5G Technology Market Research Report -- Segmentation by Component (Hardware, Software, Services); By Frequency Band (Sub-6 GHz, MMWave, C-Band); By Application (Enhanced Mobile Broadband, Massive IoT, Ultra-Reliable Low Latency Communications); By End-User (Consumer, Enterprise, Industrial, Public Safety); By Deployment (Standalone, Non-Standalone); Region - Forecast (2025 - 2030)

Published: 2025 - June

Report Code: IM-16473

Format:

Region: Global

Market Size and Overview:

The 5G Technology Market was valued at USD 163.78 billion in 2024 and is projected to reach a market size of USD 831.65 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 38.4%.

5G Technology represents the fifth generation of wireless communication technology that promises to revolutionize connectivity through ultra-high-speed data transmission, ultra-low latency, and massive device connectivity capabilities. This transformative technology has emerged as a cornerstone of digital infrastructure in the 21st century, enabling innovations across industries including autonomous vehicles, smart cities, industrial automation, and immersive entertainment experiences. With the continuous expansion of 5G networks globally, the demand for high-performance wireless connectivity is experiencing unprecedented growth and is anticipated to create substantial opportunities across telecommunications, manufacturing, healthcare, and entertainment sectors over the next decade.

Key Market Insights:

According to the Global System for Mobile Communications Association (GSMA), there were approximately 1.05 billion 5G connections worldwide by the end of 2022, representing a 76% increase from the previous year. Industry projections indicate that 5G connections will reach 5.6 billion globally by 2030, with Asia-Pacific accounting for approximately 60% of these connections. This rapid adoption demonstrates the compelling value proposition of 5G technology across diverse market segments and geographical regions.

Research conducted by Ericsson reveals that 5G networks can deliver peak data speeds up to 100 times faster than 4G LTE, with average download speeds ranging from 1.4 to 14.2 Gbps depending on deployment configuration and spectrum allocation. Additionally, 5G technology achieves latency as low as 1 millisecond compared to 4G's typical 20-30 milliseconds, enabling real-time applications that were previously technically unfeasible with earlier wireless generations.

A comprehensive survey of 2,500 enterprise decision-makers conducted by Deloitte in 2022 found that 67% of organizations plan to implement 5G solutions within the next two years, with manufacturing (78%), healthcare (72%), and transportation (69%) sectors showing the highest adoption intentions. The same study revealed that early 5G adopters reported average productivity improvements of 28% and operational cost reductions of 22% within the first year of deployment.

5G Technology Market Drivers:

The exponential growth in data consumption and the increasing demand for ultra-low latency applications are fundamentally driving the global adoption of 5G technology across consumer and enterprise segments.

The proliferation of data-intensive applications including high-definition video streaming, augmented reality, virtual reality, and cloud gaming has created unprecedented demands on wireless network capacity and performance that legacy technologies cannot adequately address. According to Cisco's Visual Networking Index, global mobile data traffic is projected to increase sevenfold between 2021 and 2026, with video content accounting for approximately 77% of total mobile data consumption by 2026. This explosive growth in data consumption requires the enhanced capacity, speed, and efficiency that 5G networks provide through advanced technologies such as massive MIMO, beamforming, and network slicing. The emergence of latency-sensitive applications including autonomous vehicles, industrial automation, remote surgery, and real-time gaming has created critical requirements for network response times that 4G technology cannot meet. For instance, autonomous vehicle operations require network latency of less than 5 milliseconds to ensure safe real-time decision-making, while remote surgical procedures demand sub-millisecond latency for precise instrument control. 5G's ultra-reliable low-latency communication capabilities enable these transformative use cases by providing consistent network performance with guaranteed quality of service parameters.

The increasing digitization of industrial processes and the growing investment in smart city infrastructure are propelling significant demand for 5G technology solutions across multiple vertical markets.

Industrial organizations are implementing comprehensive digital transformation initiatives that require wireless connectivity solutions capable of supporting mission-critical applications with guaranteed reliability and performance characteristics. Manufacturing facilities are deploying 5G-enabled industrial IoT systems for predictive maintenance, quality control, and automated production processes that can improve operational efficiency by up to 35% according to recent industry studies. The technology's ability to support network slicing enables organizations to create dedicated virtual networks with customized performance parameters for different applications, ensuring that critical systems receive prioritized network resources without interference from less critical traffic. Smart city initiatives worldwide are increasingly relying on 5G connectivity to enable integrated urban systems including intelligent transportation, public safety communications, environmental monitoring, and energy management applications.

5G Technology Market Restraints and Challenges:

Despite its transformative potential, the 5G technology market faces significant challenges that could impact its growth trajectory. The substantial infrastructure investment required for comprehensive 5G network deployment represents a major barrier, with industry estimates suggesting that global 5G infrastructure costs will exceed $1.3 trillion through 2030. Spectrum availability and regulatory complexities vary significantly across different countries and regions, creating deployment delays and increasing operational complexity for network operators. Technical challenges persist in achieving reliable millimetre-wave coverage, particularly for indoor environments and dense urban areas where signal propagation limitations require extensive small cell deployments. Security concerns related to network architecture changes and increased attack surfaces have created regulatory scrutiny and implementation delays in some markets. Additionally, the limited availability of 5G-compatible devices in certain price segments has slowed consumer adoption rates, while enterprise customers often require extensive customization and integration services that extend deployment timelines.

5G Technology Market Opportunities:

The 5G technology market presents substantial growth opportunities across multiple dimensions as organizations and governments recognize its transformative potential for economic development and technological advancement. Edge computing integration with 5G networks creates opportunities for ultra-low latency applications including autonomous systems, real-time analytics, and immersive experiences that can generate new revenue streams for service providers and technology vendors. Private 5G networks represent a particularly promising market segment, with enterprises increasingly investing in dedicated wireless infrastructure to support specialized industrial applications, campus connectivity, and critical communications requirements. The healthcare sector offers significant opportunities for 5G-enabled telemedicine, remote patient monitoring, and medical device connectivity applications that can improve patient outcomes while reducing healthcare delivery costs. Smart manufacturing applications including predictive maintenance, quality assurance, and supply chain optimization present substantial market potential as industrial organizations seek to improve operational efficiency and competitiveness.

Market Segmentation: By Component

• Hardware

• Software

• Services

In 2024, the hardware segment dominated the global 5G technology market with approximately 58.7% revenue share. This dominance is attributed to the massive infrastructure investments required for 5G network deployment, including base stations, antennas, radio equipment, and core network hardware. The hardware segment encompasses both network infrastructure equipment and end-user devices, with infrastructure representing the larger portion due to the capital-intensive nature of nationwide 5G rollouts by mobile network operators.

The services segment is projected to grow at the fastest CAGR of approximately 41.2% during the forecast period. This accelerated growth is driven by increasing demand for professional services including network planning, deployment, integration, and managed services as organizations seek specialized expertise to implement complex 5G solutions. Additionally, the emergence of new 5G-enabled service offerings such as network slicing, edge computing, and IoT connectivity services is creating new revenue opportunities for telecommunications providers and system integrators.

Market Segmentation: By Frequency Band

• Sub-6 GHz

• MMWave (Millimeter Wave)

• C-Band

The Sub-6 GHz segment accounted for the largest market share of approximately 64.3% in 2024, owing to its superior coverage characteristics and ability to penetrate buildings and obstacles more effectively than higher frequency bands. This frequency range provides the optimal balance between coverage area and data capacity, making it ideal for widespread consumer mobile services and initial 5G network deployments in urban and suburban areas.

The C-Band segment is expected to witness the highest growth rate during the forecast period, with a CAGR of approximately 43.6%. This growth is driven by recent spectrum auctions in major markets including the United States, where operators invested heavily in C-Band licenses to enhance their 5G network capacity and coverage. C-Band offers mid-band spectrum that provides better coverage than millimeter wave while delivering higher capacity than traditional sub-6 GHz frequencies, making it particularly valuable for dense urban deployments.

Market Segmentation: By Application

• Enhanced Mobile Broadband (eMBB)

• Massive IoT (mIoT)

• Ultra-Reliable Low Latency Communications (URLLC)

Enhanced Mobile Broadband emerged as the largest application segment in 2024, representing 52.4% of the market share. This segment focuses on delivering significantly improved data speeds, capacity, and user experiences for consumer mobile services including video streaming, social media, and mobile internet access. eMBB applications have driven initial 5G adoption as they provide immediate, tangible benefits to consumers and represent natural evolution from existing 4G services.

The Ultra-Reliable Low Latency Communications segment is projected to grow at the fastest CAGR of 44.8% during the forecast period. This growth is driven by emerging applications in autonomous vehicles, industrial automation, remote surgery, and critical infrastructure that require guaranteed network performance with minimal latency. URLLC applications represent the most transformative potential of 5G technology by enabling entirely new use cases that were technically impossible with previous wireless generations.

Market Segmentation: By End-User

• Consumer

• Enterprise

• Industrial

• Public Safety

The consumer segment dominated the 5G technology market in 2024 with a 43.9% share, driven by widespread adoption of 5G smartphones and mobile services across major markets. Consumer applications primarily focus on enhanced mobile broadband services that provide faster download speeds, improved video streaming quality, and better network performance in congested areas. This segment has benefited from aggressive marketing campaigns by mobile network operators and device manufacturers promoting 5G capabilities.

The industrial segment is anticipated to register the fastest growth rate during the forecast period, with a CAGR of 46.2%. This growth is driven by increasing adoption of 5G technology for manufacturing automation, predictive maintenance, supply chain optimization, and quality control applications. Industrial organizations are recognizing 5G's potential to enable new operational capabilities including real-time monitoring, automated decision-making, and seamless integration of operational technology with information technology systems.

Market Segmentation: By Deployment

• Standalone (SA)

• Non-Standalone (NSA)

Non-Standalone deployments accounted for approximately 71.6% of the market share in 2025, as this approach allows operators to leverage existing 4G core network infrastructure while adding 5G radio access capabilities. NSA deployments provide a cost-effective path to 5G service introduction and enable operators to generate revenue from 5G services while gradually transitioning to full standalone architectures over time.

The Standalone segment is projected to grow at a higher CAGR of 42.7% during the forecast period as operators complete their network evolution toward full 5G architectures that can support advanced capabilities including network slicing, ultra-low latency applications, and massive IoT connectivity. SA deployments unlock the complete potential of 5G technology by providing dedicated 5G core networks optimized for next-generation applications and services.

Market Segmentation: Regional Analysis

• North America

• Asia-Pacific

• Europe

• South America

• Middle East and Africa

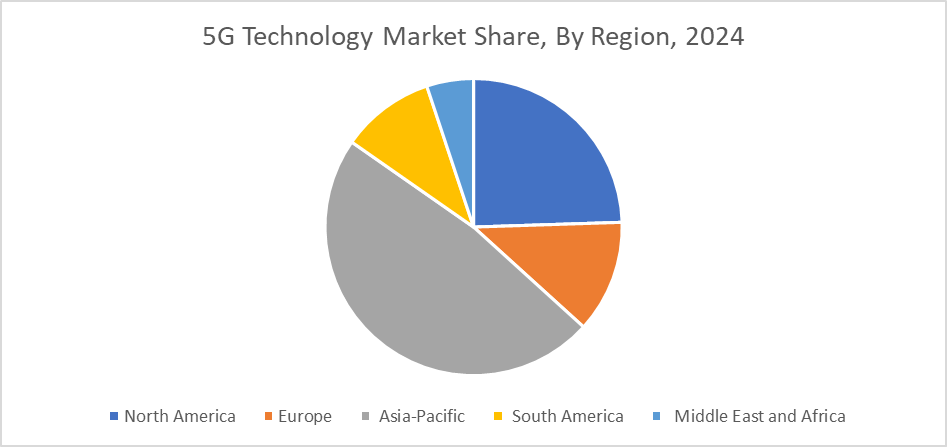

Asia-Pacific led the global 5G technology market in 2024, accounting for 47.2% of the total market share. This dominance is attributed to early and aggressive 5G deployments in countries including China, South Korea, and Japan, along with substantial government investments in 5G infrastructure development. China alone represents approximately 60% of global 5G connections and continues to lead in 5G infrastructure deployment and technology development.

North America is expected to witness significant growth during the forecast period, with a CAGR of 39.8%. The region's growth is driven by substantial investments in 5G infrastructure by major carriers, extensive C-Band spectrum deployments, and strong enterprise adoption of private 5G networks. The United States has seen accelerated 5G deployment following major spectrum auctions, while Canada is implementing nationwide 5G coverage expansion programs to support both consumer and enterprise applications.

COVID-19 Impact Analysis on the Global 5G Technology Market:

The COVID-19 pandemic initially created disruptions in 5G infrastructure deployment due to supply chain constraints, workforce limitations, and delayed spectrum auctions in some regions. However, the crisis ultimately accelerated 5G adoption by highlighting the critical importance of robust digital connectivity for remote work, distance learning, telemedicine, and digital commerce applications. Network traffic increases of 20-40% during pandemic lockdowns demonstrated the limitations of existing 4G infrastructure and created urgency for 5G capacity upgrades.

Government economic stimulus programs in several countries specifically targeted 5G infrastructure development as a key component of post-pandemic economic recovery strategies. The pandemic also accelerated enterprise interest in private 5G networks as organizations sought to reduce dependence on public connectivity and ensure reliable wireless communications for critical business operations. Healthcare applications of 5G technology gained particular prominence during the pandemic, with telemedicine consultations increasing by over 3000% in some regions and creating sustained demand for high-performance wireless connectivity solutions. These pandemic-driven changes in connectivity requirements and usage patterns are expected to sustain elevated demand for 5G technology well beyond the immediate crisis period.

Latest Trends/ Developments:

Open RAN (Radio Access Network) architecture adoption is gaining significant momentum as operators seek to reduce vendor dependence and increase network flexibility through disaggregated, standards-based infrastructure components. This trend is creating new opportunities for software-focused vendors and enabling more competitive supplier ecosystems, with major operators including Dish Network, Rakuten, and Deutsche Telekom implementing large-scale Open RAN deployments.

Private 5G networks are experiencing rapid growth as enterprises recognize the benefits of dedicated wireless infrastructure for mission-critical applications, with deployments expanding beyond traditional industrial use cases to include healthcare facilities, educational institutions, and large commercial complexes. Market research indicates that private 5G network revenues will reach $5.7 billion by 2027, driven primarily by manufacturing and logistics sector implementations.

Key Players:

• Huawei Technologies Co., Ltd.

• Ericsson AB

• Nokia Corporation

• Samsung Electronics Co., Ltd.

• Qualcomm Incorporated

• ZTE Corporation

• Cisco Systems, Inc.

• Intel Corporation

• Verizon Communications Inc.

• AT&T Inc.

Chapter 1. 5G Technology Market –Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. 5G Technology Market – Executive Summary

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis

Chapter 3. 5G Technology Market – Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. 5G Technology Market Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes

Chapter 5. 5G Technology Market - Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. 5G Technology Market – By Component

6.1. Introduction/Key Finding

6.2. Hardware

6.3. Software

6.4. Services

6.5. Y-O-Y Growth trend Analysis By Component

6.6. Absolute $ Opportunity Analysis By Component, 2025-2030

Chapter 7. 5G Technology Market – By Frequency Band

7.1. Introduction/Key Findings

7.2. Sub 6Hz

7.3. MMWave

7.4. C-Band

7.5. Y-O-Y Growth trend Analysis By Frequency Band

7.6. Absolute $ Opportunity Analysis By Frequency Band, 2025-2030

Chapter 8. 5G Technology Market – By Application

8.1. Introduction/Key Findings

8.2. Enhanced Mobile Broadband

8.3. Massive IoT

8.4. Ultra Reliable Low Latency Communication

8.5. Y-O-Y Growth trend Analysis By Application

8.6. Absolute $ Opportunity Analysis By Application, 2025-2030

Chapter 9. 5G Technology Market – By End User

9.1. Introduction/ Key Findings

9.2. Consumer

9.3. Enterprise

9.4. Industrial

9.5. Public Safety

9.6. Y-O-Y Growth trend Analysis By End User

9.7. Absolute $ Opportunity Analysis By End User, 2025-2030

Chapter 10. 5G Technology Market – By Deployment

10.1. Introduction/ Key Findings

10.2. Standalone

10.3. Non-Standalone

10.4. Y-O-Y Growth trend Analysis By Deployment

10.5. Absolute $ Opportunity Analysis By Deployment, 2025-2030

Chapter 11. 5G Technology Market, By Geography – Market Size, Forecast, Trends & Insights

11.1. North America

11.1.1. By Country

11.1.1.1. U.S.A.

11.1.1.2. Canada

11.1.1.3. Mexico

11.1.2. By Component

11.1.3. By Frequency Band

11.1.4. By Application

11.2.5. By End User

11.2.6. By Deployment

11.1.7. Countries & Segments – Market Attractiveness Analysis

11.2. Europe

11.2.1. By Country

11.2.1.1. U.K.

11.2.1.2. Germany

11.2.1.3. France

11.2.1.4. Italy

11.2.1.5. Spain

11.2.1.6. Rest of Europe

11.2.2. By Component

11.2.3. By Frequency Band

11.2.4. By Application

11.2.5. By End User

11.2.6. By Deployment

11.2.7. Countries & Segments – Market Attractiveness Analysis

11.3. Asia Pacific

11.3.1. By Country

11.3.1.1. China

11.3.1.2. Japan

11.3.1.3. South Korea

11.3.1.4. India

11.3.1.5. Australia & New Zealand

11.3.1.6. Rest of Asia-Pacific

11.3.2. By Component

11.3.3. By Frequency Band

11.3.4. By Application

11.3.5. By End User

11.3.6. By Deployment

11.3.7. Countries & Segments – Market Attractiveness Analysis

11.4. South America

11.4.1. By Country

11.4.1.1. Brazil

11.4.1.2. Argentina

11.4.1.3. Colombia

11.4.1.4. Chile

11.4.1.5. Rest of South America

11.4.2. By Component

11.4.3. By Frequency Band

11.4.4. By Application

11.4.5. By End User

11.4.6. By Deployment

11.4.7. Countries & Segments – Market Attractiveness Analysis

11.5. Middle East & Africa

11.5.1. By Country

11.5.1.1. United Arab Emirates (UAE)

11.5.1.2. Saudi Arabia

11.5.1.3. Qatar

11.5.1.4. Israel

11.5.1.5. South Africa

11.5.1.6. Nigeria

11.5.1.7. Kenya

11.5.1.8. Egypt

11.5.1.9. Rest of MEA

11.5.2. By Component

11.5.3. By Frequency Band

11.5.4. By Application

11.5.5. By End User

11.5.6. By Deployment

11.5.7. Countries & Segments – Market Attractiveness Analysis

Chapter 12. 5G Technology Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments, SWOT Analysis)

12.1. Huawei Technologies Co., Ltd.

12.2. Ericsson AB

12.3. Nokia Corporation

12.4. Samsung Electronics Co., Ltd.

12.5. Qualcomm Incorporated

12.6. ZTE Corporation

12.7. Cisco Systems, Inc.

12.8. Intel Corporation

12.9. Verizon Communications Inc.

12.10. AT&T Inc.

Download Sample

Choose License Type

2850

5250

4500

1800

Frequently Asked Questions

The 5G Technology Market was valued at USD 163.78 billion in 2024 and is projected to reach a market size of USD 831.65 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 38.4%.

The exponential growth in data consumption and the increasing demand for ultra-low latency applications are the primary drivers propelling the global 5G technology market.

Based on Component, the Global 5G Technology Market is segmented into Hardware, Software, and Services.

Asia-Pacific is the most dominant region for the Global 5G Technology Market.

Huawei Technologies Co., Ltd., Ericsson AB, Nokia Corporation, and Samsung Electronics Co., Ltd. are the key players operating in the Global 5G Technology Market.