricultural markets implementing specific provisions for agricultural drone operations that reduce compliance complexity and operational restrictions. These regulatory improvements have coincided with dramatic hardware advances, as agriculture-specific drones have achieved average flight time increases of 137% while simultaneously reducing acquisition costs by approximately 45% compared to 2018 models, significantly improving accessibility and operational economics. Modern agriculture drones now integrate seamlessly with farm management information systems, precision agriculture platforms, and IoT sensor networks, creating comprehensive digital ecosystems that multiply the value of individual technologies through data integration and synchronized operation.

Agriculture Drone Market Restraints and Challenges:

The implementation of drones has high initial setup costs which means that these drones are not as widely accessible.

Despite their promising benefits, agriculture drones face significant adoption barriers including high initial investment requirements ranging from $3,000 for basic models to over $25,000 for advanced systems with specialized sensors and application capabilities. Technical complexity presents additional challenges, with surveys indicating approximately 47% of farmers report difficulty integrating drone data with existing management systems and 38% express concerns about operational learning curves and maintenance requirements. Infrastructure limitations including inadequate rural internet connectivity (affecting real-time data transmission in 63% of global agricultural regions) and restricted access to repair services further complicate adoption.

Agriculture Drone Market Opportunities:

The integration of artificial intelligence with agriculture drone platforms presents tremendous growth opportunities, with AI-enhanced image processing capabilities improving detection accuracy by 35-45% while reducing analysis time by 87% compared to manual interpretation methods. Developing economies represent vast untapped markets, with agricultural drone penetration below 8% in regions like Southeast Asia, Africa, and Latin America despite their substantial agricultural sectors, creating expansion opportunities for manufacturers and service providers. Specialized applications including pollination assistance (addressing global pollinator declines), carbon sequestration verification (supporting emerging carbon credit markets), and microclimate monitoring are creating new market segments with premium service potential and reduced competition

Agriculture Drone Market Segmentation:

Market Segmentation: By Drone Type:

• Fixed-Wing

• Rotary Blade

• Hybrid

Based on drone type, the rotary blade segment dominated the market with approximately 67.3% revenue share. This dominance stems from rotary drones' superior manoeuvrability, ability to hover precisely over target areas, and vertical take-off and landing capabilities that eliminate the need for runways or specialized launching equipment. Their versatility across diverse applications including detailed crop inspection, spot spraying, and operation in confined areas makes them particularly suitable for small and medium-sized farms, which constitute approximately 85% of global farming operations. Additionally, recent technological advancements have extended rotary drone flight times by an average of 42% while improving payload capacities by 35% compared to 2019 models, further enhancing their practical utility.

The hybrid segment is projected to grow at the highest CAGR of 32.7% during the forecast period. This accelerated growth is driven by hybrid drones' unique combination of fixed-wing efficiency for covering large areas with rotary-style hovering capabilities for detailed inspection and precision application. Modern hybrid agriculture drones can survey approximately 300-400 acres on a single battery charge while maintaining the ability to transition to stationary flight for high-resolution imaging or targeted applications. This dual capability makes them increasingly attractive for larger operations seeking to maximize operational efficiency without sacrificing precision.

Market Segmentation: By Component

• Hardware

• Software

• Services

The hardware segment held the largest market share at 58.4% in 2022, encompassing the physical drone platforms, specialized sensors, cameras, spraying systems, and related equipment essential for agricultural drone operations. The dramatic evolution of agriculture-specific hardware features including enhanced battery systems (increasing average flight times from 22 minutes in 2018 to 52 minutes in 2022), specialized multispectral and thermal imaging sensors, and precision application systems has driven substantial replacement and upgrade cycles. Hardware innovations including spray tanks with electronically controlled nozzles that adjust flow rates based on flight speed and plant canopy density have improved application precision by approximately 40% compared to previous generation systems, creating compelling value propositions for upgrading existing equipment.

The software and analytics segment is anticipated to witness the fastest growth rate during the forecast period, with a CAGR of 29.8%. This growth reflects the increasing recognition that data collection without sophisticated analysis provides limited actionable value to farmers. Advanced software platforms incorporating machine learning algorithms have demonstrated 93% accuracy in automatically identifying over 27 common crop diseases from drone imagery, compared to 76% accuracy with conventional analysis methods. The expanding capabilities of agriculture drone software, including automated flight planning that optimizes coverage patterns based on field boundaries and crop characteristics, real-time analysis that can identify issues during flights rather than after processing, and integration with farm management information systems that convert drone data into specific application prescriptions, are creating substantial value beyond the physical drone platforms themselves.

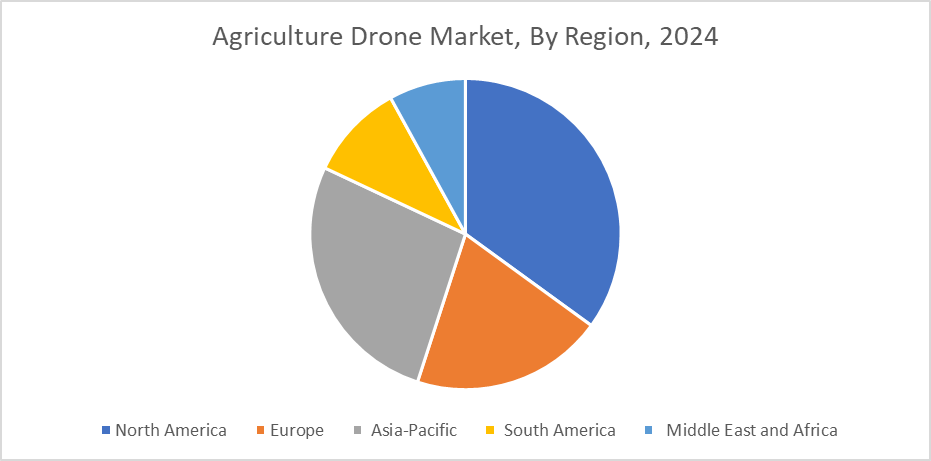

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

The North American region dominated the global agriculture drone market with a revenue share of 35%. This leadership position stems from the region's early regulatory accommodations for commercial drone applications, high technology adoption rates among large-scale farming operations, and well-developed precision agriculture infrastructure that facilitates integration of drone-derived data. The United States Department of Agriculture reports that approximately 43% of farms exceeding 2,000 acres have implemented drone technology in at least one operational area, with adoption rates increasing approximately 14% annually. The region's advanced agriculture technology ecosystem, including established relationships between drone manufacturers, farm management software developers, and agricultural consultants, has created efficient adoption pathways that reduce implementation challenges.

The Asia-Pacific region is projected to experience the fastest growth rate with an anticipated CAGR of 28.7% during the forecast period. This exceptional growth potential is driven by several converging factors, including the predominance of smallholder farming systems that benefit particularly from the operational scale and efficiency of drone technology, substantial government initiatives to modernize agricultural practices (with seven major countries implementing specific drone subsidy programs since 2020), and pressing labour shortages in rural areas. China has emerged as a particularly significant market, accounting for approximately 56% of regional agriculture drone deployments with over 42,000 units operating commercially. Japanese rice farmers have demonstrated leadership in specialized applications, with approximately 38% of rice cultivation areas receiving at least one drone-based treatment annually, establishing application protocols that are being adapted throughout the region.

COVID-19 Impact Analysis on the Global Agriculture Drone Market:

The COVID-19 pandemic created unprecedented disruptions in global supply chains while simultaneously accelerating certain aspects of agriculture drone adoption. Manufacturing facilities experienced production capacity reductions averaging 30-50% during peak restriction periods, creating delivery delays averaging 2-4 months for specialized agricultural models. Component shortages, particularly for semiconductor chips used in flight controllers, cameras, and navigation systems, resulted in temporary price increases of 15-22% across multiple drone categories and forced some manufacturers to redesign systems to accommodate available components.

Paradoxically, pandemic-related labour shortages in agricultural regions drove substantial interest in automation technologies including drones, with new agriculture drone implementations increasing by 37% in 2021 despite supply constraints. Government initiatives to strengthen food security and agricultural resilience in response to pandemic vulnerabilities included approximately $1.8 billion in programs specifically supporting farm technology adoption, with drones frequently highlighted as priority technologies.

Latest Trends/ Developments:

Integration of hyperspectral imaging technology with agricultural drones has advanced significantly, with new sensors capable of capturing data across 150+ spectral bands enabling identification of plant stress, disease presence, and nutritional deficiencies with 94% accuracy approximately 7-10 days before visual symptoms appear.

DJI's 2022 launch of the Agras T40 agricultural spraying drone capable of carrying 40kg of liquid payload represents a significant advancement in application capacity, with operational efficiency improvements of approximately 60% compared to previous generation systems and the ability to treat 40 acres per hour.

Key Players:

• DJI

• PrecisionHawk

• AeroVironment, Inc.

• Parrot Drone SAS

• AgEagle Aerial Systems

• senseFly (acquired by AgEagle)

• XAG Co., Ltd.

• Yamaha Motor Corporation

• American Robotics, Inc.

• Trimble Inc.

Chapter 1. AGRICULTURE DRONES MARKET– Scope & Methodology

1.1. Market Segmentation

1.2. Assumptions

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. AGRICULTURE DRONES MARKET– Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.3. COVID-92 Impact Analysis

2.3.1. Impact during 2023 – 2030

2.3.2. Impact on Supply – Demand

Chapter 3. AGRICULTURE DRONES MARKET– Competition Scenario

3.1. Market Share Analysis

3.2. Product Benchmarking

3.3. Competitive Strategy & Development Scenario

3.4. Competitive Pricing Analysis

3.5. Supplier - Distributor Analysis

Chapter 4. AGRICULTURE DRONES MARKET- Entry Scenario

4.1. Case Studies – Start-up/Thriving Companies

4.2. Regulatory Scenario - By Region

4.3 Customer Analysis

4.4. Porter's Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. AGRICULTURE DRONES MARKET- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. AGRICULTURE DRONES MARKET– By Component

6.1. Hardware

6.1.1. Frames

6.1.2. Control System

6.1.3. Propulsion System

6.1.4. Navigation System

6.1.5. Payload

6.1.6. Avionics

6.1.7. Others

6.2. Software

6.2.1. Imaging Software

6.2.2. Data Management Software

6.2.3. Data Analytics Software

6.2.4. Others

Chapter 7. AGRICULTURE DRONES MARKET– By Application

7.1. Crop Monitoring

7.2. Soil & Field Analysis

7.3. Planting & Seeding

7.4. Crop Spray

7.5. Others

Chapter 8. AGRICULTURE DRONES MARKET– By Type

8.1. Fixed-Wing

8.2. Rotary-Wing

8.3. Others

Chapter 9. AGRICULTURE DRONES MARKET– By Region

9.1. North America

9.2. Europe

9.3. The Asia Pacific

9.4. Latin America

9.5. Middle-East and Africa

Chapter 10. AGRICULTURE DRONES MARKET – Company Profiles – (Overview, Product Portfolio, Financials, Developments)

10.1. Company 1

10.2. Company 2

10.3. Company 3

10.4. Company 4

10.5. Company 5

10.6. Company 6

10.7. Company 7

10.8. Company 8

10.9. Company 9

10.10. Company 10

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

It refers to the use and commercialization of drones in farming for tasks like crop monitoring, spraying, mapping, and data collection to improve productivity and efficiency.

Drones are used for aerial surveillance, soil analysis, irrigation management, precision spraying, plant health assessment, and yield prediction.

They save time, reduce input costs, enhance crop yields, enable precise targeting of resources, and support data-driven decisions.

Key challenges include high initial costs, lack of operator training, regulatory restrictions, and data privacy concerns.

North America and Asia-Pacific, particularly the U.S., China, and Japan, lead due to supportive policies, advanced tech, and large-scale farms.