Global Satellite Internet Market Research Report – Segmentation by Frequency Band (L-band, C-band, K-band, X-band); By Industry (Energy & Utility, Government & Public Sector, Transport & Cargo, Maritime, Military, Corporate/Enterprises, Media & Broadcasting, Other); Region – Forecast (2025 – 2030)

Published: 2025 - July

Report Code: IM-16614

Format:

Region: Global

Market Size and Overview:

The Global Satellite Internet Market was valued at USD 10.4 billion in 2024 and is projected to reach a market size of USD 22.51 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.7%.

The Satellite Internet market is rapidly transforming global connectivity by delivering high-speed internet access to remote, underserved, and rural areas where traditional broadband infrastructure is limited or nonexistent. Powered by advancements in satellite technology—particularly low Earth orbit (LEO) satellite constellations—this market is reshaping digital inclusion and enabling seamless access to education, healthcare, e-commerce, and communication services worldwide. Satellite internet offers a scalable, resilient, and reliable alternative to ground-based networks, especially in disaster-prone regions and during emergencies. As global need for real-time connectivity and data-intensive applications surges, satellite internet is becoming an essential component of the next-generation communication ecosystem, supporting economic growth and bridging the digital divide.

Key Market Insights:

Over 45% of rural households worldwide still lack access to stable broadband connectivity, which has positioned satellite internet as a critical solution to bridging the digital divide. With the surge of remote work, online education, and digital public services, demand for reliable internet access in non-urban areas has surged. Satellite internet providers are expanding coverage aggressively, with recent launches adding thousands of new users monthly in remote locations across Asia, Africa, and Latin America.

More than 3,500 low Earth orbit (LEO) satellites have been deployed over the past few years to support high-speed, low-latency satellite internet services. This marks a shift from traditional geostationary satellites, offering improved performance and faster data transmission. Companies operating these LEO constellations are now providing latency as low as 25–35 milliseconds, making satellite internet increasingly competitive with fiber and cable broadband options, particularly in rural and mobile settings.

Approximately 70% of new satellite broadband users are first-time internet users, especially in regions where terrestrial networks have never reached. This influx is contributing to growing digital literacy, financial inclusion through mobile banking, and access to critical services like telemedicine. As user demand grows, satellite internet providers are forming partnerships with governments and telecom operators to support public Wi-Fi projects and subsidized access programs, accelerating the pace of digital inclusion worldwide.

Satellite Internet Market Drivers:

Rising Demand for Rural and Remote Connectivity Is Driving Rapid Expansion of Satellite Internet Infrastructure Across the Globe

One of the primary forces propelling the satellite internet market forward is the urgent and widespread need for reliable internet access in rural, remote, and geographically challenging regions. In many parts of the world, especially across developing countries and island nations, terrestrial broadband infrastructure like fiber optics or cable networks is either unavailable or economically unfeasible to deploy. Satellite internet eliminates the need for ground-based infrastructure, providing instant coverage over wide geographic areas from space. This capability is helping governments and private companies bridge the digital divide by enabling services such as remote education, telemedicine, e-commerce, and financial inclusion. The ability to connect underserved populations directly contributes to social and economic development, making satellite broadband a vital tool in the global effort toward digital equity.

Technological Advancements in Satellite Design, Launch Systems, and Low Earth Orbit (LEO) Constellations Are Fueling Performance and Accessibility Improvements

Breakthroughs in satellite technology—particularly the shift from traditional geostationary satellites to low Earth orbit constellations—have dramatically improved the speed, latency, and reliability of satellite internet services. These LEO satellites orbit closer to Earth, which significantly reduces latency and enables broadband speeds that are competitive with fiber-optic networks. In addition, modern satellite design has become more compact, cost-effective, and energy-efficient, while reusable rocket technology has lowered launch costs. These advances are not only enhancing service quality but also making satellite internet more commercially viable on a global scale. As deployment becomes faster and cheaper, both established tech giants and new market entrants are investing in large-scale LEO networks, making high-speed satellite internet more accessible than ever before.

Government Initiatives and Public-Private Partnerships Are Strengthening the Adoption of Satellite Internet in Underserved Markets

Many national governments are prioritizing satellite internet in their digital transformation agendas, especially in rural development and disaster recovery programs. Initiatives such as public Wi-Fi rollouts, smart village projects, and emergency communication frameworks increasingly rely on satellite connectivity for fast, scalable deployment. Additionally, public-private partnerships are playing a crucial role in building and maintaining satellite internet infrastructure, with telecom operators, space agencies, and satellite service providers joining forces to address funding gaps and accelerate implementation. These collaborations often include subsidies, shared access programs, and strategic investments to ensure satellite broadband can be delivered at affordable rates. With strong policy support and international cooperation, satellite internet is gaining traction as a reliable tool to achieve universal digital access.

The Growing Dependence on Cloud-Based Services, Real-Time Communication, and IoT Solutions Is Creating Sustained Demand for Continuous, High-Speed Connectivity

Modern life is increasingly dependent on uninterrupted internet access for everything from video conferencing and cloud computing to smart agriculture and industrial IoT. Satellite internet plays a pivotal role in providing consistent broadband connectivity in areas prone to natural disasters, network outages, or where 5G expansion is not yet viable. As industries digitize and automate, businesses in sectors like energy, mining, transportation, and logistics are integrating satellite broadband into their operations to ensure connectivity continuity in off-grid environments. Additionally, the global push for real-time data transfer and smart city infrastructure requires a reliable, omnipresent internet backbone—something satellite networks can uniquely provide.

Satellite Internet Market Restraints and Challenges:

High Deployment Costs, Signal Latency in Some Regions, and Regulatory Barriers Remain Key Restraints for the Satellite Internet Market

Despite its transformative potential, the satellite internet market faces several significant challenges that hinder widespread adoption. One major obstacle is the high initial investment required for launching satellite constellations, building ground infrastructure, and developing compatible user terminals—costs that can be prohibitive for startups or deployment in low-income regions. While low Earth orbit (LEO) satellites have reduced latency, signal delays and service interruptions can still occur in extreme weather or heavily obstructed environments, affecting user experience. Moreover, regulatory complexities, such as spectrum licensing, cross-border frequency coordination, and national security concerns, often delay service rollout and limit market access in certain regions. Combined, these factors create operational, technical, and financial hurdles that must be addressed to ensure long-term growth and equitable access to satellite internet services worldwide.

Satellite Internet Market Opportunities:

The satellite internet market presents vast opportunities, particularly in connecting the 3+ billion people worldwide who still lack reliable internet access. As demand for digital inclusion grows across rural and remote regions, satellite internet can offer rapid, cost-effective deployment without the need for extensive ground infrastructure. Emerging applications in smart agriculture, autonomous vehicles, disaster management, and offshore operations are also creating new demand for constant, high-speed connectivity in areas beyond the reach of traditional networks. Moreover, the rise of hybrid communication systems that integrate satellite and 5G technologies is opening doors for seamless connectivity in urban and remote areas alike. With government backing, international collaborations, and falling launch costs, satellite internet is poised to become a major driver of global connectivity and next-generation digital infrastructure.

Satellite Internet Market Segmentation:

Market Segmentation: By Frequency Band:

• L-band

• C-band

• K-band

• X-band

Among the various frequency bands used in the satellite internet market, the K-band (including Ka-band and Ku-band) holds the dominant position due to its ability to support high-capacity, high-speed broadband communication. This band offers greater bandwidth, making it suitable for delivering faster data rates and supporting bandwidth-heavy applications like video streaming, cloud computing, and real-time communication. It is widely adopted for both commercial and governmental uses, particularly in low Earth orbit (LEO) satellite constellations where latency and data throughput are critical. Many satellite internet providers have standardized their services around the K-band to meet the growing expectations of users for seamless, high-performance internet access, especially in remote and underserved areas.

The X-band, while traditionally reserved for military and government applications, is now emerging as the fastest-growing frequency band in specialized satellite internet deployments. It offers strong resistance to weather interference and signal degradation, making it ideal for defense communication, emergency response, and mission-critical applications in harsh environments. With governments and defense agencies around the world modernizing their communication systems, need for secure and reliable internet via X-band satellites is increasing steadily. Additionally, private-sector interest is rising in using X-band for remote infrastructure monitoring and secure industrial operations, leading to new commercial applications beyond traditional defense use.

Market Segmentation: By Industry:

• Energy & Utility

• Government & Public Sector

• Transport & Cargo

• Maritime

• Military

• Corporate /Enterprises

• Media & Broadcasting

• Others

In the satellite internet market, the Government & Public Sector holds the dominant position because of its widespread use in public safety, disaster response, rural connectivity programs, and defense-related communication networks. Governments around the world are leveraging satellite internet to bridge the urban-rural digital divide, enhance emergency communication frameworks, and enable connectivity in remote or underserved regions. Public agencies also depend on satellite services for secure communication during natural disasters or conflict situations when terrestrial networks are compromised. Additionally, numerous national-level initiatives and smart governance programs include satellite broadband as a critical component of digital infrastructure, ensuring reliable, uninterrupted service for public service delivery and administrative operations.

The Maritime industry is emerging as the fastest-growing segment, driven by the increasing need for real-time connectivity aboard ships, cargo vessels, and offshore platforms. Satellite internet provides a vital communication backbone for navigation, monitoring, crew welfare, and logistics operations in open waters where conventional networks are non-existent. As shipping companies digitize operations and adopt smart fleet management systems, high-speed, low-latency satellite broadband is becoming a necessity rather than a luxury. Moreover, regulatory requirements for vessel tracking, safety compliance, and data reporting are pushing maritime operators to invest in reliable satellite-based connectivity solutions, making this segment one of the most dynamic growth areas in the satellite internet ecosystem.

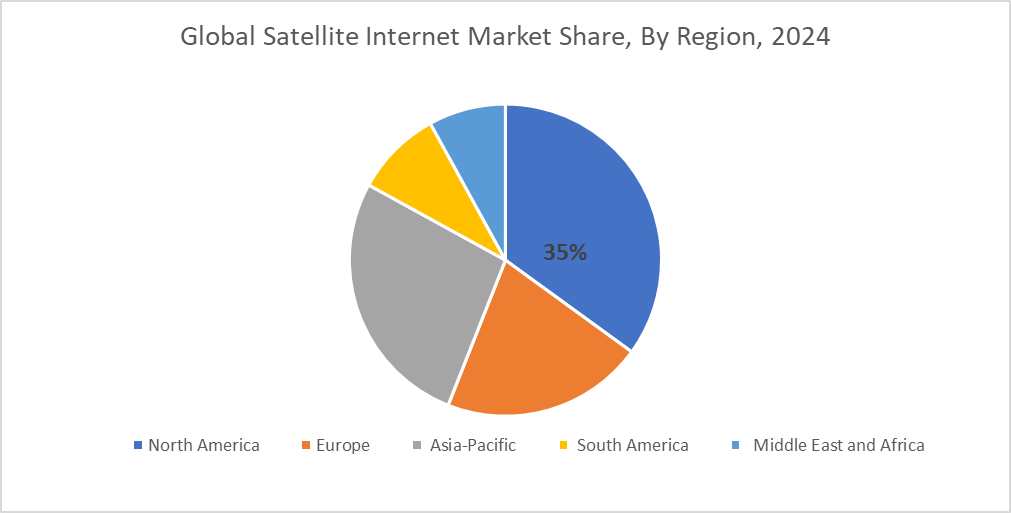

Market Segmentation: Regional Analysis:

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

In the satellite internet market, North America holds the dominant position with approximately 35% contribution, driven by early technology adoption, strong infrastructure, and significant investments from leading private players. The region is home to several major satellite internet providers, including pioneers of low Earth orbit (LEO) constellations, who have been instrumental in accelerating commercial deployment. Widespread demand for high-speed broadband in rural and underserved regions of the U.S. and Canada, combined with strong government support through programs like rural digital inclusion and emergency response systems, has helped solidify North America’s leadership in this sector.

Asia-Pacific is the fastest-growing region in the satellite internet market, accounting for 27% of the global contribution and rising steadily. Rapid urbanization, vast rural populations, and growing demand for internet access across remote and mountainous regions have created a fertile ground for satellite broadband expansion. Countries such as India, China, Japan, and Australia are investing heavily in satellite-based digital infrastructure to support education, healthcare, agriculture, and government services in hard-to-reach areas. Additionally, rising smartphone penetration and digital transformation initiatives by public and private sectors are boosting the need for uninterrupted connectivity. As more regional players and international providers enter the market, Asia-Pacific is expected to lead future growth in both adoption rates and satellite launches.

COVID-19 Impact Analysis on the Global Satellite Internet Market:

The COVID-19 pandemic significantly accelerated the demand for satellite internet as lockdowns and remote work highlighted the critical need for reliable connectivity in underserved and rural regions. With many traditional broadband networks overwhelmed or unavailable in remote areas, satellite internet emerged as a crucial solution for enabling remote education, telemedicine, virtual collaboration, and access to essential online services. The crisis also spurred governments and organizations to fast-track digital inclusion initiatives, increasing investments in satellite infrastructure.

Latest Trends/ Developments:

One of the most notable trends in the satellite internet market is the rapid deployment of low Earth orbit (LEO) satellite constellations designed to deliver high-speed, low-latency broadband across the globe. These LEO satellites orbit closer to Earth than traditional geostationary satellites, reducing signal delay and allowing for faster, more responsive internet service. Companies are now launching hundreds, even thousands, of satellites to create expansive networks capable of supporting real-time communication, cloud access, and video streaming even in the most remote corners of the world.

Another emerging development is the integration of hybrid connectivity solutions, where satellite internet is combined with terrestrial networks like fiber or cellular for enhanced reliability and coverage. This approach is gaining traction in industries such as logistics, energy, agriculture, and aviation, where constant connectivity is critical. Meanwhile, innovations in satellite ground terminals are making user equipment smaller, smarter, and more affordable—paving the way for wider residential and commercial adoption. Additionally, there’s a rising focus on sustainable satellite technology, including electric propulsion systems and debris mitigation, which is shaping the future of satellite internet with a focus on both performance and environmental responsibility.

Key Players:

• SpaceX (Starlink)

• OneWeb

• Amazon (Project Kuiper)

• Telesat

• Viasat

• Hughes Network Systems

• Eutelsat

• SES S.A.

• Iridium Communications

• Inmarsat

Chapter 1. Global Satellite Internet Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Global Satellite Internet Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. Global Satellite Internet Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. Global Satellite Internet Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. Global Satellite Internet Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. Global Satellite Internet Market – By Frequency Band

6.1. Introduction/Key Findings

6.2. L-band

6.3. C-band

6.5. K-band

6.6. X-band

6.&. Y-O-Y Growth trend Analysis By Frequency Band

6.8. Absolute $ Opportunity Analysis By Frequency Band, 2025-2030

Chapter 7. Global Satellite Internet Market – By Industry

7.1. Introduction/Key Findings

7.2. Energy & Utility

7.3. Government & Public Sector

7.4. Transport & Cargo

7.5. Maritime

7.6. Military

7.7. Corporate/Enterprises

7.8. Media & Broadcasting

7.9. Other

7.10. Y-O-Y Growth trend Analysis By Industry

7.11. Absolute $ Opportunity Analysis By Industry, 2025-2030

Chapter 8. Global Satellite Internet Market, By Geography – Market Size, Forecast, Trends & Insights

8.1. North America

8.1.1. By Country

8.1.1.1. U.S.A.

8.1.1.2. Canada

8.1.1.3. Mexico

8.1.2. By Frequency Band

8.1.3. By Industry

8.1.4. Countries & Segments – Market Attractiveness Analysis

8.2. Europe

8.2.1. By Country

8.2.1.1. U.K.

8.2.1.2. Germany

8.2.1.3. France

8.2.1.4. Italy

8.2.1.5. Spain

8.2.1.6. Rest of Europe

8.2.2. By Frequency Band

8.2.3. By Industry

8.2.4. Countries & Segments – Market Attractiveness Analysis

8.3. Asia Pacific

8.3.1. By Country

8.3.1.1. China

8.3.1.2. Japan

8.3.1.3. South Korea

8.3.1.4. India

8.3.1.5. Australia & New Zealand

8.3.1.6. Rest of Asia-Pacific

8.3.2. By Frequency Band

8.3.3. By Industry

8.3.4. Countries & Segments – Market Attractiveness Analysis

8.4. South America

8.4.1. By Country

8.4.1.1. Brazil

8.4.1.2. Argentina

8.4.1.3. Colombia

8.4.1.4. Chile

8.4.1.5. Rest of South America

8.4.2. By Frequency Band

8.4.3. By Industry

8.4.4. Countries & Segments – Market Attractiveness Analysis

8.5. Middle East & Africa

8.5.1. By Country

8.5.1.1. United Arab Emirates (UAE)

8.5.1.2. Saudi Arabia

8.5.1.3. Qatar

8.5.1.4. Israel

8.5.1.5. South Africa

8.5.1.6. Nigeria

8.5.1.7. Kenya

8.5.1.8. Egypt

8.5.1.9. Rest of MEA

8.5.2. By Frequency Band

8.5.3. By Industry

8.5.4. Countries & Segments – Market Attractiveness Analysis

Chapter 9. Global Satellite Internet Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

9.1 SpaceX (Starlink)

9.2 OneWeb

9.3 Amazon (Project Kuiper)

9.4 Telesat

9.5 Viasat

9.6 Hughes Network Systems

9.7 Eutelsat

9.8 SES S.A.

9.9 Iridium Communications

9.10 Inmarsat

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The Global Satellite Internet Market was valued at USD 10.4 billion in 2024 and is projected to reach a market size of USD 22.51 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 16.7%.

Rising demand for rural connectivity and advancements in low Earth orbit satellites.

Based on Frequency band, the Global Satellite Internet Market is segmented into L-band, C-band, K-band, X-band.

North America is the most dominant region for the Global Satellite Internet Market.

SpaceX, OneWeb, Amazon, etc. are the leading players in the Global Satellite Internet Market.