Aerogel Market Research Report – By Product (Silica, Carbon, Polymers and Others); By Technology (Supercritical Drying and Other Drying); By Form (Blanket, Panel, Particle and Monolith); By End-use (Building & Construction, Oil & Gas, Aerospace & Marine, Automotive, Performance Coatings and Others); and Region - Size, Share, Growth Analysis | Forecast (2025 – 2030)

Published: 2024 - January

Report Code: IM-5901

Format:

Region: Global

Market Size and Overview:

The Aerogel Market was valued at USD 1.9 billion in 2024. Over the forecast period of 2025-2030 it is projected to reach USD 3.55 billion by 2030, growing at a CAGR of 13.30%.

Aerogels are lightweight solid materials known for their exceptional properties. Nonetheless, recent advancements in technology have led to more efficient manufacturing approaches. The production process involves extracting liquid from a gel through a defined technique, resulting in a three-dimensional nanoporous structure containing 80 to 99% air. While aerogels can be derived from various substances, silica is most commonly used, resulting in what is known as silica aerogel.

Key Market Insights:

The aerospace and defense industries constitute a significant segment of the aerogel market, driven by the demand for lightweight materials capable of withstanding extreme temperatures and harsh conditions. Aerogels are being increasingly adopted for applications such as spacecraft and aircraft insulation, as well as protective equipment used in military operations. The focus on reducing weight to enhance fuel efficiency and overall system performance continues to fuel the demand for aerogel-based solutions, solidifying their role in high-performance environments.

Moreover, the heightened awareness of environmental concerns and the transition toward sustainable materials are playing a vital role in shaping market dynamics. As industries aim to reduce their environmental impact, aerogels offer a compelling alternative due to their low density and superior performance. Additionally, continued advancements in bio-based aerogels and eco-friendly production techniques are expected to draw further investment and interest, contributing to market growth. With sustainability emerging as a key priority, aerogels are well-positioned to capitalize on this trend, strengthening their position as a transformative material across diverse sectors.

Aerogel Market Drivers:

The global aerogel market is characterized by distinct attributes that make aerogel an appealing material for a wide range of applications.

Due to its exceptionally large surface area, ultra-lightweight nature, and low thermal conductivity, aerogel serves as an effective insulating material across numerous industries and commercial applications.

The rising demand for energy-efficient buildings, combined with the need for advanced thermal insulation in sectors such as oil and gas, automotive, construction, and aerospace, is driving dynamic growth within the aerogel market. Aerogel is also widely utilized in environmental remediation and as an electrode material for supercapacitors.

Moreover, the increasing emphasis on sustainability and eco-friendly technologies is further propelling the demand for aerogel. This focus has led to the development of innovative applications, particularly in the energy sector, positioning aerogel as a sustainable alternative to conventional insulation materials.

With its unique properties and expanding role across diverse industries, the global aerogel market is anticipated to witness substantial growth in the coming years, fueled by the ongoing shift toward energy-efficient and sustainable solutions.

Aerogel Market Restraints and Challenges:

Elevated production costs act as a limiting factor to the growth of the aerogel market.

Several elements contribute to the elevated cost of silica aerogels, including expensive raw materials, the intricacies of the manufacturing process, and the capital investment required for establishing production infrastructure. Additionally, the development of aerogel materials involves significant research and development efforts, further increasing overall costs. The manufacturing process itself is highly specialized and demands complex facilities. Among the various stages, supercritical drying is notably the most cost-intensive step in aerogel production.

Aerogel Market Opportunities:

The construction industry represents a key end-user of aerogels, particularly for advanced insulation applications.

The demand for energy-efficient materials such as aerogels is expected to grow as governments and industries worldwide seek effective solutions to reduce energy consumption and lower carbon emissions.

With the rise in construction activity across emerging economies and the global push for energy-efficient buildings, the aerogel market is projected to witness significant growth.

In the automotive industry, the use of aerogels is also increasing, driven by the need to reduce component weight and enhance fuel efficiency. As sales of electric vehicles continue to rise and consumer demand for lightweight materials intensifies, the aerogel market is poised for further expansion.

Aerogel Market Segmentation:

By Product:

● Silica

● Carbon

● Polymers

● Others

The silica segment has accounted for the largest share of the aerogel market. Silica aerogels have gained significant global attention due to their favorable chemical characteristics and wide-ranging existing and potential applications across various technological fields. These nanostructured materials are known for their high specific surface area, elevated porosity, low density, low dielectric constant, and outstanding thermal insulation capabilities.

Concurrently, the polymer aerogel segment is projected to achieve the highest growth rate throughout the forecast period. This growth is driven by the superior chemical and physical attributes of polymer aerogels compared to their silica counterparts. When fabricated in monolithic form, polymers exhibit strong mechanical properties; however, they may sacrifice some of the key advantages provided by silica aerogels, such as transparency and low thermal conductivity.

The carbon aerogel segment is also projected to witness significant growth over the forecast period, primarily due to the rising demand for energy storage solutions. Carbon aerogels possess high mass-specific surface areas and electrical conductivity while offering strong environmental compatibility. Despite their relatively low chemical inertness, these materials hold promise in a variety of applications, including catalysis, sorbents, distillation, and energy storage.

By Technology:

● Supercritical Drying

● Other Drying

The blanket segment has captured the largest share of the aerogel market. Aerogel blankets, primarily composed of silica aerogels, are recognized for their outstanding thermal resistance and low density. These properties make them particularly suitable for high-performance insulation applications across industries such as aerospace, construction, and oil and gas. With global emphasis on energy efficiency, the demand for advanced insulation materials has accelerated the innovation and widespread adoption of aerogel blankets.

The panel segment is projected to exhibit the fastest growth during the forecast period. Typically manufactured using silica aerogels, aerogel panels offer excellent thermal insulation characteristics, making them ideal for use in construction, automotive, and aerospace sectors. Their lightweight structure and energy-efficient performance are increasingly valued in applications where sustainability and performance optimization are key. The rising awareness of green building standards and energy-saving measures continues to boost the demand for aerogel panels.

By Form:

● Blanket

● Panel

● Particle

● Monolith

The oil & gas segment accounted for the largest share of the aerogel market. Aerogels, characterized by their high porosity, low density, superior thermal insulation, and robust mechanical strength, are particularly valuable in the oil and gas industry. These properties are essential for effective thermal management during drilling, transportation, and refining processes. Aerogels’ ability to endure extreme temperatures while providing efficient insulation contributes to energy savings and enhances safety within oil and gas facilities.

The performance coatings segment is expected to experience the fastest growth over the forecast period. As industries strive to lower their carbon emissions, the integration of aerogels into coatings supports these efforts by reducing energy consumption in heating and cooling applications. Furthermore, advancements in aerogel manufacturing are improving cost-effectiveness and accessibility, thereby expanding their use across a wider range of applications.

By End-use:

● Building & Construction

● Oil & Gas

● Aerospace & Marine

● Automotive

● Performance Coatings

● Others

The supercritical drying segment has dominated the market due to its ability to preserve the three-dimensional pore structure of aerogels. This preservation results in distinctive properties such as high porosity, low density, and an extensive surface area. Supercritical drying, which involves the removal of solvents from aerogel pores using supercritical fluids, is a widely utilized technique for drying wet gels.

This method is crucial for transitioning drying processes from laboratory-scale setups to pilot and industrial production, enabling the evaluation of aerogel manufacturing economics at scale. High-temperature supercritical drying with organic solvents is particularly effective in minimizing shrinkage, resulting in aerogels with densities lower than those produced using carbon dioxide.

Freeze-drying represents an alternative drying technology for wet gels. This process involves freezing the solvents within the pores by lowering the temperature below their freezing point. Subsequently, the pressure is reduced below the sublimation threshold through vacuum application, allowing the solvent to sublimate directly from solid to gas phase.

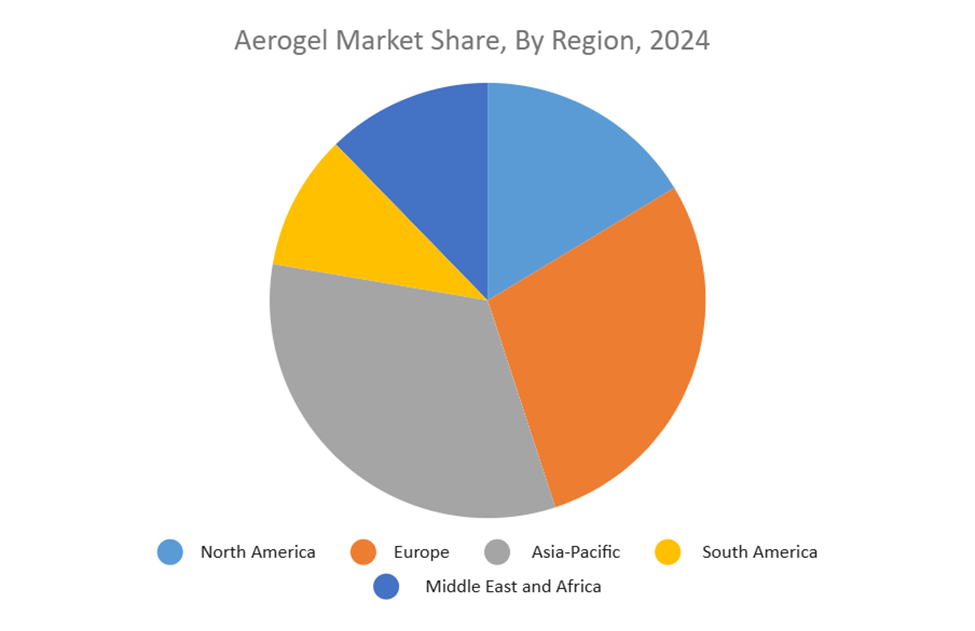

Aerogel Market Segmentation- by region

● North America

● Europe

● Asia Pacific

● South America

● Middle East & Africa

The North American aerogel market has emerged as a dominant force in the industry, propelled by rising demand across sectors such as aerospace, building and construction, automotive, and oil and gas. This region demonstrates significant growth potential in terms of application development, product quality, and innovation, with market demand largely driven by aerogels’ superior insulation capabilities and low thermal conductivity.

In particular, the U.S. aerogel market is experiencing robust expansion, fueled by advances in material science and technology. Aerogels’ distinctive properties—such as low density and excellent thermal resistance—make them highly suitable for a variety of applications, including aerospace, construction, and automotive industries. The growing emphasis on energy-efficient building materials and insulation solutions is accelerating the adoption of aerogel products, as they outperform traditional alternatives in thermal performance.

The Asia Pacific aerogel market is also projected to witness substantial growth during the forecast period. As governments and industries in the region place increasing emphasis on sustainability, the demand for innovative, low-carbon materials is rising sharply. For example, manufacturers in Japan are increasingly incorporating aerogels into thermal insulation for products like refrigerators and HVAC systems. This transition towards sustainable manufacturing aligns with stricter environmental regulations and consumer preferences for eco-friendly products, further driving aerogel adoption.

COVID-19 Pandemic: Impact Analysis

Both public and private sectors experienced significant financial challenges during the outbreak. Widespread lockdowns and social distancing measures led to the closure of businesses in numerous countries, disrupting operations globally. The aerogel industry faced considerable difficulties, including labor shortages and reduced production capacity. Consequently, demand for silica aerogels declined, particularly in key sectors such as aerospace, oil and gas, and automotive, which experienced production slowdowns and shutdowns. Nevertheless, the aerogel market is projected to recover and exhibit growth in demand in the post-pandemic period.

Latest Trends/ Developments:

September 2024: Armacell completed the acquisition of all shares in Armacell JIOS Aerogels Limited, securing control over an annual powder production capacity exceeding 700 tonnes and strengthening its presence in the energy-sector insulation market.

September 2024: Armacell introduced the ArmaGel XG product line designed for high-temperature applications and announced the establishment of a new manufacturing facility in Pune, India, which will add 1 million square meters of blanket production capacity.

Key Players:

These are top 10 players in the Aerogel Market :-

Aspen Aerogel Inc.

Cabot Corporation

American Aerogel Corporation

Dow Corning Corporation

Svenska Aerogel AB

Airglass AB

BASF SE

JIOS Aerogel

Active Aerogels

Acoustiblok UK Ltd

Chapter 1. Global Aerogel Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Aerogel Market – Executive Summary

2.1. Market Size & Forecast – (2024 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Aerogel Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Aerogel Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Aerogel Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Aerogel Market – By Product

6.1. Introduction/Key Findings

6.2. Silica

6.3. Carbon

6.4. Polymers

6.5. Others

6.6. Y-O-Y Growth trend Analysis By Product

6.7. Absolute $ Opportunity Analysis By Product, 2024-2030

Chapter 7. Global Aerogel Market – By Technology

7.1. Introduction/Key Findings

7.2. Supercritical Drying

7.3. Other Drying

7.4. Y-O-Y Growth trend Analysis By Technology

7.5. Absolute $ Opportunity Analysis By Technology, 2024-2030

Chapter 8. Global Aerogel Market – By Form

8.1. Introduction/Key Findings

8.2. Blanket

8.3. Panel

8.4. Particle

8.5. Monolith

8.6. Y-O-Y Growth trend Analysis By Form

8.7. Absolute $ Opportunity Analysis By Form, 2024-2030

Chapter 9. Global Aerogel Market – By End-use

9.1. Introduction/Key Findings

9.2. Building & Construction

9.3. Aerospace & Marine

9.4. Automotive

9.5. Performance Coatings

9.6. Others

9.7. Y-O-Y Growth trend Analysis By End-use

9.8. Absolute $ Opportunity Analysis By End-use, 2024-2030

Chapter 10. Global Aerogel Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Product

10.1.3. By Technology

10.1.4. By Form

10.1.5. By End-use

10.1.6. Countries & Segments – Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product

10.2.3. By Technology

10.2.4. By Form

10.2.5. By End-use

10.2.6. Countries & Segments – Market Attractiveness Analysis

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Product

10.3.3. By Technology

10.3.4. By Form

10.3.5. By End-use

10.3.6. Countries & Segments – Market Attractiveness Analysis

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Product

10.4.3. By Technology

10.4.4. By Form

10.4.5. By End-use

10.4.6. Countries & Segments – Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Product

10.5.3. By Technology

10.5.4. By Form

10.5.5. By End-use

10.5.6. Countries & Segments – Market Attractiveness Analysis

Chapter 11. Global Aerogel Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Aspen Aerogel Inc.

11.2. Cabot Corporation

11.3. American Aerogel Corporation

11.4. Dow Corning Corporation

11.5. Svenska Aerogel AB

11.6. Airglass AB

11.7. BASF SE

11.8. JIOS Aerogel

11.9. Active Aerogels

11.10. Acoustiblok UK Ltd

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The aerospace and defense industries constitute a significant segment of the aerogel market, driven by the demand for lightweight materials capable of withstanding extreme temperatures and harsh conditions.

The top players operating in the Aerogel Market are - Aspen Aerogel Inc., Cabot Corporation and American Aerogel Corporation.

Both public and private sectors experienced significant financial challenges during the outbreak.

The construction industry represents a key opportunity, particularly for advanced insulation applications.

Asia Pacific is the fastest-growing region in the Aerogel Market.