Global Secure Access Service Edge Market Research Report – Segmentation By Offering (Platform, Services), By Deployment Mode (On-premises, Cloud, Hybrid), By Organization Size (Large Enterprises, SMEs), By Distribution Channel (Direct Sales, Distributors, Online Retail), By Region – Forecast (2025 – 2030)

Published: 2025 - July

Report Code: IM-16613

Format:

Region: Global

Market Size and Overview:

The Global Secure Access Service Edge Market was valued at USD 12.94 billion in 2024 and is projected to reach a market size of USD 28.01 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 20.29%.

Combining network‑security features, such as Secure Web Gateway (SWG), Cloud Access Security Broker (CASB), Zero‑Trust Network Access (ZTNA), and Firewall‑as‑a‑Service (FWaaS), with SD‑WAN capabilities into a single, cloud‑native service. This integration helps businesses to impose uniform policies, minimize latency, and simplify infrastructure by resolving the security and connectivity issues presented by hybrid workforces, cloud migrations, and edge computing.

Key Market Insights:

Driven by license subscriptions to integrated security‑network stacks, SASE Platforms hold around 60% of 2024 revenues; Professional and Managed Services are the fastest-growing, with a CAGR of around 35% as businesses want professional deployment, customization, and ongoing operations assistance.

Accounting for around 22% of SASE spending, the IT and Telecom vertical uses SASE to protect dispersed branch locations and data centers during 5G rollouts; BFSI follows closely at roughly 18%, where compliance and low-latency are most important.

Hybrid SASE captures roughly 30% of deployments in 2024 and is expanding at around 28% CAGR, therefore balancing data-sovereignty needs with international edge-footprint demands by combining on-premises SDP gateways with cloud PoPs.

Early SASE adopters are mostly huge corporations (around 70%), but SMEs are the fastest expanding consumer segment with an approximate CAGR of 32% drawn by OPEX‑friendly, subscription-based security and simplified network management via online channels.

Secure Access Service Edge Market Drivers:

The security needs of the hybrid workforce are driving the demand for this market.

As remote and hybrid working styles gain acceptance, conventional hub-and-spoke VPN systems fall under the load of scattered traffic. According to a FlexJobs study, 65% of knowledge workers now look for full-time remote jobs post-pandemic; companies say 30 to 40% of their personnel work from home or edge locations. These changes cause latency, erratic security postures, and user-experience gaps when all traffic backhauls to central data centers. By strategically installing security service nodes, ZTNA, SWG, CASB, and FWaaS, across worldwide dispersed PoPs, SASE brings inspection and policy enforcement within a few hops of the end user, hence addressing these problems. Clients on corporate, home, and roaming devices claim up to 50% decrease in application‑access latency and smooth, uniform policy application. Driven by the necessity of continuous security and performance under hybrid‑work permanency, SASE's dispersed design has become a strategic priority for businesses all around.

The growing use of cloud migration and multi-cloud complexity is driving the growth of this market.

By 2025, 85% of companies will have embraced a cloud-first approach, viewing any on-premises legacy system as either "secondary" or "legacy". The resulting paradigm change has caused 80 to 90 percent of business-critical applications to be running in several public or private clouds, therefore producing a complicated network of egress fees, security blind spots, and connection bottlenecks. SASE platforms naturally interface with major cloud‑provider backbone networks (Azure WAN, AWS Transit Gateway, Google Cloud Interconnect), hence allowing policy‑driven, encrypted connection that bypasses conventional backhaul to central firewalls. By localizing inspection and maximizing routing, businesses using SASE have reported up to 30% savings on cloud-egress charges while also implementing DDoS protection and workload-level microsegmentation without compromising cloud-native performance.

The recent convergence of networking with security is said to be a major market driver.

Traditionally, businesses bought SD‑WAN and security appliances, firewalls, SWGs, CASBs, independently, leading to management silos, erratic policies, and more TCO. Driven by fewer point products, simplified orchestration, and automated policy provisioning, converging networking and security under a unified SASE control plane reduces total-cost-of-ownership by 20–25%, according to a Data Bridge Market Research analysis. One pane of glass for network-and-security policies allows IT teams to set intent-based rules that automatically apply over all edges and clouds on SASE platforms. This integration removes manual rule‑syncing errors, lowers deployment time by 40%, and reduces operational costs related to patching and compatibility testing of different devices. SASA's converged approach has become the favored architecture for resilient, cost-effective business networking as digital transformation picks up pace.

The growing adoption of zero-trust is proving to be an important market driver.

With 75% of businesses starting Zero Trust roadmaps by 2024, according to Gartner projections, Zero Trust ideas, "never trust, always verify," have gone from specialized to commonplace. Conventional VPNs give general network access and are not well suited for least-privilege enforcement, hence leaving lateral-movement routes open after initial authentication. At their heart, SASE systems incorporate ZTNA; therefore, access to particular applications that is microsegmented and ongoing, context-aware multi-factor authentication is needed for every session. Early SASE implementations have recorded a 40% drop in unauthorized-access incidents and a 35% decrease in internal-threat escalations inside the first year by doing away with implicit trust zones and implementing detailed access policies at the edge. Companies are increasingly using SASEs' built-in Zero Trust features to protect hybrid-cloud settings and mobile workforces as regulatory and cyberthreat landscapes grow.

Secure Access Service Edge Market Restraints and Challenges:

The most challenging thing for this market is to integrate with the existing systems, which is complex.

This schedule highlights the need to review current network topologies, modify routing strategies, and confirm compatibility with old QoS and VPN settings. Organizations often run hybrid architectures during this change, keeping MPLS circuits next to SD‑WAN overlays, therefore doubling operational complexity and postponing complete SASE advantages. Furthermore, hardware refresh cycles for branch routers and security devices must be synchronized with software deployments, therefore increasing project‑management overhead and purchase lead times. Firms without a phased migration plan, piloting tiny branch clusters before widespread enterprise deployment, run the danger of drawn-out ROI realization and interruption to essential business services.

The challenge of variability in the performance is said to hamper the overall growth of the market.

Many SASE services depend on shared cloud PoPs, but peak use can overwhelm them, therefore affecting throughput for latency‑sensitive applications like big‑file transfers and video conferencing. According to customer surveys, user experience might deteriorate with performance dips above 100 ms jitter and 5% loss, therefore causing ISPs to renegotiate SLAs with providers. SASE providers must intelligently route across many ISPs and strategically grow PoP density to satisfy corporate demands, often with sub-50-ms end-to-end latency for essential services. Some companies solve these problems by using hybrid deployments that integrate on‑premises security gateways with cloud PoPs to reduce latency-sensitive inspection. Still, performance instability remains a top-three consideration among early SASE adopters, therefore leading investments in network-performance monitoring and dynamic traffic-steering capabilities to sustain constant user-experience SLAs.

The concerns regarding vendor lock-in are said to be one of the major market challenges.

SASE's attraction of a single security‑network stack carries the danger of vendor lock‑in: once businesses use a single provider's integrated suite, covering SWG, CASB, FWaaS, ZTNA, and SD‑WAN, they could have trouble interfacing with third‑party tools or shifting to other platforms without major rearchitecture. Custom security rules, identity-provider integrations, and reporting procedures are exclusive due to the lack of open APIs and uniform policy models. Leaving such settings can call for total policy rewrites, SIP‑trunk reconfigurations, and security staff retraining, therefore discouraging multivendor initiatives. Some companies bargain for hybrid-vendor roadmaps and demand contract portability clauses to lessen lock-in. Still, lock-in is a cautionary tale that slows uptake among risk-averse customers since real multi-vendor SASE ecosystems are still developing.

The existence of a skill gap, particularly in the department of security operations, is said to undermine the performance of this market.

Implementing and controlling SASE calls for a convergence of skills in cloud networking, identity management, and security orchestration, areas where good talent is scarce. According to a recent survey, 47% of companies claim a lack of in‑house knowledge as a hindrance to SASE deployment; by 2025, worldwide cybersecurity job openings are expected to reach 3.5 million, according to CyberSecurity Ventures data. Companies risk misconfigurations, such as incorrect ZTNA policies or insufficient SWG inspection guidelines, that can cause security gaps or performance bottlenecks without committed SASE architects. Many businesses, therefore, depend on costly professional-services contracts or MSSP alliances, which may raise project prices by 20–30% and lengthen time-to-value. But bridging the skills gap is still a major operational difficulty for SASE maturity; as such, companies are investing in SASE-specific training programs, vendor certifications, and cross-functional "security-network" centers of excellence.

Secure Access Service Edge Market Opportunities:

The latest expansion seen in Edge PoP is said to be the most important market opportunity.

To provide low‑latency security and networking near consumers, SASE providers are fiercely expanding their worldwide Point-of-Presence (PoP). With plans to surpass 150 cities by 2026, slashing round-trip latency by up to 40 ms for remote branches, Palo Alto Networks' Prisma Access presently lists more than 90 PoP locations throughout North America, Europe, Asia Pacific, and Latin America. Cato Networks' Cloud PoP network spans 75 sites and adds new nodes quarterly, while Zscaler runs over 180 PoPs all across. This density enables businesses to send traffic to the nearest PoP for inspection, thereby lowering dependence on central firewalls and eliminating backhaul. Fast PoP growth is creating new markets in underprivileged areas like Latin America and Africa. At 24. 7% CAGR and 23% CAGR, respectively, IMARC identifies APAC and LATAM as the fastest-growing areas for SASE investments. To satisfy different company demands, providers distinguish on regional performance SLAs, compliance‑zone coverage, and integration with local cloud‑provider backbones as PoP footprints grow.

The emergence of AI-driven threat detection technology is said to be another market opportunity that would help the market improve.

Including machine-learning-based analysis into SASE systems is improving real-time threat detection and speeding incident response. To baseline typical network patterns and flag anomalies, early trials show 30% faster detection of zero-day exploits than legacy SIEM/SOAR installations. Check Point's CloudGuard SASE employs behavioural analytics engines (UEBA). By integrating AI-driven threat hunting throughout its Internet-Access and Private-Access services, Zscaler's new alliance with Vectra AI lowers false-positive rates by 25% and allows security teams to triage alerts 50% more swiftly. These artificial intelligence models operate at both edge PoPs and central analysis nodes, hence harmonizing low-latency inference, essential for blocking live assaults, with more thorough cloud-based forensic research. AI-driven SASE is now a major differentiating factor as cyber‑threat complexity rises, allowing constant adaptation to new malware, encrypted‑traffic exploits, and insider‑threat scenarios.

The chance of integrating with 5 G MEC is seen as a big opportunity for the market.

Ultra‑low‑latency secure connectivity for Industry 4.0, AR/VR, and V2X applications is being released by the convergence of SASE with 5G MEC (Multi‑Access Edge Computing). According to Versa Networks, co‑locating SASE PoPs on private 5 G MEC infrastructure can achieve sub‑10 ms end‑to‑end latency, essential for real‑time robotics control and immersive AR training in manufacturing. Ericsson's private 5 G tests show that integrating SASE security capabilities at the MEC layer forces uniform policies throughout cellular and wired networks, hence removing the need for standalone VPN gateways and lowering session‑setup time by 60%. Automotive assembly lines in Germany and Japan are testing these integrated arrangements to capture telemetry feeds from AGVs and cobots; telecom companies bundle SASE+MEC services to set their enterprise‑5G offerings apart. New vertical-specific applications and premium managed-services revenue sources will be driven by SASE‑MEC integrations as 5G adoption increases.

The buildup of a partnership ecosystem is said to give this market an opportunity to cover more area.

To provide turnkey, managed solutions especially for SMEs lacking in‑house expertise, SASE providers are developing rich partner ecosystems with SI and MSP channels. With top SD-WAN providers (Arista, Versa, Cradlepoint) and security vendors (Palo Alto, Zscaler), Microsoft's Secure Access Service Edge partner program enables co-managed service bundles and joint go-to-market solutions. To offer end-to-end connectivity and security orchestration backed by regional NOC/SOC support, Orange Business highlights its SASE Partner Ecosystem, including technology partnerships with Fortinet, Check Point, and Cisco. These relationships allow MSPs to white-label SASE solutions, provide OPEX-friendly subscription plans, and 24/7 managed-service SLAs that meet the needs of mid-market consumers. Strong channel ecosystems will be essential to scaling adoption, expanding global reach, and providing focused vertical solutions as the SASE market develops.

Secure Access Service Edge Market Segmentation:

Market Segmentation: By Offering

• Platform

• Services

The Platform segment is said to dominate the market with a market share of 60%. This is due to enterprises favouring a unified SD-WAN plus security bundle for the purpose of ease of procurement and seamless policy orchestration. The Services segment is said to be the fastest-growing segment. It is growing at a CAGR of 35%, which is due to the complexity that exists in the deployment of SASE. This makes the organization outsource operations, implementation, and design.

Market Segmentation: By Deployment Mode

• On-premises

• Cloud

• Hybrid

The On-premises segment is said to dominate this market, where SD‑WAN and security gateways are located inside client data centers, accounting for around 70% of installs, preferred by regulated businesses needing stringent data sovereignty and immediate traffic inspection. The Hybrid segment is said to be the fastest-growing segment. Combining on‑prem gateways with cloud PoPs, hybrid SASE installations are growing at roughly 28% CAGR as businesses balance sovereignty with the need for global edge presence and low-latency access for distant users. When it comes to the Cloud-based segment, pure cloud‑native SASE is attracting attention for green‑field and completely cloud‑based businesses wanting quick, no‑hardware security deployments, even though its market share remains small (about 10%).

Market Segmentation: By Organization Size

• Large Enterprises

• SMEs

The Large Enterprises segment is said to dominate this market. Driven by their sophisticated, multi-region network architectures and great demand for integrated network-and-security solutions throughout thousands of locations, large corporations account for approximately 70% of SASE expenditure. The SMEs segment is considered the fastest-growing one. SMEs projected with roughly 32% CAGR, draw subscription-based SASE that substitutes expensive MPLS and segregated firewalls with scalable, OPEX-friendly security models available through online channels.

Market Segmentation: By Distribution Channel

• Direct Sales

• Distributors

• Online Retail

The Direct Sales segment is said to lead this market. Direct OEM and large‑account sales account for roughly 55% of income as major companies obtain SASE systems via already established vendor relationships featuring customized SLAs and integration services. The Online Retail segment is the fastest-growing. Catering to tiny teams and SMBs needing fast deployment with little professional‑services engagement, self‑service, SaaS-only SASE solutions marketed through online platforms are expanding at roughly 20% CAGR. When it comes to the Distributors segment of the market, around 30% of market share belongs to value-added distributors, who provide regional clients mid-market support, financing, and integration.

Market Segmentation: By Region

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

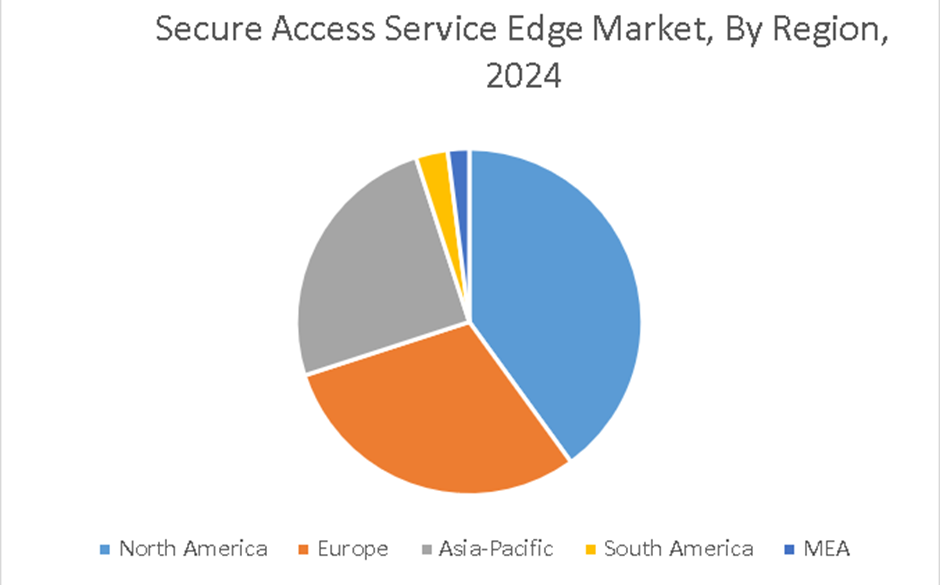

North America has emerged as the leader of this market. Led by early cloud adoption, distributed branch networks, and large corporate budgets for cybersecurity, North America holds about 40% market share. The Asia-Pacific region is considered to be the fastest-growing segment. Driven by digital transformation projects, fast cloud penetration, and hybrid-work policies in China, India, and Southeast Asia, APAC is the fastest-growing area with roughly 25% CAGR.

Europe, on the other hand, is said to hold a market share of 30%. Due to GDR-driven security modernization, the rollout of SDA in the banking and manufacturing sectors is expected. Both the MEA and South America are said to represent a market share of around 5% share overall; rising SASE acceptance in the government and telecom industries is driven by MSP alliances and infrastructure improvement initiatives.

COVID-19 Impact Analysis on the Global Secure Access Service Edge Market:

The COVID-19 pandemic is said to have a major impact on this market. But as companies looked for scalable, cloud‑native security strategies, the move to remote work hastened SASE pilot initiatives in 2021. Rising cybersecurity expenditures and stimulus-backed digital infrastructure initiatives helped SASE agreements bounce back by 25% in 2022, thus establishing SASE as a fundamental design for hybrid offices.

Latest Trends/ Developments:

Large vendors (Cisco, Palo Alto) are buying specialized start-ups (e.g., CloudKnox, Expanse) to expand SASE offerings and include sophisticated threat-intel features.

Supporting air‑gapped and low‑latency demands, new hardware devices are integrating SASE and ZTNA capabilities at the branch or campus edge.

To integrate network-and-endpoint telemetry for all-encompassing threat hunting, vendors are incorporating extended detection and response (XDR) into SASE suites.

Introduction of consumption-based SASE billing, per‑GB or per‑session pricing, facilitates cost optimization for seasonal or bursty workloads.

Key Players:

• Cisco Systems, Inc.

• Paolo Alto Networks, Inc.

• Fortinet, Inc.

• VMware, Inc.

• Zscaler, Inc.

• Netskope, Inc.

• Cloudflare, Inc.

• Cato Networks Ltd.

• Akamai Technologies, Inc.

• Check Point Software Technologies, Inc.

Chapter 1. Global Secure Access Service Edge Market–Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Secure Access Service Edge Market– Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Secure Access Service Edge Market– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Secure Access Service Edge Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Secure Access Service Edge Market- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Secure Access Service Edge Market- By Offering

6.1. Introduction/Key Findings

6.2. Platform

6.3. Services

6.4. Y-O-Y Growth trend Analysis By Offering

6.5. Absolute $ Opportunity Analysis By Offering, 2025-2030

Chapter 7. Global Secure Access Service Edge Market– By Deployment Mode

7.1 Introduction/Key Findings

7.2. On-premises

7.3. Cloud

7.4. Hybrid

7.5. Y-O-Y Growth trend Analysis By Deployment Mode

7.6. Absolute $ Opportunity Analysis By Deployment Mode, 2025-2030

Chapter 8. Global Secure Access Service Edge Market– By Organization Size

8.1. Introduction/Key Findings

8.2. Large Enterprises

8.3. SMEs

8.4. Y-O-Y Growth trend Analysis By Organization Size

8.5. Absolute $ Opportunity Analysis By Organization Size, 2025-2030

Chapter 9. Global Secure Access Service Edge Market– By Distribution Channel

9.1. Introduction/Key Findings

9.2. Direct Sales

9.3. Distributors

9.4. Online Retail

9.5. Y-O-Y Growth trend Analysis By Distribution Channel

9.6. Absolute $ Opportunity Analysis By Distribution Channel, 2025-2030

Chapter 10. Global Secure Access Service Edge Market, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Offering

10.1.3. By Deployment Mode

10.1.4. By Organization Size

10.1.5. By Distribution Channel

10.1.6. By Region

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Offering

10.2.3. By Deployment Mode

10.2.4. By Organization Size

10.2.5. By Distribution Channel

10.2.5. By Region

10.3. Asia Pacific

10.3.1. By Country

10.3.1.1. China

10.3.1.2. Japan

10.3.1.3. South Korea

10.3.1.4. India

10.3.1.5. Australia & New Zealand

10.3.1.6. Rest of Asia-Pacific

10.3.2. By Offering

10.3.3. By Deployment Mode

10.3.4. By Organization Size

10.3.5. By Distribution Channel

10.3.6. By Region

10.4. South America

10.4.1. By Country

10.4.1.1. Brazil

10.4.1.2. Argentina

10.4.1.3. Colombia

10.4.1.4. Chile

10.4.1.5. Rest of South America

10.4.2. By Offering

10.4.3. By Deployment Mode

10.4.4. By Organization Size

10.4.5. By Distribution Channel

10.4.6. By Region

10.5. Middle East & Africa

10.5.1. By Country

10.5.1.1. United Arab Emirates (UAE)

10.5.1.2. Saudi Arabia

10.5.1.3. Qatar

10.5.1.4. Israel

10.5.1.5. South Africa

10.5.1.6. Nigeria

10.5.1.7. Kenya

10.5.1.8. Egypt

10.5.1.9. Rest of MEA

10.5.2. By Offering

10.5.3. By Deployment Mode

10.5.4. By Organization Size

10.5.5. By Distribution Channel

10.5.6. By Region

Chapter 11. Global Secure Access Service Edge Market– Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

11.1. Cisco Systems, Inc.

11.2. Paolo Alto Networks, Inc.

11.3. Fortinet, Inc.

11.4. VMware, Inc.

11.5. Zscaler, Inc.

11.6. Netskope, Inc.

11.7. Cloudflare, Inc.

11.8. Cato Networks Ltd.

11.9. Akamai Technologies, Inc.

11.10. Check Point Software Technologies, Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Secure Access Service Edge Market was valued at USD 12.94 billion in 2024 and is projected to reach a market size of USD 28.01 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 20.29%.

Driven by bundled integrated SD‑WAN and security, the SASE Platform subscriptions segment is said to lead the market with around 60% market share.

The hybrid SASE installations segment is said to be the fastest-growing segment as it grew at around 28% CAGR, reconciling data-sovereignty demands with cloud‑edge agility.

Remote work security calls for quick SASE pilot projects in 2021, which then result in a 25% recovery in SASE agreements by 2022, following the first pandemic-related delays.

Driven by cloud penetration, hybrid-work rules, and digital-infrastructure investments, Asia Pacific is the fastest-growing area at almost 30% CAGR.